Market Trends of Asia-Pacific Oilfield Services Industry

This section covers the major market trends shaping the APAC Oilfield Services Market according to our research experts:

Drilling Services to Dominate the Market

Drilling services make up the biggest share of the oilfield services market, with drilling and completion services combined accounting for over 50% of the market. Moreover, the average rig count in Asia-Pacific has seen a steady increase during the past five years.

There is an ever-increasing demand for oil and gas. In order to meet the demand, it requires an increase in oilfield services for more production from existing and new wells, signifying an increase in the oilfield services market in Asia-Pacific.

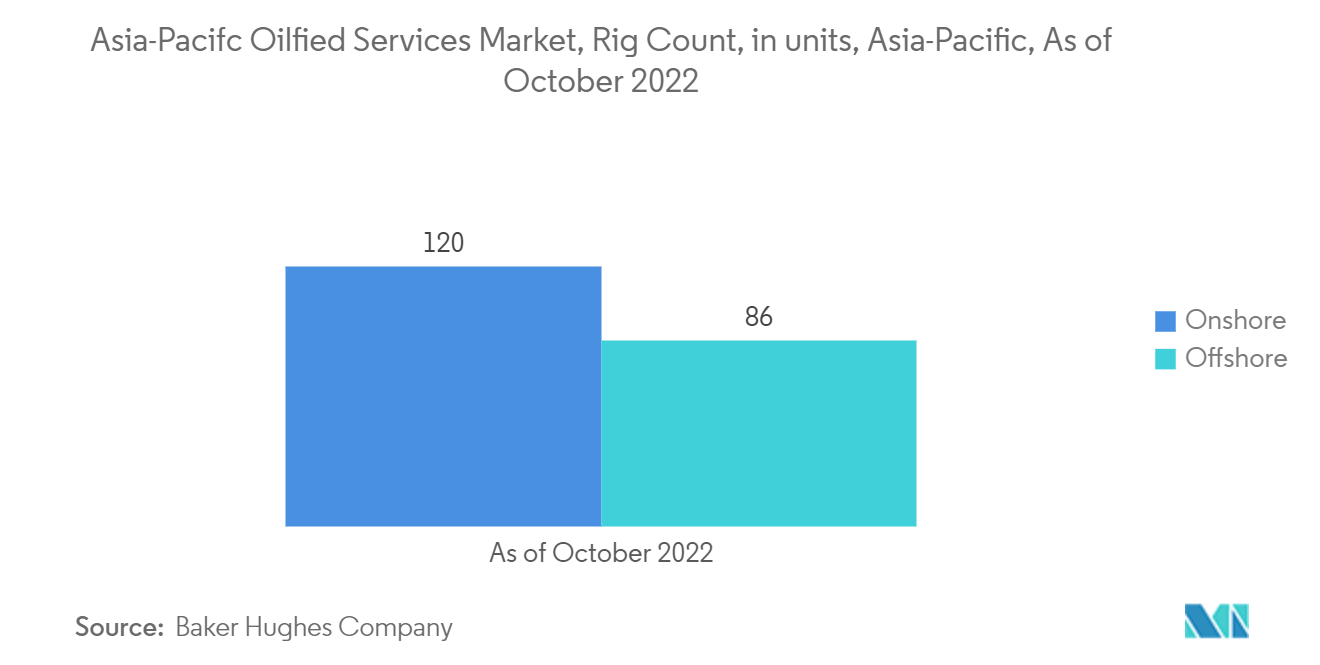

As of October 2022, Asia-Pacific hosted the third most oil and gas rigs worldwide. There were 120 onshore rigs in that region and 86 offshore.

As of November 2022, India had 78 active rigs. The country's oil production has been falling for almost a decade due to aging fields and the absence of major discoveries for years. Both state-owned and private players have been working on investment plans to raise recovery from older fields.

For instance, in April 2022, state-owned Oil and Natural Gas Corporation (ONGC) commissioned two projects costing USD 786.4 million to add 7.5 million tonnes of oil production and 1 billion cubic meters of gas output over the life of the Mumbai High fields as it doubles down efforts to raise productivity from mature and aging fields.

In September 2022, the Indian government awarded contracts for 31 oil and gas developments through the third Discovered Small Fields (DSF-3) competitive bidding round in the country's largest-ever offering of areas with known oil and gas accumulations.

In December 2021, Petronas signed two agreements regarding upstream investment in Malaysia. One agreement is a memorandum of understanding (MoU) with Petroleum Sarawak Berhad (PETROS) relating to a staggering increase of gas supplies to Sarawak, eventually raising the allocation to 1.2 billion cubic feet per day. Another one is a commercial agreement with the Sabah state government to develop Sabah's oil and gas industry.

Several offshore drilling projects in Australia, Malaysia, and Indonesia have augmented the number of activities in the region, further promulgating the demand for oilfield services.

Hence, new investments in the oil and gas industry, increasing exploration of unconventional resources, and the crude oil price stability are expected to increase the demand for the oilfield services market in Asia-Pacific.

Increasing Demand from China is Expected to Drive the Market

- China is the largest market for oilfield services in the region. The country is planning to reduce its dependency on natural gas imports and has started to exploit its shale gas reserves to meet domestic demand.

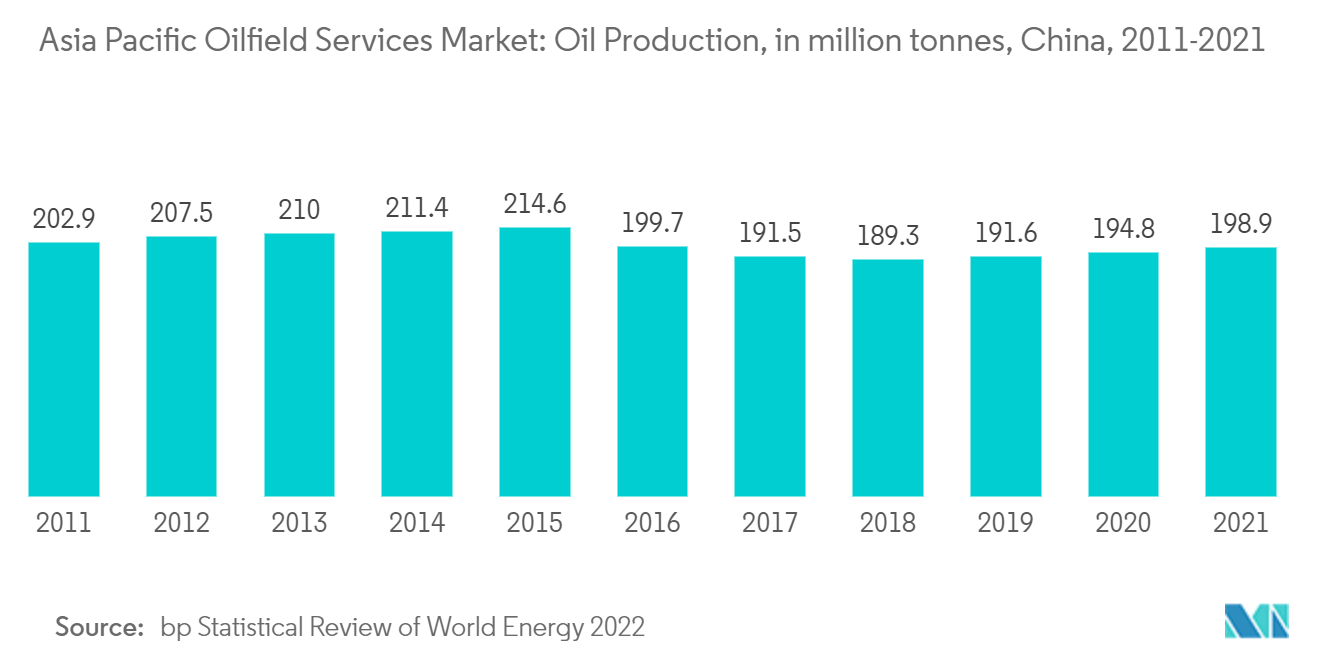

- China was the largest producer of oil in the region in 2021. Crude oil production in the country has increased by 2.1%, to 198.9 million tonnes, in 2021 from 194.8 million tonnes in 2020. The output may increase further in the forecast period and boost the China oilfield services market.

- As of November 2022, the country had around 38 offshore active rigs and no onshore active rigs. This, in turn, indicates the dominance of offshore assets in the country's upstream segment. As of 2021, more than 60% of China's offshore hydrocarbon resources are located in deepwater and ultra-deepwater areas where semi-submersibles, drillships, and other floating assets have a strong presence.

- The new reforms related to the oil and gas industry are expected to make it easier for private companies to invest in the country, which, in turn, is expected to help reduce the monopoly of state-owned companies. The growing investment by the private sector is expected to improve the oil and gas industry, in turn driving the oilfield services market in the country.

- Further, China Petroleum & Chemical Corp, also known as Sinopec, is planning its highest capital investment in history for 2022. echoing the call for energy companies to raise production. Sinopec was estimated to have spent USD 31.1 Billion in the upstream oil and gas segment, especially the crude oil bases in Shunbei and Tahe fields, and natural gas fields in Sichuan province and the Inner Mongolia region.

- In January 2022, China National Offshore Oil Corporation (CNOOC) announced net production targets for 2023 and 2024, estimated to be 640 million to 650 million barrels of oil equivalent and 680 million to 690 million barrels of oil equivalent, respectively. The company also announced its capital expenditure for 2022 is budgeted at RMB 90 billion (over USD 14 billion) to RMB 100 billion (over USD 15.6 billion), while the capital expenditures for exploration, development, production, and others will account for approximately 20%.

- In October 2022, Sinopec discovered a new shale gas reserves in the Jinshi 103HF exploratory well deployed in the Sichuan Basin, With a daily natural gas production reaching 258,600 cubic meters and an evaluated resource capacity of 387.8 billion cubic meters. The discovery represents a significant breakthrough for China's shale gas exploration, and it is the first discovery in the Cambrian Qiongzhusi Formation. This discovery has significantly increased shale gas reserves and will enhance shale gas exploration and production in the Sichuan Basin.

- Moreover, owing to air pollution and environmental concerns, the country is employing policies to increase the share of gas, and reduce the share of coal in the total energy mix. Hence, with increased exploration and production activities, supported by government initiatives, China is expected to drive the demand for oilfield services in Asia-Pacific.