Asia-Pacific Oat Milk Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

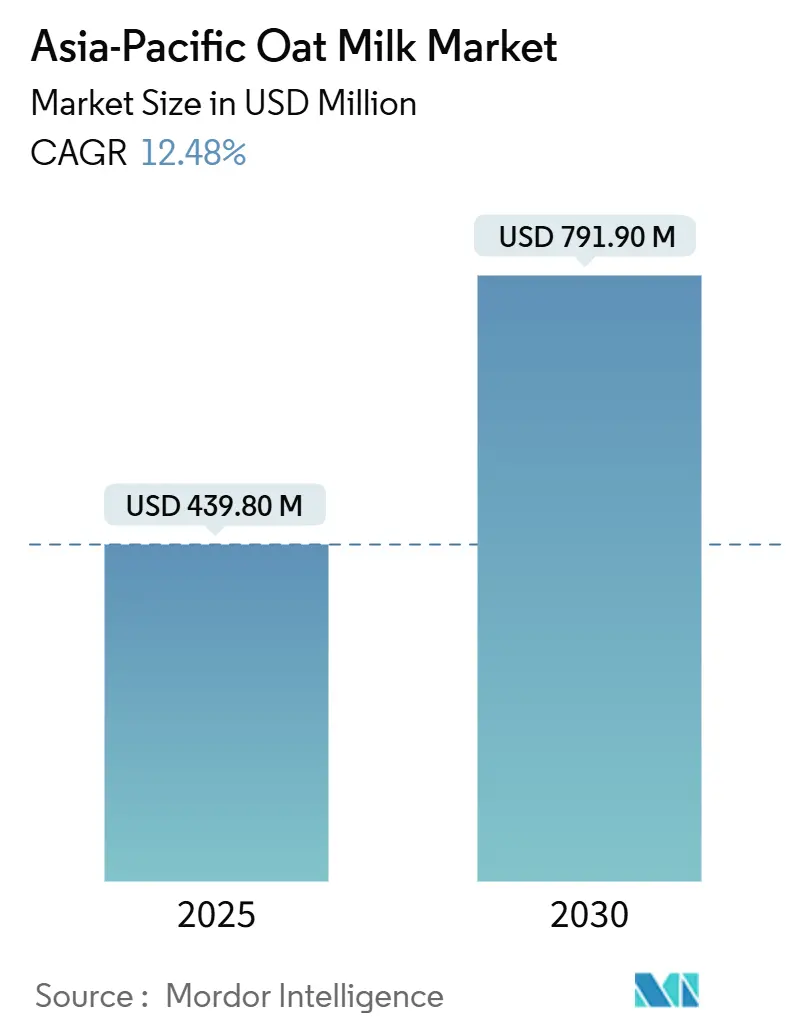

| Market Size (2025) | USD 439.80 Million |

| Market Size (2030) | USD 791.90 Million |

| Growth Rate (2025 - 2030) | 12.48% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Oat Milk Market Analysis by Mordor Intelligence

The Asia-Pacific oat milk market is expected to reach USD 439.80 million in 2025 and is projected to grow to USD 791.90 million by 2030, registering a CAGR of 12.48%. This growth highlights a shift in consumer preferences in the region, driven by factors such as lactose intolerance, environmental concerns, and the increasing demand for plant-based nutrition. The rising prevalence of lactose intolerance has led consumers to seek dairy alternatives, while growing awareness of the environmental impact of dairy farming has further boosted the demand for plant-based options like oat milk. Additionally, the nutritional benefits of oat milk, including its fiber content and suitability for vegan diets, have contributed to its popularity. However, challenges related to affordability and taste perception persist, as oat milk is often priced higher than traditional dairy milk, and some consumers remain hesitant due to differences in taste.

Key Report Takeaways

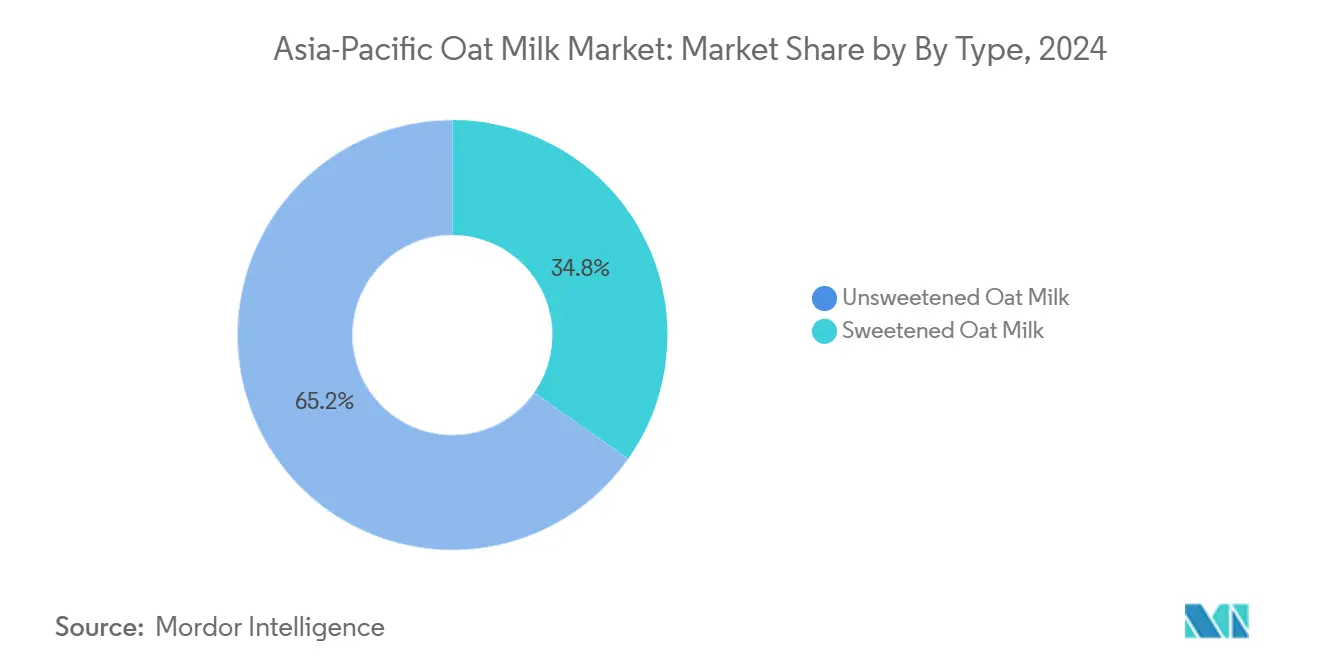

- Unsweetened oat milk commanded 65.24% share of 2024, while sweetened variants will post the fastest segment growth at 13.67% CAGR through 2030.

- Un-flavoured formats occupied 72.06% of 2024 sales, yet flavoured oat milk is forecast to advance at a 13.86% CAGR to 2030.

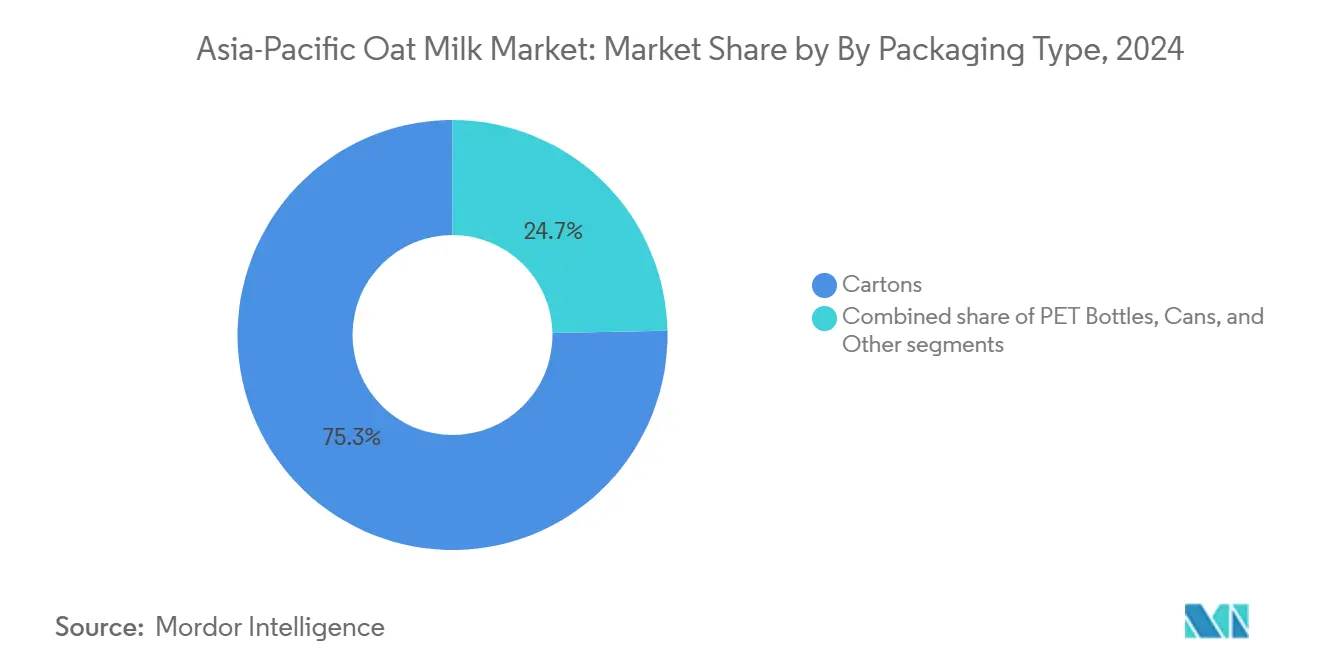

- Carton packaging secured 75.32% share in 2024; cans represent the quickest-rising format with a projected 12.99% CAGR, propelled by single-serve demand in South Korea and Japan.

- Off-trade channels contributed 91.25% of 2024 revenue; on-trade venues are expected to widen at a 14.01% CAGR as barista-grade formulations deepen penetration into café menus.

- China generated 38.65% of 2024, whereas Indonesia is poised for the fastest national growth at a 14.27% CAGR through 2030, signaling Southeast Asia’s growing weight in the Asia-Pacific oat milk market.

Asia-Pacific Oat Milk Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High lactose intolerance rates | +2.3% | China, Japan, South Korea, Southeast Asia | Long term (≥ 4 years) |

| Shift to plant-based and vegan diets | +2.1% | Urban centers across China, Japan, Australia, Singapore | Medium term (2-4 years) |

| Product innovations, such as new flavors, fortified options, and others | +1.8% | With early adoption in Japan, Australia, Singapore | Short term (≤ 2 years) |

| Expansion of foodservice channels and appeal in cafes | +1.6% | China, Indonesia, Australia, Japan | Medium term (2-4 years) |

| Environmental sustainability attracts buyers | +1.4% | Australia, Japan, Singapore, urban China | Long term (≥ 4 years) |

| Investments in local production and sustainable sourcing | +1.2% | Australia, New Zealand, China, Indonesia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High lactose intolerance rates

A significant portion of Asia's population experiences lactose malabsorption, establishing a consistent demand for dairy alternatives that conventional milk cannot fulfill. This physiological factor explains why oat milk adoption in the region skips the "trial and curiosity" phase observed in Western markets, instead addressing a critical nutritional need. Indonesia's government anticipates dairy demand to increase from 4.2 million metric tons in 2024 to 5.3 million metric tons in 2025, driven by a free nutritious meals program [1]Source: US Department of Agriculture, “Indonesia: Dairy and Products Annual,” fas.usda.gov. However, the prevalence of lactose intolerance simultaneously drives demand for plant-based substitutes. Oatly’s success in Greater China was partly attributed to positioning oat milk as a digestive-friendly option rather than solely a lifestyle product, effectively appealing to consumers who experience discomfort from dairy consumption.

Shift to plant-based and vegan diets

While consumer awareness of plant-based foods in the Asia-Pacific region is widespread, regular consumption remains limited, highlighting a significant gap between awareness and adoption. According to data published by ProVeg International in June 2024, 98% of Chinese consumers indicated they would consume more plant-based foods after being informed about the health benefits of adopting a plant-based diet[2]Source: ProVeg International, “Most people in China will eat more plant-based food when told of the benefits, survey finds,” proveg.org. Affordability and taste parity are essential to bridging this gap, as price sensitivity remains a key barrier. This indicates that local production and achieving economies of scale will be crucial in determining whether brands can capture the mass market or remain confined to premium niches. The rise of flexitarian diets, where consumers reduce but do not eliminate animal products creates a larger addressable market than strict veganism, and oat milk's neutral flavor profile positions it as a versatile ingredient in both sweet and savory applications

Product innovations, such as new flavors, fortified options, and others

Indian dairy and grocery brand Country Delight has launched a plant-based milk alternative under the name Oat Beverage. The product is made from Australian oats and is free from preservatives, chemical additives, and added sugars. It is also free of soy and nuts and is produced in an allergen-controlled facility to minimize the risk of cross-contamination. This milk alternative is designed to meet the increasing demand for dairy-free products among lactose-intolerant individuals and health-conscious consumers. Nestle Malaysia has introduced its Nestle Goodness brand of plant-protein beverages, designed to meet changing dietary preferences with Halal-certified, lactose-free, and vegan-friendly options. The beverage features a natural creamy texture and sweetness derived from hydrolysed oats and is enriched with micronutrients such as calcium and vitamins B2, D, and B3. It serves as a nutritious and flavorful alternative to dairy milk. Nestle Goodness is available in two variants: Dairy-Free Oat and Dairy-Free Almond & Oat. Flavor innovations tailored to regional preferences, such as matcha, hojicha, ube, pandan, yuzu, and calamansi, have transitioned from niche café offerings to mainstream product lines. Brands have recognized that localization encourages trial among consumers who may be hesitant about "Western" plant-based products.

Expansion of foodservice channels and expand appeal in cafes

In September 2024, Luckin Coffee announced the launch of its Oat Milk Series in Singapore, featuring the Oat Milk Latte and Oat Shakerato, both made with OATLY Barista Edition Oat Milk. This series caters to consumers seeking plant-based or lactose-free options, providing a flavorful coffee experience without compromising quality. Shanghai ranks first globally in the number of cafes, with 9,553 coffee shops as of the end of 2023, according to the State Council Information Office of China [3]Source: State Council Information Office of China, “China's coffee boom — next big opportunity for global brands,” scio.gov.cn. The increasing number of cafes, coupled with the rising popularity of veganism, is driving demand for plant-based milks, such as oat milk, in foodservice establishments. The on-trade channel not only demonstrates volume growth but also offers a premiumization opportunity, as cafes often charge higher prices for oat milk lattes compared to dairy-based options. This provides operators with a margin incentive to promote plant-based alternatives.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense competition from established alternatives like soy and almond milk | -1.5% | China, Japan, Australia, Southeast Asia | Medium term (2-4 years) |

| Supply chain issues in sourcing and processing oats | -1.2% | Indonesia, Malaysia, Thailand, India | Short term (≤ 2 years) |

| Perception of inferior taste or texture compared to dairy or other plant milks | -0.9% | China, Japan, South Korea, India | Medium term (2-4 years) |

| Regulatory hurdles and production complexities | -0.8% | Indonesia, Malaysia, Thailand, India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intense competition from established alternatives

Soy milk has maintained a dominant position in the Asia-Pacific plant-based beverages market for decades. Companies such as Vitasoy International and Yili Industrial Group leverage extensive distribution networks and strong brand recognition, presenting challenges for oat milk entrants. These new entrants must focus on differentiation rather than direct substitution to gain market share. Almond milk, while less established than soy milk, attracts consumers seeking lower-calorie options and has benefited from earlier marketing efforts. However, trial purchases do not always lead to repeat purchases, and oat milk faces competition not only from dairy but also from soy, almond, coconut, and rice milk. Moreover, price parity remains a challenge, as oat milk continues to be sold at a noticeable premium compared to soy milk in markets such as China and Indonesia, restricting its adoption primarily to affluent urban households.

Supply chain issues in sourcing and processing oats

The Asia-Pacific region produces relatively small volumes of oats compared to wheat and rice, necessitating the import of oats from countries such as Australia, Canada, or those in Europe. This reliance on imports exposes brands to challenges such as freight cost volatility, currency fluctuations, and tariff-related risks, which act as significant restraints for the market. Furthermore, processing oats into shelf-stable beverages requires specialized equipment for enzymatic hydrolysis and homogenization. These processes demand substantial capital investment, which smaller regional players often struggle to finance. This creates a financial barrier that limits the entry and growth of smaller companies, favoring multinational corporations and well-funded startups. As a result, the high dependency on imports and the capital-intensive nature of processing equipment collectively hinder the market's growth potential in the region.

Segment Analysis

By Type: Unsweetened Dominates Health-Conscious Cohorts

Unsweetened oat milk held 65.24% of the market in 2024, driven by health-conscious consumers who avoid added sugars and by foodservice operators who prefer neutral bases for flavored lattes and smoothies. Sweetened variants, forecast to grow at 13.67% CAGR through 2030, appeal to consumers transitioning from dairy milk who expect a familiar sweetness profile and to retail buyers seeking ready-to-drink convenience. Nestlé's Goodness brand, launched in Singapore in May 2024, offers naturally sweetened SKUs, allowing the company to test price elasticity and flavor preferences before broader Southeast Asian rollout.

The rapid growth of sweetened oat milk indicates that achieving taste parity with dairy is essential for mass-market adoption, while premium segments continue to focus on unsweetened formulations. Regulatory frameworks in Japan and South Korea, which require clear labeling of added sugars, may hinder the growth of sweetened variants in these markets. In Japan and South Korea, consumers are increasingly aware of sugar content due to these regulations, which could lead to a preference for unsweetened options. In contrast, Indonesia's less stringent labeling regulations offer greater flexibility for sweetened SKUs, allowing manufacturers to cater to consumer preferences for sweeter products without the same level of regulatory constraints.

Note: Segment shares of all individual segments available upon report purchase

By Flavor: Localized Variants Accelerate Trial

Un-flavoured oat milk captured 72.06% of the market in 2024, reflecting its versatility as a cooking ingredient and coffee additive, yet flavoured variants are forecast to grow at 13.86% CAGR through 2030 as brands target younger consumers who prioritize novelty and Instagram-worthy aesthetics. Introduction of matcha, hojicha, ube, pandan, yuzu, and calamansi flavors in select Asian markets in 2024 illustrates how localization can overcome the perception that oat milk is a Western import unsuited to regional palates. Oatly's Tea Master line, designed for Asian tea shops, addresses a channel-specific need that un-flavoured SKUs cannot fulfill, enabling the company to penetrate bubble tea and traditional tea cafes that represent a significant share of beverage consumption in China, Taiwan, and Thailand.

The rapid growth of flavored oat milk also indicates premiumization, as these products typically have higher retail prices compared to unflavored options. This trend is driven by consumer preferences for diverse taste profiles and the perception of added value in flavored variants. The higher price points of flavored oat milk contribute to improved per-liter margins for both brands and retailers, making it a lucrative segment within the plant-based milk market.

By Packaging Type: Cans Gain Traction in Convenience Channels

In 2024, cartons accounted for 75.32% of the packaging market share, supported by Tetra Pak's established supply relationships with retailers and the format's shelf-stable properties. These properties help reduce cold-chain costs and allow for ambient display in supermarkets, making them a preferred choice for long shelf-life products. The ability to store products without refrigeration significantly lowers logistical expenses and enhances convenience for retailers. Cans, projected to grow at a CAGR of 12.99% through 2030, are increasingly popular in convenience stores in South Korea and Japan. This growth is driven by the demand for single-serve, on-the-go beverage formats, which cater to the fast-paced lifestyles of consumers in these regions. Additionally, the recyclability of aluminum aligns with the growing environmental awareness among consumers, further boosting the adoption of cans in these markets.

PET bottles, which accounted for a smaller share in 2024, face sustainability headwinds as governments across the region consider plastic taxes and extended producer responsibility schemes. Other packaging formats, including glass bottles and pouches, remain niche but offer differentiation opportunities for premium brands targeting gift markets and specialty retailers. Tetra Pak's FSC-certified cartons, which feature prominently on Oatly and Danone packaging, provide a sustainability credential that resonates with corporate buyers and environmentally conscious consumers.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: On-Trade Growth Outpaces Retail

Off-trade channels, including supermarkets, hypermarkets, convenience stores, and online retail, accounted for 91.25% of sales in 2024. However, on-trade venues are projected to grow at a CAGR of 14.01% through 2030, supported by partnerships with coffee chains, hotels, and restaurants focusing on barista-grade formulations. Oatly’s Greater China business is heavily driven by foodservice, a channel mix that reflects the company’s cafe-first strategy and the reality that on-trade venues can charge premium prices while educating consumers on taste and texture before they commit to retail purchases. Supermarkets and hypermarkets within the off-trade segment benefit from high foot traffic and promotional opportunities, yet they also impose slotting fees and margin pressures that squeeze profitability for smaller brands.

Convenience stores provide high customer density and opportunities for impulse purchases but necessitate single-serve packaging and fast inventory turnover. Specialty stores, such as organic and health-food retailers, act as testing platforms for premium SKUs and limited-edition flavors. Online retail, which grew significantly during the COVID-19 pandemic, continues to be an essential channel for direct-to-consumer brands and for accessing consumers in tier-2 and tier-3 cities with limited physical retail presence.

Geography Analysis

China held 38.65% of regional revenue in 2024, anchored by Oatly's early entry in 2018 and its cafe-first strategy, which positioned oat milk as a premium ingredient in specialty coffee shops before expanding to retail. Collaborations with major coffee chains have introduced millions of consumers to the taste and texture of oat milk, fostering increased retail adoption. Strategic adjustments, such as consolidating production and focusing on foodservice over retail, underscore the challenges of competing with soy milk in supermarkets. Established dairy companies have utilized their distribution networks to cross-sell plant-based products, illustrating how incumbents can capitalize on growth opportunities in this category.

Indonesia, forecast to grow at 14.27% CAGR through 2030, benefits from rising dairy demand. The country's mandatory halal certification requirement, effective October 17, 2026, will compel all plant-based beverage producers to secure BPJPH approval, a regulatory threshold that favors incumbents with existing compliance infrastructure over new entrants. Indonesia's grocery retail market comprises an extensive network of convenience stores, requiring consistent inventory management and single-serve product formats. This creates distribution opportunities for brands capable of effectively addressing the logistical challenges posed by the archipelago's geography.

Australia and New Zealand together constitute a mature market with a focus on innovation, characterized by established consumer awareness and a wide range of product offerings. Japan's oat milk market, while smaller in size, benefits from favorable demographic trends, including an aging population seeking healthier dietary options and a growing interest in plant-based alternatives. India, Malaysia, Thailand, Singapore, and other Asia-Pacific countries represent emerging markets with low oat milk penetration. However, urbanization is leading to increased exposure to global food trends, rising incomes are enhancing purchasing power, and growing health awareness is encouraging consumers to explore plant-based beverages. These factors are driving latent demand, which brands can address through tailored pricing strategies, localized marketing efforts, and efficient distribution networks to reach diverse consumer bases.

Competitive Landscape

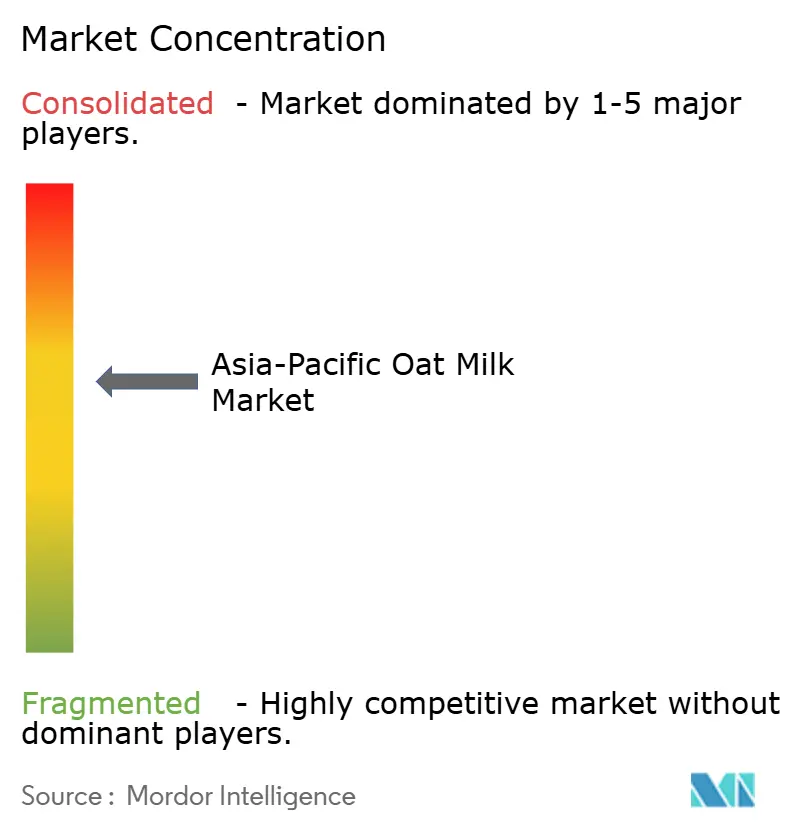

The Asia-Pacific oat milk market exhibits moderate consolidation, providing opportunities for regional disruptors to challenge established players through localized formulations, competitive pricing strategies, and channel-specific partnerships. Oatly, Danone, and Nestlé lead the premium and foodservice segments, benefiting from global brand recognition and established relationships with cafes. However, their dependence on imported oats and capital-intensive manufacturing processes results in cost structures that smaller, regionally focused competitors can undercut.

Opportunities exist in tier-2 and tier-3 cities across China, Indonesia, and India, where oat milk penetration is minimal. E-commerce provides a cost-effective alternative to physical retail expansion in these regions. Flavor innovations aligned with regional preferences, such as matcha, hojicha, ube, pandan, yuzu, and calamansi, can offer differentiation. Additionally, fortifying oat milk with calcium, vitamin D, and protein can help address nutritional gaps in plant-based diets.

Packaging innovation, especially single-serve cans designed for convenience stores and vending machines, offers a strategic opportunity to target impulse purchases and on-the-go consumption. Ingredient suppliers are also developing solutions to support fortified and high-protein oat milk variants, enabling brands to differentiate through functional nutrition. Regulatory compliance, such as Indonesia's mandatory halal certification effective October 17, 2026, is expected to benefit established players with existing BPJPH relationships. This regulation may create entry barriers for new competitors, consolidating market share among companies that invest early in compliance infrastructure.

Asia-Pacific Oat Milk Industry Leaders

-

Oatly Group AB

-

Sanitarium Health & Wellbeing

-

Nestlé SA

-

Vitasoy International Holdings Ltd

-

Danone SA (Alpro/Silk)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Indian dairy and grocery brand Country Delight has launched a plant-based milk alternative under the name Oat Beverage. The product is made from Australian oats and is free from preservatives, chemical additives, and added sugars. It is also free of soy and nuts and is produced in an allergen-controlled facility to minimize the risk of cross-contamination. This milk alternative is designed to meet the increasing demand for dairy-free products among lactose-intolerant individuals and health-conscious consumers.

- May 2024: Nestlé introduced Nestlé Goodnes, dairy-free oat milk in Singapore. Nestlé has launched its dairy-free oat milk in Singapore, offering two variants: OAT and ALMOND & OAT. Naturally sweetened from oats, both options provide essential nutrients, including Calcium and Vitamins B3, B2, and D. These products are now available at FairPrice, Cold Storage, Giant, Shopee, Redmart, and Pandamart.

- April 2024: Nestle Malaysia has introduced its Nestle Goodness brand of plant-protein beverages, designed to meet changing dietary preferences with Halal-certified, lactose-free, and vegan-friendly options. The beverage features a natural creamy texture and sweetness derived from hydrolysed oats and is enriched with micronutrients such as calcium and vitamins B2, D, and B3. It serves as a nutritious and flavorful alternative to dairy milk. Nestle Goodness is available in two variants: Dairy-Free Oat and Dairy-Free Almond & Oat.

Asia-Pacific Oat Milk Market Report Scope

Off-Trade, On-Trade are covered as segments by Distribution Channel. Australia, China, India, Indonesia, Japan, Malaysia, New Zealand, Pakistan, South Korea are covered as segments by Country.| Sweetened Oat Milk |

| Unsweetened Oat Milk |

| Flavoured |

| Un-flavoured |

| PET Bottles |

| Cans |

| Cartons |

| Others |

| On-trade | |

| Off-trade | Supermarket/Hypermarket |

| Convenience Stores | |

| Specialty Stores | |

| Online Retail |

| Other Distribution Channels |

| China |

| Japan |

| India |

| Australia |

| Indonesia |

| Malaysia |

| South Korea |

| New Zealand |

| Thailand |

| Singapore |

| Rest of Asia-Pacific |

| By Type | Sweetened Oat Milk | |

| Unsweetened Oat Milk | ||

| By Flavour | Flavoured | |

| Un-flavoured | ||

| By Packaging Type | PET Bottles | |

| Cans | ||

| Cartons | ||

| Others | ||

| By Distribution Channel | On-trade | |

| Off-trade | Supermarket/Hypermarket | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retail | ||

| Country | Other Distribution Channels | |

| China | ||

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| Malaysia | ||

| South Korea | ||

| New Zealand | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

Market Definition

- Dairy Alternatives - Dairy alternatives are foods that are made from plant-based milk/oils instead of their usual animal products, such as cheese, butter, milk, ice cream, yogurt, etc. Plant-based or non-dairy milk alternative is the fast-growing segment in the newer food product development category of functional and specialty beverage across the globe.

- Non-Dairy Butter - Non dairy butter is a vegan butter alternative that is made from a mixture of plant oils. With an increase in alternative diets like vegetarianism, veganism, and gluten intolerance, plant butter is a healthy non-dairy substitute for normal butter.

- Non-Dairy Ice Cream - Plant based ice cream is a growing category. Non-dairy ice cream is a type of dessert made without any animal ingredients. This is typically considered a substitute for regular ice cream for those who cannot or do not eat animal or animal-derived products, including eggs, milk, cream, or honey.

- Plant-Based Milk - Plant based milks are milk substitutes that are made from nuts (e.g., hazelnuts, hemp seeds), seeds (e.g., sesame, walnuts, coconuts, cashews, almonds, rice, oats, etc.) or legumes (e.g., soy). Plant-based milk such as soy milk and almond milk have been popular in East Asia and the Middle East for centuries.

| Keyword | Definition |

|---|---|

| Cultured Butter | Cultured butter is prepared by having the raw butter go through chemical processing and has been added with certain emulsifiers and foreign ingredients. |

| Uncultured Butter | This type of butter is one which has not been processed in any way |

| Natural Cheese | The type of cheese in its most natural form. It is made from natural and simple products and ingredients, including fresh and natural salts, natural colors, enzymes, and high-quality milk. |

| Processed Cheese | Processed cheese undergoes the same processes as natural cheese; however, it requires more steps and many different forms of ingredients. Making processed cheese involves melting natural cheese, emulsifying it, and adding preservatives and other artificial ingredients or colorings. |

| Single Cream | Single cream contains around 18% fat. It’s a single layer of cream that appears over boiled milk. |

| Double Cream | Double cream contains 48% fat, more than double the amount of fat of single cream. It’s heavier and thicker than single cream |

| Whipping Cream | This has a much higher fat percentage than single cream (36%). Used to top cakes, pies, and puddings and as a thickener for sauces, soups, and fillings. |

| Frozen Desserts | Desserts that are meant to be eaten in frozen condition. E.g., sherbets, sorbets, frozen yogurts |

| UHT Milk (Ultra-high temperature milk) | Milk heated at a very high temperature. Ultra-high-temperature processing (UHT) of milk involves heating for 1–8 sec at 135–154°C. which kills the spore-forming pathogenic microorganism, resulting in a product with a shelf-life of several months. |

| Non-dairy butter/Plant-based butter | Butter made from plant-derived oil such as coconut, palm, etc. |

| Non-dairy Yogurt | Yogurt made from typically made from nuts, like almonds, cashews, coconuts, and even other foods like soybeans, plantains, oats, and peas |

| On-trade | It refers to restaurants, QSRs, and bars. |

| Off-trade | It refers to supermarkets, hypermarkets, on-line channels, etc. |

| Neufchatel cheese | One of the oldest kinds of cheese in France. It is a soft, slightly crumbly, mold-ripened, bloomy-rind cheese made in the Neufchâtel-en-Bray region of Normandy. |

| Flexitarian | It refers to a consumer preferring a semi-vegetarian diet, that is centered on plant foods with limited or occasional inclusion of meat. |

| Lactose Intolerance | Lactose intolerance is a reaction in digestive system to lactose, the sugar in milk. It causes uncomfortable symptoms in response to the consumption of dairy products. |

| Cream Cheese | Cream cheese is a soft and creamy fresh cheese with a tangy taste made from milk and cream. |

| Sorbets | Sorbet is a frozen dessert made using ice combined with fruit juice, fruit purée, or other ingredients, such as wine, liqueur, or honey. |

| Sherbet | Sherbet is a sweetened frozen dessert made with fruit and some sort of dairy product such as milk or cream. |

| Shelf stable | Foods that can be safely stored at room temperature, or "on the shelf," for at least one year and do not have to be cooked or refrigerated to eat safely. |

| DSD | Direct Store Delivery is the process in supply chain management wherein the product is delivered from manufacturing plant directly to the retailer. |

| OU Kosher | Orthodox Union Kosher is a kosher certification agency based in New York City. |

| Gelato | Gelato is a frozen creamy dessert made with milk, heavy cream and sugar. |

| Grass-fed Cows | Grass-fed cows are allowed to graze in pastures, where they eat a variety of grasses and clover. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms