Asia-Pacific Less-than-Container-Load (LCL) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

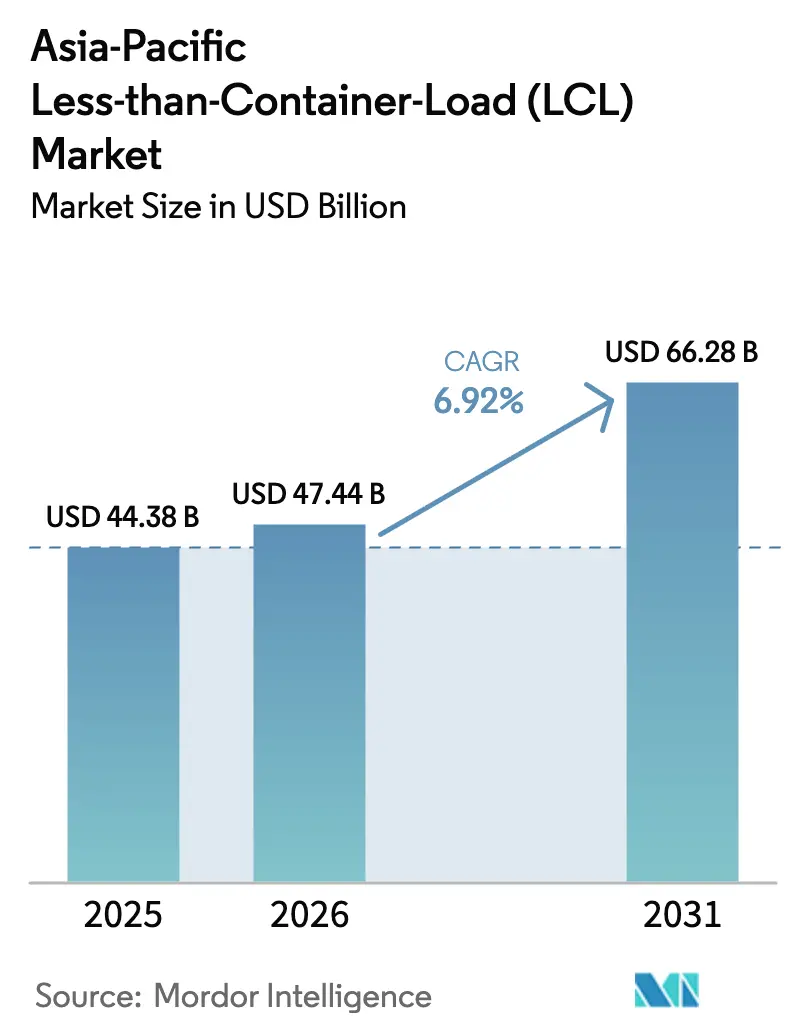

| Base Year Market Size (2025) | USD 44.38 Billion |

| Market Size (2026) | USD 47.44 Billion |

| Market Size (2031) | USD 66.28 Billion |

| Growth Rate (2026 - 2031) | 6.92% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Less-than-Container-Load (LCL) Market Analysis by Mordor Intelligence

The Asia-Pacific Less-than-Container-Load Market size was valued at USD 44.38 billion in 2025 and estimated to grow from USD 47.44 billion in 2026 to reach USD 66.28 billion by 2031, at a CAGR of 6.92% during the forecast period (2026-2031).

The explosive rise of cross-border e-commerce buoys demand, the cost advantage of LCL over air freight for small and medium shippers, and steadily widening regional free-trade frameworks. Consolidation services dominate because cargo aggregation reduces per-unit shipping costs while providing schedule flexibility. Technology adoption—especially real-time booking tools—improves shipment visibility, lowers transaction costs, and encourages first-time users to shift from air to ocean. Manufacturing diversification beyond China continues to redraw trade corridors and spur new LCL gateways in India, Vietnam, and Indonesia as companies pursue supply-chain resilience. Volatile ocean freight rates and recurring port congestion remain key risks, but infrastructure upgrades and regional trade pacts counterbalance these headwinds.

Key Report Takeaways

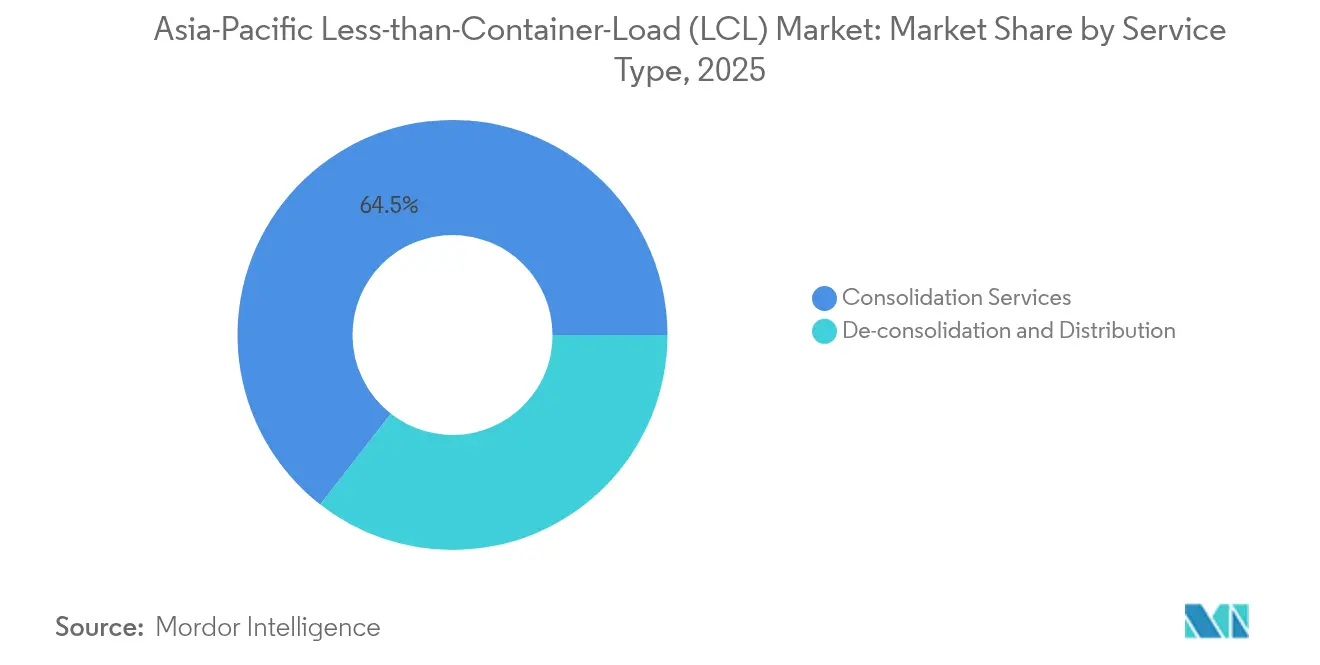

- By service type, consolidation services held 64.45% of the Asia-Pacific Less-than-Container-Load market share in 2025, whereas de-consolidation and distribution are expected to post a 4.21% CAGR from 2026 to 2031

- By destination, international routes generated 60.40% of 2025 volume, while domestic services are forecast to register a 4.66% CAGR to 2031. Meanwhile, domestic routes are projected to grow at a faster 4.66% CAGR through 2031.

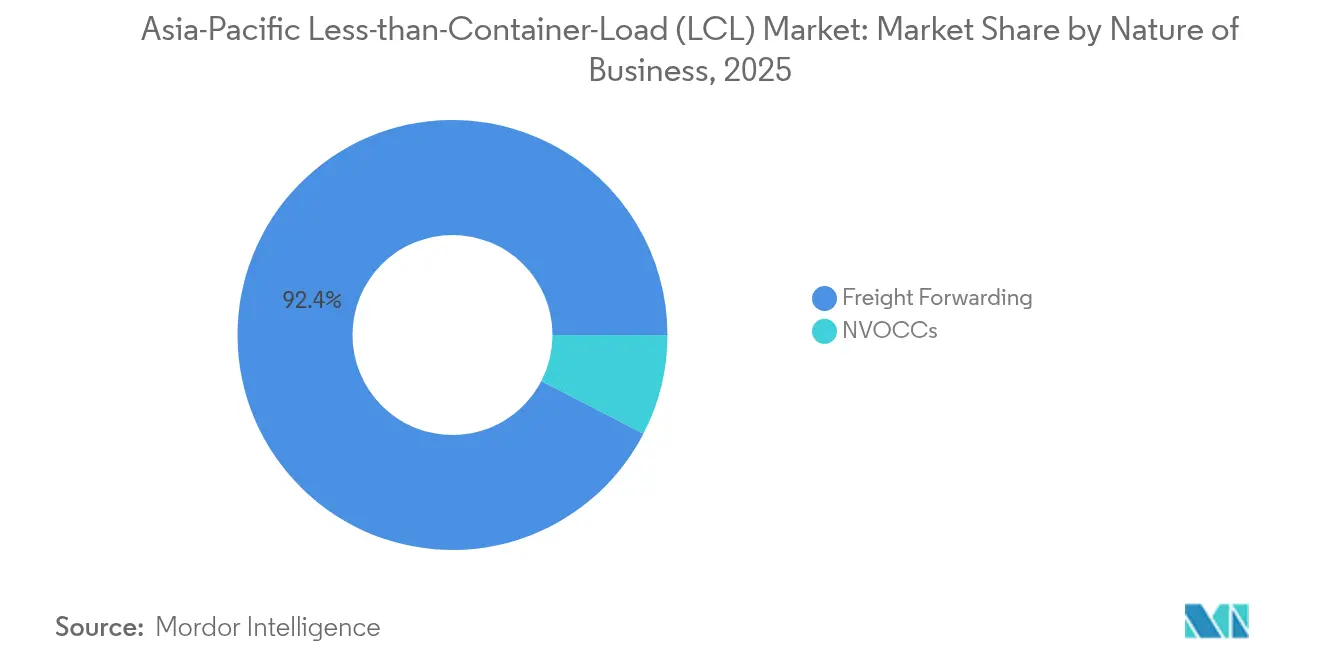

- By nature of business, freight forwarding accounted for 92.40% share of the Asia-Pacific Less-than-Container-Load market size in 2025; NVOCCs pushing their CAGR to 5.32% through 2031.

- By end user, retail & e-commerce held 35.25% of the 2025 volume. Yet, healthcare & pharmaceuticals are projected to grow at a 6.05% CAGR through 2031.

- By country, China retained 39.60% of 2025 regional value, but India is set to record the fastest expansion at a 5.12% CAGR until 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Less-than-Container-Load (LCL) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce boom & cross-border parcel trade | +2.1% | China, India, Southeast Asia | Medium term (2-4 years) |

| Supply-chain diversification of Asia-Pacific manufacturing | +1.8% | China, India, Vietnam, Indonesia | Long term (≥ 4 years) |

| Cost-efficiency of LCL over air freight for SMEs | +1.3% | Southeast Asia, emerging markets | Short term (≤ 2 years) |

| Port infrastructure expansion & FTAs | +1.0% | India, Vietnam, Indonesia | Long term (≥ 4 years) |

| Digital freight platforms with LCL spot rates | +0.9% | Singapore, Hong Kong, regional hubs | Medium term (2-4 years) |

| Green-shipping initiatives and load optimisation | +0.6% | Developed Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-commerce boom & cross-border parcel trade

Retail e-commerce sales in Southeast Asia are expected to hit USD 193 billion by 2028, equal to 17.4% of total retail spend[1]Staff Reporters, “E-commerce Sales in APAC to Hit $3.2 Trillion by 2028,” CampaignAsia.com. Rising online orders require smaller, more frequent shipments that suit LCL economics. The Philippines and Vietnam each anticipate online-retail CAGRs above 20%, creating constant demand spikes that traditional full-container contracts cannot match. RCEP customs simplification lowers transaction costs, speeding up small-batch clearances and pushing merchants toward regional inventory hubs. Omnichannel models mean inventory must be replenished across multiple markets simultaneously, reinforcing LCL’s role in synchronized stock flows. As marketplaces promote same-week delivery promises, shippers prioritize flexible sailings over absolute rate minimization.

Supply-chain diversification of Asia-Pacific manufacturing

Foreign direct investment began shifting toward Southeast Asia during 2024 as firms executed “China + 1” strategies. Smaller production footprints scattered across India, Vietnam, and Indonesia require multi-origin pick-ups for final assembly or direct export, thereby elevating LCL volumes. Japanese electronics groups moved auxiliary lines to Thailand and the Philippines, contracting specialist consolidators to synchronize outbound flows. The region needs an additional USD 60 billion in logistics assets to handle this dispersed output, further magnifying consolidation demand. Heightened geopolitical tension accelerates relocation timelines, making agile LCL nodes attractive stopgaps while multi-country plants scale. As buyers diversify suppliers, consolidation centers emerge in secondary ports, shortening inland haulage and improving turnaround.

Cost-efficiency of LCL over air freight for SMEs

A 2025 C.H. Robinson poll shows 75% of LCL users plan to increase reliance on ocean consolidation because it cuts freight spend by up to 80% versus air on non-urgent lanes[2]Greg Scott, “The Role of LCL Shipping in the Post-Pandemic World,” SupplyChainBrain.com. Carriers report on-time performance exceeding 90% on redesigned East–West loops, narrowing perceived service gaps with air. Digital booking portals slash paperwork and allow instant comparison between LCL and air quotes, making mode shift straightforward for resource-constrained exporters. Air-cargo rates have risen due to persistent capacity constraints, widening the savings window in favor of LCL. SMEs leverage LCL to hold lower inventory without committing to full containers, improving working-capital cycles.

Digital freight platforms offering LCL spot rates

Ninety-nine percent of Ocean Network Express bookings now flow through digital channels. Real-time visibility, spot pricing, and automated documentation democratize access for first-time exporters. Indonesia’s National Logistics Ecosystem spans 264 ports and 6 airports, linking customs, shipping lines, and truckers on one interface and reducing average clearance times by 17%. AI-driven load-combining engines match shipments by size, haz-clas,s and temperature, minimizing empty slots and raising vessel utilization. Blockchain pilots trim days from bill-of-lading issuance while cutting fraud risk. Digitalization also streamlines payment processing, reassuring credit-sensitive SME shippers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Port congestion & capacity constraints | -1.4% | Singapore, Shanghai, regional trans-shipment hubs | Short term (≤ 2 years) |

| Volatility in ocean-freight rates | -0.8% | Asia-US, Asia-Europe corridors | Medium term (2-4 years) |

| Limited cold-chain LCL infrastructure | -0.5% | Pharmaceutical and food lanes | Medium term (2-4 years) |

| Emerging ESG compliance burdens | -0.3% | Developed Asia-Pacific economies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Port congestion & capacity constraints

Singapore and Colombo experienced extended vessel waits after Red Sea diversions in early 2025[3]Keri Allan, “How to Solve Growing Port Congestion,” ship.nridigital.com. Berth shortages ripple into feeder schedules, delaying container de-stuffing deadlines that underpin LCL cut-off times. Feeder operators imposed congestion surcharges that directly lift LCL unit costs. Labor shortages and limited night-gate hours further restrict throughput, especially for temperature-sensitive cargo needing priority handling. Automation projects promise capacity relief, but near-term mismatches between container arrivals and yard slots will continue disrupting LCL consolidation windows. Stakeholders advocate for better berth-allocation algorithms and data-sharing to smooth peaks.

Volatility in ocean-freight rates

Asia–US West Coast spot prices fell 26.57% in February 2025 alone[4]Peter Stallion, “FBX Index March 2025: Volatility Hits Container Spot Rates,” balticexchange.com. Carriers responded with blank sailings, withdrawing 75,700 TEU in one month, which destabilized sailing schedules relied on by consolidators. Some forwarders introduced variable-fuel surcharges and two-tier contracts that pass through extraordinary rate changes, complicating budgeting for SMEs. Potential U.S. import tariffs on Chinese-built vessels would add up to USD 1.5 million per ship, creating incremental cost pressure. Dissolution of mega-alliances raises uncertainty over long-term capacity, fuelling sharper price swings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Consolidation Leads Efficient Routing

Consolidation services commanded 64.45% of 2025 revenue. Their dominance stems from the Asia-Pacific Less-than-Container-Load market economics in which cargo aggregation into shared containers drives lower per-unit costs and faster sailing frequency. Maersk’s Shanghai gateway with more than 200 direct lanes evidences the scale required to sustain daily consolidations. De-consolidation and distribution, though smaller, post a 4.21% CAGR to 2031 as retailers seek destination-side break-bulk for rapid e-commerce fulfillment. Integrated providers bundle in-country distribution with upstream consolidation to secure door-to-door contracts.

Demand for consolidation services rises with each additional omnichannel stock-point merchant set up across Asia. The Asia-Pacific Less-than-Container-Load market responds by opening new hub-and-spoke facilities in Penang, Cebu, and Surabaya. De-consolidation growth also mirrors the adoption of bonded e-commerce warehouses, where shipment splitting, labeling, and returns handling occur inside free-trade zones. Value-added distribution tasks, such as kitting or light assembly, allow consolidators to move up the service ladder, capturing higher margins.

By Destination: International Dominance with Domestic Momentum

International shipments generated 60.40% of the 2025 value, illustrating the export-oriented nature of many Asian production centers. The Asia-Pacific Less-than-Container-Load market size tied to overseas routes remains anchored by North American and European consumption cycles. Nevertheless, domestic LCL lanes are expected to post a faster 4.66% CAGR (2026-2031) as intra-Asia sourcing spreads. RCEP’s common rule of origin is forecast to add USD 90 billion to regional trade and feed domestic consolidation flows.

Domestic LCL expansion pairs with rising middle-class demand for imported components assembled locally. This trend supports multi-country production chains in electronics and automotive, triggering back-and-forth movements of semi-finished goods. Consolidators refine trucking alliances for first-mile pick-ups to ensure container stuffing deadlines remain intact when origin points multiply. Forwarders also renegotiate depot leases in land-constrained metro areas to shorten drayage.

By Nature of Business: Freight Forwarders Retain Command

Freight forwarders handled 92.40% of 2025 volume, underscoring the relationship-based complexity of Asia-Pacific trade lanes. The Asia-Pacific Less-than-Container-Load market depends on forwarders to interpret diverse customs rules, arrange multimodal combinations, and secure cargo insurance. Digitalization allows some NVOCCs to win share, pushing their CAGR to 5.32% through 2031, but forwarders continue to scale technology investments to defend their turf.

Global forwarders court SME exporters through self-service portals while still providing human expertise for escalations. Meanwhile, several NVOCCs adopt dynamic routing algorithms that bypass congested hubs. Competitive pressure pushes both models to integrate carbon-reporting dashboards, a growing tender requirement. As importers demand landed-cost visibility, forwarders expand duty-and-tax advisory, reinforcing their value proposition beyond line-haul execution.

By End User: Healthcare Logistics Accelerates

Retail & e-commerce generated 35.25% of 2025 spend as online orders proliferated. Yet healthcare & pharmaceuticals now hold the fastest lane, with a 6.05% CAGR (2026-2031) supported by DHL’s EUR 500 million (USD 520 million) regional cold-chain expansion. The Asia-Pacific Less-than-Container-Load market share of temperature-controlled lanes will climb as biotech manufacturing clusters emerge in South Korea, Singapore, and India. Manufacturing and automotive continue to rely on LCL for components with short lead-time tolerances.

Pharma shippers demand GDP-certified hubs, real-time temperature telemetry, and validated packaging. Consolidators respond by adding reefer consolidation cells and training staff in cold-chain SOPs. E-commerce returns create new backhaul loads, improving container utilization. Agriculture and forestry rely on LCL to move specialty inputs such as fertilizer additives or seedlings to island economies, keeping niche volumes steady.

Geography Analysis

China held 39.60% of the 2025 value, leveraging extensive port infrastructure and digital freight ecosystems. The Asia-Pacific Less-than-Container-Load market continues to treat Shanghai, Ningbo, and Shenzhen as primary load centers. Rising labor costs and compliance scrutiny prompt some exporters to shift heavy, labor-intensive processing elsewhere, but high-tech manufacturing persists, sustaining outbound consolidation demand. Investment in smart-port automation raises throughput efficiency, partially offsetting congestion spikes.

India is expected to record the highest expansion at a 5.12% CAGR (2026-2031). The National Logistics Policy aims to trim logistics cost-to-GDP from 14% to 8%, supporting corridor developments such as the Dedicated Freight Corridor and inland multimodal parks. Unified Logistics Interface Platform digitizes documentation, reducing clearance times. Inland container depots near Jaipur and Indore enable hinterland SMEs to access LCL gateways without long drays to coastal ports, broadening market reach.

Competitive Landscape

The Asia-Pacific Less-than-Container-Load market exhibits moderate fragmentation. ECU Worldwide, Shipco, Vanguard Logistics, and Rhenus Logistics dominate pure consolidation, each operating proprietary CFS (container freight station) networks in more than 15 regional ports. Integrated giants—DHL Global Forwarding, Kuehne + Nagel, and DSV—leverage end-to-end offerings, coupling LCL with air charter and contract logistics. The top five players control roughly 32% of total throughput, leaving ample share for regional specialists.

Technology adoption shapes competitive edges. Ocean Network Express attains 99% digital booking penetration, shortening booking windows from two days to two hours. Maersk embeds predictive ETAs into its Shanghai gateway, giving customers auto-alerts on cut-off shifts. Vanguard pilots blockchain bills of lading on Hong Kong–Los Angeles lanes, trimming documentation time by 38%. Sustainability also differentiates providers: ITOCHU pledges net-zero by 2040 and tests bio-fuel blends on intra-Asia shuttles.

Mergers and partnerships accelerate scale. DSV’s EUR 14.3 billion (USD 14.9 billion) takeover of Schenker doubles its global footprint, adding crucial Asian CFS assets and nearly 160,000 staff across 90 countries. Asian carriers Sinotrans and TS Lines launch a Mexico service, widening LCL routing choices and intensifying margin competition on trans-Pacific lanes. White-space remains in pharma-grade and high-value electronics consolidation where qualified CFS capacity is undersupplied, offering room for niche entrants.

Asia-Pacific Less-than-Container-Load (LCL) Industry Leaders

ECU Worldwide (Part of All Cargo Logistics)

Shipco

Vanguard Logistics

Rhenus Logistics

Kuehne + Nagel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DHL Group announced a EUR 500 million (USD 520 million) spend in Asia Pacific for life-sciences logistics expansion, adding GDP-certified hubs and reefer capacity.

- April 2025: DSV completed the EUR 14.3 billion (USD 14.9 billion) acquisition of Schenker, targeting DKK 9 billion (USD 1.3 billion) in annual savings by 2028.

- March 2025: Sinotrans Container Lines and TS Lines introduced an Asia–Mexico service starting April 2025 in response to USD 90 billion of Chinese exports to Mexico in 2024.

- February 2024: Maersk named Shanghai its global LCL gateway, opening 200+ direct routes and deepening consolidation capacity.

Asia-Pacific Less-than-Container-Load (LCL) Market Report Scope

LCL stands for less than the container load. It refers to circumstances in which the cargo has modest volumes or dimensions that do not require the complete volume of a container. The shipper can choose LCL, which combines their shipment with other smaller cargoes in this example. A consolidated container is one in which numerous smaller goods are merged to be shipped in the same container. A complete background analysis of the Asia-Pacific Less-than-Container Load (LCL) Market, including the assessment of the economy and contribution of sectors in the economy, a market overview, market size estimation for key segments, emerging trends in the market segments, market dynamics and geographical trends, and COVID-19 impact, is covered in the report.

The Asia-Pacific less-than container load (LCL) market is segmented by destination (domestic and international), end-user (manufacturing, retail (including e-commerce), healthcare and pharmaceuticals, agriculture, and other end-users), and country (Australia, China, India, Indonesia, Japan, Malaysia, Thailand, Vietnam, and other Asia-Pacific countries).

The report offers market size and forecast values (USD) for all the above segments.

| Consolidation Services |

| De-consolidation & Distribution |

| Domestic |

| International |

| Freight Forwarding |

| NVOCCs |

| Manufacturing and Automotive |

| Retail & E-commerce |

| Healthcare & Pharmaceuticals |

| Agriculture & Forestry |

| Other End Users |

| China |

| India |

| Indonesia |

| Japan |

| Malaysia |

| Thailand |

| Vietnam |

| Australia |

| Rest of Asia-Pacific |

| By Service Type | Consolidation Services |

| De-consolidation & Distribution | |

| By Destination | Domestic |

| International | |

| By Nature of Business | Freight Forwarding |

| NVOCCs | |

| By End User | Manufacturing and Automotive |

| Retail & E-commerce | |

| Healthcare & Pharmaceuticals | |

| Agriculture & Forestry | |

| Other End Users | |

| By Country | China |

| India | |

| Indonesia | |

| Japan | |

| Malaysia | |

| Thailand | |

| Vietnam | |

| Australia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the 2026 value of the Asia-Pacific Less-than-Container-Load market?

It is USD 47.44 billion.

How fast is regional LCL demand expected to grow through 2031?

The forecast compound annual growth rate is 6.92%.

Which service type currently dominates regional revenue?

Consolidation services command 64.45% of 2025 value.

Which end-user segment is growing the quickest?

Healthcare & pharmaceuticals is projected to expand at a 6.05% CAGR to 2031.

Why are SMEs shifting shipments from air to LCL?

LCL can cut freight costs by up to 80% on non-urgent routes while maintaining satisfactory transit times.

Page last updated on: