Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

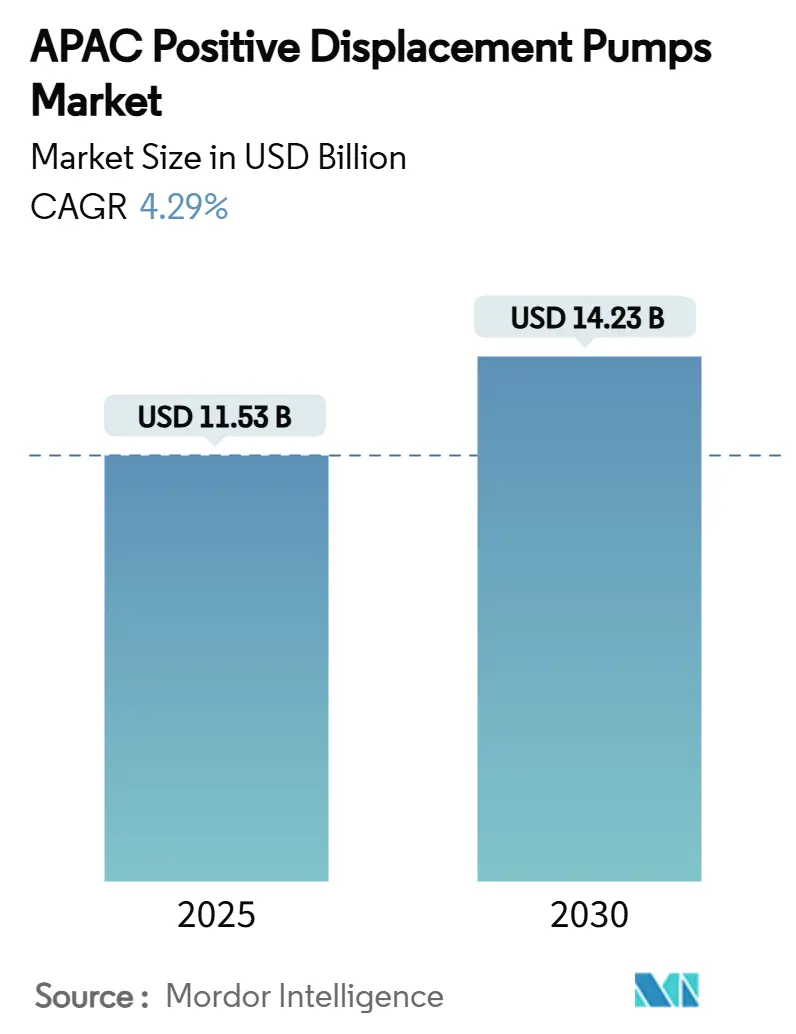

| Market Size (2025) | USD 11.53 Billion |

| Market Size (2030) | USD 14.23 Billion |

| Growth Rate (2025 - 2030) | 4.29% CAGR |

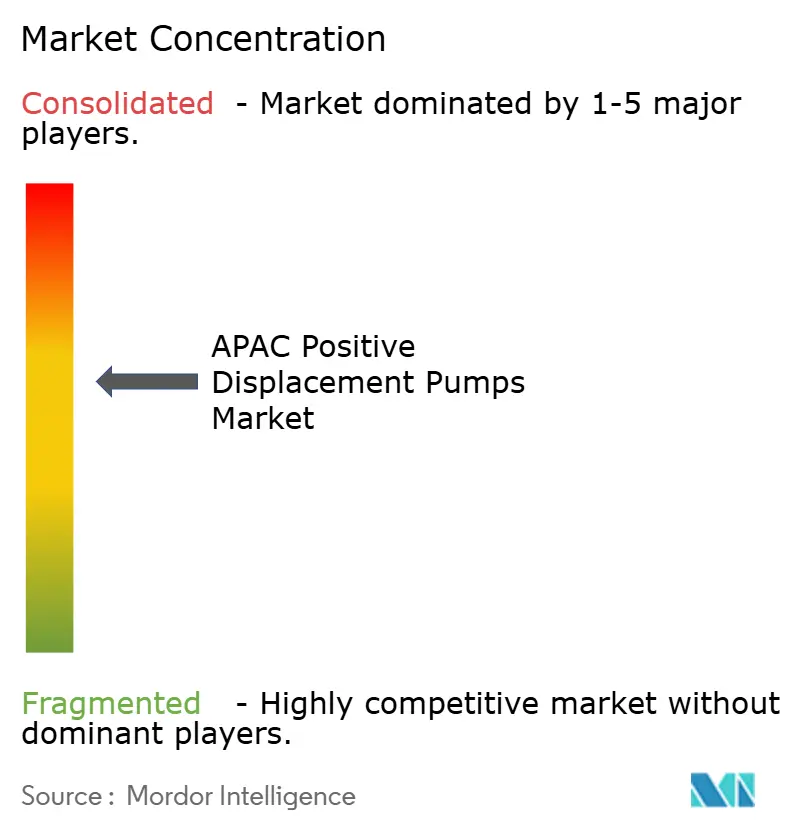

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Positive Displacement Pumps Market Analysis by Mordor Intelligence

The APAC positive displacement pumps market size is estimated at USD 11.53 billion in 2025 and is forecast to reach USD 14.23 billion by 2030, reflecting a 4.29 % CAGR over the period. The measured expansion of the APAC positive displacement pumps market is grounded in a structural pivot toward digitized, environmentally compliant industrial ecosystems that favor low-emission and smart-sensor technologies.[1]International Energy Agency, “Southeast Asia Energy Outlook 2024,” iea.org Demand intensifies as municipalities across China, India and Southeast Asia accelerate wastewater infrastructure programs, while chemical processors in Jiangsu, Shandong and Guangdong provinces adopt seal-less configurations to comply with volatile organic compound (VOC) limits. Offshore electrification projects in Australia, Malaysia and Indonesia further reinforce the APAC positive displacement pumps market, because low-shear rotary and twin-screw designs minimize emulsion damage during multiphase hydrocarbon handling. Meanwhile, India’s Bureau of Indian Standards (BIS) modernization and expanding pharmaceutical capacity underpin the fastest national growth rate, embedding stringent certification into procurement cycles. Cost inflation in stainless steel and copper, coupled with a scarcity of skilled maintenance labor for progressive cavity systems, tempers growth but also accelerates adoption of predictive-maintenance solutions.

Key Report Takeaways

- By pump type, rotary units led with 51.4% revenue share in 2024; peristaltic systems are projected to expand at a 7.15% CAGR through 2030.

- By driving method, electric-motor systems held 63.8% of the APAC positive displacement pumps market share in 2024, while solar-powered models record the highest projected CAGR at 9.56% through 2030.

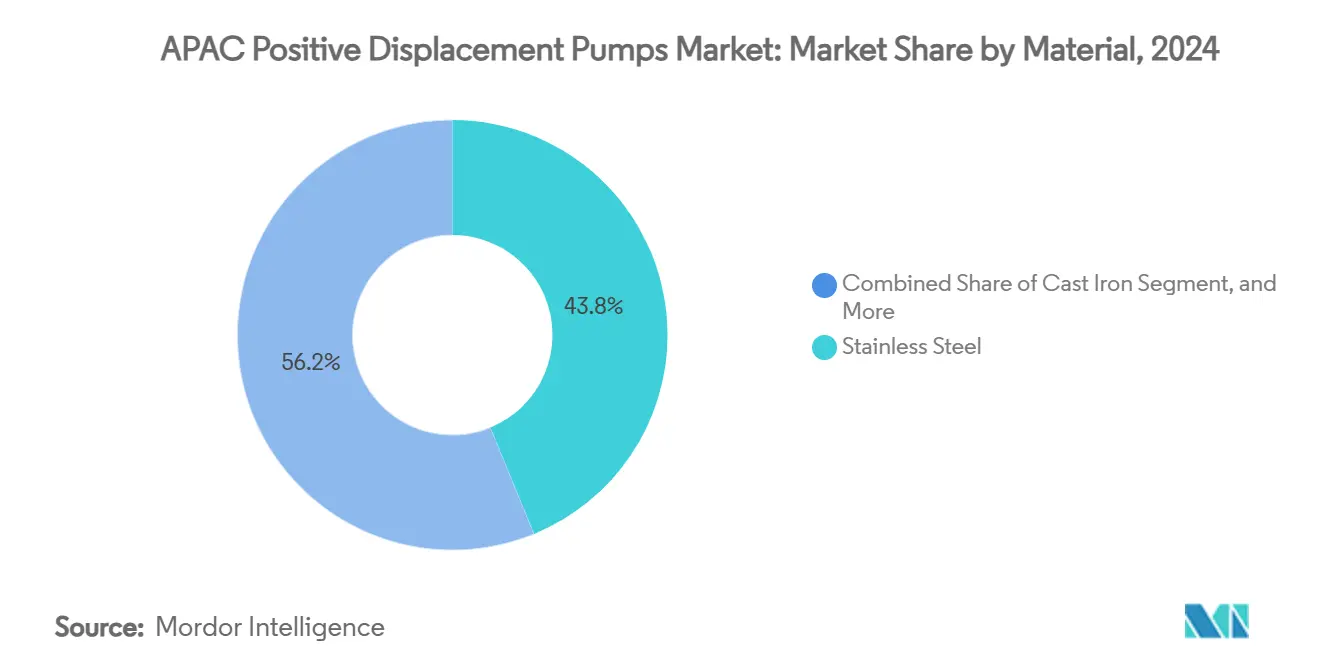

- By material, stainless steel commanded 43.8% of the APAC positive displacement pumps market size in 2024; duplex and exotic alloys are set to grow at a 6.43% CAGR between 2025-2030.

- By end-user industry, oil and gas accounted for 29.1% of demand in 2024, whereas pharmaceutical and biotech applications advance at an 8.76% CAGR to 2030.

- By geography, China held 42.9% of 2024 revenue; India is forecast to lead growth with a 6.24% CAGR through 2030.

Asia-Pacific Positive Displacement Pumps Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid build-out of Asia’s municipal wastewater infrastructure | +0.8% | China, India, Southeast Asia core markets | Medium term (2-4 years) |

| Tightening VOC discharge limits in China’s specialty-chemicals clusters | +0.6% | China primary, spillover to Vietnam, Thailand | Short term (≤ 2 years) |

| Electrification of offshore platforms raises demand for low-shear pumps | +0.4% | Australia, Malaysia, Indonesia offshore regions | Long term (≥ 4 years) |

| Mini-bulk biopharma facilities adopting single-use peristaltic skids | +0.7% | India, Singapore, South Korea biotech hubs | Medium term (2-4 years) |

| OEM shift to smart sensor-enabled rotary pumps | +0.5% | Japan, South Korea, advanced APAC markets | Medium term (2-4 years) |

| Capex rebound in F&B processing lines | +0.4% | Regional, concentrated in Thailand, Vietnam | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Build-out of Asia’s Municipal Wastewater Infrastructure

Expanding municipal wastewater networks spur recurring orders for progressive cavity and screw units that handle viscous sludges with stable flow, making these pumps a preferred choice for biological treatment and chemical dosing.[2]NETZSCH Pumps & Systems, “What You Need to Know about Progressing Cavity Pumps,” pumps-systems.netzsch.com China and India allocate significant stimulus to decentralized plants, and Southeast Asian nations seek modular skid packages that can be deployed quickly in peri-urban areas. Progressive cavity suppliers therefore bundle monitoring sensors to flag wear on rotors and stators, reducing on-site service calls. Local fabricators in Indonesia and Vietnam also scale up cast iron models for budget-sensitive municipalities, but stainless variants continue to dominate lifecycle assessments. The APAC positive displacement pumps market benefits as water utilities anchor long-term service agreements that guarantee throughput performance across 10-year concessions.

Tightening VOC Discharge Limits in China’s Specialty-Chemicals Clusters

Stringent rules mandating leak detection thresholds below 2,000 ppm push processors to specify magnetic-drive and hermetically sealed designs, creating a material premium yet reducing fugitive emissions liability. Pump makers integrate dual mechanical seals with sensor-enabled pressure compensation to ensure regulatory audits pass on first inspection. Compliance deadlines intensify replacement cycles in Jiangsu, Shandong and Guangdong complexes, positioning the APAC positive displacement pumps market for retrofit revenue. Companies offering VOC-monitoring analytics secure framework agreements with specialty polymer producers that require real-time reporting to local environmental bureaus.

Electrification of Offshore Platforms Raises Demand for Low-Shear Pumps

Hybrid renewable power systems on floating production units mandate equipment that operates reliably under variable frequency drives and fluctuating torque. Progressive cavity and twin-screw pumps exhibit stable performance at partial speeds, reducing shear and preserving fluid integrity.[3]Asia-Pacific Economic Cooperation, “APEC Energy Overview 2024,” aperc.or.jp Australian operators pioneer digital twins that simulate pump behavior under grid-connected and battery-only modes, informing predictive replacement schedules. Vendors deliver corrosion-resistant duplex alloys to withstand seawater ingress and sour gas exposure. This long-term trend drives higher service-based revenue streams within the APAC positive displacement pumps market as remote monitoring contracts extend beyond typical OEM warranties.

Mini-Bulk Biopharma Facilities Adopting Single-Use Peristaltic Skids

India, Singapore and South Korea expand biologics capacity using modular, single-use equipment; peristaltic units eliminate cross-contamination and support quick batch changeovers. Tube material innovation—advanced silicone and fluoropolymers—extends sterility cycles and enhances chemical compatibility. Suppliers preload sensors that record cumulative tube flex, enabling pharmaceutical quality teams to forecast tubing replacement proactively. Cleanroom-packaged units ship pre-validated, shortening facility commissioning timelines and escalating peristaltic market penetration across the APAC positive displacement pumps market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile stainless-steel and copper prices inflate pump BOM cost | -0.7% | Regional, particularly affecting China, India manufacturing | Short term (≤ 2 years) |

| Skilled-labor shortage for complex progressive-cavity pump MRO | -0.5% | Japan, South Korea, Australia developed markets | Long term (≥ 4 years) |

| Rising preference for seal-less mag-drive centrifugals in pharma | -0.4% | India, Singapore, South Korea pharmaceutical hubs | Medium term (2-4 years) |

| Lengthy BIS certification cycle delays India roll-outs | -0.3% | India primary, spillover to regulatory-sensitive markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Stainless-Steel and Copper Prices Inflate Pump BOM Cost

Raw materials account for up to 60% of finished-pump cost; a 15% spike in stainless price can cut gross margins by 300 bps if not passed through swiftly. Suppliers diversify into duplex or low-molybdenum grades and redesign housings to reduce wall thickness without compromising pressure ratings. Larger OEMs lock annual contracts with mills, while smaller fabricators risk cash-flow tightness, prompting consolidation within the APAC positive displacement pumps market. Design-for-cost engineering accelerates the transition to composite polymer components in non-critical housings, easing volatility exposure.

Skilled-Labor Shortage for Complex Progressive-Cavity Pump MRO

Rotor-stator alignment and elastomer selection require specialized technicians; retirements in Japan and Australia shrink the talent pool. OEMs respond by embedding augmented-reality service guides and offering remote commissioning support. End-users with limited in-house expertise opt for contract maintenance, transferring capex to opex and marginally lowering lifetime cost comparisons against centrifugal alternatives. The constraint slows adoption of progressive cavity units in new greenfield projects but accelerates digital service adoption inside the APAC positive displacement pumps market.

Segment Analysis

By Pump Type: Rotary Dominance Faces Peristaltic Disruption

Rotary units contributed 51.4% of 2024 revenue, equating to the largest slice of the APAC positive displacement pumps market size and validating their versatility in chemicals, oil and gas and food handling applications. Peristaltic pumps, however, lead volume growth at a 7.15% CAGR by satisfying single-use bioprocessing protocols and chemical-feed duties where zero contamination is non-negotiable.

Gear and twin-screw products now ship with vibration and pressure sensors that feed OEM cloud dashboards, accelerating predictive-maintenance uptake across the APAC positive displacement pumps market. Lobe designs ride demand from dairy and beverage expansions, while vane variants maintain niche roles in lubrication circuits.

By Driving Method: Electric Motors Lead Solar Surge

Electric-motor models delivered 63.8% of 2024 revenue, underscoring their entrenched role in factory automation and conveying applications across the APAC positive displacement pumps market share. Solar-powered packages, though still a niche, achieve a 9.56% CAGR as agricultural irrigation and remote water supply projects benefit from declining photovoltaic costs.

Variable-frequency drives paired with high-efficiency IE4 motors cut lifecycle energy use, while diesel units retreat to emergency and off-grid roles under tightening emission norms. Pneumatic systems retain a foothold in hazardous environments where intrinsic safety trumps energy efficiency.

By Material: Stainless Steel Dominance Challenged by Exotic Alloys

Stainless steel versions represented 43.8% of 2024 sales, underscoring their balanced cost-to-performance ratio in the APAC positive displacement pumps market. Duplex and other exotic alloys grow at 6.43% CAGR by providing superior chloride stress-crack resistance demanded by offshore and specialty-chemical clients.

OEMs invest in alloy development that reduces nickel use, bolstering cost certainty while meeting mechanical thresholds. Composite housings emerge in metering applications, though brittleness concerns restrict broader uptake.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-user Industry: Oil and Gas Leadership Faces Pharma Growth

Oil and gas secured 29.1% of 2024 demand, reflecting upstream multiphase transfer and downstream additive injection operations. Pharmaceutical and biotech entities expand spend at 8.76% CAGR as continuous processing and single-use formats proliferate across the APAC positive displacement pumps market size.

Chemical producers drive specification of low-emission sealed units, while food & beverage processors emphasize CIP compliance and gentle handling to limit shear-induced product degradation.

Geography Analysis

China retained 42.9% revenue in 2024, reinforcing its scale advantage and influencing design standards that increasingly incorporate environmental compliance—especially for VOC control in specialty chemicals. Local manufacturers co-develop magnetic-drive models with European licensors, elevating quality perceptions and supporting export ambitions.

India posts the highest national CAGR at 6.24% through 2030 as BIS reforms shorten certification timelines and encourage multinational investment in local production. Pharmaceutical plant expansions in Hyderabad and Gujarat dominate peristaltic and diaphragm tenders, while smart-city wastewater schemes adopt progressive cavity packages with IoT enablement.

Japan, South Korea and Australia supply stable replacement demand, governed by stringent energy-efficiency rules and aging asset renewals. Australian mines specify abrasion-resistant twin-screw models and demand remote diagnostics given their isolated locales. South Korean semiconductor fabs procure sanitary gear units to support ultra-pure chemical feeds, influencing technology roadmaps for the broader APAC positive displacement pumps market.

Competitive Landscape

The APAC positive displacement pumps market remains moderately fragmented: the top five suppliers control an estimated 48% of regional turnover, leaving ample share for specialized and domestic challengers. Atlas Copco, Grundfos and Flowserve sustain scale advantages through broad portfolios and integrated service networks, while NETZSCH and Sulzer differentiate on progressive cavity and multi-phase expertise.

Digitalization shapes go-to-market tactics; Grundfos monetizes cloud-based energy-optimization analytics, and Flowserve bundles asset-performance management software with new installations. Global leaders emphasize sustainability messaging, leveraging lower total-cost-of-ownership to counter regional price competition.

Regional firms such as Roto Pumps and Wangen advance by filling application niches—abrasive slurries, biogas digesters—and leveraging proximity advantages to expedite delivery and customization. Strategic collaborations with sensor and automation vendors speed digital retrofits, ensuring feature parity with global incumbents.

Asia-Pacific Positive Displacement Pumps Industry Leaders

-

The Weir Group PLC

-

Atlas Copco AB

-

KSB SE and Co. KGaA

-

NETZSCH Holding GmbH

-

Pentair plc

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2025: Atlas Copco closed the acquisition of Pumpenfabrik Wangen GmbH, adding EUR 46.4 million (USD 50.3 million) in progressive cavity revenue and positioning the group to capture biogas and sludge applications.

- January 2025: Graco disclosed a 14% decline in APAC net sales for Q4 2024 as currency headwinds dampened demand.

- September 2024: Grundfos completed the acquisition of Culligan’s commercial & industrial water-treatment businesses in Italy, France and UK, bolstering process-water expertise transferable to Asian breweries and electronics fabs.

- April 2024: Sulzer inaugurated new production lines in Easley, South Carolina, to manufacture submersible sewage and grinder pumps, freeing capacity in China for high-mix, low-volume specialty units aimed at APAC chemical customers.

Asia-Pacific Positive Displacement Pumps Market Report Scope

The market study analyses the market trends and opportunities for different types of positive displacement pumps, such as Diaphragm, Piston, Gear, Lobe, Progressive Cavity, Screw, Vane, and Peristaltic others that are used in the various end-user industry application. These pumps find applications in process, and manufacturing industries, among others. Further, the study analyzes the impact of COVID-19 on the market players and its stakeholders across the supply chain.

By Pump Type

| Reciprocating Pumps | Piston |

| Diaphragm | |

| Rotary Pumps | Gear |

| Lobe | |

| Screw | |

| Vane | |

| Progressive Cavity | |

| Peristaltic |

By Driving Method

| Electric Motor |

| Diesel/IC Engine |

| Pneumatic |

| Hydraulic |

| Solar |

By Material

| Cast Iron |

| Stainless Steel |

| Other Materials |

By End-user Industry

| Oil and Gas |

| Chemicals |

| Food and Beverage |

| Waste and Wastewater |

| Pharmaceutical and Biotech |

| Power Generation |

| Pulp and Paper |

| Mining and Metals |

| Other Industries |

By Country

| China |

| Japan |

| India |

| South Korea |

| Australia and New Zealand |

| Rest of Asia-Pacific |

| By Pump Type | Reciprocating Pumps | Piston |

| Diaphragm | ||

| Rotary Pumps | Gear | |

| Lobe | ||

| Screw | ||

| Vane | ||

| Progressive Cavity | ||

| Peristaltic | ||

| By Driving Method | Electric Motor | |

| Diesel/IC Engine | ||

| Pneumatic | ||

| Hydraulic | ||

| Solar | ||

| By Material | Cast Iron | |

| Stainless Steel | ||

| Other Materials | ||

| By End-user Industry | Oil and Gas | |

| Chemicals | ||

| Food and Beverage | ||

| Waste and Wastewater | ||

| Pharmaceutical and Biotech | ||

| Power Generation | ||

| Pulp and Paper | ||

| Mining and Metals | ||

| Other Industries | ||

| By Country | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the APAC positive displacement pumps market?

The market is valued at USD 11.53 billion in 2025 and is forecast to reach USD 14.23 billion by 2030 at a 4.29% CAGR.

Which pump type leads the APAC positive displacement pumps market?

Rotary pumps hold the largest share at 51.4% of 2024 revenue, while peristaltic pumps grow fastest at 7.15% CAGR.

Why is India the fastest-growing country market?

Modernization of BIS certification, expanding pharmaceutical capacity and infrastructure projects deliver a 6.24% CAGR through 2030.

How are VOC regulations affecting pump procurement in China?

Stricter leak-detection thresholds accelerate adoption of magnetic-drive and hermetically sealed designs in specialty-chemical clusters.

Which material segment is expected to grow fastest?

Duplex and exotic alloys expand at 6.43% CAGR due to superior corrosion resistance demanded in offshore and chemical environments.

What strategic themes dominate recent industry developments?

Acquisitions that reinforce niche technologies, localization to shorten lead times, and digitalization for predictive maintenance are primary themes.

Page last updated on: