Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

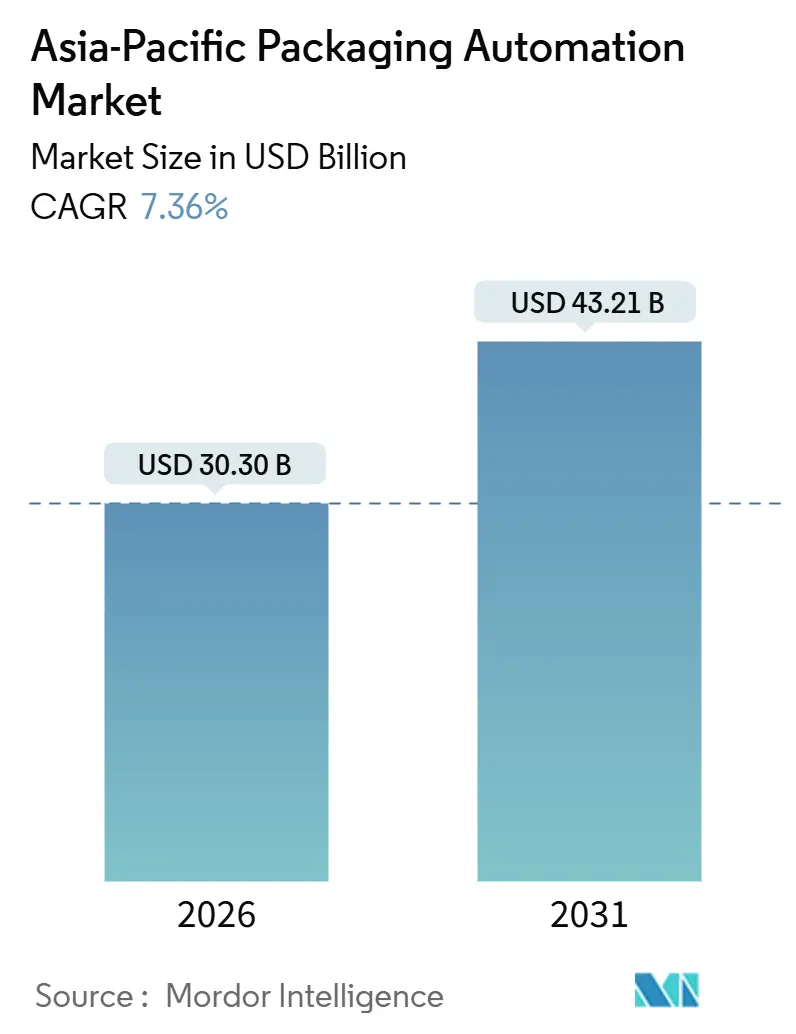

| Market Size (2026) | USD 30.30 Billion |

| Market Size (2031) | USD 43.21 Billion |

| Growth Rate (2026 - 2031) | 7.36% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Packaging Automation Market Analysis by Mordor Intelligence

The Asia-Pacific packaging automation market size reached USD 30.3 billion in 2026 and is projected to increase to USD 43.21 billion by 2031, growing at a 7.36% CAGR over the period. Strong momentum comes from rising labor costs, an expanding e-commerce ecosystem, and broad government support for Industry 4.0 adoption. Demand is also boosted by demographic shifts that tighten factory labor pools, semiconductor upgrades that enable higher throughput, and growing pressure on brand owners to cut packing waste. Manufacturers are prioritizing end-of-line robotics, while retailers and logistics providers are moving toward fully automated fulfillment nodes that shrink last-mile delivery times. Capital-light subscription models are emerging, and the Asia-Pacific packaging automation market is benefiting from this financing flexibility.

Key Report Takeaways

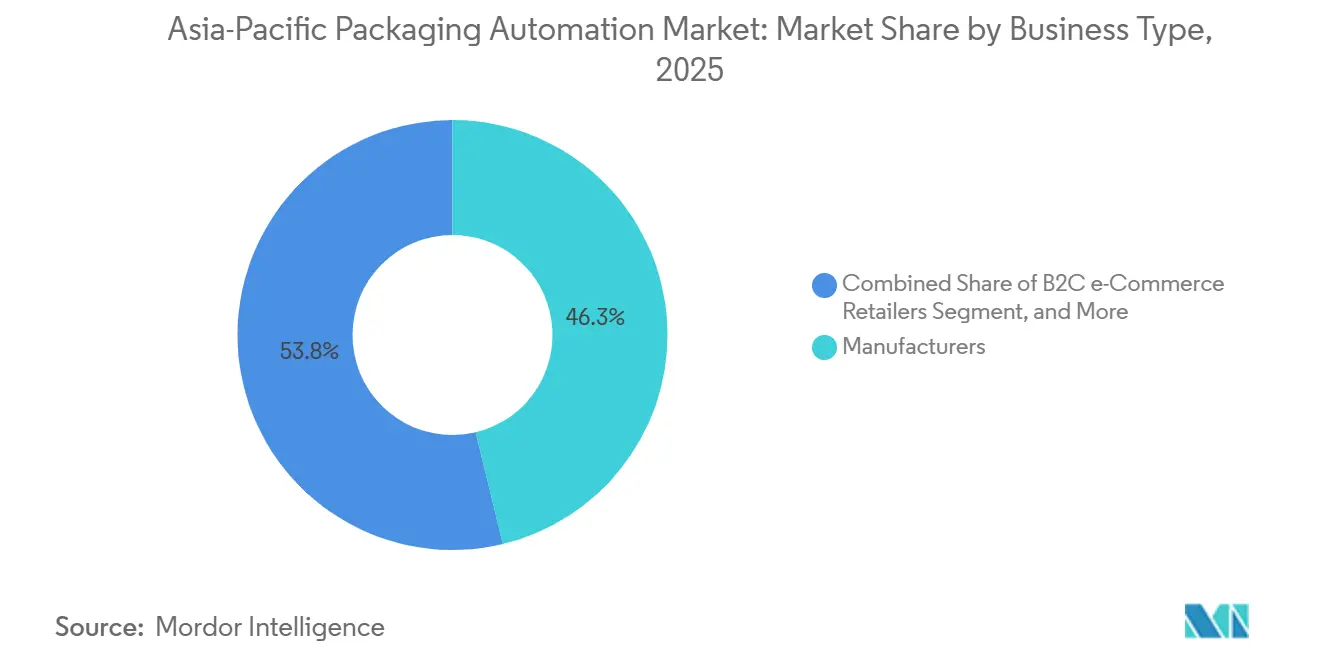

- By business type, manufacturers captured 46.25% of the Asia-Pacific packaging automation market share in 2025. However, the B2C e-commerce retailers segment is projected to rise at a 9.17% CAGR during the forecast period.

- By product type, filling machines accounted for a 28.84% share of the Asia-Pacific packaging automation market size in 2025. While, palletizing segment is projected to grow at an 8.97% CAGR between 2026 and 2031.

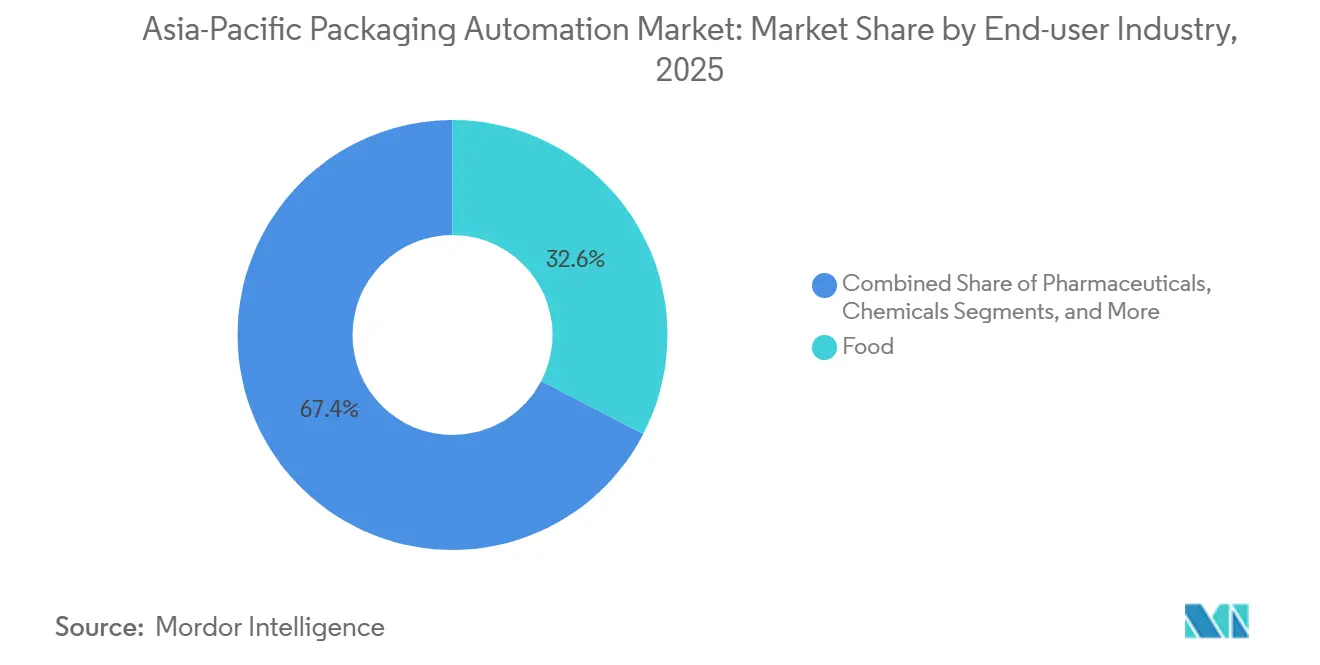

- By end-user industry, food captured 32.62% of the Asia-Pacific packaging automation market revenue share in 2025. In contrast, Pharmaceutical is expected to expand at an 8.67% CAGR during the forecast period.

- By country, China accounted for 41.36% of the 2025 revenue share in the Asia-Pacific packaging automation market. However, India is projected to grow at a 9.59% CAGR from 2026 to 2031.

Asia-Pacific Packaging Automation Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising labour costs and shrinking working-age population in APAC | +1.8% | Japan, South Korea, Singapore, and spillover to China's coastal regions | Medium term (2-4 years) |

| Explosive B2C/B2B e-commerce parcel volumes requiring high-speed fulfilment | +2.1% | China, India, Southeast Asia | Short term (≤ 2 years) |

| Government Industry 4.0 subsidy programs | +1.2% | Malaysia, Singapore, Thailand, Hong Kong, emerging Vietnam, and Indonesia | Medium term (2-4 years) |

| Sustainability-driven switch to lightweight flexible packs | +0.9% | Japan, Australia, South Korea, region-wide brand owners | Long term (≥ 4 years) |

| AI-enabled predictive maintenance lowers unplanned downtime | +0.7% | Japan, South Korea, Singapore, China, tier-1 cities | Medium term (2-4 years) |

| Adoption of collaborative robots for secondary and end-of-line tasks | +0.6% | Automotive and electronics hubs across the Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Explosive B2C/B2B E-Commerce Parcel Volumes Requiring High-Speed Fulfilment

Parcel numbers across the Asia-Pacific region surged in 2025, prompting distribution centers to install smarter sortation and adaptive packing cells that process various stock-keeping units at line speeds exceeding 1,200 parcels per hour. China shipped more than 800,000 automated packing units, and Southeast Asia nearly doubled its capacity, illustrating the scale at which the Asia-Pacific packaging automation market responds to the surge in online retail. Retailers are adopting machine-vision stations that reduce void fill, decrease corrugated consumption, and enhance dimensional weight compliance. Amazon’s regional roll-out of robotic packing arms now achieves 99.92% cube optimization accuracy, which trims last-mile freight costs.[1]Amazon Robotics, “Advanced Packaging Automation Systems Deployment,” amazon.com These installations require open-interface controllers that are compatible with warehouse execution systems, reinforcing the move toward PackML and OPC UA standards. As same-day delivery gains ground, quick-swap tooling and modular conveyors become non-negotiable, keeping the Asia-Pacific packaging automation market on a high-growth trajectory.

Government Industry 4.0 Subsidy Programs

Targeted incentives continue to lower adoption barriers for small and mid-size enterprises. Malaysia’s RM 200 million (USD 44.4 million) automation fund covers up to 40% of qualifying investments, while Singapore co-finances advanced manufacturing pilots under its transformation map. Japan backs cross-border robotics platforms that align ASEAN factories with domestic component suppliers. Thailand and Indonesia embed automation grants into broader economic corridors, making capital available for vision-guided packing cells in newly established industrial parks. Program managers emphasize the transfer of knowledge, so integrators receive vouchers to train plant staff on servo tuning and line balancing. This blended financial-technical support accelerates the Asia-Pacific packaging automation market, particularly in regions where factory payrolls exceed USD 7,000 per worker annually.

Rising Labour Costs and Shrinking Working-Age Population in Asia-Pacific

Japan’s workforce contracted by 2.1% per year, resulting in an 8% increase in average manufacturing wages in 2024 and prompting factories to seek labor substitution rather than relocation. South Korea registers similar trends, with posted vacancies for secondary packing technicians remaining open twice as long as in 2023. China’s coastal hubs are facing a surge of younger employees migrating to service jobs, which is weakening the availability of skills for shift-based packaging work. Automated case erectors, palletizers, and collaborative cappers fill these gaps, yielding fast labor savings. Talent deficits also encourage the use of remote monitoring platforms, which enable one engineer to supervise multiple lines across provinces, thereby preserving productivity as the Asia-Pacific packaging automation market continues to expand.

Sustainability-Driven Switch to Lightweight Flexible Packs Needs New Automation

Brand owners are pressing for a 25% reduction in greenhouse gas emissions by 2030, and lightweight mono-material films are pivotal to achieving these targets. Switching from rigid to flexible formats reduces resin use by up to 70%, yet demands precise tension control, gentle product handling, and high-integrity seal bars. Japanese regulations mandate a 30% recycled content threshold for many consumer packs, and Australia’s National Packaging Targets stipulate 100% recyclable formats by 2026. Equipment builders respond with low-inertia sealing jaws and motion-profiled feeders that prevent film stretch, underscoring why sustainability drives every investment decision in the Asia-Pacific packaging automation market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capex for multi-line turnkey systems | -1.4% | SMEs across emerging ASEAN and India | Short term (≤ 2 years) |

| Scarcity of systems-integration talent across emerging ASEAN markets | -0.8% | Vietnam, Indonesia, Philippines, Thailand | Medium term (2-4 years) |

| Lack of cross-vendor interoperability standards | -0.6% | Region-wide multi-vendor factories | Long term (≥ 4 years) |

| Semiconductor-driven PLC/servo lead-time volatility | -0.9% | APAC plants reliant on Taiwan and South Korea fabs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex for Multi-Line Turnkey Systems

Complete packaging lines that combine filling, cartooning, palletizing, and stretch wrapping can cost USD 2 million to USD 5 million, stretching SME balance sheets, particularly where local lending rates sit above 9%. While Equipment-as-a-Service plans reduce entry fees by 60%, uptake remains limited outside tier-1 cities. Currency swings add risk; U.S. tariffs of 18% on Chinese goods drive inflate landed cost structures. Governments’ grant ceilings seldom cover auxiliary expenses, such as power upgrades or clean-room modifications, which dampens orders even as the Asia-Pacific packaging automation market sees strong long-term fundamentals.

Semiconductor-Driven PLC/Servo Lead-Time Volatility

Persistent chip shortages stretch controller-led times to 16 weeks, forcing integrators to redesign cabinets around available components and carry larger inventories. Taiwan and South Korea fabs dominate supply, so geopolitical risk factors into procurement strategies. Machine builders respond by qualifying dual-sourced motion cards, yet commissioning delays still slow plant start-ups. These bottlenecks shave nearly a full point off the Asia-Pacific packaging automation market CAGR in the near term, although normalizing wafer capacity by 2028 should restore predictable delivery cycles.

Segment Analysis

By Business Type: E-Commerce Retailers Reshape Investment Priorities

The Asia-Pacific packaging automation market size attributed to B2C e-commerce retailers is rising at a 9.17% CAGR. Manufacturers still captured 46.25% of revenues in 2025 as they updated legacy lines, but retail fulfillment centers now order right-sizing pack machines that cut void fill and freight expense. Modular sorters process mixed stock-keeping units and hand off to vision-guided tapers within the same footprint, catering to omnichannel workflows. Surge events create demand peaks that only automated packing cells with instantaneous format changeovers can effectively absorb. Retailers link package data directly to transport booking systems, reducing handover delays and supporting same-day commitments that enhance customer satisfaction.

Next-generation labelers apply dynamic routing codes, allowing parcels to self-sort at cross-docks, thereby eliminating manual induction stages. Collaborative robots capably erect mailers and insert invoices, freeing staff for exception handling. The Asia-Pacific Packaging Automation Market, therefore, migrates from classic conveyor islands to cloud-orchestrated nodes that broadcast performance data to centralized control rooms. Manufacturers emulate retail models, adding direct-to-consumer channels and investing in compact cartoners that fit within constrained brownfield footprints. This convergence of retail and manufacturing workflows cements robust demand across the wider Asia-Pacific packaging automation market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Product Type: Palletizing Systems Move Up the Agenda

Filling machines held a 28.84% share of the Asia-Pacific packaging automation market size in 2025. Yet, the palletizing segment is forecast to grow at the fastest rate, with an 8.97% CAGR, as factories seek to automate labor-intensive end-of-line operations. Programmable layer patterns help load stability for taller trucks, reducing transport costs. Articulated robots equipped with servo grippers handle diverse case sizes without requiring mechanical change parts, easing the shipping of mixed stock prevalent in e-commerce.

Vision-guided depalletizes upstream also slashes inbound receiving times, creating holistic flow from raw material entry to dispatched pallet. Component prices for compact six-axis arms fell by 14% between 2023 and 2025, expanding the buyer base. Film wrapping units coupled to automatic corner post applicators reinforce sustainability credentials by cutting film gauge. Case packers equipped with AI defect rejection modules achieve a 99.8% pack integrity rate, meeting the rising expectations of consumers. The Asia-Pacific packaging automation market is thereby shifting toward integrated, turnkey cells rather than isolated machine upgrades.

By End-user Industry: Pharmaceuticals Traceability Accelerates Spend

Food applications generated 32.62% of 2025 revenues as continuous motion fillers and hygienic designs remain essential. Pharmaceutical spending is now expanding at an 8.67% CAGR, reflecting the implementation of strict track-and-trace rules that pair serialization printers with tamper-evident sealers. Vial packers monitor in-nest temperature to protect biologics shipped through regional cold chains. Regulatory auditors demand electronic batch records, so packaging execution software integrates seamlessly with enterprise resource planning systems, adding analytics licenses that embed recurring revenue into the Asia-Pacific packaging automation market.

Cosmetics and household chemical producers deploy gentle handling pick-and-place units to avoid surface marring on glossy finishes. Chemical plants install flameproof sealers compliant with ISO 14001 to package aggressive reagents. Beverage brands pursue canning lines rated at 120,000 units per hour, yet require agile filler blocks capable of switching from carbonated to still beverages within 45 minutes. The cross-pollination of pharmaceutical validation techniques into food allergen control drives overall technology sophistication upward across the Asia-Pacific packaging automation market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

China remains the anchor of the Asia-Pacific packaging automation market, accounting for 41.36% of the 2025 revenue share and showcasing a deep integration of AI-enabled predictive maintenance frameworks. Coastal regions are pivoting toward fewer operators per line, future-proofing facilities against labor scarcity. Local equipment manufacturers are now exporting servo-controlled flow wrappers to Latin America, indicating a rising level of competitiveness.

India’s acceleration hinges on Digital India infrastructure and consumer appetite for fast delivery. Local integrators collaborate with global robot OEMs to offer variant-rich turnkey solutions adapted to warm climates, shielding drives and PLCs from voltage fluctuations. Pharmaceutical exporters in Hyderabad install serialization modules that meet the requirements of the U.S. Drug Supply Chain Security Act, thereby elevating automation content.

Southeast Asia forms the frontier battleground. Vietnam’s industrial clusters receive tax holidays that spur multinational relocations. Thailand’s Eastern Economic Corridor channels capital into packaging upgrades, while Malaysia’s automation fund offsets upfront expenditures for SMEs. Still, the scarcity of certified PackML engineers slows multi-vendor line validation. The Asia-Pacific packaging automation market thus, balances clear top-line momentum with execution complexity across diverse regulatory and talent landscapes.

Competitive Landscape

Competition is moderate fragmentation. Krones deepened its process know-how through a 60% stake in GHS Separationstechnik and full acquisition of Can Systems Worldwide, securing niche capabilities in continuous solid-liquid separation and aluminum can depalletizing.[2]Krones AG, “Strategic Acquisitions Strengthen Technology Portfolio,” krones.com Syntegon utilizes AI analytics to predict seal-bar wear, resulting in a 20% reduction in unplanned downtime. Meanwhile, ABB scales modular cell libraries, which reduce configuration time for small-batch orders.

Regional challengers capitalize on flexible film expertise, offering delta robots with vacuum pitch control tuned for pouch snacks. Chinese suppliers package cobots and conveyors under a single warranty, improving value perception among cost-sensitive buyers. Equipment-as-a-Service now accounts for 15% of Krones’ regional bookings, signaling appetite for subscription models. Universal Robots expanded training centers in Ho Chi Minh City and Jakarta, addressing integrator shortages and widening its installed base.

Component volatility tests supply chains. ABB dual-sources critical drives, building safety stock in Singapore to buffer clients against semiconductor shocks. Mitsubishi Electric equips its servo controllers with built-in self-diagnostics, and Omron pushes PackML kits that standardize code across machine brands, alleviating interoperability pain.[3]Omron Corporation, “Industrial Automation and Robotics Solutions,” omron.com This blend of hardware resilience and software standardization influences purchasing criteria across an increasingly sophisticated Asia-Pacific packaging automation market.

Asia-Pacific Packaging Automation Industry Leaders

-

Amcor plc

-

Krones AG

-

Syntegon Technology GmbH

-

Sidel Group

-

Mitsubishi Electric Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- September 2025: Krones AG acquired 60% of GHS Separationstechnik and 100% of Can Systems Worldwide to expand separation and beverage packaging capabilities.

- September 2025: Japan’s Ministry of Economy, Trade, and Industry selected Industry Alpha to develop an ASEAN robot management system for packaging lines.

- August 2025: The Japanese government funded autonomous delivery robot projects led by Toyota, Panasonic, Rakuten, and Hakobot to enhance end-to-end e-commerce logistics.

- July 2025: Epson launched a four-company collaboration to automate food box packing for meal kit providers across the APAC region.

Asia-Pacific Packaging Automation Market Report Scope

The scope of the study on the Asia-Pacific Packaging Automation Market encompasses an in-depth analysis of automated packaging solutions deployed across various industries, including food, pharmaceuticals, cosmetics, household, beverages, chemicals, warehousing, and 3PL, as well as other end-user industries, within the Asia-Pacific region.

The study examines technological advancements, including IoT-enabled smart packaging lines, AI-driven quality inspection, and energy-efficient systems, and their impact on operational efficiency and cost reduction. Regional coverage spans major economies, including China, India, Japan, South Korea, Australia, and the Rest of the Asia-Pacific, with a focus on adoption trends, regulatory compliance, and investment patterns in automation infrastructure.

The Asia-Pacific Packaging Automation Market Report is Segmented by Business Type (B2B E-Commerce Retailers, B2C E-Commerce Retailers, Omni-Channel Retailers, Wholesale Distributors, and Manufacturers), Product Type (Filling, Labelling, Horizontal/Vertical Pillow, Case Packaging, Bagging, Palletising, Capping, and Wrapping), End-User Industry (Food, Pharmaceuticals, Household, Beverages, Chemicals, Warehousing and 3PL, and Other End-user Industries), and Country. The Market Forecasts are Provided in Terms of Value (USD).

By Business Type

| B2B e-Commerce Retailers |

| B2C e-Commerce Retailers |

| Omni-Channel Retailers |

| Wholesale Distributors |

| Manufacturers |

By End-user Industry

| Food |

| Pharmaceuticals |

| Cosmetics |

| Household |

| Beverages |

| Chemicals |

| Warehousing and 3PL |

| Other End-user Industries |

By Product Type

| Filling |

| Labelling |

| Horizontal / Vertical Pillow |

| Case Packaging |

| Bagging |

| Palletising |

| Capping |

| Wrapping |

By Country

| China |

| India |

| Japan |

| South Korea |

| Australia |

| Rest of Asia-Pacific |

| By Business Type | B2B e-Commerce Retailers |

| B2C e-Commerce Retailers | |

| Omni-Channel Retailers | |

| Wholesale Distributors | |

| Manufacturers | |

| By End-user Industry | Food |

| Pharmaceuticals | |

| Cosmetics | |

| Household | |

| Beverages | |

| Chemicals | |

| Warehousing and 3PL | |

| Other End-user Industries | |

| By Product Type | Filling |

| Labelling | |

| Horizontal / Vertical Pillow | |

| Case Packaging | |

| Bagging | |

| Palletising | |

| Capping | |

| Wrapping | |

| By Country | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected value of the Asia-Pacific packaging automation market in 2031?

The market is expected to reach USD 43.21 billion by 2031, reflecting a 7.36% CAGR.

Which country will grow the fastest through 2031?

India is forecast to post the highest 9.59% CAGR, driven by the Digital India policies and the booming e-commerce sector.

Which product category currently shows the quickest uptake?

Palletizing systems lead with an 8.97% CAGR as warehouses automate end-of-line tasks.

What share of 2025 revenues did food applications generate?

Food applications accounted for 32.62% of 2025 revenues, underpinning segment leadership.

Why are semiconductor shortages a concern for automation?

Extended PLC and servo lead times of up to 16 weeks delay project completions and weigh on short-term growth.

How much funding does Malaysia provide for automation upgrades?

The RM 200 million (USD 44.4 million) automation fund subsidies up to 40% of eligible investments.

Page last updated on: