Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

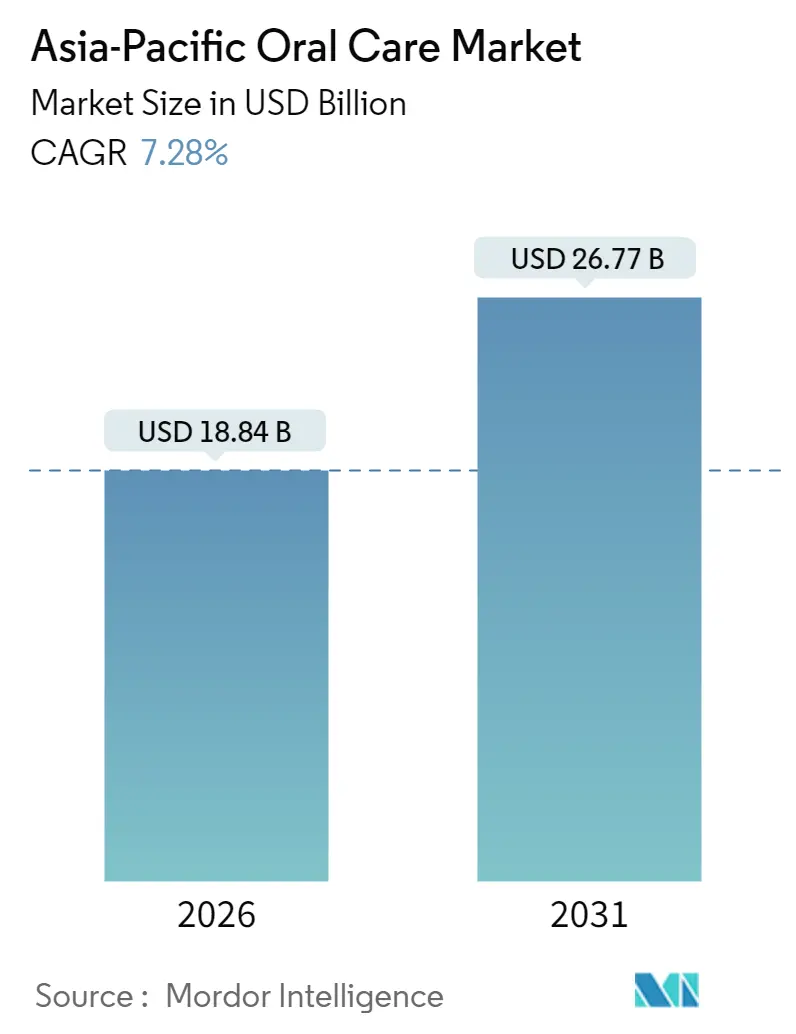

| Market Size (2026) | USD 18.84 Billion |

| Market Size (2031) | USD 26.77 Billion |

| Growth Rate (2026 - 2031) | 7.28% CAGR |

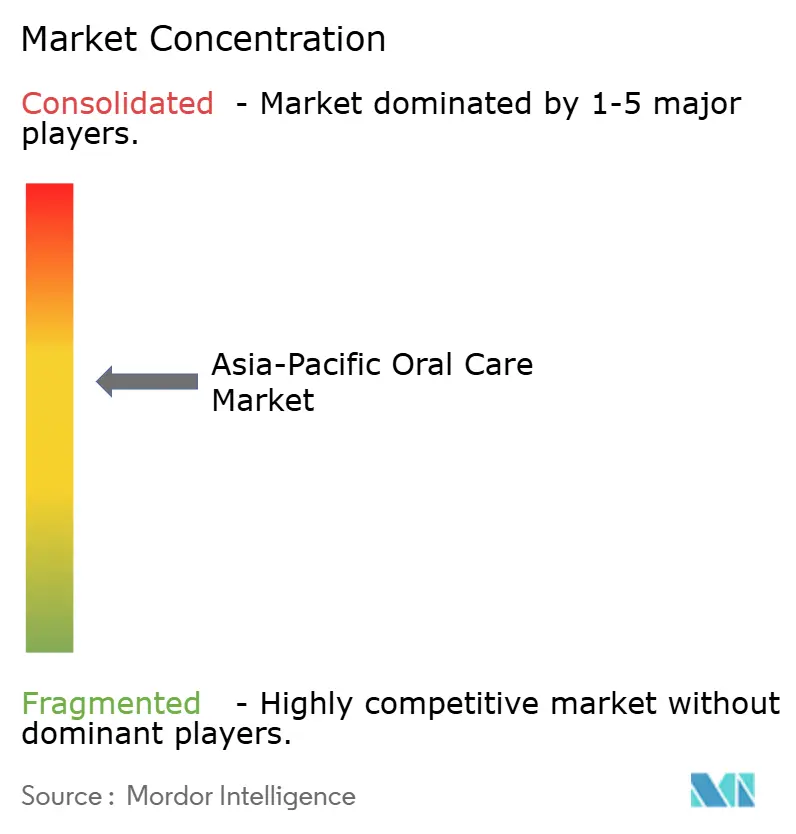

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Oral Care Market Analysis by Mordor Intelligence

The Asia-Pacific oral care market was valued at USD 17.56 billion in 2025 and estimated to grow from USD 18.84 billion in 2026 to reach USD 26.77 billion by 2031, at a CAGR of 7.28% during the forecast period (2026-2031). Increasing disposable incomes, rapid urbanization, and government-supported oral health programs are driving a shift among households from occasional treatments to regular preventive care, thereby expanding the market's reach in the Asia-Pacific region. The integration of smart technologies in electric toothbrushes, growing consumer demand for natural and Ayurvedic products, and standardized regulatory frameworks under the ASEAN Cosmetic Directive are fostering growth opportunities while reducing cross-border compliance costs. Additionally, the rise of digital commerce, particularly direct-to-consumer models that combine subscription deliveries with telehealth services, is disrupting traditional pricing structures and creating opportunities for agile competitors in the Asia-Pacific oral care market. However, traditional tooth-cleaning practices, high price sensitivity in emerging economies, and persistent safety concerns regarding synthetic ingredients are limiting the adoption of premium products in lower-income segments of the region.

Key Report Takeaways

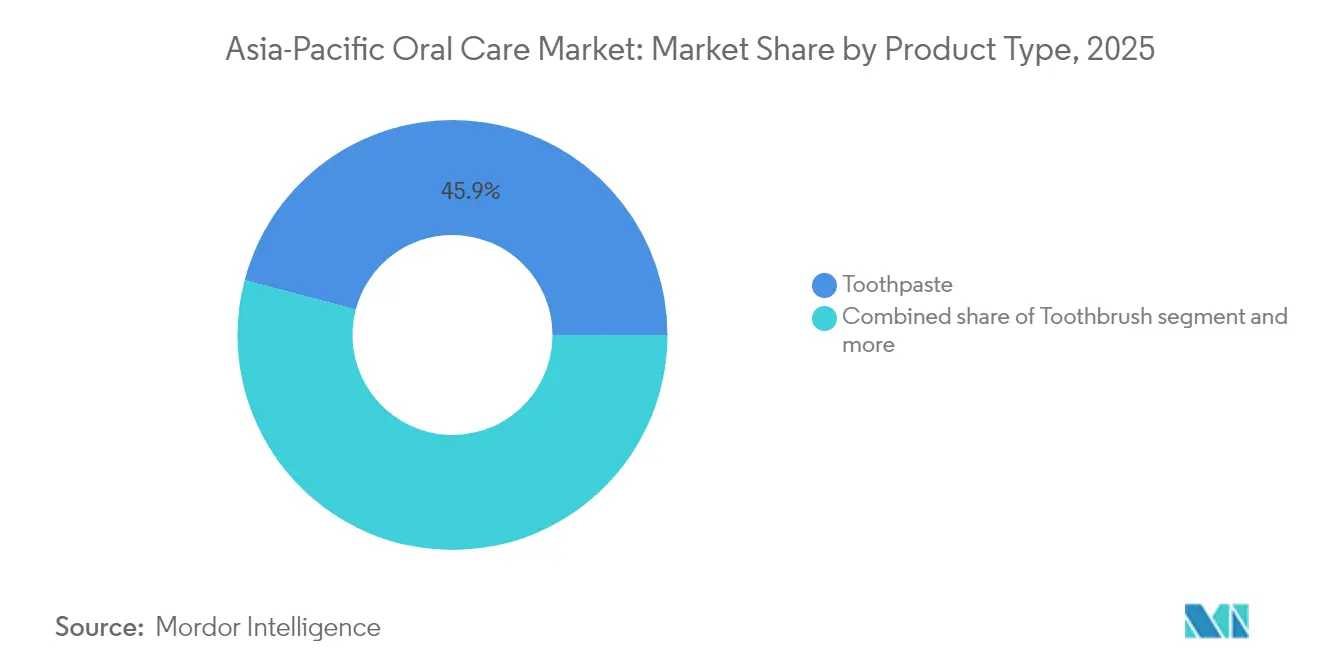

- By product type, toothpaste led with a 45.90% share of the Asia-Pacific oral care market in 2025, while toothbrushes, propelled by electric variants, are forecast to expand at a 7.66% CAGR through 2031.

- By ingredient, conventional formulations accounted for 89.80% of the Asia-Pacific oral care market share in 2025, whereas natural and organic products are projected to register an 8.17% CAGR to 2031.

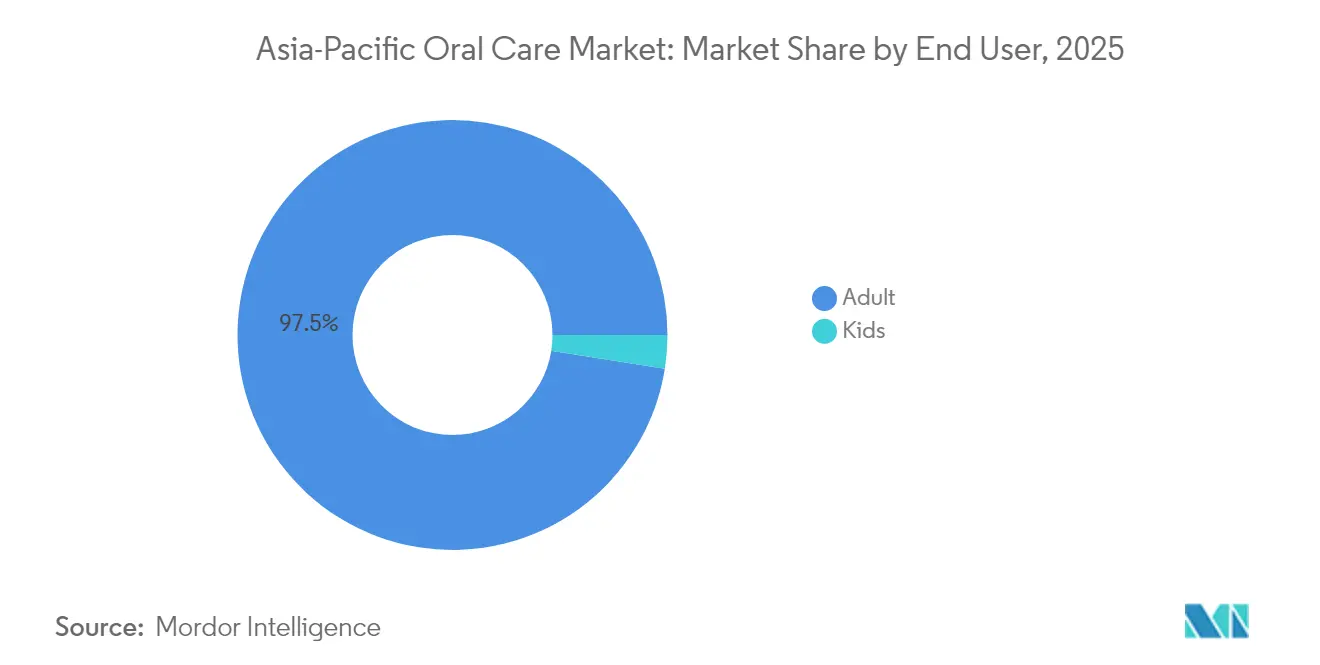

- By end user, adults represented 97.50% of demand in 2025; kids’ oral-care products are advancing at a 7.59% CAGR on the back of school-based screening programs.

- By distribution channel, supermarkets and hypermarkets held 35.10% of the Asia-Pacific oral care market size in 2025, yet online retail is the fastest-growing channel with an 8.38% CAGR outlook.

- By geography, China commanded 33.90% revenue share in 2025, whereas India is forecast to deliver the fastest national growth at a 7.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Oral Care Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising oral-health awareness and preventive-care adoption | +1.2% | Global, with strongest gains in India, Indonesia, Thailand | Medium term (2-4 years) |

| Growing disposable incomes and urbanization | +1.5% | China, India, Southeast Asia urban corridors | Long term (≥ 4 years) |

| Integration of smart technologies in electric toothbrush | +0.9% | China, Japan, South Korea, Australia | Short term (≤ 2 years) |

| Growing prevalence of dental diseases creating demand | +1.3% | Global, acute in South Asia and Southeast Asia | Long term (≥ 4 years) |

| Elevated consumer demand for natural and herbal oral care products | +1.1% | India, China, Thailand | Medium term (2-4 years) |

| Increasing penetration of digital marketing and influencer endorsements | +0.8% | Urban centers across Asia-Pacific, spill-over to tier-2 cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising oral-health awareness and preventive-care adoption

Government-led dental screening programs in schools, along with WHO-supported oral health initiatives, are encouraging a shift from occasional treatments to regular preventive care. India's National Oral Health Programme has expanded its scope, requiring biannual check-ups and fluoride varnish applications for schoolchildren, thereby promoting early intervention. In 2024, the Indian government allocated INR 858 Crores to the National Oral Health Programme, according to the Public Health Department[1]Source: Public Health Department, National Oral Health Programme", phd.maharashtra.gov.in. In Japan, the growing number of dental clinics has led to an increase in adults seeking preventive cleanings instead of emergency treatments. For example, the number of dental clinics in Japan reached 66,820 in 2023, as reported by the Statistics Bureau of Japan[2]Source: Statistics Bureau of Japan, "Survey of medical institutions 2023", stat.go.jp. This change in behavior is driving demand for specialized products, such as remineralizing toothpastes, interdental brushes, and alcohol-free mouthwashes, that address issues like enamel erosion and gingival inflammation. Compliance with ISO 11609:2017 standards enhances the credibility of product efficacy claims, reducing consumer skepticism and encouraging the adoption of premium formulations.

Growing disposable incomes and urbanization

With rising per capita incomes in tier-2 and tier-3 cities across India, Indonesia, and Vietnam, households are increasingly allocating higher budgets to oral care. This shift reflects a transition from reliance on basic commodity toothpaste to adopting more comprehensive, multi-product oral care regimens. China's National Bureau of Statistics reported that, nationwide, per capita disposable income in China reached CNY 41,314 in 2024, representing a nominal increase of 5.3% compared to the previous year[3]Source: China's National Bureau of Statistics, Households' Income and Consumption Expenditure in 2024", stats.gov.cn. This upward trend in income levels has significantly influenced consumer behavior, particularly in the electric toothbrush segment, which has seen notable growth. Additionally, urbanization has played a pivotal role in exposing consumers to Western lifestyle habits and dental aesthetics, such as teeth whitening treatments and orthodontic aligners, thereby creating new revenue opportunities in adjacent markets. For instance, Indonesia's Klar, a startup specializing in aligners, successfully raised USD 4.5 million in funding in 2022. This development highlights how rising incomes are unlocking demand for discretionary oral health services that were previously inaccessible to many consumers.

Integration of smart technologies in electric toothbrush

AI-powered electric toothbrushes, now integrated with advanced features such as pressure sensors, real-time plaque mapping, and mobile app connectivity, are transforming the premium market segment. These innovations are setting new benchmarks for oral care technology. Oclean, a Chinese company holding an impressive portfolio of 519 global patents, exemplifies how technological advancements can challenge and potentially surpass well-established Western brands in this space. In 2024, Procter and Gamble introduced its Oral-B iO Series 10, which utilizes a combination of oscillating, rotating, and pulsating technology, enhanced by AI-guided brushing zones to optimize oral hygiene. Clinical studies conducted in South Korea demonstrated that telemonitoring toothbrushes significantly improved plaque removal compared to manual brushing, providing robust evidence that insurers and employers could leverage to encourage the adoption of smart toothbrushes. Additionally, Bluetooth-enabled toothbrushes collect valuable behavioral data, enabling brands to deliver personalized product recommendations. This approach not only enhances user experience but also creates recurring revenue opportunities for companies, extending beyond the initial hardware sales.

Elevated consumer demand for natural and herbal oral care products

India is leading the transition toward natural oral care, with a significant increase in toothpaste launches that prominently feature herbal and Ayurvedic ingredients. This trend is driven by growing consumer preference for products containing traditional components like neem, clove, and miswak, which are widely regarded for their effectiveness and minimal side effects. In China, the implementation of the GB 8372-2017 standard has introduced a requirement for full disclosure of all toothpaste ingredients. Under the classification of toothpaste as a special cosmetic, regulated by the NMPA, this standard has accelerated the reformulation of products to include plant-based surfactants and natural sweeteners such as stevia. In 2024, Himalaya Wellness and Dabur achieved organic certifications for their herbal toothpaste ranges. This accomplishment not only supports premium pricing strategies but also facilitates their entry into export markets like Australia and New Zealand, where consumer demand for clean-label products is deeply ingrained. Additionally, in Japan and South Korea, Hydroxyapatite, a biomimetic mineral, is increasingly being used as a substitute for fluoride in toothpaste formulations. Clinical trials have demonstrated that Hydroxyapatite provides comparable remineralization benefits to fluoride while eliminating the ingestion risks for children, making it a safer alternative.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prevalence of traditional tooth cleaning methods | -0.6% | Rural India, Indonesia, Thailand, Vietnam | Long term (≥ 4 years) |

| Limited access to professional dental care | -0.5% | Rural and remote areas across Asia-Pacific | Long term (≥ 4 years) |

| Concern over chemical ingredients used | -0.4% | Urban China, India, Australia, New Zealand | Medium term (2-4 years) |

| Price sensitivity in emerging economies | -0.7% | India, Indonesia, Philippines, Vietnam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Prevalence of traditional tooth cleaning methods

In rural India, Indonesia, and parts of Southeast Asia, cultural traditions and economic factors continue to drive the preference for miswak sticks, charcoal powder, and salt-based scrubs over commercial toothpaste. Many households in these regions rely on neem twigs or ash for their daily oral hygiene routines, viewing these options as both natural and cost-effective. This deeply ingrained behavior creates significant barriers to market growth, particularly in areas with high population density but low penetration of commercial oral care products. Although some brands, such as Dabur, have attempted to bridge the gap by incorporating traditional ingredients like clove and camphor into their products (e.g., Dabur's Red Paste), the transition from free or nearly free methods to paid alternatives remains a challenge. Achieving this shift requires sustained efforts, including comprehensive educational campaigns to raise awareness about the benefits of commercial products. Additionally, companies must address logistical challenges by establishing distribution networks that can effectively reach remote villages, where retail infrastructure is often underdeveloped or entirely absent.

Price sensitivity in emerging economies

Price sensitivity in emerging Asia-Pacific economies, such as India, Indonesia, and parts of Southeast Asia, reduces consumers' inclination to purchase premium oral care products. Despite being aware of the benefits, consumers in these regions prioritize affordable essentials over higher-priced options like electric toothbrushes, whitening toothpastes, or natural/herbal variants. This preference slows the adoption of innovative, high-margin products. In countries like India, Indonesia, and the Philippines, households dedicate a smaller share of their budgets to oral care, creating obstacles for premiumization efforts. Electric toothbrushes priced above USD 30 remain unaffordable for most, while mid-tier toothpastes face stiff competition from unbranded local sachets sold at USD 0.10 each. Furthermore, India's goods and services tax (GST) on oral care products increases retail prices, discouraging consumers from upgrading. To address this, brands are offering smaller pack sizes and economy variants; however, this strategy compresses margins and limits investments in innovation.

Segment Analysis

By Product Type: Electric Variants Accelerate Category Growth

Toothpaste holds the largest market share at 45.90% in 2025, supported by frequent repurchases and low per-unit costs. However, growth in this category is slowing as it approaches maturity. To address this, brands are expanding their portfolios to meet the demand for natural ingredients and sustainability. At the same time, mouthwash and rinses are gaining popularity in Japan and South Korea. Consumers in these markets prefer alcohol-free formulations with probiotics and peptides, which help prevent biofilm without the discomfort associated with traditional rinses. Other dental products, such as interdental brushes and tongue cleaners, remain niche but are growing in markets with high dental awareness. For example, in Australia, where the Therapeutic Goods Administration (TGA) regulates therapeutic claims, these products are seeing increased adoption.

Between 2026 and 2031, toothbrush sales are anticipated to grow at a robust CAGR of 7.66%, marking the highest growth rate among all product types. This significant expansion is primarily attributed to the rising adoption of electric toothbrushes, which are increasingly equipped with advanced AI-powered features. These innovations, combined with a price point below USD 50, are making electric toothbrushes more accessible in key markets such as China and South Korea. Despite this shift, manual toothbrushes continue to dominate in terms of unit sales due to their affordability and widespread availability. However, their revenue contribution is showing signs of stagnation as consumers gradually transition to higher-end options like sonic and oscillating models, which offer enhanced performance and appeal to a growing preference for premium dental care solutions.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Ingredient: Natural Formulations Outpace Conventional Growth

Conventional formulations still hold 89.80% of the market share in 2025, reflecting established consumer preferences and the cost-effectiveness of synthetic ingredients. However, increasing concerns about ingredients like sodium lauryl sulfate (SLS), triclosan, and microplastics are prompting reformulations. In Japan and South Korea, fluoride is being replaced with hydroxyapatite, a biomimetic mineral. Clinical studies show that hydroxyapatite provides similar remineralization benefits without the ingestion risks associated with fluoride, particularly for children. Additionally, peptides are emerging as a solution for enamel repair, while probiotics are being adopted for their role in preventing biofilm formation. These innovations create a scientific balance between the efficacy of natural and conventional products. Compliance with ISO 11609:2017 standards ensures that natural products meet the same performance benchmarks as conventional ones, reducing the risk of greenwashing and enhancing consumer confidence.

Between 2026 and 2031, natural and organic oral care products are expected to grow at a CAGR of 8.17%, nearly twice the growth rate of conventional products. This growth is fueled by consumers increasingly examining ingredient labels and choosing plant-based alternatives. India is leading this trend, with a growing number of toothpaste launches highlighting herbal and Ayurvedic ingredients. Herbal toothpaste has become a dominant segment in India's oral care market. Brands such as Dabur and Himalaya Wellness have achieved organic certifications and are expanding exports to markets like Australia and New Zealand. In China, the GB 8372-2017 standard, which classifies toothpaste as a special cosmetic under NMPA regulation, requires full ingredient disclosure. This regulation has driven a shift toward natural surfactants and sweeteners, such as stevia, in toothpaste formulations.

By End User: Kids Segment Gains Momentum with Pediatric Initiatives

Adults constitute 97.50% of end-user demand, reflecting their greater purchasing power and wider range of product usage. Their preferences include whitening toothpastes, therapeutic mouthwashes, and electric toothbrushes. Aging populations in countries such as Japan, South Korea, and Australia are driving demand for products addressing gingival recession, root caries, and denture care. Additionally, the adult segment is increasingly integrating oral care into broader wellness routines. Brands like Oral Essentials are positioning mouthwashes as key components of self-care regimens, often incorporating essential oils and probiotics.

Between 2026 and 2031, the kids' oral care market is anticipated to grow at a significant CAGR of 7.59%, surpassing the growth of the adult segment. This expansion is driven by government-led initiatives, such as school dental programs, and the introduction of pediatric formulations free from fluoride and artificial sweeteners, which are promoting early preventive care. Events like National Children's Dental Health Month, along with school programs and government efforts, are encouraging early hygiene habits, leading to increased adoption of child-specific products. Brands are addressing this demand by offering character-themed packaging, mild flavors like strawberry and bubblegum, and low-abrasivity formulations designed to protect developing enamel.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Online Retail Disrupts Traditional Dominance

Supermarkets and hypermarkets hold the largest market share at 35.10% in 2025. Their success is supported by high foot traffic, attractive in-store promotions, and the ability to provide tactile product experiences. However, their growth is slowing as consumers increasingly prefer online channels for their convenience and competitive pricing. Drug stores and pharmacies remain crucial for therapeutic products such as high-fluoride toothpastes and prescription mouthwashes, where pharmacist consultations offer added value. Furthermore, other distribution channels, including convenience stores and direct sales, address the needs of rural and semi-urban areas with limited retail infrastructure.

Between 2026 and 2031, online retail stores are projected to experience the fastest growth among all distribution channels, with a robust CAGR of 8.38%. This significant expansion is primarily driven by evolving consumer purchasing behaviors, influenced by the rise of direct-to-consumer brands, the increasing adoption of quick commerce platforms, and the growing popularity of subscription-based models. Colgate India has reported that quick commerce platforms are growing at a faster pace compared to traditional e-commerce. These platforms leverage 10-minute delivery windows to encourage impulse purchases while effectively addressing stockout issues, making them a key driver of growth in the online retail segment.

Geography Analysis

China holds a 33.90% share of the Asia-Pacific oral care market in 2025, driven by its large urban population, extensive smartphone usage, and government regulations requiring ingredient transparency. The National Medical Products Administration (NMPA) reclassified toothpaste as a special cosmetic under GB 8372-2017, prompting brands to reformulate and creating opportunities for domestic players. The adoption of electric toothbrushes is increasing, with Oclean's 519 global patents offering features such as real-time plaque mapping and Bluetooth connectivity, appealing to tech-savvy consumers in major cities like Shanghai and Beijing.

India is projected to grow at a CAGR of 7.95% from 2026 to 2031, the fastest among major geographies. Rising disposable incomes, a preference for Ayurvedic formulations, and government-led oral health initiatives are driving demand, particularly in rural areas. Regulatory measures, including the Bureau of Indian Standards' IS 6356:2017 specification for toothpaste and the Ayush Ministry's promotion of herbal products, have strengthened domestic brands. Notably, Dabur and Himalaya Wellness obtained organic certifications in 2024. Quick commerce platforms are expanding eight times faster than traditional e-commerce, but price sensitivity remains a challenge. Many rural households continue to use neem twigs or ash for daily cleaning, limiting market growth in densely populated regions.

Japan and South Korea lead the region in per capita oral care spending, driven by aging populations, advanced dental infrastructure, and a preference for premium and therapeutic products. Brands such as Lion's Clinica Enamel Pearl and Kao's Clear Clean Premium are shifting away from fluoride, incorporating hydroxyapatite and peptides for remineralization to address parental concerns about ingestion risks. South Korea's Ministry of Food and Drug Safety (MFDS) enforces strict labeling requirements, creating barriers for new entrants and strengthening the position of established players like LG Household and Health Care and Amorepacific. Rapid urbanization and growing e-commerce adoption are evident in Southeast Asian countries such as Thailand, Indonesia, and Singapore. Meanwhile, Australia and New Zealand, regulated by the Therapeutic Goods Administration (TGA) and Food Standards Australia New Zealand (FSANZ), demonstrate strong consumer preferences for natural and sustainable products. Colgate Elixir's vegan formulation and recyclable tube resonate with environmentally conscious consumers.

Competitive Landscape

The Asia-Pacific oral care market is moderately concentrated, with Colgate-Palmolive, Procter and Gamble, and Unilever holding a significant share. However, the competitive landscape is becoming fragmented due to the emergence of direct-to-consumer disruptors and local brands. Multinational companies are employing a dual strategy: acquiring regional portfolios to manage regulatory complexities and introducing premium sub-brands to compete with D2C challengers. In 2023, Procter and Gamble expanded its Oral-B production facility in Singapore and launched the AI-powered iO Series 10 toothbrush, highlighting its focus on premiumization and smart technology to counter declining sales of manual toothbrushes.

Leading companies, including Procter and Gamble, Colgate-Palmolive, GlaxoSmithKline, Pigeon Corporation, and Unilever, are introducing products with natural benefits and investing heavily in marketing these launches. These players are leveraging opportunities in emerging markets by expanding their product portfolios to address specific needs, such as gum and plaque issues, sensitivity, and pain relief.

Rural areas in India, Indonesia, and Vietnam offer significant growth opportunities due to low penetration rates and the continued use of traditional tooth-cleaning methods. Brands that provide affordable electric toothbrushes priced under USD 30, subscription models to spread costs, and culturally relevant products, such as miswak-infused toothpastes, can attract first-time buyers. Compliance with ISO 11609:2017 for toothpaste and ISO 20126:2012 for toothbrushes ensures that new entrants meet performance standards, reducing the likelihood of product recalls and fostering consumer trust.

Asia-Pacific Oral Care Industry Leaders

-

Colgate-Palmolive Company

-

GlaxoSmithKline plc

-

Unilever Plc

-

Pigeon Corporation

-

Procter and Gamble Company

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- September 2025: Clove Oral Care has unveiled a new range of clinically tested and tailored toothpaste and toothbrushes. This introduction underscores Clove Oral Care's commitment to enhancing preventive care and promoting oral health education across India.

- December 2024: Xiaomi has introduced its latest electric toothbrush in China, featuring a sleek color display for enhanced user interaction, an impressive 180-day battery life for extended usage without frequent charging, and IPX8 waterproof certification, ensuring durability and reliability even in wet conditions.

- December 2024: Colgate has introduced its new MaxFresh range in India, aiming to enhance the oral care experience by incorporating a unique sensory element. This launch reflects the brand's commitment to innovation and meeting consumer preferences in the oral care market.

- September 2024: Colgate-Palmolive India launched its Visible White Purple toothpaste, featuring Purple optic brighteners designed to counteract yellow tones. The new product is accessible both online and in physical stores.

Asia-Pacific Oral Care Market Report Scope

By Product Type

| Toothpaste | |

| Mouthwash/Rinses | |

| Toothbrush | Electric Toothbrush |

| Manual Toothbrush | |

| Other Product Types |

By Ingredient

| Conventional |

| Natural/Organic |

By End User

| Kids/Children |

| Adult |

By Distribution Channel

| Supermarkets/Hypermarket |

| Drug Stores/Pharmacies |

| Online Retail Stores |

| Others Distribution Channel |

By Country

| China |

| Japan |

| India |

| Thailand |

| Singapore |

| Indonesia |

| South Korea |

| Australia |

| New Zealand |

| Rest of Asia-Pacific |

| By Product Type | Toothpaste | |

| Mouthwash/Rinses | ||

| Toothbrush | Electric Toothbrush | |

| Manual Toothbrush | ||

| Other Product Types | ||

| By Ingredient | Conventional | |

| Natural/Organic | ||

| By End User | Kids/Children | |

| Adult | ||

| By Distribution Channel | Supermarkets/Hypermarket | |

| Drug Stores/Pharmacies | ||

| Online Retail Stores | ||

| Others Distribution Channel | ||

| By Country | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Asia-Pacific oral care market?

It is valued at USD 18.84 billion in 2026 and is forecast to reach USD 26.77 billion by 2031.

Which country is projected to grow the fastest within the region?

India is expected to post a 7.95% CAGR through 2031 due to income gains and Ayurvedic product demand.

Which product category holds the largest share?

Toothpaste leads with 45.90% market share in 2025, buoyed by high repurchase frequency.

How quickly is online retail expanding?

Online retail is projected to grow at an 8.38% CAGR, the fastest among all distribution channels.