Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 165.79 Billion |

| Market Size (2031) | USD 218.21 Billion |

| Growth Rate (2026 - 2031) | 5.65% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Luxury Goods Market Analysis by Mordor Intelligence

The Asia-Pacific Luxury Goods Market size in 2026 is estimated at USD 165.79 billion, growing from 2025 value of USD 156.93 billion with 2031 projections showing USD 218.21 billion, growing at 5.65% CAGR over 2026-2031. Sustained expansion reflects deep-seated demographic shifts, with India and Southeast Asia adding large cohorts of first-time affluent shoppers, and a gradual growth in demand for jewelry products. According to the World Gold Council, the demand for gold across India was about 803 metric tons in 2024. This represented an increase of five percent in comparison to the previous year, when the gold demand was 761 metric tons[1]Source: World Gold Council, "Annual demand volume of gold across India", gold.org. A favorable currency backdrop turns Japan into a regional shopping hub, lifting luxury sales in H1 2024 as tourists capitalize on the weak yen. Younger buyers account for a rising share of expenditure and increasingly value craftsmanship, environmental responsibility, and digital convenience. Brands respond with intensified omnichannel investments, selective price increases, and tighter control of inventory to protect exclusivity while capturing demand swings across geographies.

Key Report Takeaways

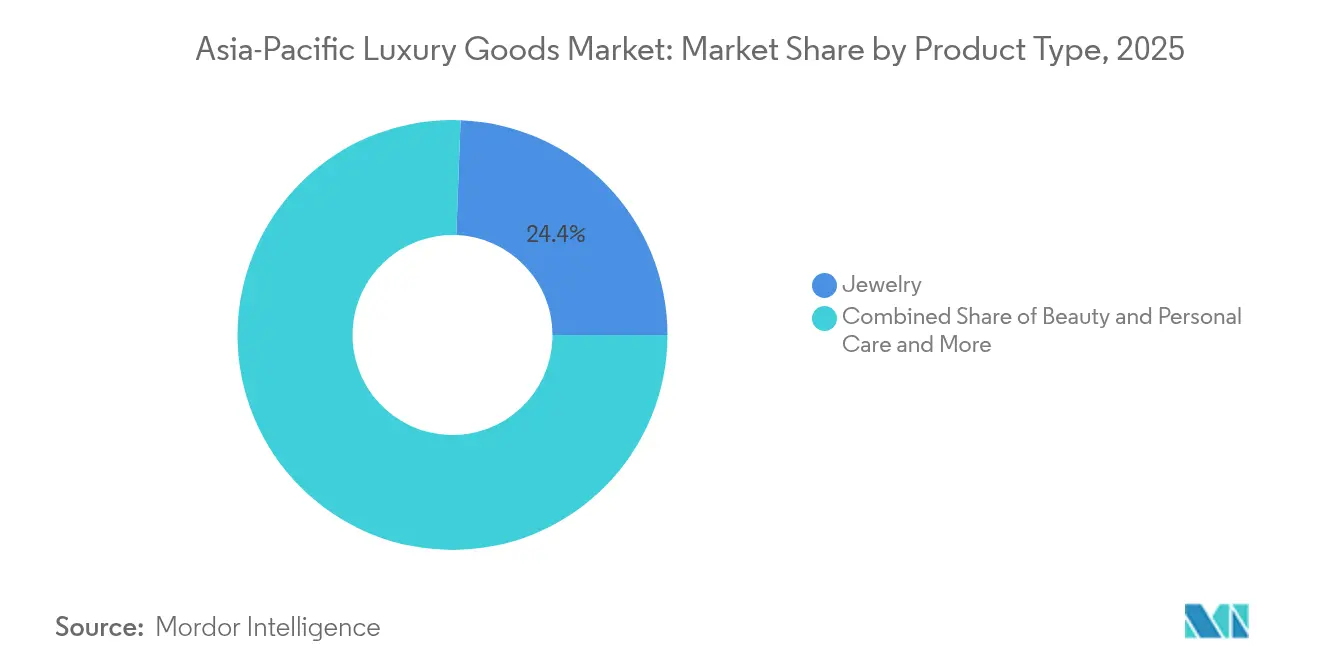

- By product category, jewelry led with 24.40% of the Asia-Pacific luxury goods market share in 2025, while beauty and personal care is projected to record the fastest 6.54% CAGR to 2031.

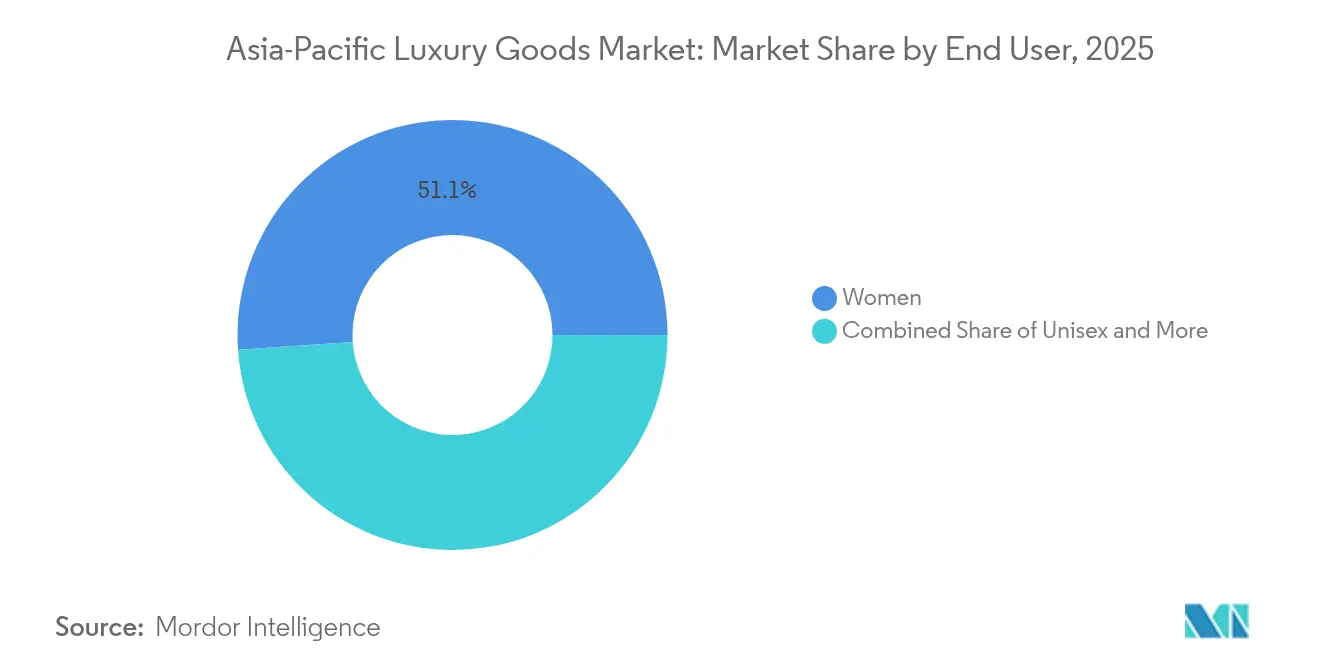

- By end user, women accounted for 51.10% of spending in 2025, and the unisex segment shows the highest 6.05% CAGR outlook through 2031.

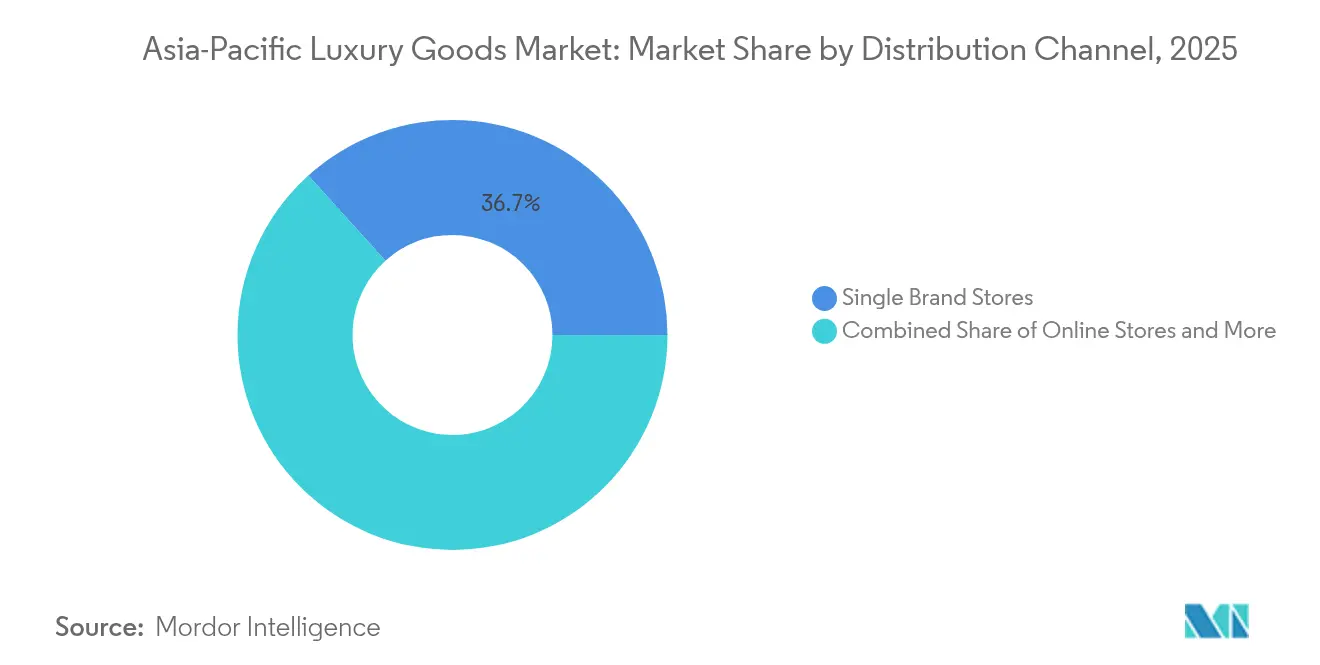

- By distribution channel, single-brand stores commanded 36.70% of revenue in 2025, but online stores are expected to post the strongest 9.32% CAGR to 2031.

- By geography, China retained a 40.70% share in 2025, whereas India is set to expand at a 5.98% CAGR and emerge as the fastest-growing market through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Luxury Goods Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Brand Consciousness and Premiumization | +1.2% | Global, with the strongest impact in China, India, and Southeast Asia | Medium term (2-4 years) |

| Sustainability and Ethical Preferences | +0.8% | Global, particularly strong in Japan, Australia, and Singapore | Long term (≥ 4 years) |

| Product Innovation and Customization | +0.9% | Global, with emphasis on Japan, South Korea, and China | Short term (≤ 2 years) |

| Technology Integration in Retail | +1.1% | Global, led by China, South Korea, and Japan | Short term (≤ 2 years) |

| Tourism and Duty-Free Shopping | +0.7% | Japan, Thailand, Singapore, and Hong Kong | Medium term (2-4 years) |

| Growth of Aspirational Consumers and Younger Demographics | +1.0% | India, Southeast Asia, and China (lower-tier cities) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Brand Consciousness and Premiumization

The premiumization wave across Asia-Pacific reflects a sophisticated evolution beyond traditional status signaling toward quality-driven consumption. Chinese consumers increasingly favor high-quality products without prominent logos, indicating a maturation from conspicuous to conscious luxury consumption. This behavioral shift creates opportunities for heritage brands that emphasize craftsmanship over brand visibility, while challenging newer entrants reliant on logo-centric strategies. Government policy and tourism flows amplify that premiumisation: China’s central and trade ministries have rolled out consumption-support measures and duty-free enhancements (the “International Consumption Season” and downtown duty-free policy changes) that boosted discretionary spending and duty-free luxury pull in 2024–25, while Japan’s rapid inbound tourism recovery in 2024 materially raised tourist spending on high-end goods, both effects favour premium/luxury sales concentrated in core shopping destinations. For instance, according to the Japan National Tourism Organization, in 2024, the number of inbound visitors traveling to Japan amounted to approximately 36.87 million, setting a new record[2]Source: Japan National Tourism Organization, "Number of Foreign Visitors to Japan (December 2024 and Annual Estimates), jnto.go.jp.

Sustainability and Ethical Preferences

Driven by heightened environmental awareness, luxury consumption patterns are undergoing a seismic shift. Regulatory frameworks, notably the EU's Corporate Sustainability Due Diligence Directive and Asia-Pacific's emerging ESG reporting mandates, are pushing luxury brands to prioritize transparency in their supply chains and to actively work on reducing their environmental footprints. In Asia, Singapore mandates climate-related disclosures for its listed companies, while Japan has bolstered its ESG reporting requirements. These regulations are not just bureaucratic hurdles; they're reshaping the very strategies of luxury brands. As consumers increasingly show a willingness to pay a premium for sustainable products, brands that champion sustainability are beginning to eclipse their traditional luxury counterparts in market share. This trend is especially pronounced among younger consumers, who are not just seeking luxury but are also championing environmental responsibility. Brands that genuinely weave sustainability into their core values are reaping significant competitive advantages.

Product Innovation and Customization

In the Asia–Pacific luxury goods market, brands are harnessing product innovation and customization to fuel growth and bolster resilience. By tapping into the rising demand for individuality, these brands are not only driving higher-margin sales but also cultivating deeper customer loyalty. Through technical innovations, like new movements, materials, and micro-editions, alongside digital tools and in-store bespoke services, brands are transforming one-off experiences into consistent revenue streams and repeat purchases. Furthermore, by offering limited-run, locally tailored products, they are adeptly defending their price points even in softer macroeconomic conditions. This strategy amplifies the commercial benefits of localized product drops and personalization services, especially as shoppers are increasingly opting for premium, bespoke items either at home or in travel-retail hubs, rather than abroad. Illustrating this trend, Louis Vuitton is set to expand its “Mon Monogram” personalization service in April 2025, broadening customization options across more icons and colorways, allowing customers to co-create uniquely meaningful pieces. Similarly, Omega's June 2025 launch of the Aqua Terra 30mm, featuring new calibres and sizing, underscores the brand's strategy of engineering products for specific demographics, like younger buyers and women's categories, while also emphasizing personalization to rejuvenate desirability.

Tourism and Duty-Free Shopping

As international travel rebounded post-COVID, affluent tourists increasingly funneled their discretionary spending into arrival and downtown duty-free channels in the Asia-Pacific. These channels, known for high-margin purchases and impulse buys, played a pivotal role in helping brands recover top-line sales, even amidst a dip in local consumption. This trend was further bolstered by government policy shifts. For instance, China's 2024 expansion of downtown duty-free zones and the widening of eligible shoppers (set to take effect in October 2024) were strategic moves to channel more spending into domestic duty-free outlets. This not only amplified on-shore luxury sales but also nudged brands to prioritize their travel-retail assortments. Meanwhile, Japan's tourism resurgence, marked by record arrivals in 2024 and upcoming reforms to tax-free shopping in 2025, spurred a surge in travel-retail purchases. This momentum justified brands' decisions to roll out larger, travel-exclusive launches and invest in in-store experiences.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit Products and Brand Dilution | -0.6% | Global, particularly severe in China and Southeast Asia | Medium term (2-4 years) |

| Intense Competition | -0.4% | Global, most pronounced in mature markets like Japan, Hong Kong | Short term (≤ 2 years) |

| Sustainability Costs and Practices | -0.3% | Global, with higher impact in regulated markets like Singapore and Australia | Long term (≥ 4 years) |

| Regulatory and Compliance Challenges | -0.5% | Varies by jurisdiction, strongest in China, India, and Indonesia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Counterfeit Products and Brand Dilution

Despite bolstered enforcement mechanisms and tech solutions, luxury brands in the Asia-Pacific grapple with persistent intellectual property violations. Brands are increasingly turning to blockchain authentication and digital verification systems as part of their anti-counterfeiting investments. However, these sophisticated counterfeit operations swiftly adapt, often sidestepping these protective measures. The rise of online marketplaces further complicates brand protection, demanding constant monitoring and enforcement. This not only escalates operational costs but also diverts resources from growth pursuits. Moreover, uneven intellectual property enforcement across regions adds layers of compliance challenges, pushing brands to tailor their protection strategies for each jurisdiction. As counterfeit sophistication outpaces traditional authentication, educating consumers becomes paramount. This urgency drives brands to bolster investments in customer awareness initiatives and advanced verification technologies.

Intense Competition

As established luxury segments reach saturation, brands are pivoting towards innovation and enhanced customer experiences to stand out, moving away from conventional positioning strategies. In South Korea and India, a clear polarization in the luxury market emerges: elite brands such as Hermès, Louis Vuitton, and Chanel are celebrating record sales, while their mid-range counterparts grapple with significant downturns. This trend underscores a shift in consumer preferences, gravitating towards either the ultra-premium or the more accessible luxury tiers. The Ministry of Corporate Affairs in India highlighted that in the fiscal year 2023, luxury giant Louis Vuitton raked in over INR 7 billion in revenue, marking a notable 33% surge from the prior year. Meanwhile, digital disruption is leveling the playing field, allowing newcomers to directly challenge established brands via direct-to-consumer strategies and savvy social media marketing, effectively dismantling traditional market entry barriers. While price wars are rare in the luxury realm, brands are increasingly compelled to showcase their worth through superior services, unique experiences, and innovative products. Notably, the competitive landscape is not uniform; the beauty and personal care sector witnesses a more vigorous rivalry compared to the traditional luxury goods market.

Segment Analysis

By Product Type: Jewelry Dominance Amid Beauty Acceleration

In 2025, Jewelry holds the largest market share at 24.40%, underscoring the Asia-Pacific's deep-rooted cultural ties to precious metals and gemstones, both as symbols of status and means of wealth preservation. Meanwhile, the Beauty and Personal Care segment is on a rapid ascent, boasting a 6.54% CAGR projected through 2031. This surge is fueled by a trend towards premiumization and a growing consumer sophistication in skincare and cosmetics. Notably, the Asia-Pacific beauty market commands a significant slice of the global pie, with digital sales poised to make significant inroads in China by 2027.

While Clothing and Apparel grapple with a shift in consumer focus towards experiential luxury, Footwear is riding high on the wave of athleisure trends and a burgeoning premium sneaker culture among younger audiences. Eyewear is witnessing consistent growth, buoyed by a blend of fashion-forward designs and a rising demand for luxury prescription eyewear. Leather Goods are thriving, especially in markets like South Korea, where sales of luxury handbags are on the rise, paralleling those of jewelry and timepieces. Department stores in the region are also noting upticks in luxury accessory sales. This evolving landscape hints at a broader shift: a move towards functional luxury and tailored beauty solutions, as traditional markers of status adapt to the changing values and lifestyles of consumers across the diverse Asia-Pacific region.

Note: Segment shares of all individual segments available upon report purchase

By End User: Women Lead While Unisex Accelerates

In 2025, women account for 51.10% of luxury goods demand in the Asia-Pacific, maintaining their dominance in categories like jewelry, beauty, and fashion accessories. Unisex categories, however, are growing fastest, with a 6.05% CAGR through 2031, driven by younger consumers and shifting gender norms. South Korean data highlights this trend, with Gen Z favoring gender-neutral fashion and accessories, prioritizing personal expression over traditional gendered luxury.

Men's luxury consumption is rising steadily in watches, leather goods, and grooming products, reflecting growing interest in self-care. A 2025 Hot Pepper Beauty Academy survey found 54.2% of Japanese men in their twenties visited beauty parlors in the past year. Japan also shows increased male participation in luxury fashion and accessories, supported by cultural shifts toward individual expression. Unisex segment growth is bolstered by brands focusing on inclusive design and marketing, appealing to consumers who value versatility and authenticity. These shifts push luxury brands to adapt strategies to meet evolving consumer preferences across the Asia-Pacific region.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Single Brand Stores Prevail as Online Surges

In 2025, Single Brand Stores secured a 36.70% distribution share, solidifying their status as the top choice for luxury retail across the Asia-Pacific. This stronghold underscores luxury brands' commitment to curated brand experiences and top-tier service, especially in regions where personal ties and service excellence influence buying choices. Meanwhile, online stores are surging ahead with a robust 9.32% CAGR growth rate projected through 2031, fueled by digital transformation and evolving consumer habits. A testament to this shift is LVMH's deepened alliance with Alibaba in May 2024, showcasing a blend of online and offline strategies to elevate luxury shopping. Multi-brand stores, caught between the rise of single-brand outlets and the online boom, are now pivoting towards unique selections and distinct shopping experiences to stand out.

Other Distribution Channels, such as duty-free and airport retail, are reaping the rewards of a tourism resurgence, with 2024 seeing a notable spike in tax-free shopping revenues. Japan stands out, boasting recovery rates that outpace pre-pandemic figures. Given the regional disparities in channel preferences, there's a pressing need for customized distribution strategies. For instance, while China leads the globe in online shopping penetration, Japan still shows a robust inclination towards brick-and-mortar retail.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

China maintained a 40.70% share in 2025, yet its luxury growth slowed to 5.8% amid macro uncertainty and more discerning consumption. Even so, renewed domestic duty-free quotas and mainland store openings anchor long-term leadership. The Asia-Pacific luxury goods market size attached to China could still surpass USD 90.1 billion by 2031 if urbanization and wealth creation persist. Shoppers gravitate toward understated designs and invest more in wellness and home aesthetics, signaling market maturity.

Japan’s sales surge in H1 2024 illustrates currency-driven tourist inflows. Recovery rates for tax-free luxury shopping hit growth rates, underlining the yen’s pull as a spending catalyst. Brands expand Ginza and Osaka footprints, anticipating Expo 2025 visitor spikes. Hong Kong repositions as a cultural destination to regain mainland travelers, while Macau’s luxury casinos roll out personalized VIP retail suites.

India shines as the region’s fastest-growing market with a 5.98% CAGR to 2031. Domestic mall developers allocate prime space to first-time entrants such as Cartier and Prada, targeting an affluent class projected to double by 2030. Southeast Asia contributes steady gains; Thailand benefits from medical tourism, whereas Indonesia’s tax hike tempers near-term momentum but raises government revenue for infrastructure upgrades that ultimately enhance retail ecosystems.

Competitive Landscape

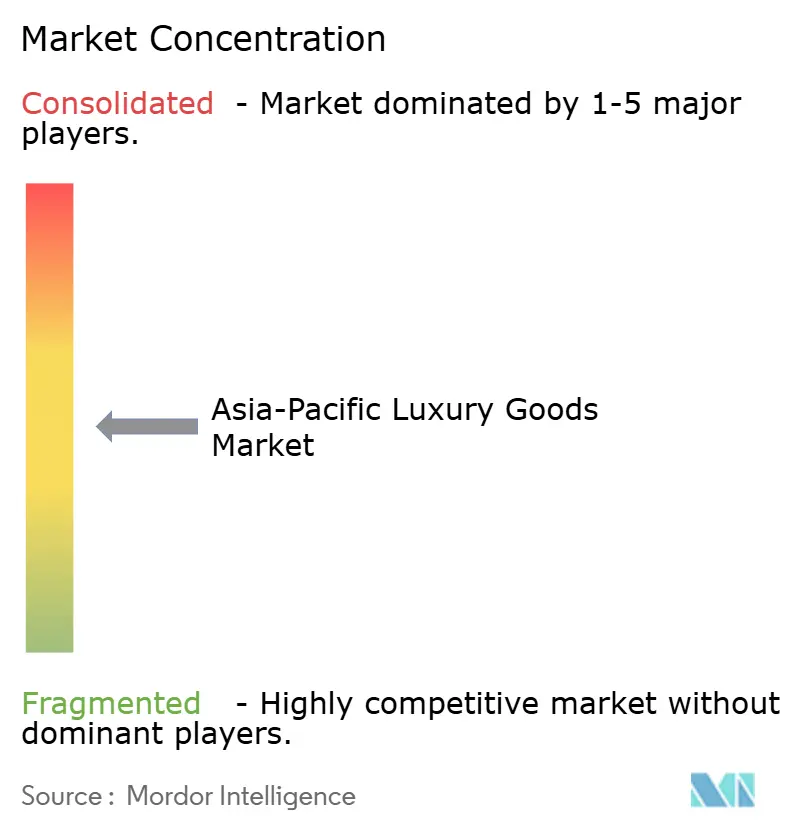

In the Asia-Pacific luxury goods market, a moderate concentration is evident. While LVMH, Kering, and Hermès command a significant revenue pool, their combined share falls short of the 70% mark typically associated with an oligopoly, suggesting room for challengers to emerge. Notably, Hermès bucked the trend, posting a 13% growth in Q2 2024, even as peers grappled with softer market conditions. Meanwhile, the USD 2.7 billion merger that birthed Saks Global underscores a trend of consolidation, driven by the pursuit of enhanced bargaining power and a broader omnichannel presence.

Technology has emerged as the new frontier in this arena. LVMH's bolstered partnership with Alibaba harnesses real-time analytics, fine-tuning client outreach and optimizing product drop schedules. In a similar vein, Richemont is pioneering blockchain technology to ensure the provenance of Cartier diamonds. Kering, on the other hand, is fast-tracking circular economy initiatives via its resale platform, Vestiaire Collective. Regional players like Chow Tai Fook and Titan Company are capitalizing on their domestic insights and nimble decision-making to carve out a larger share in the jewelry and watch segments. While opportunities for entry remain in India's burgeoning market and the rising luxury corridors of Vietnam, success is contingent on a localized approach, balancing pricing, curating festival-specific collections, and selecting culturally resonant brand ambassadors.

The pace of brand popularity is accelerating; platforms like social media can swiftly elevate niche brands, such as Polène, into the limelight. In response, major conglomerates are establishing venture investment divisions as a buffer against the unpredictability of trends. The competition for talent has also intensified: creative directors are now being offered multi-year contracts tied to digital engagement metrics, marking a shift from traditional sales-based performance evaluations.

Asia-Pacific Luxury Goods Industry Leaders

-

Chanel S.A

-

Hermès International S.A

-

Kering S.A.

-

Rolex SA

-

LVMH Moet Hennessy Louis Vuitton SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Breitling launched its Superocean Heritage line and introduced multiple case sizes (36 mm, 40 mm, 42 mm, and 44 mm), with the 40 mm variant becoming the thinnest at just 11.73 mm, making it more wearable for a broader audience. Powered by the in-house B31 automatic calibre with a 70-hour power reserve, the line retained the collection’s distinctive ceramic bezel and retro-inspired dial, but now featured refined lug profiles and enhanced water resistance.

- June 2025: OMEGA launched its women-focused Aqua Terra collection in Kyoto, which signaled OMEGA’s investment in smaller, more refined mechanical watches without compromising on technical mastery. The 12 models featured miniaturized Co-Axial Master Chronometer calibres, Moonshine Gold cases or accents, lacquered pastel dials, and diamond hour markers.

- February 2025: Bianchet revealed its B 1.618 UltraFino watch, which measured just 8.9 mm thick. The watch was launched with a tonneau-shaped titanium case that houses an automatic flying tourbillon movement engineered around the Golden Ratio (1.618). According to the company, the rotor follows a Fibonacci spiral motif, while bridges are sculpted into concentric circular arcs, creating a geometric harmony visible through the sapphire caseback.

- November 2024: To mark its APAC presence, Grand Seiko released an Asia-Pacific limited edition SBGJ285. The model reinterprets the 44GS case aesthetic with a “wisteria”-inspired dial and is explicitly billed as an Asia-Pacific exclusive, a classic example of region-targeted limited editions that leverage local symbolism and collector appeal.

Asia-Pacific Luxury Goods Market Report Scope

A luxury product is an expensive product that solely serves as a status symbol. Higher-income people generally purchase it to flaunt their affluence and gain social prestige. The Asia-Pacific luxury goods market is segmented by type, distribution channel, and geography. Based on type, the market is segmented into clothing and apparel, footwear, bags, jewelry, watches, and other types. Based on distribution channels, the market is segmented into single-brand stores, multi-brand stores, online stores, and other distribution channels. Based on geography, the market is segmented into China, Japan, India, Australia, South Korea, and the rest of Asia-Pacific. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Product Type

| Clothing and Apparel |

| Footwear |

| Eyewear |

| Leather Goods |

| Jewelry |

| Watches |

| Beauty and Personal Care |

By End User

| Men |

| Women |

| Unisex |

By Distribution Channel

| Single Brand Stores |

| Multi Brand Stores |

| Online Stores |

| Other Distribution Channels |

By Geography

| China |

| Japan |

| India |

| Thailand |

| Singapore |

| Indonesia |

| South Korea |

| Australia |

| Rest of Asia-Pacific |

| By Product Type | Clothing and Apparel |

| Footwear | |

| Eyewear | |

| Leather Goods | |

| Jewelry | |

| Watches | |

| Beauty and Personal Care | |

| By End User | Men |

| Women | |

| Unisex | |

| By Distribution Channel | Single Brand Stores |

| Multi Brand Stores | |

| Online Stores | |

| Other Distribution Channels | |

| By Geography | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current value of the Asia Pacific luxury goods market in 2026?

The Asia Pacific luxury goods market is valued at USD 165.79 billion in 2026.

How fast is the luxury segment in India growing?

India is on track for a 5.98% CAGR through 2031—the fastest among regional peers.

Which product category is expanding the quickest?

Beauty and personal care lead with a projected 6.54% CAGR to 2031.

Why are Japan’s luxury sales outperforming?

A weak yen attracts tourists, lifting tax-free shopping to 232% of 2019 levels.

How big is online luxury retail becoming?

Online channels are forecast to post a 9.32% CAGR, approaching parity with department stores by 2031.

What main challenge do luxury brands face in the Asia Pacific?

Counterfeit activity remains a top concern, subtracting an estimated 0.6% from forecast CAGR due to brand dilution.

Page last updated on: