Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

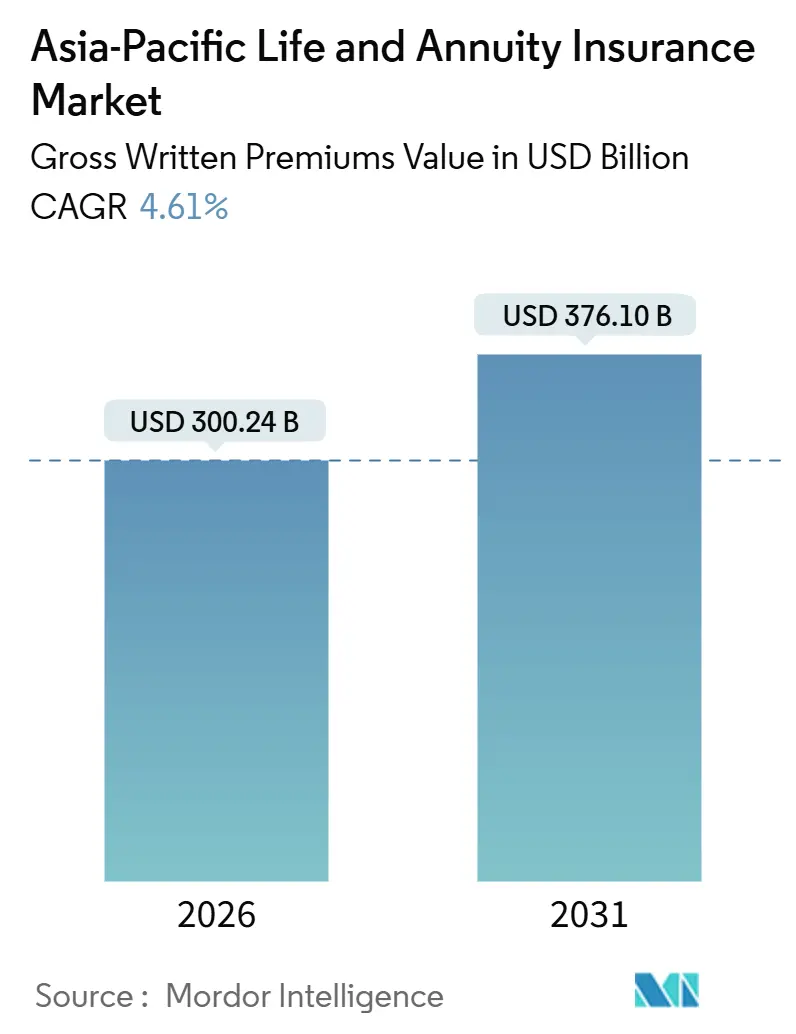

| Market Size (2026) | USD 300.24 Billion |

| Market Size (2031) | USD 376.10 Billion |

| Growth Rate (2026 - 2031) | 4.61% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Life And Annuity Insurance Market Analysis by Mordor Intelligence

The Asia Pacific life annuity insurance market size reached USD 300.24 billion in 2026 and is projected to reach USD 376.1 billion by 2031, expanding at a 4.61% CAGR. Rapid population aging is increasing demand for retirement income solutions, prompting consumers to seek products that provide long-term financial security. At the same time, the widespread adoption of digital tools is reducing acquisition costs and streamlining distribution, making it easier for insurers to reach a broader customer base. Regulatory reforms across the region are also fostering market expansion by encouraging product innovation, opening up capital access, and facilitating more flexible distribution channels. Shifts in product design are further fueling growth, as insurers move away from traditional savings-focused endowments toward risk-oriented term life and annuity products that balance solvency, earnings stability, and consumer preferences for decumulation income. Rising longevity and retirement protection gaps are driving lifetime income features into the mainstream, reflecting increasing consumer awareness of long-term financial needs. Additionally, ecosystem partnerships and embedded distribution models are simplifying market entry for first-time buyers, while insurers’ focus on speed-to-market, data integration, and operational automation is enhancing competitiveness and enabling scalable, profitable growth.

Key Report Takeaways

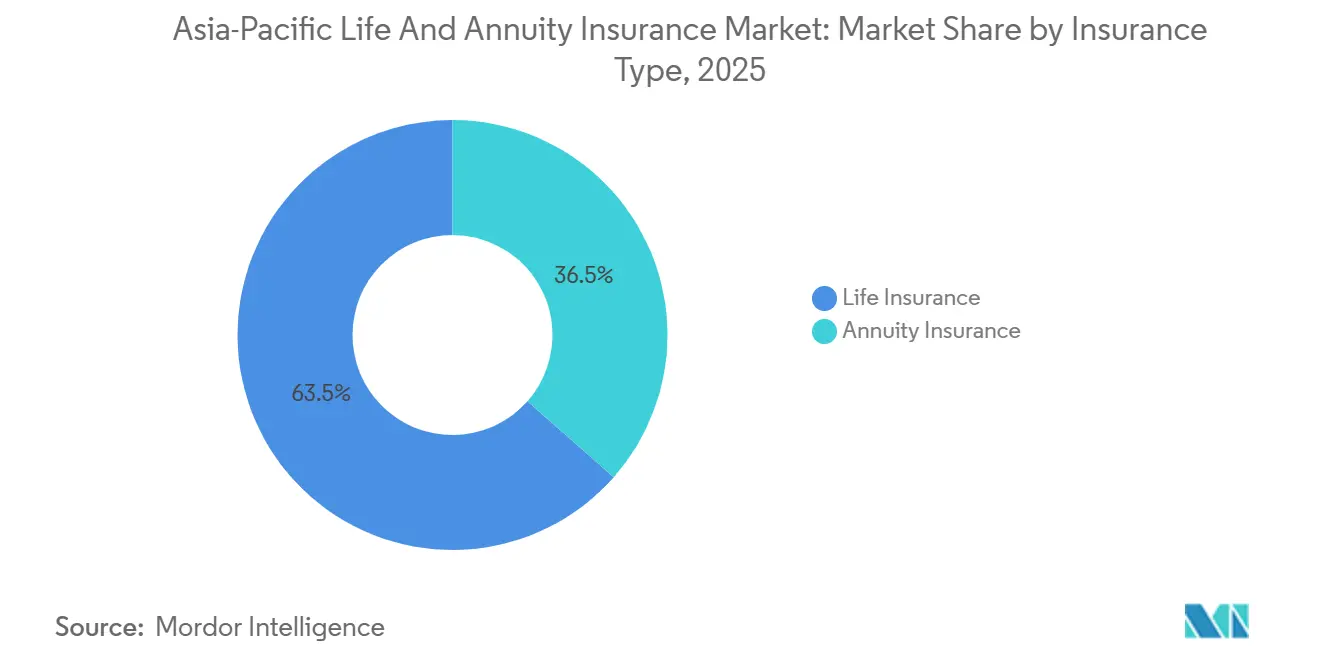

- By insurance type, life insurance led with 63.5% of the Asia Pacific life and annuity insurance market share in 2025 and is projected to expand at a 7.82% CAGR through 2031.

- By distribution channel, brokers and agents held 28.8% of the Asia Pacific life and annuity insurance market share in 2025, while brokers and agents recorded the highest projected CAGR at 5.67% through 2031.

- By geography, India accounted for 34.2% of the Asia Pacific life and annuity insurance market share in 2025 and is advancing at a 7.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Life And Annuity Insurance Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demographic Aging and Retirement Security Demand | +0.9% | Global APAC, highest intensity in Japan, South Korea, Singapore, and China | Long term (≥ 4 years) |

| Rising Disposable Incomes in Emerging APAC Economies | +1.2% | India, Vietnam, Indonesia | Medium term (2-4 years) |

| Improving Financial Literacy and Retirement Awareness | +0.5% | Global APAC, particularly emerging markets (India, Indonesia, rural China) | Long term (≥ 4 years) |

| Increasing Life Expectancy and Longevity Risk | +0.7% | Global APAC, spill-over concentration in Hong Kong, Singapore, and mature Northeast Asia | Long term (≥ 4 years) |

| Digitalization of Insurance and Investment Products | +0.7% | APAC core: China, Singapore, South Korea; spill-over to India, Southeast Asia | Short term (≤ 2 years) |

| Regulatory and Government-Led Financial Inclusion Initiatives | +0.8% | India, Indonesia, Vietnam, Thailand; selective gains in China (pension reforms) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Demographic Aging and Retirement Security Demand

Asia is experiencing unprecedented population aging, which is driving a significant shift in demand for retirement and health-linked insurance products. As of 2023, the Asia‑Pacific region has approximately 697 million people aged 60 and over (14.8 % of the total population), including 489 million aged 65+ and 89 million aged 80+. The older population is projected to rise rapidly to 885 million by 2030 and 1.34 billion by 2050, with the 60+ share increasing to 25.9 %. This demographic transformation is fueled by declining fertility rates (1.9 births per woman) and rising life expectancy of 74.9 years, resulting in a growing cohort of longer-living seniors[1]Source: United Nations ESCAP, “Population Data Sheet 2024 – Demographic Indicators for Asia‑Pacific”, population-trends-asiapacific.org. The accelerated aging trend is increasing demand for retirement income solutions, annuities, and health-linked protection, as individuals face longer post-retirement periods and rising pressure on public pension systems. Governments are emphasizing policies that support healthy aging and extended working lives, such as China’s goal to increase average life expectancy to around 80 years by 2030, which aligns with expanding retirement security needs.

Rising Disposable Incomes in Emerging APAC Economies

Rising household incomes across emerging Asia are expanding the pool of first-time buyers and deepening demand for both protection and savings-linked products. In India, the insurance sector has benefited directly from this trend: the market has grown at a ~17 % CAGR over the past two decades and is projected to reach ₹19,30,290 crore (USD 222 billion) by FY26, driven by higher premiums, growing middle-class participation, and rising per capita premium levels, reflecting higher disposable income and affordability [2]Source: India Brand Equity Foundation, “Growth of the Indian Insurance Industry with Market Size & Trends,” IBEF, ibef.org. Nationwide inclusion goals and digital platforms are broadening access, channeling new middle-class purchasing power into formal insurance, while modest penetration relative to population size means that even small increases in awareness and income can translate into significant premium growth. Consumer surveys indicate strong demand for flexible solutions combining life and health features, particularly among younger buyers entering the market who seek bundled benefits rather than single-purpose coverage. Emerging cities and smaller towns are becoming increasingly important sources of new business, as distribution expands beyond metropolitan centers and digital engagement complements traditional advice-led sales.

Digitalization of Insurance and Investment Products

Digital adoption is reshaping how policies are designed, distributed, and serviced across the region. Asia Insurance on 8 Oct 2025 adopted CoverGo’s digital health insurance platform to digitise policy and claims processing, speed product launches, expand digital distribution, and improve customer and partner experience[3]Source: ITIJ, “Asia Insurance adopts CoverGo platform to streamline health insurance services,” ITIJ.com, 8 Oct 2025. Insurers are shortening product cycles and improving underwriting speed as cloud-native platforms and AI automation scale across core processes for the Asia Pacific life annuity insurance market. Reported performance gains include faster product launches, material reductions in case handling times, and higher straight-through processing in underwriting and claims. At the same time, digital claims capabilities, intelligent assistants, and omnichannel service are boosting customer satisfaction while bending the operations cost curve. The resulting speed and convenience are enabling broader access to smaller-ticket policies that suit first-time buyers and micro-savers as embedded coverage becomes more common in daily financial journeys. These technology gains support balanced growth by raising service quality, increasing conversion, and unlocking new pockets of demand in both developed and emerging markets.

Regulatory and Government-Led Financial Inclusion Initiatives

Policy actions around inclusion, taxation, and market access are expanding the addressable base and improving affordability. In India, the removal of GST on individual life and health policies and the approval of 100% foreign direct investment are reinforcing long-term inclusion objectives and catalyzing partnerships to reach semi-urban and rural households. The IAIS promotes financial inclusion by guiding regulators to improve access to affordable, responsible insurance. Initiatives focus on capacity building, inclusive regulations, and digital innovation, supporting broader insurance penetration in the Asia Pacific[4]Source: International Association of Insurance Supervisors (IAIS), “Financial inclusion,” iais.org. This mix of regulatory clarity and national platforms is drawing more capital to the sector and giving insurers a wider set of tools to serve underserved segments at lower cost. As solvency, risk-based frameworks, and customer protection policies advance across the region, insurers are retooling product portfolios and redesigning distribution to align with higher standards. The net effect is a healthier operating environment that rewards transparent pricing, prudent risk management, and data-driven service. The Asia Pacific life annuity insurance market stands to benefit as reforms enhance trust, encourage innovation, and allow scale players to invest for multi-year growth.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low Financial Literacy and Trust Deficits | -0.8% | Rural India, Indonesia, Vietnam, and pockets of rural China | Long term (≥ 4 years) |

| High Cost Perception and Affordability Constraints | -0.6% | Emerging markets (price-sensitive segments); medical inflation pressure in Hong Kong, Singapore | Medium term (2-4 years) |

| Regulatory Complexity and Compliance Burden | -0.4% | Highly regulated markets such as Japan, South Korea, Singapore | Medium term (2–4 years) |

| Limited Product Awareness and Digital Divide | -0.3% | Rural and semi-urban areas across Southeast Asia, smaller towns in China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Low Financial Literacy and Trust Deficits

Awareness gaps and trust barriers slow conversion from interest to purchase in many communities across emerging Asia. Penetration remains modest in large markets where significant shares of the population still rely on informal mechanisms and short planning horizons for financial security. Consumer research indicates a clear preference for bundled life and health propositions rather than pure life policies, which means traditional single-purpose protection products can underperform against customer expectations. The shortfall in long-term planning is visible in protection gap measures that show both mortality and health shortfalls, with a high concentration in emerging markets where advice and guidance are limited. Efforts to close these gaps rely on trusted advice, simple product narratives, and transparent servicing that reinforce confidence at the point of need. The Asia Pacific life annuity insurance market continues to see positive outcomes when consumer education, distribution quality, and product relevance improve together.

High Cost Perception and Affordability Constraints

Perceived affordability remains a core barrier to uptake even as awareness rises. Medical cost inflation runs near 10% in some hubs such as Hong Kong, while headline inflation has remained much lower, which pressures benefit adequacy and premium affordability for health-linked riders in life policies. Protection gap estimates for health indicate a large premium-equivalent shortfall across major Asian markets, with a significant portion of the gap concentrated in emerging economies where out-of-pocket spending is heavy. Several markets are addressing price sensitivity through tax changes and inclusion policies that reduce the all-in cost of purchase and increase product flexibility. Preference continues to shift toward severity-based and staged benefit structures that align payout with need and reduce headline premiums for younger and lower-income buyers. Over time, affordability interventions and product redesign support steadier growth in the Asia Pacific life annuity insurance market by broadening access while improving alignment with household cash flows.

Segment Analysis

By Insurance Type: Carriers Pivot from Savings Endowments to Risk-Focused Annuities

Life insurance commanded a 63.5% share in 2025 and is projected to expand at a 7.82% CAGR through 2031, setting the pace among product categories in the Asia Pacific life annuity insurance market. This momentum reflects a deliberate shift in product mix toward risk-focused offerings with income features that help policyholders manage longevity risk and sequence-of-returns risk in retirement. As populations age, lifetime income options and care-linked features become central to household planning, and customer surveys show a strong tilt toward integrated solutions over standalone protection. Leading carriers are also weaving care and service ecosystems into annuity-linked propositions to support aging at home, faster claims, and personalized service. With retirement security rising as a primary goal for more households, the Asia Pacific life annuity insurance industry is repositioning product architecture around reliable income, transparent guarantees, and service quality that holds up over time.

The depth of the retirement income need is visible in longevity gap indicators, and in the way senior-focused products are now positioned at the center of advisory conversations. Income features that blend guaranteed payouts with measured exposure to growth assets are emphasized in wealth planning for the region’s mass affluent and high-net-worth customers. Product innovation highlights include flexible income start dates, inflation-aware payout options, and healthcare riders that adapt coverage as medical needs evolve with age. Global groups in Asia are building broader platforms to serve decumulation, estate planning, and cross-border financial goals, tying insurance with asset management capabilities. This evolution supports stable growth for the Asia Pacific life annuity insurance market as more households convert savings to sustainable income streams with built-in protection.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Agency Networks Transition to AI-Augmented Hybrid Advisors

Brokers and agents retained a 28.8% share in 2025 and are projected to grow at a 5.67% CAGR through 2031, reflecting the continued relevance of advice-led distribution in the Asia Pacific life annuity insurance market. Agency distribution remains the single largest channel, with intermediary-led models favored for complex needs such as retirement income and estate planning that require tailored guidance. Leading insurers report productivity lifts from targeted recruitment, continuous training, and the integration of AI-based tools that enhance needs analysis, illustration, and service. Performance models now rely more on quality metrics and lifetime value rather than volume, which aligns incentives with customer outcomes and regulatory expectations. This steady upgrade of the advisory channel is central to reaching new buyers and supporting higher-value conversations that match longer-term financial goals.

Banks are deepening their role in life and retirement distribution across Southeast Asia as customers adopt combined wealth and protection conversations. In ASEAN markets, bancassurance premium pools are rising at double-digit rates through the decade, with life products dominating the mix and Thailand holding a significant regional share. New business flows in select bank partnerships have grown sharply, showing that structured wealth and retirement propositions resonate with customers who prefer to transact inside trusted financial relationships. Direct-to-consumer and digital channels are also growing at a healthy clip, aided by embedded journeys and straight-through processing that reduce friction for simpler products. These channel dynamics support broad-based expansion of the Asia Pacific life annuity insurance industry while maintaining focus on advice where complexity and long-horizon decisions demand it.

Geography Analysis

India opened 2026 with a strong policy tailwind, and it holds a 34.2% share in 2025 with a projected 7.86% CAGR to 2031, making it the fastest-growing major geography in the Asia Pacific life annuity insurance market. The national agenda to extend coverage and improve affordability includes the removal of GST on individual life and health policies and the approval of 100% foreign direct investment, which together expand access and catalyze capital formation. Penetration is still low relative to country size, and inclusion efforts now reach deeper into smaller cities and towns where a majority of new premiums have been generated. Distribution partnerships between insurers and financial institutions are scaling to reach new customers, while digital platforms support streamlined onboarding and service. With continued policy support and a large working-age population, India is positioned to contribute a large share of incremental growth in the Asia Pacific life annuity insurance market.

China remains a central pillar for regional growth, supported by its large base, rising longevity, and a policy focus on healthy aging. National targets call for higher life expectancy by 2030 with expanded senior care services, which encourages product designs that blend income, care, and protection benefits. Leading carriers are investing in agency quality upgrades, data-driven service, and bancassurance partnerships to deliver wealth and retirement solutions at scale. Fast claims processing and AI-enabled service are reshaping customer expectations and cost structures, strengthening competitiveness in a market where trust and convenience are decisive. As investors and households prioritize long-term security, participating and income-focused policies gain prominence in household portfolios. The Asia Pacific life annuity insurance market benefits as China advances health and elder-care initiatives that complement private coverage with public programs.

Mature markets like Japan, South Korea, Singapore, and Australia have reoriented toward senior-focused solutions as longevity rises and household planning shifts toward income and legacy needs. Policy dialogues around solvency, risk-based capital, and systemic importance continue to shape product, investment, and distribution strategies for large groups with regional hubs. Insurers are introducing lifetime income features and health-linked riders that match the needs of retirees who want reliable payouts and care support over longer horizons. Banks and advisers in financial centers support complex cases for high-net-worth clients, while digital service and automation improve speed for simpler decisions. This balanced approach sustains steady growth in developed markets and complements higher-volume gains in emerging economies, keeping the Asia Pacific life annuity insurance market on a durable growth path.

Competitive Landscape

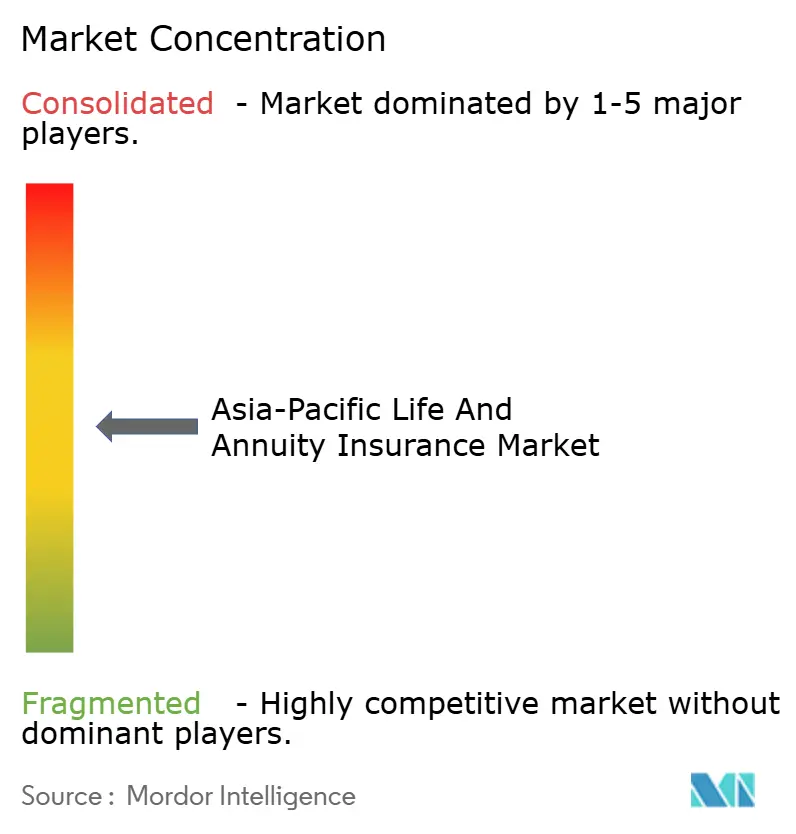

The Asia Pacific life annuity insurance market remains moderately concentrated, with the top five carriers accounting for around half of total premiums. Competitive intensity is increasing as technology becomes a core differentiator in speed-to-market, underwriting efficiency, servicing quality, and claims performance. Insurers are reporting meaningful improvements in product launch timelines, underwriting cycle times, and automation rates across customer service functions. Generative AI and cloud-native platforms are now deployed in production, supporting marketing, sales enablement, and frontline service use cases. As digital capabilities, data, and distribution converge, the advantage increasingly favors players that combine advice-led models with embedded and direct digital journeys.

Market leaders are pursuing a wide range of strategic operating models to strengthen positioning and sustain growth. Integrated ecosystems that connect finance, health, and care are enabling faster decisions and improved post-sale service through AI-enabled workflows. High-performing agency franchises are enhancing productivity through targeted recruitment, advanced training, and digital toolkits that support consultative selling. Bancassurance partnerships continue to scale structured wealth and retirement solutions, with several groups reporting strong new business value growth under revised partnership economics. Cross-border expansion and capability development in asset management, health services, and retirement platforms are widening addressable markets and supporting multi-country operating leverage.

Market structure is further evolving as partnerships and M&A reshape distribution reach, product breadth, and operating scale. In Singapore, a planned majority acquisition of a leading composite insurer is expected to strengthen a global player’s regional footprint, subject to regulatory approvals. In India, inclusion-focused policy reforms are enabling new bancassurance, digital, and reinsurance initiatives in anticipation of sustained long-term growth. Reinsurers and carriers are introducing advanced underwriting and medical assessment solutions to reduce processing times and improve risk selection. Japanese insurers are expanding international platforms and investment capabilities to diversify earnings and strengthen governance, reinforcing the shift toward capital-efficient, technology-enabled, and customer-centric models.

Asia-Pacific Life And Annuity Insurance Industry Leaders

AIA Group

Nippon Life Group

Life Insurance Corporation of India (LIC)

China Life Insurance Group

Muang Thai Life Assurance Group

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2025: India approved an increase in the foreign direct investment limit in insurance companies to 100%, a step expected to accelerate capital inflows and deepen strategic partnerships.

- September 2025: India abolished the 18% GST on individual life and health insurance policies, supporting affordability and near-term sales momentum.

- July 2025: Jio Financial Services Limited and Allianz SE announced a 50:50 reinsurance joint venture in India to serve a fast-expanding protection landscape.

- July 2025: Axis Max Life Insurance launched an all-in-one mobile app for Android and iOS that simplifies policy management and enhances customer experience with features like real-time service tracking, easy premium payments, online policy purchases, AI chatbots, and integrated wellness benefits, including health assessments and fitness tracking.

Asia-Pacific Life And Annuity Insurance Market Report Scope

Life Insurance seeks to provide an individual's family with a lump-sum fiscal payout when that individual dies; annuities act as safety nets by providing individuals with a lifetime of guaranteed income streams.

The Asia-Pacific life and annuity insurance market is segmented by insurance type, distribution channel, and by country. By insurance type, the market is segmented into annuity insurance and life insurance. By distribution channel, the market is segmented into direct, banks, agents, online, and other distribution channels. By geography, the market is further segmented into China, India, Singapore, and the Rest of Asia-Pacific.

The report offers market size and forecasts for the Asia-Pacific life and annuity insurance market in value (USD) for all the above segments.

By Insurance Type

| Life Insurance |

| Annuity Insurance |

By Distribution Channel

| Brokers/Agents |

| Banks |

| Direct Sales |

| Other Channels |

By Country

| China |

| India |

| Japan |

| Singapore |

| Australia |

| Rest of APAC |

| By Insurance Type | Life Insurance |

| Annuity Insurance | |

| By Distribution Channel | Brokers/Agents |

| Banks | |

| Direct Sales | |

| Other Channels | |

| By Country | China |

| India | |

| Japan | |

| Singapore | |

| Australia | |

| Rest of APAC |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size and projected growth of the Asia Pacific life annuity insurance market?

The Asia Pacific life annuity insurance market size reached USD 300.24 billion in 2026 and is projected to reach USD 376.1 billion by 2031 at a 4.61% CAGR.

Which product segment leads and which grows fastest through 2031?

Life insurance led with a 63.5% share in 2025 and is projected to expand at a 7.82% CAGR through 2031, setting the pace among product categories.

Which distribution channel is expected to be the growth leader?

Brokers and agents held a 28.8% share in 2025 and are projected to grow at a 5.67% CAGR, supported by AI-augmented advisory models and productivity gains.

Which geography contributes the most to future growth?

India held a 34.2% share in 2025 and is projected to grow at a 7.86% CAGR through 2031, supported by inclusion policies and capital access.

What are the most impactful growth drivers?

Demographic aging, rising incomes in emerging markets, accelerated digitalization of underwriting and claims, and inclusion-focused policies are the strongest contributors to multi-year expansion.