Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

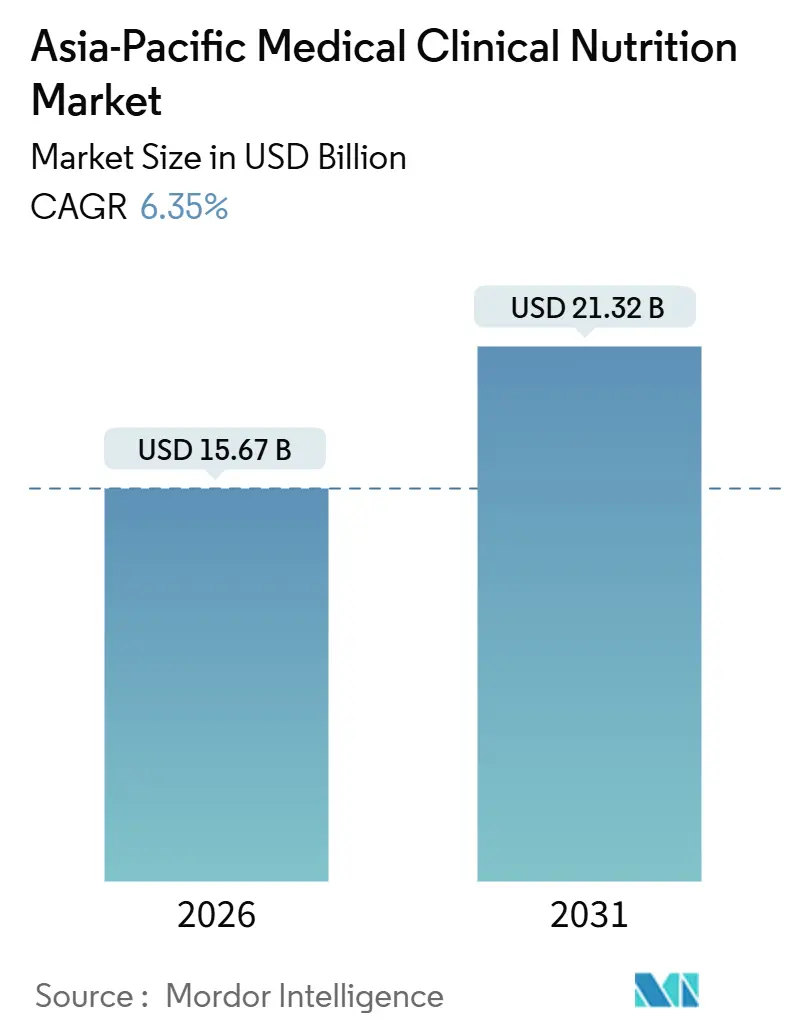

| Market Size (2026) | USD 15.67 Billion |

| Market Size (2031) | USD 21.32 Billion |

| Growth Rate (2026 - 2031) | 6.35% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Medical Clinical Nutrition Market Analysis by Mordor Intelligence

The Asia-Pacific Medical Clinical Nutrition Market size is estimated at USD 15.67 billion in 2026, and is expected to reach USD 21.32 billion by 2031, at a CAGR of 6.35% during the forecast period (2026-2031).

Clinical demand is being reshaped by the rapid aging of the population, a mounting metabolic disease burden, and the relocation of parenteral nutrition production to regional plants that shorten cold-chain routes. Hospitals are scaling precision-compounded total parenteral nutrition, while home-care programs that rely on smart pumps and telehealth are broadening outpatient access. Governments in China, India, and Vietnam now mandate nutrition screening upon admission, creating a consistent demand for specialty formulas. Meanwhile, manufacturers with ISO-certified regional facilities are trimming lead times by 50% and winning tenders that favor supply-chain resilience.

Key Report Takeaways

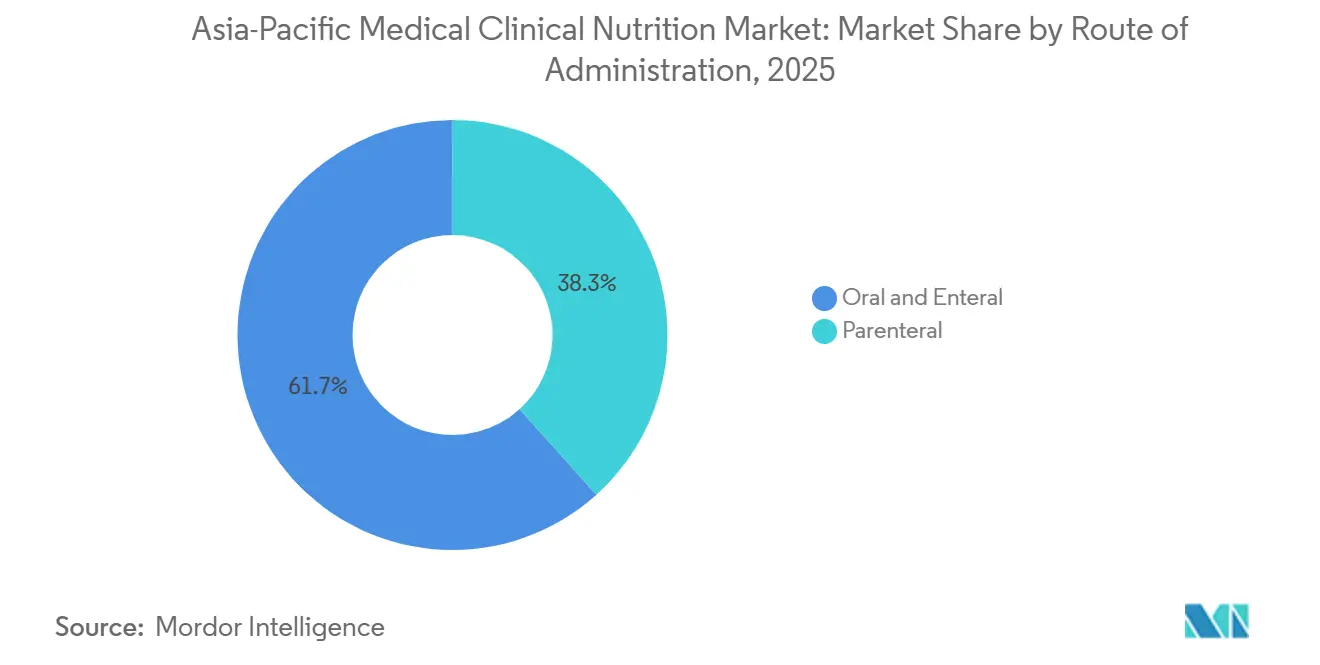

- By route of administration, oral and enteral products held 61.68% of Asia-Pacific medical clinical nutrition market share in 2025; parenteral solutions are projected to grow fastest at a 9.32% CAGR through 2031.

- By application, the cancer segment is forecast to expand at a 9.93% CAGR through 2031, while malnutrition remains the largest category, with a 26.73% revenue share in 2025.

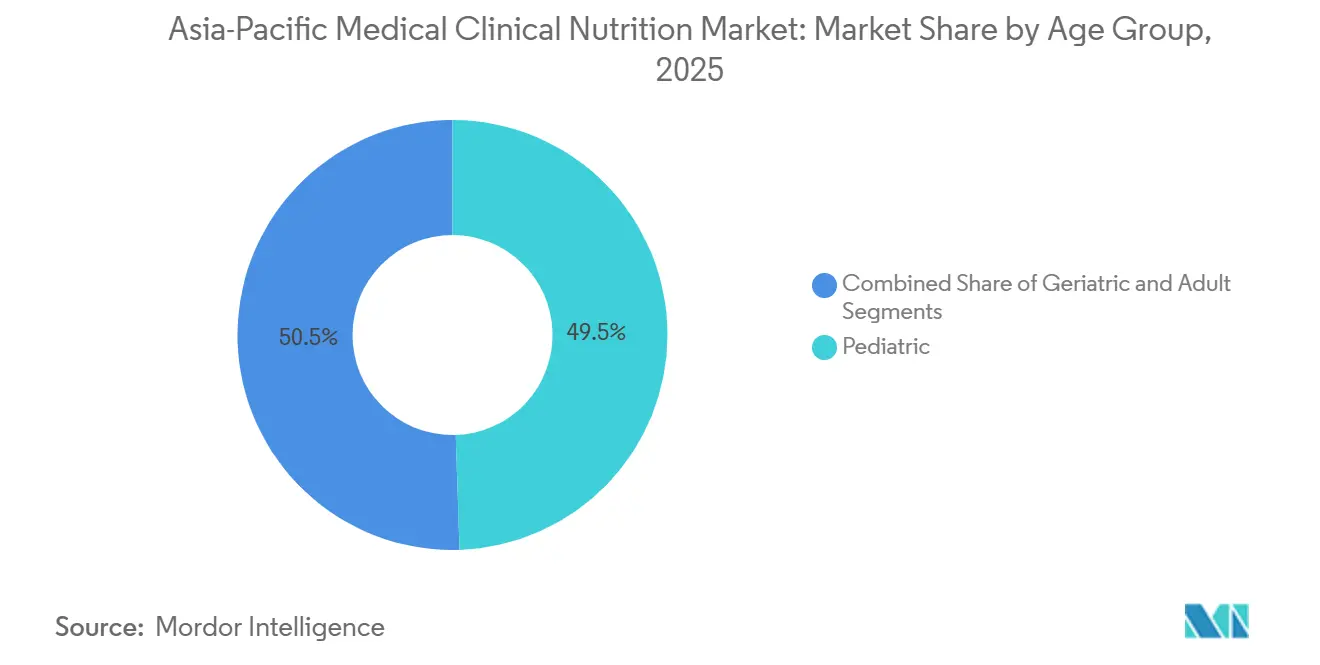

- By age group, pediatric formulas accounted for a 49.48% share of the Asia-Pacific medical clinical nutrition market size in 2025, and geriatric formulas are projected to advance at an 8.15% CAGR through 2031.

- By distribution channel, hospitals led with 46.41% of the revenue in 2025; online and home-care providers are expected to grow at an 11.76% CAGR through 2031.

- By country, China captured 35.06% of the Asia-Pacific medical clinical nutrition market size in 2025, whereas India is anticipated to post the highest CAGR of 10.69% over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Medical Clinical Nutrition Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Metabolic & Chronic Diseases | +1.8% | Global, with peak intensity in China, India, and Southeast Asia | Medium term (2-4 years) |

| Expanding Geriatric Population | +1.5% | Japan, South Korea, Australia, with spillover to urban China | Long term (≥ 4 years) |

| Growing Healthcare Spending & Middle Class | +1.2% | India, Indonesia, Vietnam, Philippines | Medium term (2-4 years) |

| Home-Based Nutrition Uptake Via Smart Pumps & Telehealth | +0.9% | Australia, Singapore, Japan, South Korea | Short term (≤ 2 years) |

| HEOR Evidence Shaping Reimbursement | +0.6% | Australia, Japan, South Korea, Taiwan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Metabolic and Chronic Diseases

Hospital caseloads of diabetes, renal failure, and metabolic syndrome are swelling, with regional diabetes prevalence projected to rise from 295.8 million in 2021 to 411.7 million by 2045.[1] International Diabetes Federation, “IDF Diabetes Atlas 10th Edition,” diabetesatlas.org Many patients now present at younger ages, lengthening lifetime dependence on medical nutrition. Singapore’s 2024 chronic disease initiative, which combines continuous glucose monitoring with dietitian-led counseling, is already showing improvements in adherence metrics. South Korea has documented a parallel uptick in metabolic syndrome admissions requiring intravenous amino acid solutions. Formulas fortified with branched-chain amino acids, omega-3 fatty acids, and fiber blends are therefore displacing standard polymeric products in critical-care wards. Hospitals that integrate proactive metabolic-nutrition pathways report shorter stays and lower readmission bills, reinforcing payer support for specialized products.

Expanding Geriatric Population

The share of residents aged 60 plus is on track to double to 22.9% by 2050 in Southeast Asia.[2]World Health Organization, “Ageing and Health in South-East Asia,” who.int Sarcopenia, dysphagia, and polypharmacy are boosting the need for hyper-protein, texture-modified formulas. Japan’s 2024 long-term care reforms fund home enteral regimens that can be stored at room temperature, thereby increasing demand in rural prefectures. Eleven nations endorsed the Colombo Declaration on Healthy Ageing, pledging routine nutrition screening in primary care. Updated Chinese guidelines now recommend 1.2-1.5 g of protein per kilogram for frail seniors, up from 1.0 g, which raises per-capita formula volumes.

Growing Healthcare Spending and Middle-Income Expansion

Higher disposable incomes are prompting families to self-fund disease-specific nutrition where insurance coverage is limited. Private hospital chains in India and Indonesia employ nutrition support teams in oncology and intensive-care units, creating steady institutional orders. India’s 2023 device-rule amendments halved approval time for feeding pumps, easing market entry for suppliers. Vietnam’s 2025 mandate for malnutrition screening within 24 hours of admission is set to double diagnosis rates and related procurement. Regional manufacturing by Abbott and Fresenius Kabi trims landed costs by 20% to 30%, aligning products with price-sensitive buyers.

Home-Based Nutrition Uptake Via Smart Pumps and Telehealth

Remote monitoring pilots in New South Wales demonstrated a 35% reduction in catheter infections and a 28% decrease in readmissions by linking Bluetooth pumps to hospital dashboards.[3]Health NSW, “Remote Patient Monitoring Pilot for Home Parenteral Nutrition,” health.nsw.gov.au Singapore’s tele-nutrition program, launched in 2025, combines dietitian chats with glucose analytics, resulting in a 40% increase in supplement adherence. New Zealand has earmarked USD 90 million for telehealth networks to reach rural tube-feeding patients. Reimbursement codes in Japan now cover virtual nutrition consults, encouraging hospitals to shift stable patients to home care and freeing bed capacity.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inconsistent Reimbursement Across APAC | -1.2% | Indonesia, Philippines, Vietnam, Thailand | Medium term (2-4 years) |

| Low Inventory Appetite in Hospital Pharmacies | -0.8% | China, India, Southeast Asia | Short term (≤ 2 years) |

| Counterfeit Products in Emerging ASEAN Markets | -0.5% | Indonesia, Philippines, Vietnam | Medium term (2-4 years) |

| Shortage of Precision-Nutrition Dietitians | -0.6% | India, Indonesia, rural China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Inconsistent Reimbursement Across APAC

Only 40% of regional governments fund home enteral nutrition. Cash-pay reliance forces caregivers to prepare blenderized feeds that risk microbial contamination. Thailand lifted reimbursement caps in 2024, yet still covers just 60% of standard-formula costs, excluding premium disease-specific variants. India’s flagship health insurance plan omits the enteral and parenteral categories, limiting its penetration to urban households with annual incomes above USD 5,000. Manufacturers, therefore, run dual portfolios, releasing value-engineered lines priced below USD 2 per serving for cash markets while reserving premium immunonutrition for reimbursed systems in Japan and Australia.

Low Inventory Appetite in Hospital Pharmacies

Just-in-time policies have reduced clinical-nutrition stock levels by up to 40% in Chinese tertiary hospitals, shifting the expiry risk to suppliers. Group-purchasing contracts across India and Vietnam now demand consignment inventory with 90-day payment terms, squeezing distributor margins. Heat-sensitive lipid emulsions complicate storage in tropical zones prone to power outages. Vendors that offer RFID-enabled vendor-managed inventory Fresenius Kabi and Baxter most notably are winning tenders but must carry extra buffer stock. Regional compounding hubs operated by Abbott in Singapore and Kelun Pharma in Sichuan allow 48-hour order-to-delivery windows, easing pharmacy concerns over shelf life.

Segment Analysis

By Route of Administration – Parenteral Uptake Accelerates Amid Enteral Dominance

Enteral formats held 61.68% of Asia-Pacific medical clinical nutrition market share in 2025, reflecting affordability and compatibility with functional gastrointestinal tracts. Nevertheless, parenteral formulations are posting a 9.32% CAGR due to rising ICU admissions and the broader use of automated compounding, which reduces contamination to 0.1%. China’s 2024 device-approval reforms enabled domestic three-chamber bags to reach hospitals a year faster than before, reducing reliance on imports. Hospitals across Japan and South Korea are transitioning from manual mixing to premixed multi-chamber bags, which are delivered within 48 hours, thereby decreasing pharmacy labor and waste. Enteral innovation continues, with thickened “jelly” formats mitigating aspiration risk in dysphagic elders while oral immunonutrition shortens surgical stays by 2.5 days.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application – Oncology Nutrition Leads Growth Curve

Malnutrition remained the most significant indication at 26.73% revenue share in 2025, yet oncology formulas are expanding at 9.93% CAGR as 40%-80% of cancer inpatients present undernourished. China’s nationwide audit revealed only 38% of malnourished oncology patients received dedicated intervention, underscoring a sizeable treatment gap. Japan cleared three new perioperative immunonutrition products in 2025, accelerating specialty launches across the region. Formulas targeting inflammatory bowel disease, chronic kidney disease, and liver disorders continue to generate stable demand, while exclusive enteral nutrition achieved a 60% remission rate in pediatric Crohn’s cohorts in 2025.

By Age Group – Geriatric Demand Narrows the Pediatric Lead

Pediatric solutions accounted for 49.48% of Asia-Pacific medical clinical nutrition market size in 2025, driven by high stunting rates and the rollout of therapeutic feeding programs in India and Indonesia. Amino-acid formulas show 90% tolerance in cow's milk protein allergy, supporting premium pricing. Geriatric demand is catching up, growing at an 8.15% CAGR as Japan’s super-aged population and South Korea’s long-term care insurance subsidize high-protein blends. China’s 2022 guideline update, which lifts protein targets for frail seniors, is further boosting per-capita intake.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel – Online and Home-Care Gain Momentum

Hospitals accounted for 46.41% of the revenue in 2025; however, online and home-care providers are projected to post a 11.76% CAGR from 2025 to 2031. Telehealth pilots in Australia demonstrated a 35% reduction in infections by linking infusion pumps to hospital dashboards. Singapore’s e-commerce portals now bundle dietitian chat support with next-day delivery, pushing compliance up by 40%. Pharmacies remain critical for over-the-counter oral supplements, while nursing homes in Japan and South Korea are expanding reimbursed purchases under revisions to long-term care funding.

Geography Analysis

China generated 35.06% of Asia-Pacific medical clinical nutrition market size in 2025, buoyed by mandatory nutrition screening in tertiary hospitals and streamlined device approvals that cut parenteral-bag registration to 12 months. By 2035, the aging population, which is expected to comprise 25% of the population over 65, will shift demand toward high-protein geriatric formulas. E-commerce giants JD Health and Alibaba invested USD 50 million in 2025 to establish a cold-chain delivery system for oncology patients, extending their reach beyond tier-1 cities.

India is advancing at a forecasted 10.69% CAGR as local compounding plants launched under the Make in India initiative shorten supply routes and private hospital chains embed nutrition teams. Device-rule amendments in 2023 halved approval timelines for feeding pumps, while state-run child-nutrition programs secure institutional volumes. The absence of coverage under Ayushman Bharat, however, limits broader affordability.

Japan continues to see robust uptake through home medical care. Reimbursement updates in 2024 now cover remote dietitian consultations, which is expected to increase home-based volumes to 30% by 2028. Domestic firms dominate jelly-type formats that mitigate aspiration, and the 2024 Otsuka–ICU Medical joint venture guarantees a 48-hour supply of multi-chamber bags.

Australia, South Korea, and the rest of the APAC region contribute the remaining share. Australia’s NDIS allotted USD 23 million in 2025 for enteral feeds, standardizing access nationwide. South Korea expanded high-protein sarcopenia coverage in 2025, underpinning geriatric growth. Thailand, Vietnam, and Indonesia continue to widen reimbursement lists, yet caps still require partial out-of-pocket funding.

Competitive Landscape

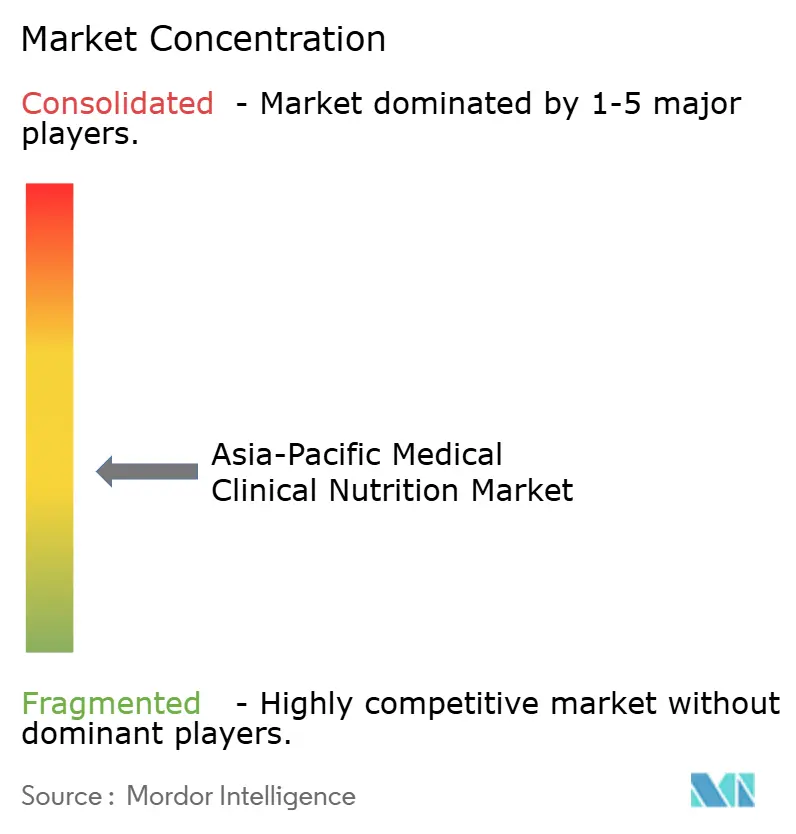

The Asia-Pacific medical clinical nutrition market is moderately concentrated, with key players including Abbott, Fresenius Kabi, Baxter, Nestlé Health Science, and Danone Nutricia. Abbott’s Q3 2024 nutrition sales reached USD 2.1 billion, driven by double-digit gains in the Asia-Pacific region and supported by its Singapore manufacturing hub. Fresenius Kabi booked EUR 1.5 billion in 2024 clinical nutrition revenue and is outfitting ISO Class 5 compounders across India and China to supply patient-specific bags with 0.1% contamination. Otsuka’s 2024 tie-up with ICU Medical unites 16 regional IV-solution plants, slashing lead times for premixed bags to 48 hours.

Local champions are exploiting regulatory agility: Kelun Pharma’s three-chamber launch in 2024 won multiple Chinese tenders, JW Pharmaceutical controls 52.4% of Korea’s parenteral market and began exporting to Mongolia in 2025, and Terumo has bolstered its feeding-pump installation base in Japanese long-term care facilities. Digital disruptors such as JD Health and Apollo Pharmacy are carving B2B2C channels that bypass traditional distribution while offering dietitian services, forcing incumbents to adopt subscription models and direct-to-patient logistics.

Technology leadership is emerging as a key differentiator. RFID-based vendor-managed inventory from Baxter and Fresenius Kabi cuts waste and eases pharmacy cash-flow constraints, often clinching long-term procurement deals despite higher unit prices. Multinationals maintain an edge in the premium oncology and immunonutrition segments, which require extensive clinical dossiers, while regional firms compete aggressively in tender-driven standard formulas.

Asia-Pacific Medical Clinical Nutrition Industry Leaders

Abbott

Baxter

B. Braun SE

Danone Nutricia

Nestlé Health Science

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2025: Glenmark Pharmaceuticals initiated a community nutrition program in the Philippines to improve access among vulnerable groups.

- July 2025: Nestlé introduced Milo Pro, a high-protein ready-to-drink line initially launched in Indonesia with regional expansion planned.

- May 2025: Otsuka Pharmaceutical and ICU Medical finalized a joint venture combining 16 Asia-Pacific IV-solution plants to deliver multi-chamber parenteral bags within 48 hours.

- May 2025: Arla Foods Ingredients extended its protein-ingredient distribution deal with Brenntag to Vietnam, Thailand, and Indonesia, enhancing local supply for medical and sports formulas.

Asia-Pacific Medical Clinical Nutrition Market Report Scope

As per the report's scope, medical clinical nutrition is a specialized field focusing on the assessment, diagnosis, and treatment of nutritional problems in patients. It aims to optimize health and recovery through tailored dietary plans and nutritional support. This discipline addresses conditions like malnutrition, metabolic disorders, and chronic diseases. It plays a vital role in improving patient outcomes and overall well-being.

The Asia-Pacific medical clinical nutrition market is segmented by route of administration (oral and enteral, and parenteral), application (malnutrition, metabolic disorders, gastrointestinal diseases, neurological diseases, cancer, and other diseases), end-user (pediatric and adult), distribution channel (pharmacies, hospitals, nursing homes, and others) and geography (China, Japan, India, Australia, South Korea, Rest of Asia-Pacific). The report offers values in USD for the abovementioned segments.

By Route of Administration

| Oral & Enteral |

| Parenteral |

By Application

| Malnutrition |

| Metabolic Disorders |

| Gastrointestinal Diseases |

| Neurological Diseases |

| Cancer |

| Other Diseases |

By Age Group

| Pediatric |

| Adult |

| Geriatric |

By Distribution Channel

| Hospitals |

| Pharmacies & Drug Stores |

| Nursing Homes & Long-Term Care |

| Online & Home-Care Providers |

By Country

| China |

| Japan |

| India |

| Australia |

| South Korea |

| Rest of Asia-Pacific |

| By Route of Administration | Oral & Enteral |

| Parenteral | |

| By Application | Malnutrition |

| Metabolic Disorders | |

| Gastrointestinal Diseases | |

| Neurological Diseases | |

| Cancer | |

| Other Diseases | |

| By Age Group | Pediatric |

| Adult | |

| Geriatric | |

| By Distribution Channel | Hospitals |

| Pharmacies & Drug Stores | |

| Nursing Homes & Long-Term Care | |

| Online & Home-Care Providers | |

| By Country | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the forecast value of the Asia-Pacific medical clinical nutrition market in 2031?

The market is projected to be valued at USD 21.32 billion by 2031, growing at a 6.35% CAGR from 2026.

Which segment is expanding fastest within clinical nutrition applications?

Oncology-focused nutrition formulas are the fastest-growing, with a 9.93% CAGR expected through 2031.

How is home-based nutrition influencing market growth?

Bluetooth pumps, telehealth consults, and e-commerce deliveries are pushing the home-care channel to an 11.76% CAGR, reducing hospital reliance and widening access.

Why are parenteral products gaining traction despite enteral dominance?

Intensive-care complexity and automated compounding systems that lower contamination drive a 9.32% CAGR for parenteral solutions.

Which country leads regional revenue and which is growing fastest?

China held 35.06% of revenue in 2025, while India is predicted to record the highest 10.69% CAGR to 2031.