Market Size of Asia Pacific Plastic Packaging Film Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

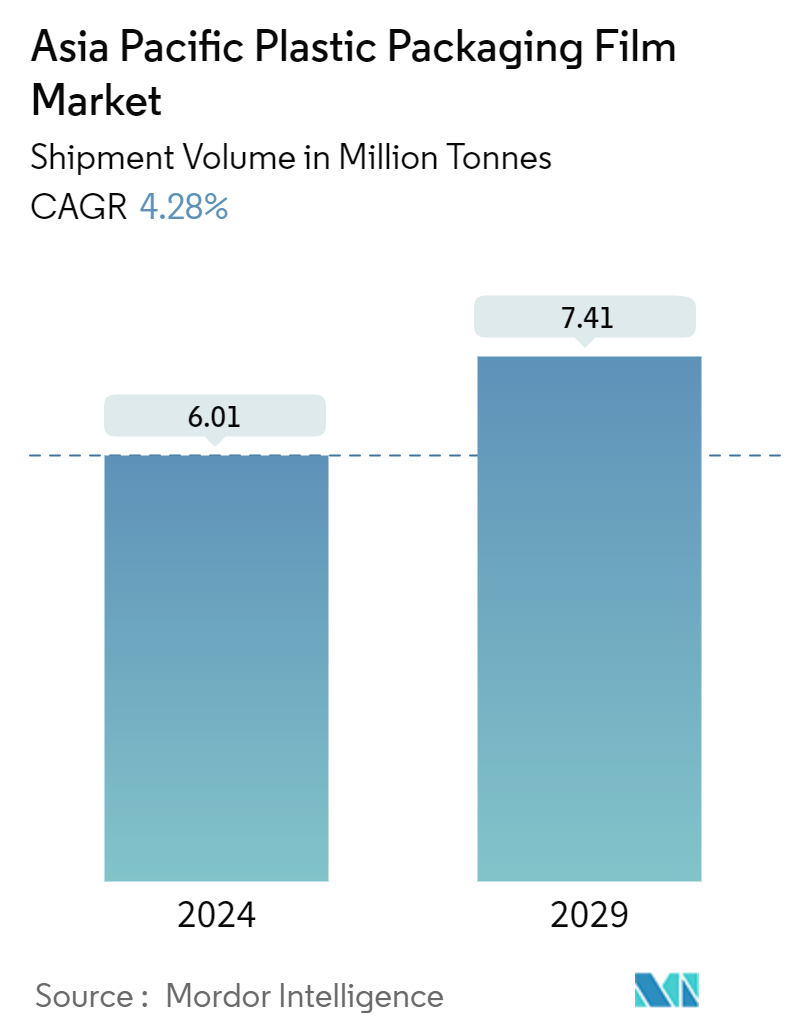

| Market Volume (2024) | 6.01 Million tonnes |

| Market Volume (2029) | 7.41 Million tonnes |

| CAGR (2024 - 2029) | 4.28 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Asia Pacific Plastic Packaging Film Market Analysis

The Asia Pacific Plastic Packaging Film Market size in terms of shipment volume is expected to grow from 6.01 Million tonnes in 2024 to 7.41 Million tonnes by 2029, at a CAGR of 4.28% during the forecast period (2024-2029).

- Asia-Pacific is poised to dominate the global flexible plastic packaging market in the coming years. Rapid urbanization, escalating disposable incomes, and a rising appetite for packaged foods can be attributed to this growth. The retail sector's swift expansion is bolstering the market. The surge in consumer goods available through e-commerce platforms amplifies the need for packaging films. These films are crucial in e-commerce, ensuring products are portable, secure, and durable.

- Asia-Pacific is significant in the global plastic films and sheets market, with China spearheading the demand. With both China and India showing consistent growth, Asia-Pacific is poised to retain its leading position globally. The surge in the consumption of ready-to-eat meals is fueling the demand for safe and eco-conscious packaging.

- The food and beverage industry is a primary consumer of plastic film packaging. This industry is pivoting toward eco-conscious packaging solutions. The market exhibits fragmentation; major players are actively creating innovative, cost-effective solutions to cater to evolving consumer needs.

- In January 2023, Ester Industries Limited (Ester Filmtech Limited) announced the commencement of commercial production at Telangana's new polyester (BOPET) film manufacturing facility. The 48,000 MTPA unit spans 50 acres and costs around INR 650 crore (USD 78.5 million). When the factory operates at its peak efficiency, it is anticipated to provide revenue of about INR 600 crores (USD 72.62 million). The products resulting from this new unit will primarily be utilized in the flexible packaging sector and contribute to expanding the flexible packaging sector's value chain.

- The retail sector in the Asia-Pacific region is vibrant and varied, with a range of formats such as supermarkets, hypermarkets, convenience stores, traditional shops, and online platforms. Given that the region hosts some of the world’s largest and swiftest-growing economies, its retail sector is thriving. In the Asia-Pacific region, the retail sector is poised to play a pivotal role in propelling the growth of the flexible packaging film market.

- The market faces challenges from evolving regulatory standards driven by mounting environmental apprehensions. In response to public awareness about plastic packaging waste, the federal governments of several countries like India and China are rolling out stringent regulations to curtail environmental harm and enhance waste management. This heightened environmental consciousness, coupled with concerns over single-use plastics and unsustainable business models, is prompting consumers to seek products with reduced environmental footprints.

Asia Pacific Plastic Packaging Film Industry Segmentation

Plastic films are thin, continuous materials typically wound on a core or cut into sheets. The study tracks the demand for converted packaging films across the major resin and application types. The analysis delves into various film types, including polypropylene (PP), polyethylene film (PE), polyethylene terephthalate films (PET), polystyrene films (PS), bio-based, and other variants. The segmentation extends to encompass end-user industries and specific countries.

The Asia-Pacific plastic packaging film market is segmented by type (polypropylene (biaxially oriented polypropylene (BOPP) and cast polypropylene (CPP)), polyethylene (low-density polyethylene (LDPE) and linear low-density polyethylene (LLDPE)), polyethylene terephthalate (biaxially oriented polyethylene terephthalate (BOPET)), polystyrene, bio-based, and PVC, EVOH, PETG, and other film types) and end user (food [candy & confectionery, frozen foods, fresh produce, dairy products, dry foods, meat, poultry, and seafood, pet food, and other food products], healthcare, personal care & home care, industrial packaging, and other end users). The market sizes and forecasts are provided in terms of volume (units) for all the above segments.

| By Type | |

| Polypropylene (Biaxially Oriented Polypropylene (BOPP), Cast polypropylene (CPP)) | |

| Polyethylene (Low-Density Polyethylene (LDPE), Linear low-density polyethylene (LLDPE)) | |

| Polyethylene Terephthalate (Biaxially Oriented Polyethylene Terephthalate (BOPET)) | |

| Polystyrene | |

| Bio-Based | |

| PVC, EVOH, PETG, and Other Film Types |

| By End User | ||||||||||

| ||||||||||

| Healthcare | ||||||||||

| Personal Care & Home Care | ||||||||||

| Industrial Packaging | ||||||||||

| Other End-use Industry Applications |

| By Country | |

| China | |

| India | |

| Japan | |

| Thailand | |

| Australia and New Zealand | |

| Indonesia | |

| Vietnam |

Asia Pacific Plastic Packaging Film Market Size Summary

The Asia-Pacific plastic packaging film market is set to experience significant growth, driven by factors such as rapid urbanization, increasing disposable incomes, and a growing demand for packaged foods. The region is expected to maintain its dominance in the global flexible plastic packaging market, with China and India leading the charge. The expansion of the retail sector, particularly through e-commerce platforms, is further propelling the demand for packaging films, which are essential for ensuring product safety and durability during transit. The food and beverage industry remains a major consumer of plastic film packaging, with a notable shift towards eco-conscious solutions. The market is characterized by fragmentation, with key players focusing on innovation and cost-effectiveness to meet evolving consumer preferences.

The market landscape is marked by significant investments and expansions, such as Ester Industries Limited's new polyester film manufacturing facility in India and Toray Industries' increased production capacity for BOPP films in Japan. BOPP films, known for their versatility and superior properties, are gaining traction across various sectors, including pharmaceuticals and cosmetics, due to their effective sealing and oxygen barrier capabilities. The Indian market, in particular, is witnessing robust growth in frozen foods and snacks, driven by changing consumer lifestyles and preferences. However, the market faces challenges from stringent environmental regulations aimed at reducing plastic waste, prompting a shift towards sustainable packaging solutions. Major players are actively developing innovative products to enhance packaging performance and sustainability, ensuring the market's continued expansion.

Asia Pacific Plastic Packaging Film Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Attractiveness - Porter's Five Forces Analysis

-

1.2.1 Bargaining Power of Buyers

-

1.2.2 Bargaining Power of Suppliers

-

1.2.3 Threat of Substitutes

-

1.2.4 Threat of New Entrants

-

1.2.5 Intensity of Competitive Rivalry

-

-

1.3 Industry Value Chain Analysis

-

-

2. MARKET SEGMENTATION

-

2.1 By Type

-

2.1.1 Polypropylene (Biaxially Oriented Polypropylene (BOPP), Cast polypropylene (CPP))

-

2.1.2 Polyethylene (Low-Density Polyethylene (LDPE), Linear low-density polyethylene (LLDPE))

-

2.1.3 Polyethylene Terephthalate (Biaxially Oriented Polyethylene Terephthalate (BOPET))

-

2.1.4 Polystyrene

-

2.1.5 Bio-Based

-

2.1.6 PVC, EVOH, PETG, and Other Film Types

-

-

2.2 By End User

-

2.2.1 Food

-

2.2.1.1 Candy & Confectionery

-

2.2.1.2 Frozen Foods

-

2.2.1.3 Fresh Produce

-

2.2.1.4 Dairy Products

-

2.2.1.5 Dry Foods

-

2.2.1.6 Meat, Poultry, And Seafood

-

2.2.1.7 Pet Food

-

2.2.1.8 Other Food Products

-

-

2.2.2 Healthcare

-

2.2.3 Personal Care & Home Care

-

2.2.4 Industrial Packaging

-

2.2.5 Other End-use Industry Applications

-

-

2.3 By Country

-

2.3.1 China

-

2.3.2 India

-

2.3.3 Japan

-

2.3.4 Thailand

-

2.3.5 Australia and New Zealand

-

2.3.6 Indonesia

-

2.3.7 Vietnam

-

-

Asia Pacific Plastic Packaging Film Market Size FAQs

How big is the Asia Pacific Plastic Packaging Film Market?

The Asia Pacific Plastic Packaging Film Market size is expected to reach 6.01 million tonnes in 2024 and grow at a CAGR of 4.28% to reach 7.41 million tonnes by 2029.

What is the current Asia Pacific Plastic Packaging Film Market size?

In 2024, the Asia Pacific Plastic Packaging Film Market size is expected to reach 6.01 million tonnes.