APAC Payments Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

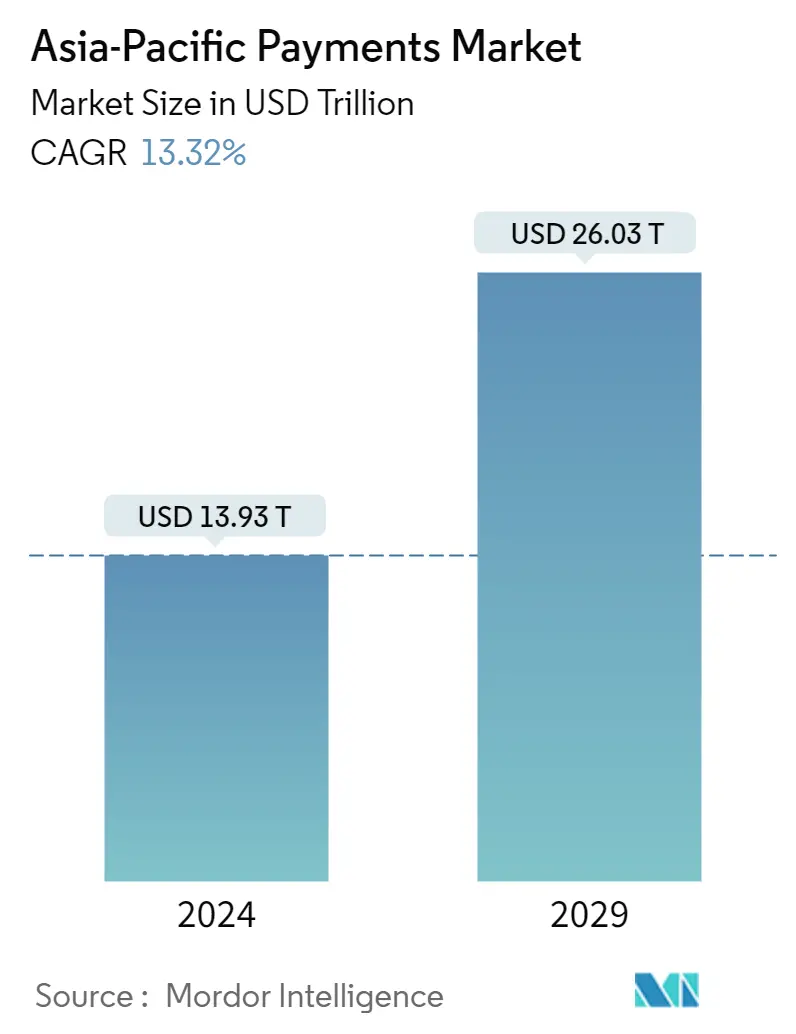

| Market Size (2024) | USD 13.93 Trillion |

| Market Size (2029) | USD 26.03 Trillion |

| CAGR (2024 - 2029) | 13.32 % |

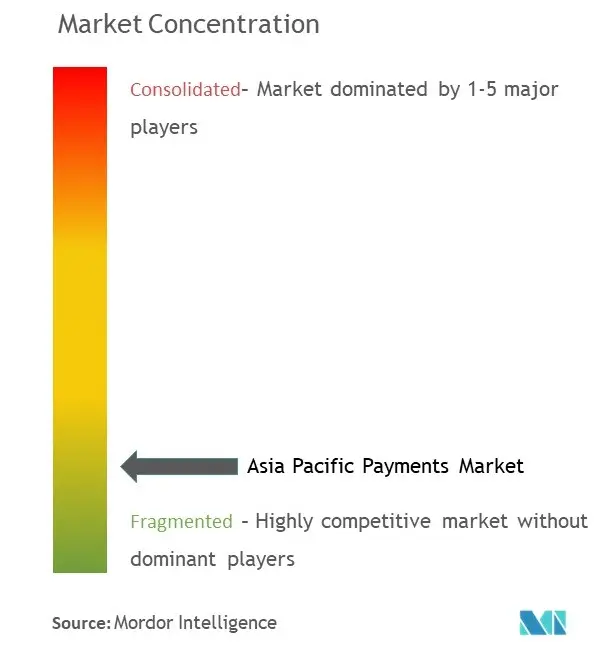

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

APAC Payments Market Analysis

The Asia-Pacific Payments Market size is estimated at USD 13.93 trillion in 2024, and is expected to reach USD 26.03 trillion by 2029, growing at a CAGR of 13.32% during the forecast period (2024-2029).

- In Asia-Pacific, consumers are increasingly moving to contactless and electronic payments. They continue to move away from using cash. The main reason for this change is the incredible speed at which payment technology is evolving in the region.

- In emerging and developing regions such as the Asia Pacific, mobile payments have grown tremendously due to the ease of transactions, the widespread use of smartphones, and the financial inclusion capabilities of technology.

- With the spread of smartphones and the Internet, the adoption of mobile wallets has been accelerating over the years. China and India now make up more than 50% of the world's smartphone population, making e-Wallet use the mainstream. They provide convenience and security for payment processing and are currently at the forefront of payment changes. Additionally, the unique characteristics of the payment environment in the Asia-Pacific region are that the government is actively pursuing policies that encourage cashless payments.

- However, data privacy remains a big challenge for mobile phone applications providing payment services. Companies continuously attempt to create simpler and safer methods of authenticating their clients' identities, increasing their policies' safety and dependability. Some companies look forward to integrating official papers like driver's licenses to verify users and avoid fraudulent accounts. Such measures help to strengthen mobile payments.

- •During the COVID-19 pandemic, digital payments accelerated in the Asia-Pacific region. Physical or contactless cards and digital wallets were the most common payment methods during the pandemic, but in some countries, during the Covid-19 pandemic cash remained the primary payment method. Further, to seamlessly transition to mobile payments, which may be an integral part of the more digital post-COVID-19 world, the Asian economies are poised to strengthen their regulatory frameworks and invest in digital networks and infrastructure, such as those enabling the usage of digital IDs.

APAC Payments Market Trends

Online sales segment to show higher growth

- The mobile payment landscape across Asia is changing due to digital transformation. Also, the technological developments in the smartphone have enabled e-commerce payments and on-the-go fund transfers, fueling the global market growth. Mobile payment platforms like Tencent, based in China, have grown rapidly. Tencent also expanded in other Asian countries, like Thailand, and it is searching for major partners to help it localize its services.

- The most common payment medium is projecting QR codes at the shop, wherein small-scale local shops also accept mobile payments. As China and India have been leading in this form of payment, countries like Japan are slowly introducing initiatives to promote QR code-based payments due to the government's aim to double cashless transactions to JPY 120 trillion (90 Billion USD) in 2025.

- The consumer preference toward digital payment methods indicates the increasing use of contactless payment modes. For instance, in the current year, Worldline, a provider of payment services, teamed up with Casio, a business with its headquarters in Japan, to enable card payments and cashless shopping in Japan. Offering this service in Japan will support efforts to change that country's more traditional retail environment. This will also involve Vesca, a regional payment solution supplier, focusing on a large Japanese market primarily of small business retailers.

- The rise of e-commerce and the O2O market has created many scenarios for people to adopt mobile payments in recent years. According to WorldPay, digital/mobile wallet is expected to occupy 60.2% of e-commerce payments in 2024 in Asia-Pacific, followed by credit card (16.1%). On the other hand, mobile payment was crucial in reducing friction and making on-demand, small-ticket services easily adoptable when they first emerged in the region. Rapid developments in these sectors, in turn, further drive the uptake in mobile payment usage.

- Further, the e-commerce sector in retail businesses is witnessing a spike in demand as consumers order essential items such as food and clothes, among others, through e-commerce websites, where most consumers prefer the digital mode of payment. According to a survey of cross-border e-commerce enterprises last year, PayPal was the dominant digital payment platform in the Philippines, with 74% of the enterprises using it.

- According to RBI, the digital payments index (DPI), launched in January of last year to indicate the extent of digitization of payments in India, the index for September of the same year stood at 304.06 against 270.59 in March. This shows the rapid adoption and deepening of digital payments across the country.

Malaysia is Expected to hold Major Market Share of the Market

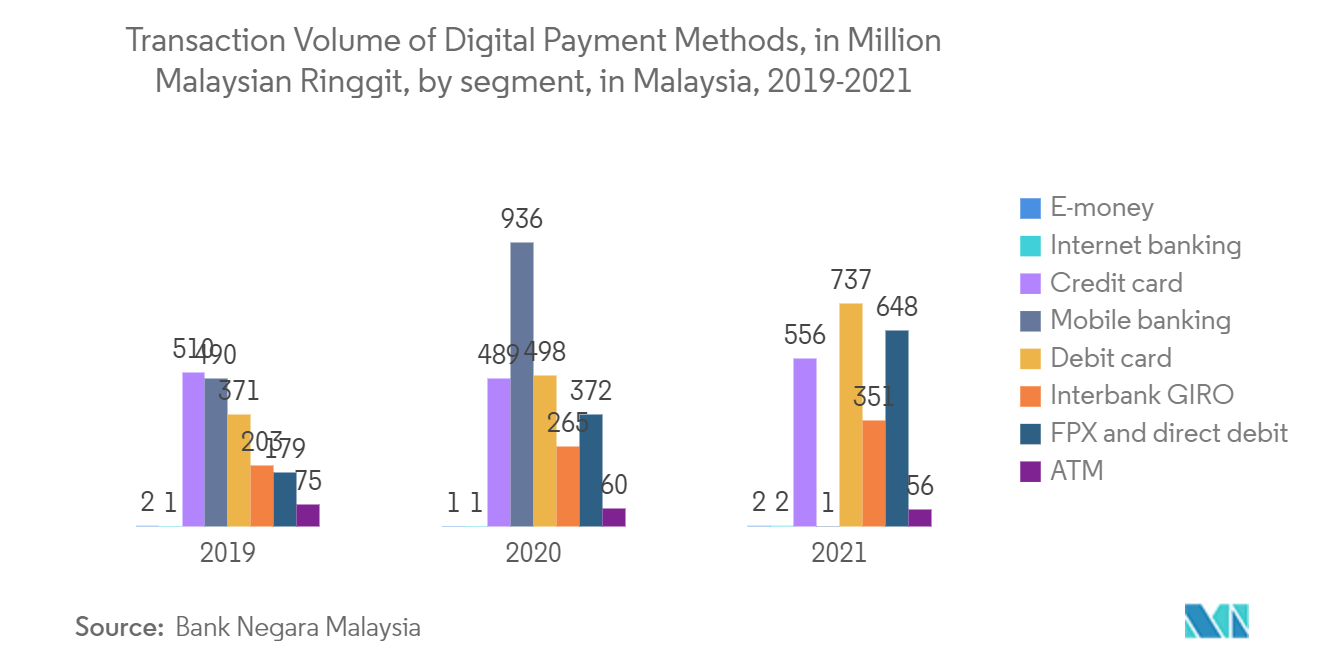

- Payment systems are an essential component of a country's economic infrastructure. The Bank Negara Malaysia-owned Payments Network Malaysia Sdn Bhd (PayNet), a payment subsidiary, operates Malaysia's extensive value payment system, RENTAS, which permits the transfer and settlement of high-value interbank payments and securities. Its failure could trigger a systemic crisis and send shockwaves through the financial system. With RENTAS's effective operation, transactions may be completed securely and promptly, boosting economic performance. According to Bank Negara Malaysia, the overall transaction value for digital payment methods in Malaysia last year, including e-money, online banking, FPX, and mobile internet, was RM 7.9 Billion (1.71 Billion USD). Total transaction value increased by 1.9 billion Malaysian ringgit over the previous year.

- Payment systems that are secure and effective are essential for promoting financial stability as they make it simpler for Bank Negara Malaysia to carry out its monetary policy by allowing it to use more market-based instruments to accomplish its goals while also improving the effectiveness of the financial system and the economy. Given its significance, one of the bank's primary foundations is promoting a reliable, efficient, and secure payment system.

- Furthermore, COVID-19 resulted in a significant boost in demand for digital payments in the country. Malaysia has achieved substantial progress in financial inclusion in recent years, owing to favorable policies, innovation, and a growing banking sector. Recently, in April of the current year, Bank Negara Malaysia (BNM) announced five successful applications for digital bank licenses, which Malaysia's Minister approved Finance. The applicants will undergo operational preparedness following this announcement, which BNM will verify through an audit before commencing operations. BNM is expected to continue collaborating with the financial and fintech sectors and key stakeholders through the five strategic thrusts outlined in the Financial Sector Blueprint 2022-2026 to continuously improve access to financial services nationwide and among all societal segments.

- As Malaysia moves closer to becoming a cashless society and digital payments become more widely used, market providers are improving their payment options to help shops and merchants position themselves for the future of commerce and meet customer expectations. However, small businesses continue to rely heavily on cash transactions. Getting cashless will also be difficult for certain small businesses, and street vendors need help acquiring the equipment to keep their digital currency.

- The growing collaborations and partnerships to meet the growing demand for payments in the country are the key factors contributing to the market growth rate. For instance, in September of the year, Ingenico, a Worldline Brand, and Paysys(M) Sdn Bhd, a wholly owned subsidiary of GHL Systems Bhd, announced merging their commercial competencies to address the Malaysian payment market. Ingenico will likely sell some of its client and business assets to GHL in Malaysia as part of this deal. By developing this new operating model, Ingenico will strengthen its position in Malaysia by utilizing Paysys' in-depth understanding of the market and bringing Ingenico's wide array of payment solutions to open new opportunities with more clients and unlock new payment experiences.

APAC Payments Industry Overview

The Asia-Pacific payments market is highly competitive as crucial players in the region are developing new solutions in the e-commerce market for various end-user applications. Companies also invest and form partnerships to grow their regional businesses and provide the country's e-commerce platform. Some market players, such as Visa, Mastercard, Samsung Pay, American Express, and Naver Corporation, are increasing their market presence by moving across the untapped market space.

In June 2022, Samsung Pay introduced the Samsung Wallet by combining Samsung Pay and Samsung Pass. This wallet could securely save passwords and monitor digital assets like cryptocurrencies. Moreover, the Samsung Wallet included features to store driving licenses and student IDs.

In March 2022, Mastercard, DBS Bank, and Pine Labs partnered to launch Mastercard Installation Payments with Pine Labs. This new program allows DBS/POSB credit cardholders to pay interest-free installments with merchants by simply presenting the DBS / POSB and using a later pay identifier card at checkout.

APAC Payments Market Leaders

-

Matercard Inc.

-

Visa Inc

-

American Express Company

-

Samsung (Samsung Pay)

-

Naver Corporation (Naver Pay)

*Disclaimer: Major Players sorted in no particular order

APAC Payments Market News

- October 2023, According to a statement made by the National Payments Corporation of India (NPCI), six Indian banks contributing to the arrangement are Indian Bank, Axis Bank, Bank, DBS Bank India, ICICI Indian Overseas Bank, as well as State Bank of India. India and Singapore are all set to increase the range of their digital payment link after they proclaimed the milestone linkage between India’s Unified Payments Interface (UPI) in addition to Singapore’s PayNow.

- •July 2023, Razorpay announced that it plans to strengthen its presence in Malaysia and the company launched its first international payment gateway through Curlec The newly launched Curlec Payment Gateway is projected to serve more than 5,000 companies with an objective of RM10 Bn in annualized Gross Transaction Value (GTV) by the year 2025.

APAC Payments Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Stakeholder Analysis

4.3 Industry Attractiveness- Porter's Five Forces Analysis'

4.3.1 Bargaining Power of Suppliers

4.3.2 Bargaining Power of Buyers/Consumers

4.3.3 Threat of New Entrants

4.3.4 Threat of Substitute Products

4.3.5 Intensity of Competitive Rivalry

4.4 Evolution of the payments landscape in the region

4.5 Assessment of Impact of COVID-19 on the Market

4.6 Analysis of Growing Payment Fraud in Asia-Pacific and its Impact on the Payments Market

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 High Proliferation of E-commerce and Rising Adoption of M-commerce

5.1.2 Enablement Programs by Key Retailers and Government Encouraging Digitization of the Market

5.1.3 Growing Adoption of Buy Now Pay Later in Asia-Pacific Countries

5.2 Market Challenges

5.2.1 Lack of a Standard Legislative Policy Remains, Especially in the Case of Cross-border Transactions

5.3 Market Opportunities

5.3.1 New Entrants to Drive Innovation Leading to Higher Adoption

5.4 Key Regulations and Standards in the Digital Payments Industry

5.5 Analysis of Major Case Studies and Use-cases

5.6 Analysis of Key Demographic Trends and Patterns Related to Payments Industry in the Asia Pacific (Coverage to include Population, Internet Penetration, Banking Penetration/Unbanking Population, Age & Income etc.)

5.7 Analysis of the Increasing Emphasis on Customer Satisfaction and Convergence of Global Trends in the Asia Pacific

5.8 Analysis of Cash Displacement and Rise of Contactless Payment Modes in the Asia-Pacific

6. MARKET SEGMENTATION

6.1 By Mode of Payment

6.1.1 Offline (Point of Sale)

6.1.1.1 Card Payments (includes debit cards, credit cards, and bank financing prepaid cards)

6.1.1.2 Digital Wallets (includes mobile wallets)

6.1.1.3 Cash

6.1.1.4 Other Modes of Payment

6.1.2 Online Sale (E-commerce)

6.1.2.1 Card Payments (includes debit cards, credit cards, and bank financing prepaid cards)

6.1.2.2 Digital Wallets (includes mobile wallets)

6.1.2.3 Other Modes of Payment (Includes cash on delivery, bank transfer, and buy now pay later)

6.2 By End-user Industry

6.2.1 Retail

6.2.2 Entertainment

6.2.3 Healthcare

6.2.4 Hospitality

6.2.5 Other End-user Industries

6.3 By Country

6.3.1 China

6.3.2 India

6.3.3 South Korea

6.3.4 Taiwan

6.3.5 Singapore

6.3.6 Philippines

6.3.7 Malaysia

6.3.8 Indonesia

6.3.9 Vietnam

6.3.10 Australia

6.3.11 Japan

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles

7.1.1 Matercard Inc.

7.1.2 Visa Inc

7.1.3 American Express Company

7.1.4 Samsung (Samsung Pay)

7.1.5 Naver Corporation (Naver Pay)

7.1.6 PayCo (NHN Corp.)

7.1.7 kakaopay Corp.

7.1.8 JCB Co., Ltd.

7.1.9 Toss Financial Services Private Limited

7.1.10 Smile Pay

7.1.11 Paypal Holdings Inc.

7.1.12 Google Pay (Alphabet Inc.)

7.1.13 Ipay88 (m) Sdn. Bhd

7.1.14 Samsung Pay (Samsung Electronics Co.ltd)

7.1.15 Grab Pay (grab Holdings Limited)

7.1.16 Huawei Pay (Huawei Technologies Co. Limited

- *List Not Exhaustive

8. INVESTMENT ANALYSIS

9. MARKET OPPORTUNITIES AND FUTURE TRENDS

APAC Payments Industry Segmentation

The scope of the study tracks transactions generated at offline (POS) physical stores and online (E-commerce/digital) channels in Asia-Pacific. Online payments include online purchases of goods and services, such as purchases on e-commerce websites and online bookings for travel and accommodation. However, they do not include online purchases of motor vehicles, real estate, utility bills (such as water, heating, and electricity), mortgage payments, loans, credit card bills, or purchases of shares and bonds. In the offline segment, all transactions at the physical point of sale are included in the market scope. It includes traditional in-store and face-to-face transactions, regardless of where they occur. Cash is also considered for both cases (cash on delivery for e-commerce sales).

The Asia-Pacific Payments Market is Segmented by Mode of Payment (Offline/Point of Sale (Card Payments, Digital Wallets, Cash), Online Sale/E-commerce (Card Payments, Digital Wallet)), End-user Industries (Retail, Entertainment, Healthcare, Hospitality), and Country (China, India, South Korea, Taiwan, Singapore, Philippines, Malaysia, Indonesia, Vietnam, Australia, and Japan).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Mode of Payment | ||||||

| ||||||

|

| By End-user Industry | |

| Retail | |

| Entertainment | |

| Healthcare | |

| Hospitality | |

| Other End-user Industries |

| By Country | |

| China | |

| India | |

| South Korea | |

| Taiwan | |

| Singapore | |

| Philippines | |

| Malaysia | |

| Indonesia | |

| Vietnam | |

| Australia | |

| Japan |

APAC Payments Market Research FAQs

How big is the Asia-Pacific Payments Market?

The Asia-Pacific Payments Market size is expected to reach USD 13.93 trillion in 2024 and grow at a CAGR of 13.32% to reach USD 26.03 trillion by 2029.

What is the current Asia-Pacific Payments Market size?

In 2024, the Asia-Pacific Payments Market size is expected to reach USD 13.93 trillion.

Who are the key players in Asia-Pacific Payments Market?

Matercard Inc., Visa Inc, American Express Company, Samsung (Samsung Pay) and Naver Corporation (Naver Pay) are the major companies operating in the Asia-Pacific Payments Market.

What years does this Asia-Pacific Payments Market cover, and what was the market size in 2023?

In 2023, the Asia-Pacific Payments Market size was estimated at USD 12.29 trillion. The report covers the Asia-Pacific Payments Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Asia-Pacific Payments Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

APAC Payment Systems Industry Report

The Asia-Pacific Payments Market Report provides an in-depth industry analysis, offering valuable industry information and an industry outlook for the coming years. This comprehensive report covers various modes of payment, including offline/point of sale options such as card payments, digital wallets, and cash, as well as online sale/e-commerce methods like card payments and digital wallets. The industry research extends to multiple end-user industries, including retail, entertainment, healthcare, and hospitality, across numerous countries in the Asia-Pacific region.

The report includes market data and a market forecast, highlighting the expected market growth and market trends over the forecast period. It reviews the market segmentation and market value, providing a detailed market overview and market predictions. The analysis also identifies market leaders, offering insights into their market outlook and market review.

Additionally, the report features industry reports and industry statistics, giving a clear picture of the industry's current state and future prospects. It includes a report example and a report PDF for further reference. The research companies involved provide extensive industry research, ensuring the accuracy and reliability of the findings.

In summary, this report is an essential resource for understanding the dynamics of the Asia-Pacific payments market, offering detailed market segmentation, market value, and market predictions, supported by comprehensive industry statistics and trends.

APAC Payment Systems Market Report Snapshots