Asia-Pacific Medical Tourism Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

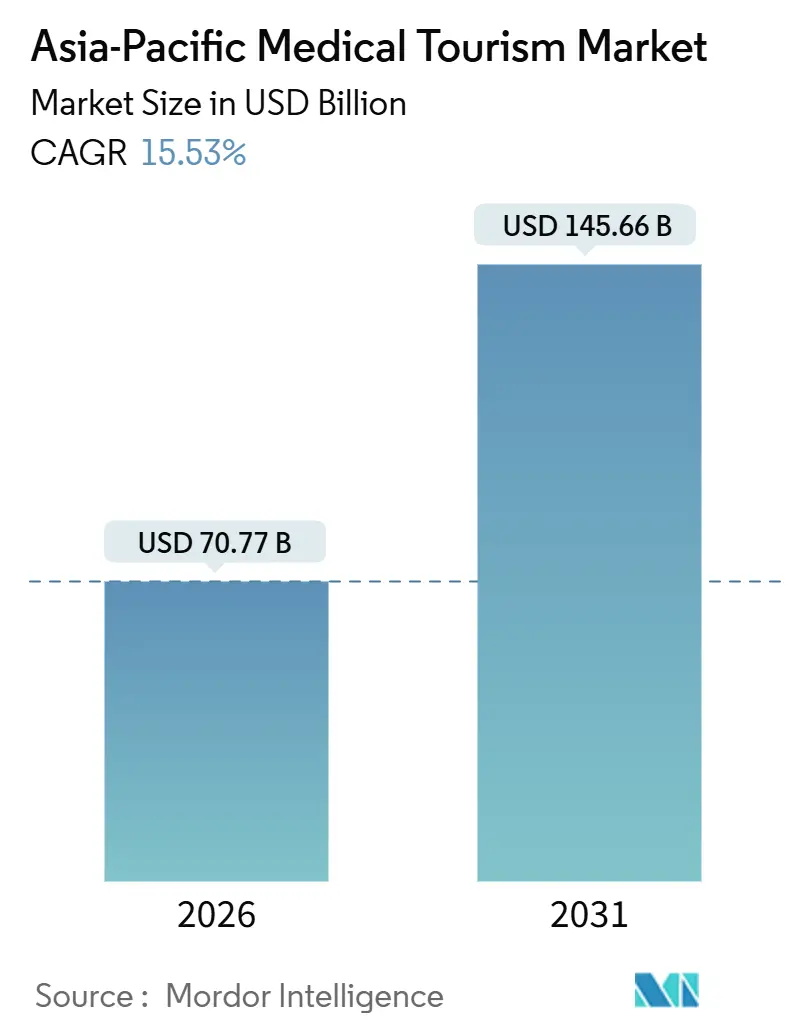

| Market Size (2026) | USD 70.77 Billion |

| Market Size (2031) | USD 145.66 Billion |

| Growth Rate (2026 - 2031) | 15.53% CAGR |

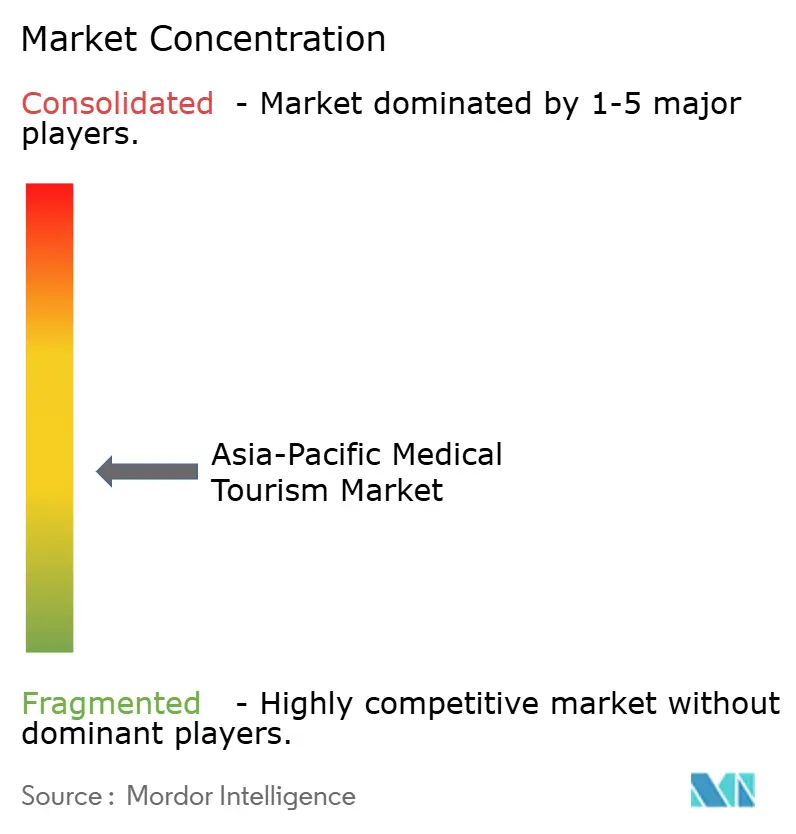

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Medical Tourism Market Analysis by Mordor Intelligence

The Asia-Pacific Medical Tourism Market size is estimated at USD 70.77 billion in 2026, and is expected to reach USD 145.66 billion by 2031, at a CAGR of 15.53% during the forecast period (2026-2031).

Demand rests on a structural 40%–80% cost advantage over OECD providers, an expanding network of more than 1,100 Joint Commission International (JCI)-accredited hospitals, and rapid adoption of surgical robotics that narrows perceived quality gaps. Private hospital chains continue to invest in specialized oncology, fertility, and robotic orthopedic suites, while ASEAN cross-border insurance pilots and visa liberalization reduce administrative friction for patients. Mid-tier facilities in Vietnam and Malaysia are scaling capacity to serve middle-income travelers who now access partial insurance reimbursement for overseas care. Conversely, travel-health concerns and medical inflation of 5%–8% annually temper the cost arbitrage that underpins patient flows.

Key Report Takeaways

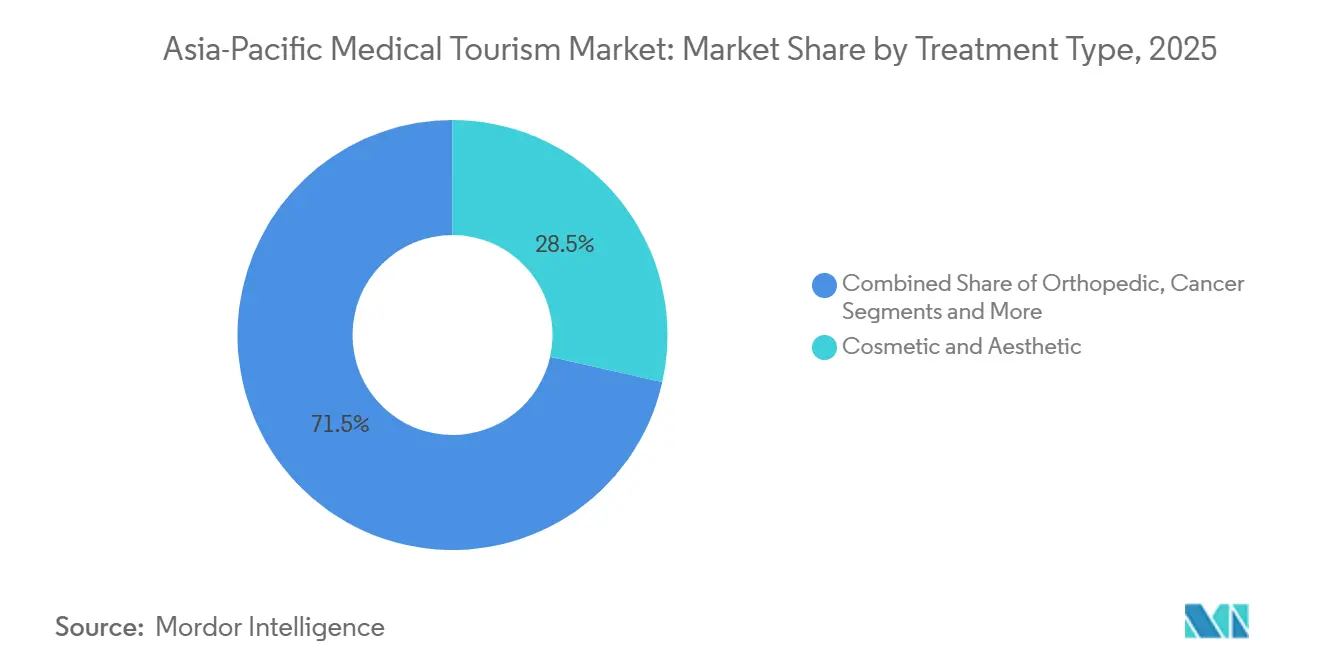

- By treatment type, cosmetic and aesthetic procedures held 28.55% revenue share of the Asia-Pacific medical tourism market in 2025, while orthopedic surgery is forecast to grow at an 18.25% CAGR to 2031.

- By service provider, private hospitals captured 60.53% of the Asia-Pacific medical tourism market share in 2025, whereas ambulatory surgical centers record the fastest projected CAGR at 19.85% through 2031.

- By country, India accounted for 25.13% of the Asia-Pacific medical tourism market size in 2025 and Vietnam is advancing at an 18.51% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Medical Tourism Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost differential versus OECD countries | +3.2% | India, Thailand, Vietnam, Malaysia | Long term (≥4 years) |

| Rising middle-class affluence & insurance portability | +2.8% | Thailand, Malaysia, Vietnam, India, China | Medium term (2-4 years) |

| Government visa & promotion schemes | +2.1% | India, Thailand, Vietnam, Malaysia, South Korea | Short term (≤2 years) |

| Proliferation of JCI-accredited hospitals | +2.5% | Thailand, Singapore, India, South Korea | Medium term (2-4 years) |

| Adoption of surgical robotics & advanced tech | +3.0% | South Korea, Japan, Singapore, India, China | Long term (≥4 years) |

| ASEAN cross-border insurance frameworks | +1.7% | ASEAN member states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost Differential Versus OECD Countries

Elective procedures in Bangkok or Chennai cost 40%–80% less than in the United States, United Kingdom, or Australia[1]Bangkok Hospital Group, “International Patient Pricing Guide,” bangkokhospital.com. A knee replacement in Thailand averages USD 12,000 against USD 50,000 in the United States, and cosmetic rhinoplasty in Seoul runs USD 3,500 compared with USD 15,000 in Sydney. Lower physician salaries, subsidized medical-device production under India’s Production Linked Incentive scheme, and cheaper real-estate underpin the advantage. Malaysia’s “Year of Medical Tourism 2026” bundles treatment and hotel packages priced 60% below home-country rates for Gulf patients.

Rising Middle-Class Affluence & Insurance Portability

ASEAN added 50 million middle-income households between 2020 and 2024, lifting discretionary healthcare budgets. Cross-border insurance pilots now allow Thai citizens to obtain orthopedic or cardiac care in Malaysia with up to 70% reimbursement. Fertility tourism benefits most: Malaysia attracts Indonesian couples seeking halal-compliant IVF protocols, while Singapore draws Chinese and Indian patients for premium genetic screening.

Government Visa & Promotion Schemes

India’s Medical Visa processed 635,000 entries in 2023, up 40% on 2022, and offers triple-entry stays of 60 days[2]Ministry of External Affairs India, “Medical Visa Statistics 2024,” mea.gov.in. Thailand grants 90-day medical visas with caregiver access, and Vietnam’s 2024 e-visa cut processing from 15 to 3 days. Malaysia earmarked USD 15 million for global marketing in 2026, emphasizing halal food and prayer facilities.

Proliferation of JCI-Accredited Hospitals

Regional JCI accreditations rose from 800 in 2020 to more than 1,100 in 2025, lifting international-patient confidence. Thailand leads with over 60 certified facilities, and Vietnam added five in 2024 alone. Bumrungrad International now holds direct billing with 500+ insurers, an outcome tied to its accreditation status.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Travel-health uncertainty & pandemic after-effects | −2.3% | Japan, Australia, China | Short term (≤2 years) |

| Perceived quality / safety variability | −1.8% | Vietnam, Philippines, Indonesia | Medium term (2-4 years) |

| Post-operative continuity-of-care gaps | −1.5% | Global | Long term (≥4 years) |

| Medical inflation eroding price advantage | −1.9% | India, Thailand, Malaysia, Vietnam | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Travel-Health Uncertainty & Pandemic After-Effects

Outbound travel from Japan and Australia recovered to only 70% of 2019 levels in 2024, reflecting lingering infection fears and higher insurance premiums[3]Japan Tourism Agency, “Outbound Travel Survey 2024,” mlit.go.jp. China’s outbound trips stayed subdued at 300,000 because of visa lags and capital-control scrutiny. Booking lead times for Bangkok hospitals stretched to 12 weeks as patients requested multiple teleconsults before traveling.

Perceived Quality / Safety Variability

Singapore publishes annual infection and readmission data, bolstering trust. Vietnam and the Philippines rely on voluntary audits, leading to rare but publicized adverse-event reports. Liability awards remain low, USD 50,000-100,000 in Thailand, versus multi-million-dollar U.S. settlements, which deters risk-averse patients.

Segment Analysis

By Treatment Type: Orthopedics Re-shapes Demand Mix

Cosmetic and aesthetic procedures held 28.55% of the Asia-Pacific medical tourism market in 2025, underpinned by 705,044 dermatology patients in South Korea and Thailand’s booming device market. In contrast, orthopedic surgery is projected to expand at an 18.25% CAGR, the highest among segments, driven by robotic joint replacements and long public wait times in Japan and Australia. The Asia-Pacific medical tourism market size for dental treatments is climbing on Thailand’s USD 4.2 billion forecast by 2031, with travelers saving up to 70% on implants. Cardiovascular, oncology, fertility, and neurological procedures collectively broaden the regional case-mix as proton therapy and advanced IVF labs open across the region.

Technological parity with OECD centers is narrowing. Proton therapy availability in India and South Korea, together with AI-enabled diagnostic imaging, elevates clinical confidence among high-acuity patients. Meanwhile, bundled wellness add-ons—post-operative rehabilitation in Thai resorts or Ayurvedic recovery in Kerala—enhance perceived value. The Asia-Pacific medical tourism industry consequently attracts both cost-sensitive and outcome-driven travelers, balancing elective cosmetics with life-saving oncology and cardiac interventions.

Note: Segment shares of all individual segments available upon report purchase

By Service Provider: Ambulatory Centers Capture Day-Case Migration

Private hospitals generated 60.53% of 2025 revenue as multilingual staff and insurer tie-ups funnel patients toward full-service campuses. Ambulatory surgical centers (ASCs), however, are growing 19.85% annually by accommodating low-complexity day cases, particularly ophthalmology and aesthetic procedures in Seoul’s Gangnam district and Singapore’s Novena corridor. The Asia-Pacific medical tourism market share for ASCs is expected to widen as regulators issue streamlined licenses to relieve public-hospital backlogs.

Hospital chain consolidation adds scale efficiencies. IHH Healthcare’s 80-facility network standardizes protocols and centralizes device procurement, trimming costs by up to 20%. Specialty clinics—fertility, dental, eye-care—extend into Tier-2 cities where real-estate and labor are cheaper, offering resilient domestic demand that buffers international volatility. Collectively, these dynamics reinforce patient choice, diversify supply, and encourage price competition.

Geography Analysis

India controlled 25.13% of 2025 regional revenue, buoyed by 635,000 arrivals in 2023 and a 2 million-arrival target for 2030. The Asia-Pacific medical tourism market size for India is set for double-digit growth as Apollo, Fortis, and Max invest USD 500 million to add 2,000 beds and 15 cath labs, and as the domestic SSI Mantra robot lowers entry costs for Tier-2 hospitals. Cardiac surgery prices of USD 8,000 and 45 JCI-accredited hospitals preserve India’s competitive edge.

Thailand welcomed 1.2 million patients in 2024, generating USD 850 million in revenue. Over 60 JCI hospitals, a 90-day medical visa, and USD 20 million in 2024 marketing spend underscore state support. Cosmetic and IVF volumes climb as Thailand’s aesthetic devices market approaches USD 7.51 billion by 2027, helped by Korean and Chinese demand.

Vietnam posts the fastest country CAGR at 18.51% through 2031, propelled by Vinmec’s 10-hospital expansion and Resolution 06/NQ-CP visa liberalization. FV Hospital’s JCI accreditation in 2024 elevates quality perception, while government targets 1 million medical tourists by 2030. South Korea received 1.17 million foreign patients in 2024, with dermatology representing 56.6% of volume, and designated six medical cities that offer tax breaks to high-volume hospitals.

Malaysia returned to pre-pandemic levels with 1.2 million arrivals in 2023 and seeks USD 2.7 billion revenue by 2030 through its 2026 promotional campaign. Singapore positions itself at the premium end, treating 30,000 foreign oncology and cardiac patients in 2024 at average case values above USD 25,000. China remains a major source market but is also expanding inbound robotics centers, while Australia primarily sends patients abroad to sidestep long orthopedic and dental queues.

Competitive Landscape

The top groups, IHH Healthcare, Bangkok Dusit Medical Services (BDMS), Apollo Hospitals, Bumrungrad International, and Raffles Medical—collectively account for less regional revenue, confirming a fragmented arena ripe for niche specialists. IHH leverages its 80-hospital footprint across 10 countries to cross-refer oncology and cardiac cases, reducing device costs via bulk procurement. BDMS operates 50 hospitals in Thailand, Cambodia, and Myanmar, channeling complex cases to Bangkok flagships equipped with proton therapy suites. Apollo’s 71-facility network services underserved South Asian and African patients, aided by a telemedicine platform spanning 140 countries.

Competitive strategy centers on technology and insurer partnerships. Bumrungrad International maintains 500+ direct-billing agreements that insulate revenue from currency swings. Robotic-surgery installations correlate with 20%–30% upticks in overseas inquiries within a year. Emerging disruptors include Vinmec in Vietnam, which added 1,500 beds and secured three JCI accreditations since 2023, and Gangnam’s high-volume cosmetic clinics, each performing 10,000+ annual rhinoplasties at 30% below full-service hospital prices.

Asia-Pacific Medical Tourism Industry Leaders

Apollo Hospital Enterprise Limited

Bumrungrad International Hospital

Fortis Healthcare Limited

KPJ Healthcare Berhad

Aditya Birla Memorial Hospital

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Malaysia Healthcare Travel Council named the inaugural Flagship Medical Tourism Hospital under its FMTH program to elevate Malaysia as a preferred destination.

- December 2025: Association of Healthcare Providers India and UAE-based Mulk Med Healthcare Group signed a partnership to expand inbound patient flows to India.

Asia-Pacific Medical Tourism Market Report Scope

Medical tourism is traveling to another country to obtain medical treatment or procedures. It may be done for various reasons, such as seeking lower costs for medical care, accessing treatments or procedures that may not be available in one's home country, or avoiding long waiting lists for certain medical procedures.

Asia-Pacific Medical Tourism Market is segmented by treatment type (dental treatment, cosmetic treatment, cardiovascular treatment, orthopedic treatment, neurological treatment, cancer treatment, fertility treatment, and other treatments), service provider (public and private), and country (India, China, Japan, Australia, South Korea, Vietnam, and rest of Asia-Pacific). The report offers market size and values in (USD) for the above segments.

| Dental |

| Cosmetic & Aesthetic |

| Cardiovascular |

| Orthopedic |

| Neurological |

| Oncology (Cancer) |

| Fertility & Reproductive |

| Other Treatments |

| Public Hospitals |

| Private Hospitals |

| Specialty Clinics |

| Ambulatory Surgical Centers |

| China |

| Japan |

| Australia |

| India |

| South Korea |

| Vietnam |

| Rest of Asia-Pacific |

| By Treatment Type | Dental |

| Cosmetic & Aesthetic | |

| Cardiovascular | |

| Orthopedic | |

| Neurological | |

| Oncology (Cancer) | |

| Fertility & Reproductive | |

| Other Treatments | |

| By Service Provider | Public Hospitals |

| Private Hospitals | |

| Specialty Clinics | |

| Ambulatory Surgical Centers | |

| By Country | China |

| Japan | |

| Australia | |

| India | |

| South Korea | |

| Vietnam | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large is the Asia-Pacific medical tourism market today?

The Asia-Pacific medical tourism market size is USD 70.77 billion in 2026 and is forecast to reach USD 145.66 billion by 2031.

Which treatment type is growing fastest across the region?

Orthopedic surgery leads with an 18.25% CAGR through 2031, propelled by robotic joint-replacement demand and long public-system wait times.

Why do patients choose Asia over OECD countries for medical care?

Key reasons are 40%-80% lower procedure costs, fast visa processing, and more than 1,100 JCI-accredited hospitals that assure quality.

Which country captured the largest share in 2025?

India held 25.13% of regional revenue after processing 635,000 medical visas in 2023 and expanding hospital capacity in 2024-2025.

What role do ambulatory surgery centers play?

ASCs are the fastest-growing provider category at 19.85% CAGR because they handle low-complexity day cases at 40%50% lower operating costs than full-service hospitals.