Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

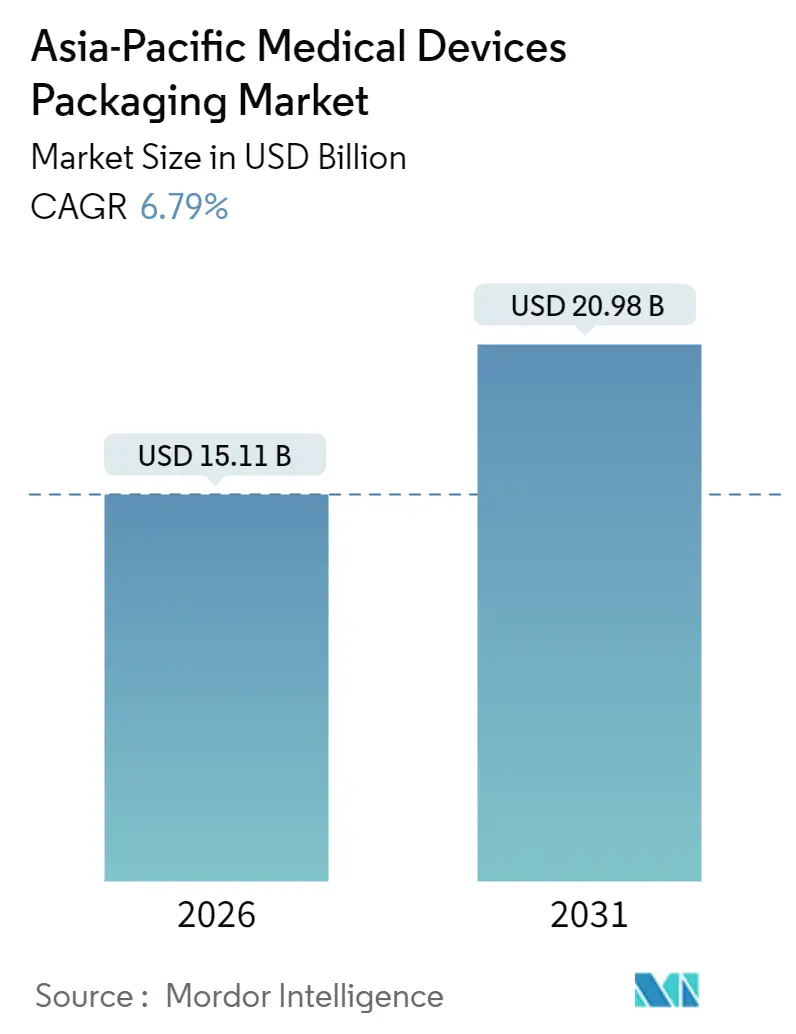

| Market Size (2026) | USD 15.11 Billion |

| Market Size (2031) | USD 20.98 Billion |

| Growth Rate (2026 - 2031) | 6.79% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Medical Devices Packaging Market Analysis by Mordor Intelligence

Asia-Pacific medical devices packaging market size in 2026 is estimated at USD 15.11 billion, growing from 2025 value of USD 14.15 billion with 2031 projections showing USD 20.98 billion, growing at 6.79% CAGR over 2026-2031. Robust manufacturing expansion across China, India, and Southeast Asia, rising healthcare spending in developed economies such as Japan and Australia, and a steady shift toward smart, sensor-enabled packs form the core growth drivers of the Asia-Pacific medical devices packaging market. Cost-efficient regional production hubs stimulate large-volume demand for plastics, even as bio-based alternatives gain regulatory traction. Hospitals, clinics, and contract service providers represent the largest buyers, while direct-to-patient e-commerce distribution urges tertiary pack redesign for parcel integrity. Competitive intensity revolves around sterile barrier validation, sustainability credentials, and digital traceability, allowing suppliers that master these capabilities to capture higher-margin contracts in the Asia-Pacific medical devices packaging market.

Key Report Takeaways

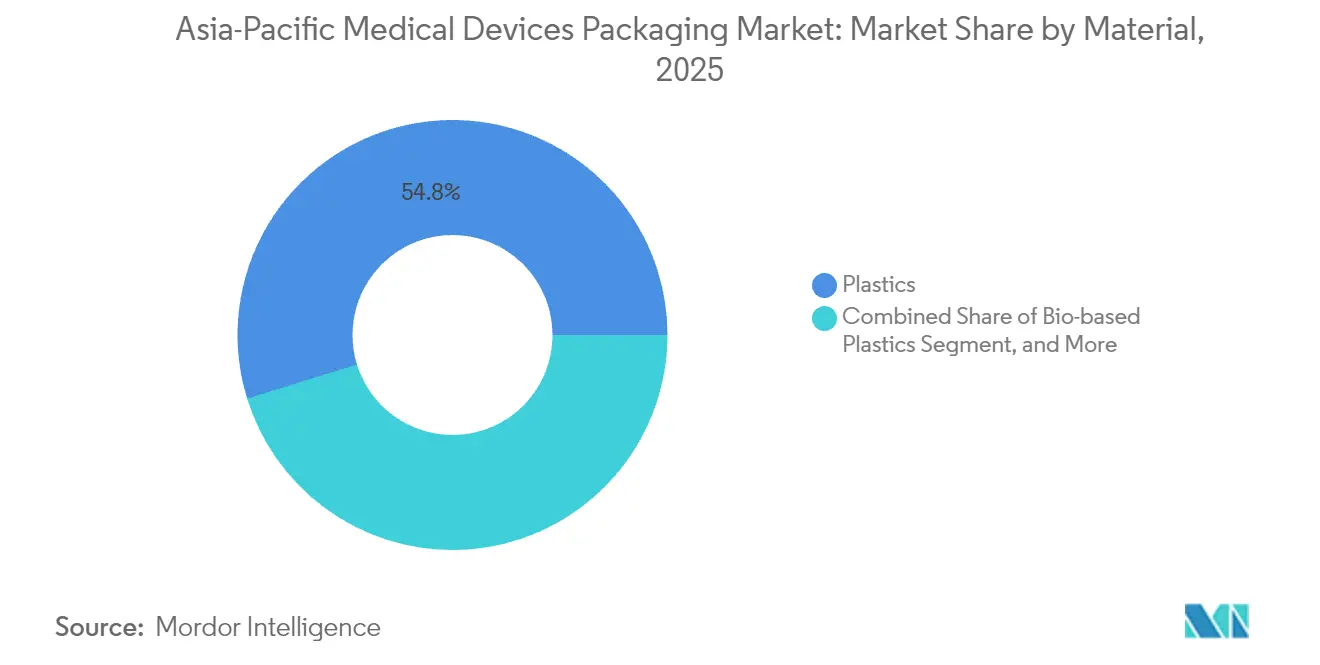

- By material, plastics accounted for 54.78% of the Asia-Pacific medical devices packaging market share in 2025, while bio-based plastics are poised to expand at a 7.78% CAGR through 2031.

- By product type, pouches and bags led with 36.05% revenue share in 2025; trays and containers are forecast to grow at a 7.12% CAGR to 2031.

- By application, sterile packaging controlled 64.72% of the Asia-Pacific medical devices packaging market size in 2025, and active/smart formats are advancing at an 7.9% CAGR to 2031.

- By packaging level, primary packs controlled 52.01% of the Asia-Pacific medical devices packaging market size in 2025, and are advancing at a 3.63 % CAGR to 2031.

- By end user, hospitals and clinics held 39.88% share of the Asia-Pacific medical devices packaging market size in 2025, whereas contract manufacturing and sterilization organizations record the highest projected CAGR at 7.11% through 2031.

- By geography, China commanded 21.98% of the Asia-Pacific medical devices packaging market share in 2025, and India is projected to post an 7.99% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Medical Devices Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Asia-Pacific medical-device manufacturing hub | +1.8% | China, India, Vietnam, Malaysia | Medium term (2-4 years) |

| Growing demand for sterile barrier systems | +1.4% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Increasing healthcare expenditure and aging demographics | +1.2% | Japan, South Korea, Australia, urban China | Long term (≥ 4 years) |

| Stringent regulatory norms mandating tamper-evident packs | +0.9% | Global, with early adoption in Japan, Australia | Short term (≤ 2 years) |

| Rise of direct-to-patient e-commerce deliveries | +0.7% | Urban centers across APAC | Medium term (2-4 years) |

| Integration of smart sensors and digital tracking | +0.6% | China, Japan, South Korea technology hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of APAC Medical-Device Manufacturing Hub

Multinational device makers intensified production migration to Asia in 2024, with China’s output rising 12.3% and India’s capacity climbing 18.7% after Production Linked Incentive funding. Clustered factories in Vietnam and Malaysia now feed sterile-pack volume lines that demand validated barrier materials at competitive cost. Such scaling enables packaging converters to amortize automation investment while satisfying ISO 11607 across multijurisdiction export lanes. Regional resin supply constraints nonetheless force dual-sourcing, nud,ging converters toward Southeast Asian petrochemical partners. The result is a manufacturing ecosystem that underpins steady orders for trays, pouches and labels in the Asia-Pacific medical devices packaging market.

Growing Demand for Sterile Barrier Systems

ASEAN regulators harmonized toward ISO 11607 in 2024, prompting OEMs to upgrade peel-pouch and thermoformed tray validation. Contract sterilizers saw a 23% capacity-utilization jump as gamma, ethylene oxide, and vaporized hydrogen peroxide runs accelerated. Barrier substrates with antimicrobial coatings gain favor because they extend device shelf life without altering sterilization cycles. Suppliers that provide cross-method validation increasingly win multi-country contracts, boosting their footprint in the Asia-Pacific medical devices packaging market. Hospitals likewise mandate tamper-proof sterile barriers to curb healthcare-associated infections, reinforcing long-term demand.

Increasing Healthcare Expenditure and Aging Demographics

Japan spent JPY 48.2 trillion (USD 322 billion) on healthcare in 2024, funneling 8.3% to device procurement. Elderly-care facilities specify larger-print labels and easy-grip openings to aid dexterity-impaired users. South Korea’s seniors are projected to represent 40% of the population by 2030, spurring home-use device packs with tamper indicators and dose-tracking inserts. Australia’s Therapeutic Goods Administration tightened labeling for aged-care devices in 2024, incentivizing packaging with intuitive symbols and scan-and-trace codes. These demographic currents keep premium yet patient-centric formats at the forefront of the Asia-Pacific medical devices packaging market.

Stringent Regulatory Norms Mandating Tamper-Evident Packs

Counterfeit incidents in 2024 led Japan’s Pharmaceuticals and Medical Devices Agency to enforce serialization on Class III devices and require pack-level data uploads to centralized servers. Singapore extended tamper requirements to temperature-sensitive devices, compelling cold-chain indicators on outer cartons. Such rulemaking advantages converters proficient in digital printing, holographic films, and track-and-trace modules. Traditional vendors lacking secure-print or RFID experience risk disqualification from high-value bids in the Asia-Pacific medical devices packaging market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in polymer-resin prices | -0.8% | Global, with acute impact in China, India | Short term (≤ 2 years) |

| Cost-reduction pressure from device OEMs | -0.6% | Manufacturing centers: China, Vietnam, Malaysia | Medium term (2-4 years) |

| Weak recycling infrastructure for multi-material packs | -0.5% | ASEAN core, emerging APAC markets | Long term (≥ 4 years) |

| ASEAN ISO-11607 harmonization delays | -0.4% | ASEAN member countries, cross-border trade | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Polymer-Resin Prices

Polyethylene and polypropylene spot swings hit 23% in 2024, pulling converter margins downward on fixed-price supply deals. China’s stricter refinery emissions rules shrank domestic resin availability, pushing regional prices 15% above global averages. Larger converters hedge through multi-country sourcing and long-term contracts, while small firms face consolidation pressure. Elevated resin risk tempers capital spending across family-owned converters, mildly restraining growth in the Asia-Pacific medical devices packaging market.

Cost-Reduction Pressure from Device OEMs

Packaging represents 3-7% of device manufacturing cost, yet OEMs demanded 12% average price cuts from converters in 2024. Commodity pouches endured the steepest reductions, forcing suppliers into thinner gauges and faster cycle times. Automation investment offsets labor but raises debt levels, making profitability hinge on value-added features such as RFID or sustainable substrates. The squeeze is most intense for high-volume exporters based in China and Vietnam, where cost leadership is a prerequisite for long-term contracts within the Asia-Pacific medical devices packaging market.

Segment Analysis

By Material: Plastics Dominance Faces Sustainability Challenge

Plastics held 54.78% of the Asia-Pacific medical devices packaging market share in 2025, underpinned by cost-efficiency and broad sterilization compatibility. Bio-based variants, including DuPont’s next-generation Tyvek, earned multi-country clearance and drive a 7.78% CAGR through 2031. The Asia-Pacific medical devices packaging market size allocated to plastics reached USD 7.75 billion in 2025. Yet regulatory carbon caps in Japan and Australia push procurement teams toward renewable feedstocks, accelerating pilot projects with chemically recycled polyethylene. Metals and foils retain niche value in radiation shielding and moisture-barrier layers for implant kits, while glass remains confined to reusable scopes and premium analyzers.

Investment in integrated resin-to-film lines secures supply continuity for leading converters. Multilayer co-extrusion that combines recycled core layers with virgin contact surfaces reduces virgin-polymer intensity without jeopardizing ISO 10993 compliance. Converters partnering with petrochemical suppliers on mass-balance certification now bid advantageously on multinational device tenders. The sustainability mandate, therefore, refines, but does not overturn, the plastic-led material portfolio in the Asia-Pacific medical devices packaging market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Product Type: Pouches Lead While Containers Innovate

Pouches and bags contributed 36.05% to 2025 revenue, owing to the form-fill-seal economy and validated peelability. The Asia-Pacific medical devices packaging market size for pouches is projected to advance at a 6.04% CAGR to 2031. Thermoformed trays and rigid containers, however, are expanding 7.12% annually as robotic surgery kits and implant systems need custom cavities and drop resistance. Sonoco’s 2024 recyclable tray launch married rigid protection with sustainable resin blends, aligning with hospital waste-reduction targets.

Blister packs bridge pharmaceutical-device hybrids like insulin pens, leveraging existing blistering infrastructure. Corrugated cartons evolve into smart secondary carriers, embedding QR codes that sync with hospital inventory software. Automated line efficiency drives pack geometry standardization to maximize throughput in high-speed sealers. Collectively, product-type innovation sustains broad option ranges within the Asia-Pacific medical devices packaging market.

By Application: Smart Packaging Disrupts Sterile Dominance

Sterile packs held 64.72% of the 2025 value, mirroring ISO 11607 enforcement, yet smart packs incorporating IoT sensors and RFID tags grow 7.9% per year. The Asia-Pacific medical devices packaging market size allocated to active and smart packs is forecast at USD 3.39 billion by 2031. Avery Dennison’s RFID-enabled sterile barrier supports real-time temperature and location logging without compromising microbial integrity. OEM quality teams now require digital chain-of-custody data for high-risk implants shipped across humid tropical corridors.

Non-sterile packs address durable equipment, but increasingly adopt tamper indicators and environmental monitors due to home-healthcare expansion. Regulators explore cybersecurity guidance for sensor-equipped packs to protect patient data on cloud-linked dashboards. This convergence of sterility and interactivity differentiates premium offerings in the Asia-Pacific medical devices packaging market.

By End User: Contract Organizations Reshape Supply Chains

Hospitals and clinics consumed 39.88% of 2025 demand, yet contract manufacturing and sterilization organizations are growing 7.11% annually as OEMs outsource complex processes. Group purchasing bodies in Japan bundle devices and pack specifications, streamlining supplier onboarding but tightening price points. Diagnostic labs and imaging centers specify anti-static pouches to protect electronics during inter-facility transit.

Home-health providers request child-safe closures and clear instructions decoded into local languages to reduce misuse. Consolidators with sterile-pack lines across China and Malaysia can serve multiple OEMs, capturing scale benefits that bolster competitiveness in the Asia-Pacific medical devices packaging market. End-user diversification requires converters to maintain flexible production cells that can swing between implant trays and moisture-barrier pouches within short changeover windows.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Packaging Level: Tertiary Growth Reflects Distribution Evolution

Primary packs made direct contact with devices and retained a 52.01% share in 2025; nonetheless, tertiary packaging is rising 7.86% as e-commerce permeates medical supply. Cartons now integrate shock sensors and temperature indicators to certify parcel integrity during last-mile delivery. The Asia-Pacific medical devices packaging market size invested in tertiary solutions is expected to reach USD 3.93 billion by 2031.

Secondary packs provide regulatory labeling and logistical barcodes, increasingly printed in dual languages for cross-border movement inside ASEAN. CCL Industries’ 2024 launch of NFC-equipped tertiary shippers allows hospitals to confirm receipt and temperature compliance via smartphone. Even primary blisters adopt serialized 2D codes to link with outer-carton identifiers, extending traceability through all packaging levels, a prerequisite for future automated recalls in the Asia-Pacific medical devices packaging market.

Geography Analysis

China accounted for 21.98% of 2025 revenue, supported by Made in China 2025 subsidies and integrated supply chains anchoring raw resin through device assembly in single industrial zones. IoT-centric smart pack pilots clustered around Shenzhen leverage domestic sensor manufacturers, enhancing localization advantages. Healthy China 2030 programs expand rural clinics, broadening distribution footprints and elevating tertiary packaging needs that withstand multi-leg logistics.

India’s projected 7.99% CAGR mirrors health-infrastructure outlays under the Production Linked Incentive scheme worth INR 9,400 crore (USD 1.13 billion). Mumbai and Bangalore incubators adapt pharmaceutical blister know-how to sterile device trays, lowering validation lead-times. Central government initiatives to harmonize state-level device rules simplify pack compliance, drawing foreign converters to establish sterilization lines near emerging MedTech clusters.,

Japan, South Korea and Australia form a mature triad that emphasizes premium sustainability credentials, pushing converters toward bio-based resins and closed-loop recycling pilots. Japan’s serialization mandate for Class III devices catalyzes label-printer upgrades, while South Korea’s digital-health ecosystem demands cloud-linked NFC tags. Australia’s remote geography enforces stringent drop-test and vibration standards to protect devices traversing interstate trucking. These high-spec markets serve as proving grounds before roll-out across emerging Southeast Asian countries, reinforcing innovation circulation within the Asia-Pacific medical devices packaging market.

Competitive Landscape

Global majors such as Amcor, Sealed Air, and DuPont defend their share with proprietary barrier films, integrated sterilization labs, and multi-country regulatory teams. Regional converters gain ground by aligning with local OEM cost targets and offering shorter lead times. Acquisition activity accelerated in 2024 when DuPont bought European sterile-pack assets for USD 340 million to expand Tyvek production in Singapore and Malaysia. Sealed Air’s tie-up with Sensoro delivers cold-chain smart cartons, demonstrating cross-sector collaboration as a competitive lever.

Patent offices recorded 127 smart-pack applications in 2024, covering antimicrobial coatings and RFID-linked cloud dashboards.[3]World Intellectual Property Organization, “Medical Packaging Patent Filings 2024,” wipo.int Start-ups employ direct-to-manufacturer e-commerce portals to bypass distributor mark-ups, pressuring legacy supply chains. ISO 11607 testing capability remains a gatekeeper; converters without in-house labs partner with contract research organizations, while vertically integrated players leverage test data to secure multi-year sterile barrier contracts in the Asia-Pacific medical devices packaging market.

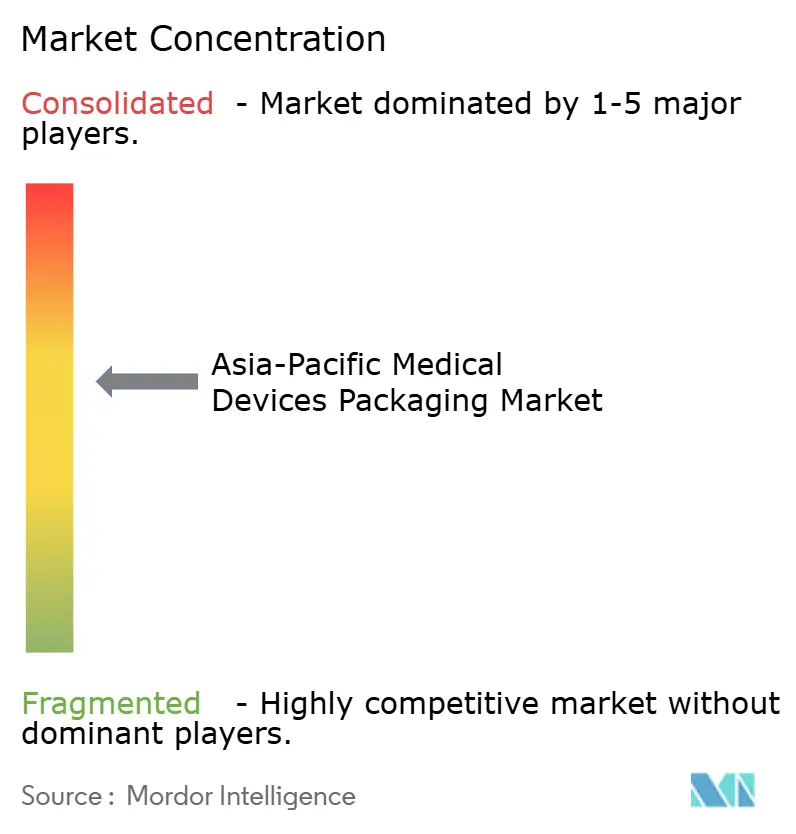

Market power is moderate: the top five suppliers capture roughly a 45% share, leaving ample room for regional specialists. Sustainable material capacity and serialization technology are the chief differentiators guiding 2025 bid evaluations. Consequently, strategy hinges on dual investment—expanding renewable-resin extrusion lines and embedding digital traceability features—to maintain relevance in the Asia-Pacific medical devices packaging market.

Asia-Pacific Medical Devices Packaging Industry Leaders

Amcor Plc

DuPont de Nemours, Inc.

Mitsubishi Chemical Group Corp.

Smurfit WestRock

Sonoco Products Company

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- July 2025: Amcor inaugurated an advanced coating facility in Selangor, Malaysia, the first in Asia to employ air-knife technology for precision water-based coatings used on both the top and bottom webs of sterile medical device packs, creating an integrated one-stop regional supply hub.

- April 2025: Nelipak expanded its Asia-Pacific medical-packaging operations by adding regional commercial and technical teams and introducing new sterile-barrier roll-stocks, lids, and pouches tailored to healthcare customers across China, Japan, and Southeast Asia.

- April 2025: Amcor completed an all-stock combination with Berry Global, forming a larger global supplier with expanded flexible and rigid healthcare-packaging capacity and identifying USD 650 million in cost-synergy opportunities to be captured by FY 2028.

- January 2025: DuPont opened submissions for its second annual Tyvek Sustainable Healthcare Packaging Awards, encouraging device makers and hospitals in the Asia-Pacific to showcase measurable carbon-reduction achievements using Tyvek sterile-barrier materials.

Asia-Pacific Medical Devices Packaging Market Report Scope

Medical devices are pivotal in diagnosing and treating diseases, enhancing the quality of life for those with disabilities. Equally critical is the packaging of these devices. Subpar packaging can lead to significant issues for manufacturers and healthcare facilities alike. The report provides a holistic evaluation of the market.

The Asia-Pacific medical devices packaging market is segmented by packaging type (plastic containers, glass containers, lids, pouches, wrap films, and paper cans) and geography (China, Japan, India, Australia, and the Rest of Asia-Pacific). The market size and forecasts are provided in terms of value (USD) for all the above segments.

By Material

| Plastics |

| Paper and Paperboard |

| Metals and Foils |

| Glass |

| Bio-based Plastics |

By Product Type

| Pouches and Bags |

| Trays and Containers |

| Boxes and Cartons |

| Blister Packs |

| Other Product Types |

By Application

| Sterile Packaging |

| Non-sterile Packaging |

| Active / Smart Packaging |

By End User

| Hospitals and Clinics |

| Diagnostic and Imaging Centers |

| Home Healthcare |

| Contract Manufacturing and Sterilization Organization |

By Packaging Level

| Primary |

| Secondary |

| Tertiary |

By Country

| China |

| Japan |

| India |

| South Korea |

| Australia |

| Rest of Asia-Pacific |

| By Material | Plastics |

| Paper and Paperboard | |

| Metals and Foils | |

| Glass | |

| Bio-based Plastics | |

| By Product Type | Pouches and Bags |

| Trays and Containers | |

| Boxes and Cartons | |

| Blister Packs | |

| Other Product Types | |

| By Application | Sterile Packaging |

| Non-sterile Packaging | |

| Active / Smart Packaging | |

| By End User | Hospitals and Clinics |

| Diagnostic and Imaging Centers | |

| Home Healthcare | |

| Contract Manufacturing and Sterilization Organization | |

| By Packaging Level | Primary |

| Secondary | |

| Tertiary | |

| By Country | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the 2026 value of Asia-Pacific medical devices packaging?

The segment is valued at USD 15.11 billion in 2026 with a forecast 6.79% CAGR to 2031.

Which material dominates current pack demand?

Plastics maintain 54.78% share due to cost-efficiency and broad sterilization compatibility.

How fast are bio-based plastics growing?

Bio-based plastics are projected at 7.78% CAGR, outpacing overall market growth.

Which country leads regional demand?

China holds 21.98% share, leveraging integrated manufacturing clusters and export support.

What application is expanding the fastest?

Active and smart packaging leads with an 7.9% CAGR as IoT sensors integrate into sterile packs.

What is driving tertiary packaging growth?

E-commerce and direct-to-patient deliveries push tertiary packs to a 7.86% CAGR through 2031.