Market Trends of Asia-Pacific Less-than Container Load (LCL) Industry

Increase in sea freight in the region driving the market

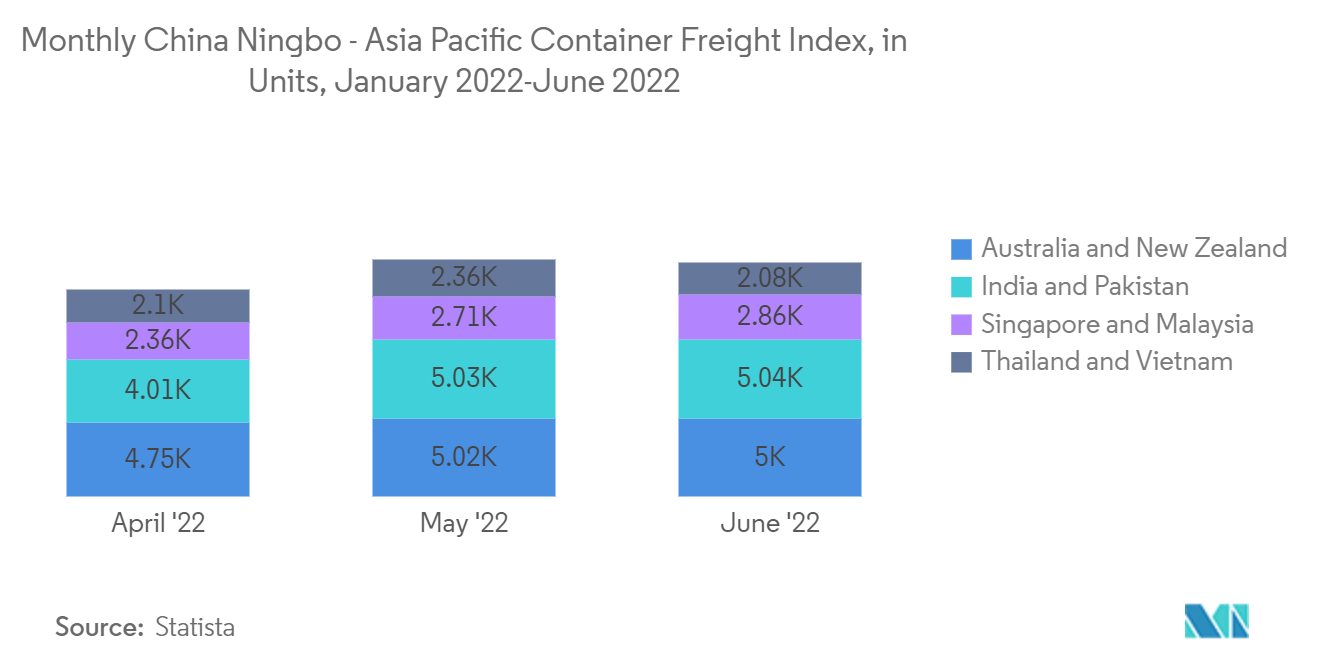

- The current global shipping industry position is complicated, as container rates are declining significantly, with contract rates approaching spot rates. This tendency is visible in other places, such as China and Southeast Asia, where, despite the drop in container rates, demand for shipping remains weak due to global inflation and constrained demand, resulting in a large drop in freight prices. The shipping sector's long-term prospects remain uncertain, as poor consumer demand in North Europe and gradual market recovery in China indicate that the industry will likely continue to struggle. Container rates in key Asian ports such as Ningbo, Shanghai, and Singapore have declined dramatically in the last year, indicating that the current situation may persist in the foreseeable future.

- Container trends are an important indicator of economic success and global trade, and the market picture now appears grim. Container pricing and leasing rates are falling, and the global shipping sector is experiencing a container rate freefall. Blank sailings have not been able to keep prices from falling, and the industry's mid-term view indicates a downturn in container activity on the Asia-EU and Asia-America trade lanes. Contract prices, on the other hand, are closer to spot rates, indicating a lack of demand for long-term commitments due to market uncertainty.

- Intra-Asian trade is exhibiting some resiliency, with comparatively higher container demand. Nonetheless, the mid-term prognosis did not anticipate demand returning to the high levels seen in 2020 and 2021, except for a possible inventory replenishment cycle, which was expected to generate some demand for containers. Falling container rates and rising availability in certain parts of the world indicate poor demand and slower economic growth. In summary, the global shipping sector is in a difficult condition, with container prices falling, demand weakening, and trade routes shifting. While the shipping industry may recover in the future, the current picture is bleak.

Understand The Key Trends Shaping This Market

Download PDF

Increase in intra-continental trade driving the market

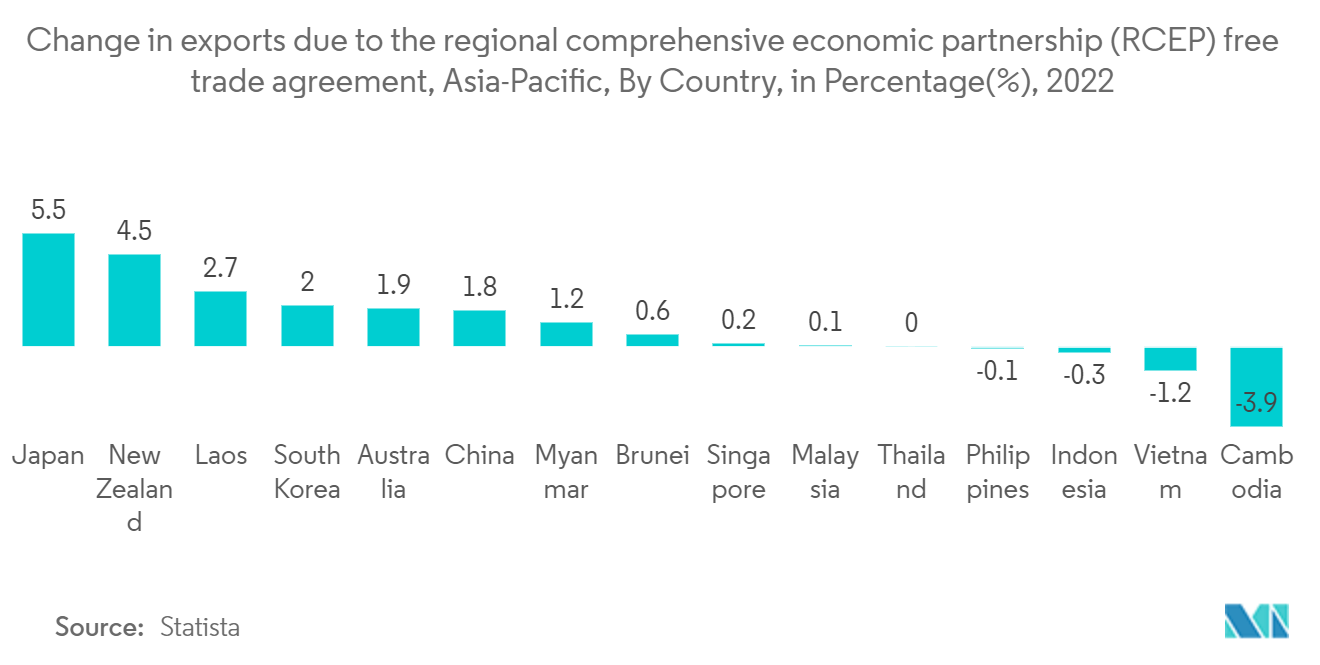

- Policymakers in Asia are correct to be concerned about the potential reconfiguration of global supply chains, given the consequences for the development of their export-oriented and open economies. While there is justification for focusing on prospective alterations on the supply side of the global and regional economic systems, equally drastic shifts on the demand side merit equal attention. There is expanding significance of final demand originating in emerging Asia and drawing policy implications for the region's future trade integration. Trade has been a primary driver of East Asian development, with Korea and Japan achieving high-income status through export-driven development plans.

- Initially, rapid intra-industry trade drove much of East Asia's intra-regional trade integration, which mirrored the development of cross-border global value chains with higher vertical specialization and geographical dispersion of production processes across the region. This resulted in a dramatic increase in intermediate product trade among emerging Asian economies, but the EU, Japan, and the United States remained the primary export customers for finished goods. Consider semiconductors and other computer parts traded from high-wage economies such as Japan, Korea, and Taiwan, China for final assembly to lower-wage economies such as Malaysia and China, and more recently Vietnam, with final products such as TV sets, computers, and cell phones shipped to consumers in the United States, Europe, and Japan.

Get Analysis on Important Geographic Markets

Download PDF