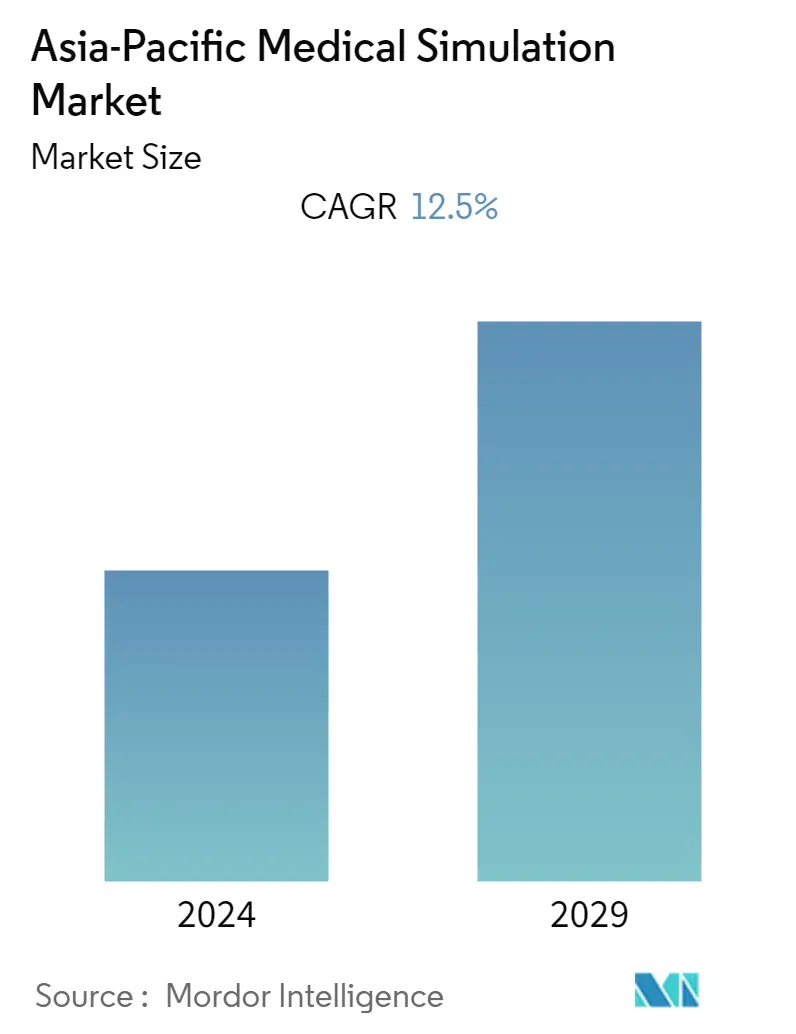

Market Size of Asia-Pacific Medical Simulation Industry

| Study Period | 2021 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Historical Data Period | 2021 - 2022 |

| CAGR | 12.50 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Asia Pacific Medical Simulation Market Analysis

The Asia-Pacific medical simulation market is expected to register a CAGR of 12.5% during the forecast period.

COVID-19 had a profound impact on the medical simulation market owing to the cancellations of minimally invasive surgeries and a decline in research initiatives by key players in the initial phases of the pandemic. Various healthcare organizations also organized medical simulation training for the better management of COVID-19, which has also impacted the market growth. For instance, according to an article published in the Australian Journal of General Practice in June 2020, a simulation training course for family medicine residents in Shanghai, China, was conducted virtually to train the management of COVID-19. 96% of participants found the simulation extremely beneficial. However, the market has been recovering well over the last two years since the restrictions were lifted. With the new product launches and rising minimally invasive surgeries in the Asia-Pacific region, the market is expected to gain pace during the forecast period.

In addition, the increasing demand for minimally-invasive treatments, continuous technology innovation, and growing focus on patient safety is actively affecting the growth of the market studied.

Minimally-invasive techniques are becoming standard for several surgical procedures at a very fast pace. Minimally-invasive surgery (MIS) is associated with less pain, shorter hospital stays, and fewer post-surgical complications. For instance, according to an article published in the South Asian Journal of Cancer in December 2021, the postoperative complication rate of the minimally invasive esophagectomy (MIE) group was much less (18.5%) as compared with the open esophagectomy (OE) group (41%). Pulmonary complications reported in the MIE group was 7.4% compared to 25.6% in the OE group for Resectable Esophageal Cancer. Also, a research article published in BMC Psychiatry Journal in January 2022 reported the prevalence of minimally invasive facial cosmetic surgery (MIFCS) among Chinese college students was 2.7% among the surveyed population. The advantages of MIS and the high incidence of these surgeries are estimated to propel the market growth during the forecast period. Therefore, the requirement of medical simulation in the training of minimally-invasive surgery has been established over the past few years and is expected to propel the market growth during the forecast period.

Furthermore, the utility of medical simulation in cataract surgical procedures is propelling market growth. For instance, in October 2021, B.J. Government Medical College launched a pilot program with HelpMeSee to bring its virtual reality, simulation-based training in order to combat the cataract blindness epidemic in India by training more cataract specialists. The training also allowed ophthalmologists to overcome the limits of COVID-19 on surgical skills training to increase patient safety. In December 2021, 190 trainees completed simulation-based training in India. These courses will create an opportunity for various hospitals to treat more untreated patients in developing and underdeveloped countries with fewer doctors, which is anticipated to propel the market growth during the forecast period.

Therefore, owing to the factors such as rising medical simulation training for MIS and increasing strategic initiatives by key players, the market studied is anticipated to witness growth over the analysis period. However, the high cost of simulators and reluctance to adopt new training methods is likely to impede the market growth.

Asia Pacific Medical Simulation Industry Segmentation

As per the scope of the report, medical simulation is the modern-day methodology for training healthcare professionals through advanced educational technology. Medical simulation is experiential learning that every healthcare professional may need but cannot always be engaged in during real-life patient care.

The Asia-Pacific Medical Simulation Market is Segmented by Product (Interventional/Surgical Simulators (Laparoscopic Surgical Simulators, Gynecology Surgical Simulators, Cardiac Surgical Simulators, Arthroscopic Surgical Simulators), Task Trainers, and Other Products), Services and Software (Web-based Simulation, Simulation Training Services, Other Services and Softwares), Technology (High-fidelity, Medium-fidelity, and Low-fidelity Simulators), End User (Academic and Research Institutes

and Hospitals), and Geography (China, Japan, India, Australia, South Korea, and Rest of Asia-Pacific). The report offers value (in USD million) for the above segments.

| By Product | ||||||

| ||||||

| Task Trainers | ||||||

| Other Products |

| By Services and Software | |

| Web-based Simulation | |

| Simulation Training Services | |

| Other Services and Softwares |

| By Technology | |

| High-fidelity Simulators | |

| Medium-fidelity Simulators | |

| Low-fidelity Simulators |

| By End-User | |

| Academic and Research Institutes | |

| Hospitals |

| By Geography | |

| China | |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific |

Asia-Pacific Medical Simulation Market Size Summary

The Asia-Pacific medical simulation market is poised for significant growth, driven by the increasing demand for minimally invasive surgeries and advancements in technology. The market experienced initial setbacks due to the COVID-19 pandemic, which led to a temporary decline in research initiatives and the cancellation of surgeries. However, the recovery has been robust, with healthcare organizations leveraging medical simulation training to enhance COVID-19 management. The rising adoption of minimally invasive techniques, which offer benefits such as reduced pain and shorter recovery times, is a key factor propelling market expansion. Additionally, the use of medical simulation in training for cataract surgeries is gaining traction, particularly in countries like India, where initiatives are underway to address cataract blindness through virtual reality training programs.

The market is further bolstered by strategic initiatives from key players and the increasing integration of medical simulation in academic and research institutions. These institutions are mandating simulation training for healthcare professionals, which is expected to enhance the quality of care. India's significant market share is attributed to increased healthcare expenditure and the launch of new products, alongside strategic partnerships and investments in research and development. The competitive landscape is characterized by a few dominant companies, with international and local players holding substantial market shares. Recent developments, such as the launch of augmented reality surgical navigation solutions and the expansion of simulation-based medical education facilities, underscore the dynamic nature of the market and its potential for continued growth.

Asia-Pacific Medical Simulation Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.2.1 Increasing Demand for Minimally-Invasive Treatments

-

1.2.2 Continuous Innovation in Technology

-

1.2.3 Increasing Focus on Patient Safety

-

-

1.3 Market Restraints

-

1.3.1 High Cost of Simulators

-

1.3.2 Reluctance to Adopt New Training Methods

-

-

1.4 Porter's Five Forces Analysis

-

1.4.1 Threat of New Entrants

-

1.4.2 Bargaining Power of Buyers/Consumers

-

1.4.3 Bargaining Power of Suppliers

-

1.4.4 Threat of Substitute Products

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION (Market Size by Value in USD Million)

-

2.1 By Product

-

2.1.1 Interventional/Surgical Simulators

-

2.1.1.1 Laparoscopic Surgical Simulators

-

2.1.1.2 Gynecology Surgical Simulators

-

2.1.1.3 Cardiac Surgical Simulators

-

2.1.1.4 Arthroscopic Surgical Simulators

-

-

2.1.2 Task Trainers

-

2.1.3 Other Products

-

-

2.2 By Services and Software

-

2.2.1 Web-based Simulation

-

2.2.2 Simulation Training Services

-

2.2.3 Other Services and Softwares

-

-

2.3 By Technology

-

2.3.1 High-fidelity Simulators

-

2.3.2 Medium-fidelity Simulators

-

2.3.3 Low-fidelity Simulators

-

-

2.4 By End-User

-

2.4.1 Academic and Research Institutes

-

2.4.2 Hospitals

-

-

2.5 By Geography

-

2.5.1 China

-

2.5.2 Japan

-

2.5.3 India

-

2.5.4 Australia

-

2.5.5 South Korea

-

2.5.6 Rest of Asia-Pacific

-

-

Asia-Pacific Medical Simulation Market Size FAQs

What is the current Asia-Pacific Medical Simulation Market size?

The Asia-Pacific Medical Simulation Market is projected to register a CAGR of 12.5% during the forecast period (2024-2029)

Who are the key players in Asia-Pacific Medical Simulation Market?

3D Systems, Canadian Aviation Electronics (CAE) Inc., Kyoto Kagaku Co. Ltd, Laerdal Medical and Limbs & Things Ltd are the major companies operating in the Asia-Pacific Medical Simulation Market.