Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 193.09 Billion |

| Market Size (2031) | USD 240.43 Billion |

| Growth Rate (2026 - 2031) | 4.49% CAGR |

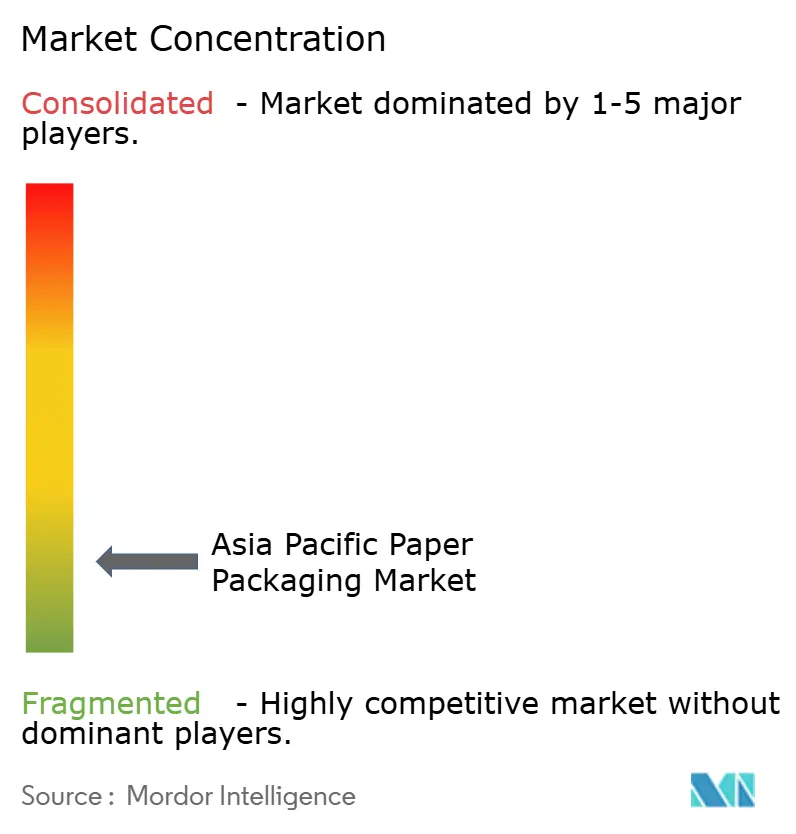

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific Paper Packaging Market Analysis by Mordor Intelligence

Asia Pacific paper packaging market size in 2026 is estimated at USD 193.09 billion, growing from 2025 value of USD 184.79 billion with 2031 projections showing USD 240.43 billion, growing at 4.49% CAGR over 2026-2031. Robust urbanization exceeding 60% across leading economies, coupled with e-commerce that already commands 80% of packaging demand, underpins near-term volume expansion. Region-wide adoption of Extended Producer Responsibility (EPR) regimes in Vietnam, Australia and Thailand is steering capital toward recycled grades and high-barrier coatings, thereby nudging average selling prices upward while trimming virgin-fiber exposure. Containerboard remains the workhorse substrate because corrugated formats dominate last-mile logistics, yet carton board is rapidly gaining favor in premium consumer goods and regulated healthcare channels as brand owners prioritize print quality, barrier functionality and sustainability. Producers are investing in AI-enabled design software and short-run digital printing to satisfy explosive SKU proliferation, even as hardwood pulp price swings and Chinese over-capacity keep margins under pressure.

Key Report Takeaways

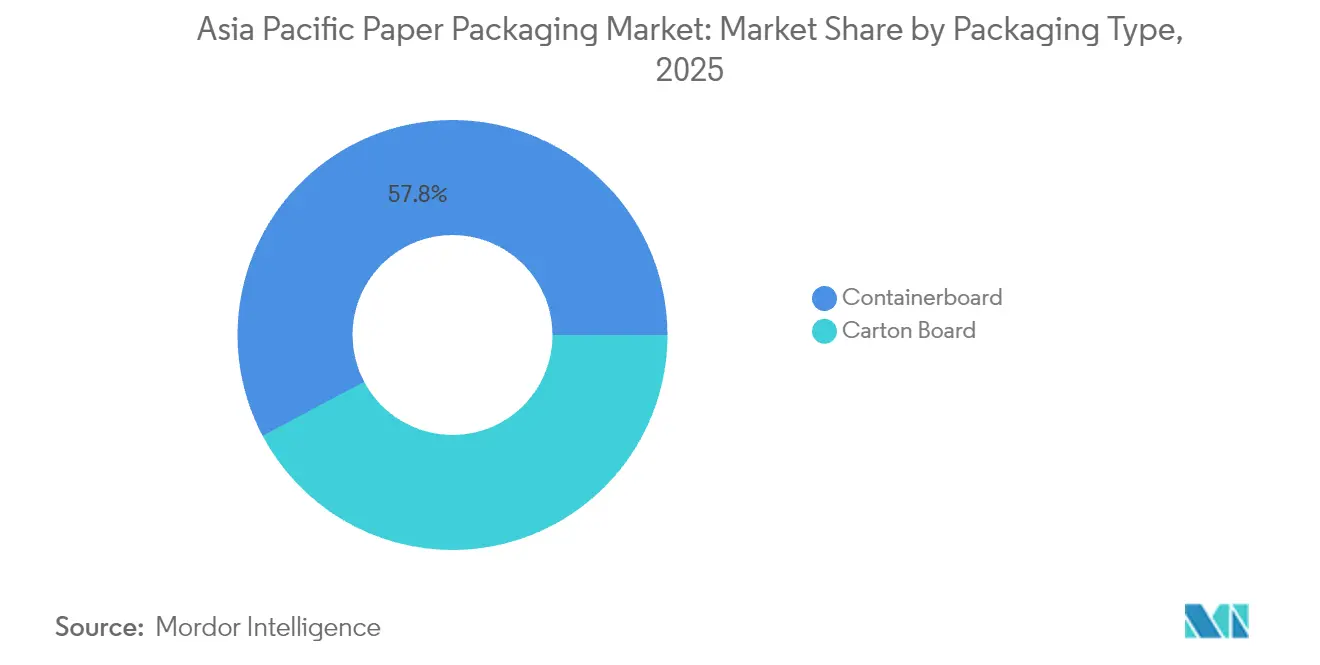

- By packaging type, containerboard led with 57.76% of Asia Pacific paper packaging market share in 2025, while carton board is projected to advance at a 5.39% CAGR to 2031.

- By grade, Other Testliners captured 39.10% share of the Asia Pacific paper packaging market size in 2025; white-top kraftliner is expanding at a 6.46% CAGR through 2031.

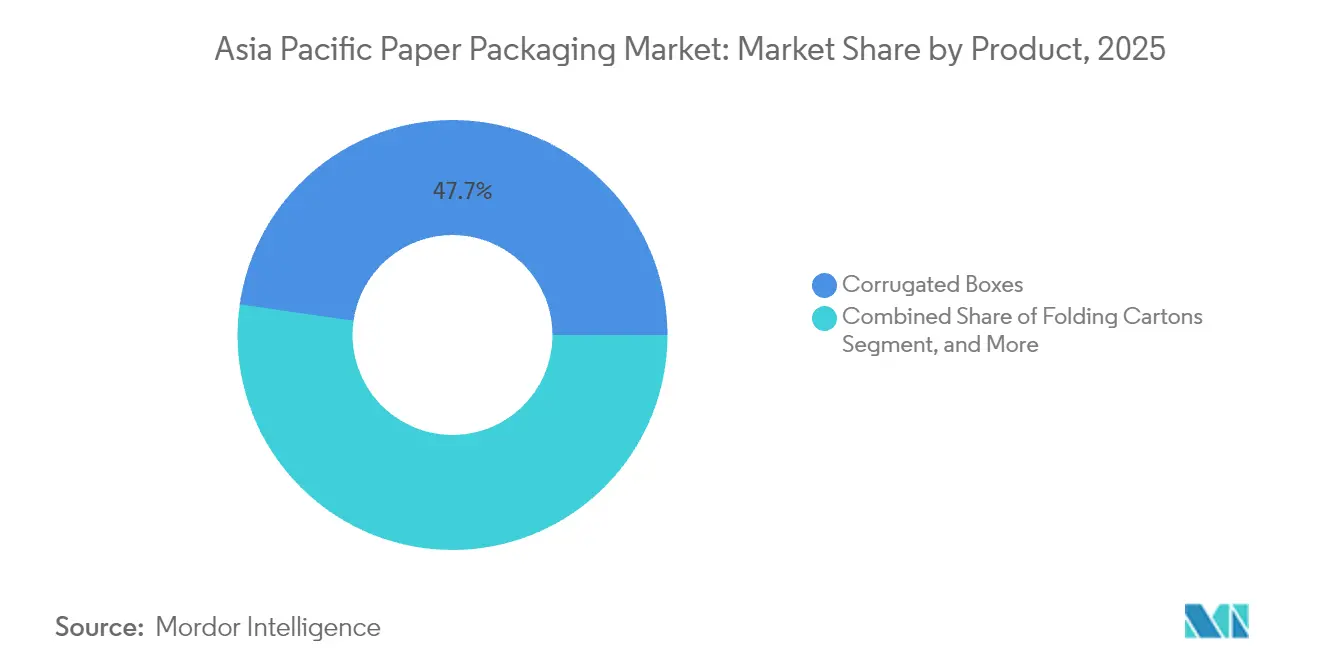

- By product, corrugated boxes accounted for 47.72% of the Asia Pacific paper packaging market share in 2025, whereas folding cartons record the fastest 5.72% CAGR to 2031.

- By end-user industry, food claimed 27.10% revenue share in 2025, but electrical & electronics exhibits the highest 8.17% CAGR across the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia Pacific Paper Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in e-commerce packaging demand | +1.2% | Global, with concentration in China, India, Southeast Asia | Short term (≤ 2 years) |

| Rapid shift toward recycled paper grades | +0.8% | APAC core, regulatory spillover to emerging markets | Medium term (2-4 years) |

| Expansion of food, beverage and healthcare sectors | +0.7% | India, Indonesia, Vietnam with urban concentration | Medium term (2-4 years) |

| EPR and content-mandate regulations across APAC | +0.6% | Australia, Vietnam, Thailand with regional expansion | Long term (≥ 4 years) |

| High-barrier coated paper replacing plastics | +0.5% | Japan, Australia, South Korea leading adoption | Long term (≥ 4 years) |

| Generative AI-enabled design and short-run printing | +0.4% | China, Japan, South Korea technology hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in e-commerce packaging demand

Corrugated formats now ship 80% of all e-commerce parcels in Asia Pacific, pushing annual box volumes to record highs and spurring mill conversions from newsprint to recycled containerboard.[1]Norske Skog, “Update on Strategic Projects in Norske Skog,” norskeskog.comChinese express shipments alone generated roughly 22 million tons of packaging waste in 2024, prompting municipal pilots that subsidize reusable corrugated totes. Regional sellers simultaneously deploy fit-to-product systems that trim board usage by up to 30% without sacrificing protection, heightening demand for algorithm-based design services. Manufacturers are therefore establishing micro-hubs that bring die-cutting and digital print capacity closer to fulfillment centers, allowing 24-hour turnaround on custom graphics. Intensifying competition in same-day delivery widens the opportunity for lightweight, high-strength fluting grades that lower last-mile freight costs.

Rapid shift toward recycled paper grades

Vietnam’s EPR decree mandates 20% recycling for carton packaging beginning 2024, accelerating mill investment in closed-loop fiber recovery lines that boost de-inking capacity. Australia’s 2024 draft regulation sets minimum recycled-content thresholds for all packaging, transferring liability to brand owners should targets be missed and elevating demand for certified post-consumer fiber. India already derives 70% of paper output from non-wood sources, offering domestic converters a cost hedge against virgin pulp volatility. Higher dependence on secondary fibers, however, raises energy intensity 15-20% owing to contaminant removal, prompting mills to pilot enzyme-assisted cleaning technologies. Early adopters tout double-digit EPR-fee savings, positioning recycled-grade specialists as preferred suppliers to multinational consumer-goods clients.

Expansion of food, beverage and healthcare sectors

Rising incomes and urban convenience cultures swell packaged-food purchases, while regulatory reforms spur pharmaceutical serialization and hygienic dispensing. India targets USD 204.81 billion in sectoral value by 2025, pulling through demand for grease-resistant folding cartons and multilayer liquid packaging. Japan’s Positive List for food-contact materials, effective June 2025, increases compliance hurdles for synthetic resins and nudges retailers toward paper-based trays that meet migration limits. Healthcare distributors specify substrates compatible with RFID and tamper-evident seals, favoring coated carton board over flexible plastics in cold-chain logistics. Beverage market premiumization in Thailand further catalyzes adoption of paper bottles with bio-based barrier layers, broadening the customer base for high-density cupstock.

EPR and content-mandate regulations across APAC

Government interventions create predictable demand for compliant substrates, yet they also raise operating complexity for converters active in multiple jurisdictions. Australia, Vietnam and Thailand now require traceable reporting of post-consumer recovery volumes, encouraging vertically integrated firms to acquire material-recovery facilities. Producers with region-wide compliance expertise monetize certification services, effectively bundling packaging supply with regulatory assurance. Over the long term, mandated thresholds are expected to ratchet upward, underpinning steady price realization for recycled containerboard and recycled folding boxboard that meet tier-based incentives. Companies lacking scale are likely to exit unprofitable grades or form joint ventures to share recovery infrastructure.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pulp price volatility and supply shocks | -0.9% | Global, with acute impact on import-dependent markets | Short term (≤ 2 years) |

| Cost-competitive flexible plastic alternatives | -0.6% | Southeast Asia, price-sensitive applications | Medium term (2-4 years) |

| Chinese over-capacity driving price wars | -0.5% | China domestic, spillover to regional exports | Short term (≤ 2 years) |

| Carbon-intensity pressure on paper mills | -0.4% | Japan, Australia, South Korea with strict emissions targets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Pulp price volatility and supply shocks

Hardwood pulp averaged 30% price inflation during 2024 as climate events constrained forestry output, forcing Asian mills to announce USD 31.50 per-ton price hikes for early 2025. Currency depreciation in Indonesia and Thailand inflated landed costs a further 5-10%, eroding converter margins tied to fixed contracts. Import-heavy processors responded by forward-buying to lock in supplies, but storage constraints and inventory value-at-risk limit this tactic. Substitution toward recycled fibers lowers exposure, yet quality variation in recovered material heightens run-rate instability. Mills with captive plantations or balanced fiber baskets thus gain negotiating leverage over downstream box-plants.

Cost-competitive flexible plastic alternatives

Mono-material polyolefin films now attain oxygen barrier rates below 0.1 cm³/m²·day following atomic-layer deposition, while remaining 20-40% cheaper than coated paper in price-sensitive Southeast Asian snack formats.[2]Farshad Sharbafian et al., “Alternative Oxygen Barrier Coatings,” mdpi.com Thailand’s expansion of bio-ethylene capacity underscores plastics industry adaptation, offering renewable content without surrendering cost leadership. Food brands selling single-serve sachets weigh unit cost above recyclability, slowing paper substitution. To compete, carton converters are standardizing blank sizes and automating gluing to shave labor costs, while lobbying for landfill levies on non-recyclable films that would narrow the economics gap.

Segment Analysis

By Packaging Type: Containerboard dominance amid carton board acceleration

Containerboard controlled 57.76% of 2025 revenue as corrugated cases became the default shipper for omnichannel retail. The Asia Pacific paper packaging market size for containerboard is forecast to expand steadily, supported by fit-to-product algorithms that maintain board demand even as weights decline. Carton board’s 5.39% CAGR reflects premium positioning: folding boxboard and solid bleached sulfate satisfy high-graphic food, beauty and pharma needs, capturing share from rigid plastics.

Investment momentum favors recycled containerboard, illustrated by Norske Skog’s EUR 320 million Golbey conversion that will add 550,000 tpa of RCF-based liner by 2025. Integrated giants exploit captive OCC streams, whereas niche carton specialists capitalize on shorter change-over times and print-surface excellence. As EPR fees tilt cost curves toward recyclability, mid-sized independents face consolidation pressure or must pivot to service-driven carton niches.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Grade: Testliner leadership challenged by kraftliner innovation

Other Testliners held 39.10% of containerboard volume in 2025, benefiting from abundant recovered fiber and lower cost. Asia Pacific paper packaging market share for these grades could erode as brand owners demand stronger, brighter, white-top variants that lift shelf appearance. White-top kraftliner is growing fastest at 6.46% CAGR because high-definition flexo and digital graphics migrate onto shipper cartons, a trend amplified by social-media unboxing.

Folding boxboard dominated carton board grades at 41.12% while also leading grade growth at 6.05% CAGR. Next-generation clay and PVOH coatings grant water-vapor transmission rates suitable for dairy powders, anchoring FBB’s expansion. Producers that retrofit curtain-coaters can pivot between grease-proof food liners and pharma blister-wallet backers, enhancing asset flexibility. Mills lacking coating capability will likely cede ground to integrated rivals that bundle substrate, design and compliance documentation.

By Product: Corrugated box stability versus folding carton dynamism

Corrugated boxes captured 47.72% revenue in 2025, underpinned by e-commerce parcel flows and appliance cushioning. Lightweight fluting innovations maintain stack strength while shedding up to 15% grammage, supporting Asia Pacific paper packaging market competitiveness against plastic crates. Folding cartons are poised for 5.72% CAGR as pharma, personal-care and gourmet confectionery require high-resolution print and tamper evidence.

Digital inkjet presses with water-based inks unlock profitable micro-runs, persuading contract packers to onshore graphics rather than import blanks. Liquid packaging board remains a specialized niche tied to aseptic beverages; however, local fillers are piloting paper-bottle sleeves to meet plastic-reduction targets. Paper bags and sacks gain momentum in quick-service retail, helped by municipal bans on thin plastic carry-bags.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Industry: Food leadership challenged by electronics acceleration

Food applications represented 27.10% of 2025 sales, powered by retail ready and shelf-stable meal formats. Rising obesity awareness encourages portion-controlled packs, lifting demand for smaller, structurally rigid cartons. The Asia Pacific paper packaging market size attached to food is projected to grow 4.22% annually, though brand reformulation toward low-sugar snacks could moderate volume per SKU.

Electrical & electronics will advance at 8.17% CAGR through 2031 as semiconductor fabs multiply in India and Vietnam. Static-dissipative liners, cushioning honeycomb pads and serialized carton barcodes are now standard in high-value chip logistics. Personal-care and household-care segments post mid-single-digit growth, with sulfate-free detergent brands adopting coated paper pouches that stand upright on shelf yet recycle curbside. Healthcare cartons integrate RFID and braille, complicating print operations but fortifying supplier defensibility.

Geography Analysis

China’s heft derives from vertically integrated mills supplying domestic brands and export shippers, yet over-capacity keeps liner prices volatile. Government carbon-peak pledges push mills toward biomass boilers and wastewater heat recovery, inflating capital budgets but unlocking green-finance incentives. Producers such as Nine Dragons and APP diversify into pulp in Guangxi and Hainan to secure fiber and qualify for forestry carbon credits, reinforcing regional influence.

India’s ascent is supported by youthful demographics, fast-moving consumer goods penetration and a policy pivot toward circularity that rewards mills using agro-residue or recovered fiber. Export earnings from paper and paperboard multiplied six-fold between 2016-2022, highlighting competitiveness in light grammage carton board even with logistic bottlenecks. New capacity announcements from JK Paper and Century Plyboards underscore investor confidence despite power-tariff hikes.

Secondary markets present varied outlooks. Vietnam expects packaging value of USD 3.58 billion by 2026 on 9.58% annual growth, aided by near-shoring of electronics assembly. Thailand marries upstream biopolymers with downstream converters to offer bio-ethylene derived coatings, aligning with ASEAN plastic-waste reduction goals. Australia legislates recycled-content floors that spark M&A interest from global players seeking an ESG-friendly manufacturing base. Less mature economies across South Asia and Pacific Islands remain volume-light but promise first-mover advantages as retail formalizes.

Competitive Landscape

The region exhibits moderate fragmentation: the top five groups hold roughly 45% of linerboard capacity, with APP, Nine Dragons and SCG Packaging leading volumes. Vertical integration into pulp, energy and conversion fortifies cost positions, whereas mid-tier independents rely on customer intimacy in niche folding carton segments. Recent AI-enabled design rollouts by Japanese converters differentiate service speed, shrinking concept-to-shelf timelines from weeks to days.

Strategic capital is concentrating on barrier-coating lines and closed-loop OCC recovery. Amcor’s patent on AmFiber Performance Paper illustrates first-mover advantages in high-barrier recyclable formats. SCG Packaging reported EBITDA of VND 9.78 trillion in Q1 2025, crediting lightweight recyclable products for margin uplift. International Paper and Kimberly-Clark allocate North American funds to sustain global integration, yet still direct R&D to Asia for high-growth segments.

Patent filings in marine-biodegradable coatings and enzyme-assisted de-inking suggest sustained technology race. Emerging disruptors include specialized chemistry start-ups supplying bio-based resin additives and platform companies offering generative-AI design SaaS. Traditional converters respond through partnerships with OEMs such as Heidelberg for inline barrier-coat flexo presses, bundling print technology with substrate supply to lock in brand-owner relationships.

Asia Pacific Paper Packaging Industry Leaders

SCG Packaging PCL

International Paper Company

Oji Holdings Corporation

Sarnti Packaging Co., Ltd.

Mondi Group

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: International Paper posted net sales of USD 2.141 billion for Q1 2025, with corrugated shipments up 2.5%.

- April 2025: Stora Enso commenced production at its new consumer-board line in Oulu, Finland, targeting Asian exports via trans-Siberian routes.

- March 2025: Major Chinese mills, including APP and Nine Dragons, implemented USD 31.50-per-ton price increases to counter pulp and energy inflation.

- September 2024: Oji Fibre Solutions confirmed closure of its Penrose recycled-paper mill in New Zealand amid persistent losses.

Asia Pacific Paper Packaging Market Report Scope

Paper is frequently used to package products in several end-user industries. There are numerous grades of paperboard packaging. Like folding cartons, paperboard is the most common material used to manufacture containers. In manufacturing, the paperboard requires pulping, bleaching (optional), refining, sheet forming, drying, calendaring, and winding. Paper packaging materials can be efficiently reused and recycled compared to other materials, such as metals and plastics. This is why paper packaging is considered an eco-friendly and economical form of packaging. The study tracks the demand in the paper packaging market through the revenue accrued from the various paper packaging products offered by vendors operating in the market in the region.

The Asia-Pacific paper and packaging market report is segmented by grade (carton board [solid bleached sulfate (SBS), solid unbleached sulfate (SUS), folding boxboard (FBB), coated recycled board (CRB), and uncoated recycled board (URB)) and containerboard [white-top kraft-liner, other kraft-liners, white top test-liner, other test-liners, semi-chemical fluting, and recycled fluting]), product type (folding cartons, corrugated boxes), end-user industry (food, beverage, healthcare, personal care, household care, electrical products, and other end-user industry), and country (china, India, Japan, Indonesia, Thailand, Vietnam, Australia and New Zealand, rest of Asia-Pacific). The market size and forecasts are provided in terms of value (USD) for all the above segments.

By Packaging Type

| Carton Board |

| Containerboard |

By Grade

| Carton Board | Solid Bleached Sulfate (SBS) |

| Solid Unbleached Sulfate (SUS) | |

| Folding Boxboard (FBB) | |

| Coated Recycled Board (CRB) | |

| Uncoated Recycled Board (URB) | |

| Containerboard | White-top Kraftliner |

| Other Kraftliners | |

| White-top Testliner | |

| Other Testliners | |

| Semi-chemical Fluting | |

| Recycled Fluting |

By Product

| Folding Cartons |

| Corrugated Boxes |

| Liquid Packaging Board |

| Paper Bags and Sacks |

By End-User Industry

| Food |

| Beverage |

| Healthcare and Pharmaceuticals |

| Personal Care and Cosmetics |

| Household Care |

| Electrical and Electronics |

| Other End-user Industry |

By Country

| China |

| India |

| Japan |

| Indonesia |

| Thailand |

| Vietnam |

| Australia and New Zealand |

| Rest of Asia-Pacific |

| By Packaging Type | Carton Board | |

| Containerboard | ||

| By Grade | Carton Board | Solid Bleached Sulfate (SBS) |

| Solid Unbleached Sulfate (SUS) | ||

| Folding Boxboard (FBB) | ||

| Coated Recycled Board (CRB) | ||

| Uncoated Recycled Board (URB) | ||

| Containerboard | White-top Kraftliner | |

| Other Kraftliners | ||

| White-top Testliner | ||

| Other Testliners | ||

| Semi-chemical Fluting | ||

| Recycled Fluting | ||

| By Product | Folding Cartons | |

| Corrugated Boxes | ||

| Liquid Packaging Board | ||

| Paper Bags and Sacks | ||

| By End-User Industry | Food | |

| Beverage | ||

| Healthcare and Pharmaceuticals | ||

| Personal Care and Cosmetics | ||

| Household Care | ||

| Electrical and Electronics | ||

| Other End-user Industry | ||

| By Country | China | |

| India | ||

| Japan | ||

| Indonesia | ||

| Thailand | ||

| Vietnam | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the Asia Pacific paper packaging market?

The market is valued at USD 193.09 billion in 2026 and is projected to reach USD 240.43 billion by 2031 at a 4.49% CAGR.

Which packaging type dominates sales in the region?

Containerboard leads with 57.76% of 2025 revenue, reflecting heavy corrugated-box use in e-commerce.

Which segment shows the fastest growth?

Carton board is expanding at 5.39% CAGR as premium foods, cosmetics and pharma adopt high-printability grades.

Why is India the fastest-growing country market?

Government targets, rising consumption and high recycled-fiber utilization fuel a 7.34% CAGR through 2031

How are regulations shaping material choices?

EPR laws across Australia, Vietnam and Thailand mandate recycled-content thresholds, steering demand toward recovered-fiber containerboard and barrier-coated carton board.

What technologies are driving competitive advantage?

Generative-AI design platforms and high-barrier, recyclable paper coatings allow converters to offer rapid customization and plastic replacement solutions.