Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

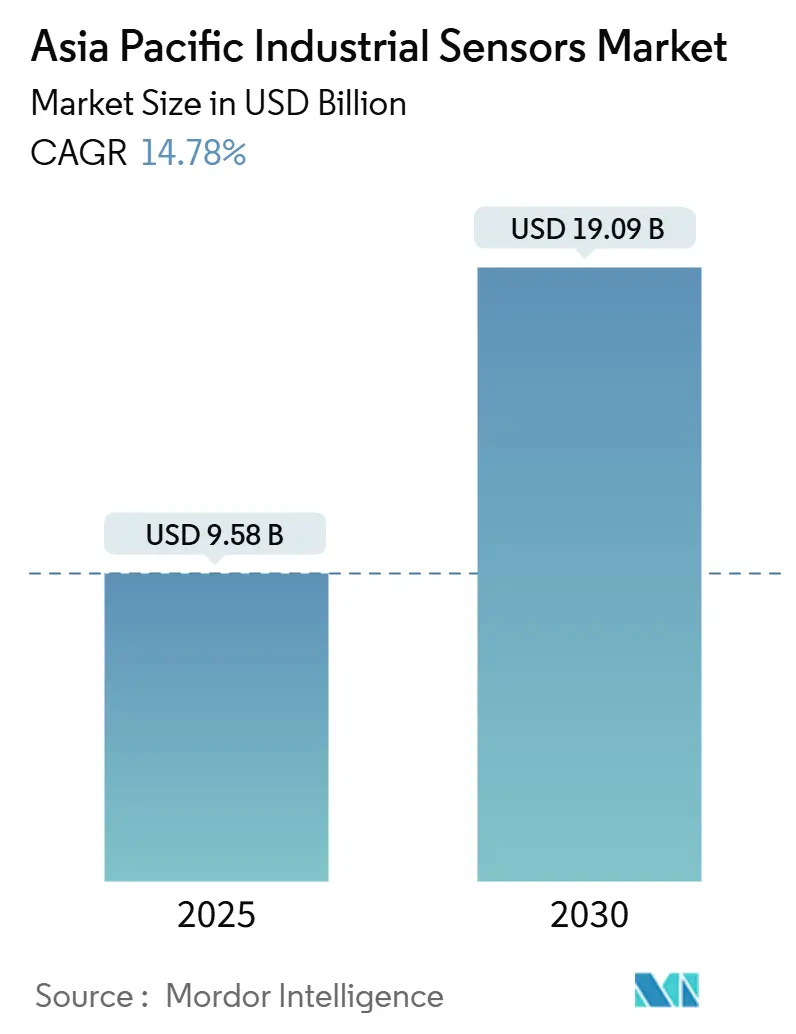

| Market Size (2025) | USD 9.58 Billion |

| Market Size (2030) | USD 19.09 Billion |

| Growth Rate (2025 - 2030) | 14.78% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Industrial Sensors Market Analysis by Mordor Intelligence

The Asia-Pacific industrial sensors market size is valued at USD 9.58 billion in 2025 and is forecast to reach USD 19.09 billion by 2030, advancing at a 14.78% CAGR. Intensifying digital factory programs, aggressive automation in electronics and automotive corridors, and expanding private 5G coverage are the pivotal forces driving sensor deployment across the region. China’s 94% industrial-AI adoption rate underscores how sensor density now dictates competitive throughput, while India’s Production Linked Incentive scheme is translating fiscal subsidies into large purchase orders for pressure, temperature, and vision sensors. IO-Link standardization and edge-configurable devices are lowering commissioning times, shifting total-cost-of-ownership equations in favor of mid-sized manufacturers. At the same time, spectrum liberalization for private 5G in markets such as Thailand and Malaysia is removing latency barriers that once confined wireless sensors to non-critical loops.[1]Ericsson, “Private 5G for Industrial Applications,” ericsson.com These trends collectively accelerate retrofit activity across brownfield sites and seed fresh demand in new greenfield lines.

Key Report Takeaways

- By product type, pressure sensors led with a 34.74% share of the Asia-Pacific industrial sensors market in 2024 and are projected to expand at a 15.11% CAGR through 2030.

- By end-user industry, automotive held 26.62% of the Asia-Pacific industrial sensors market size in 2024, whereas pharmaceuticals and life sciences are set to grow at a 14.99% CAGR through 2030.

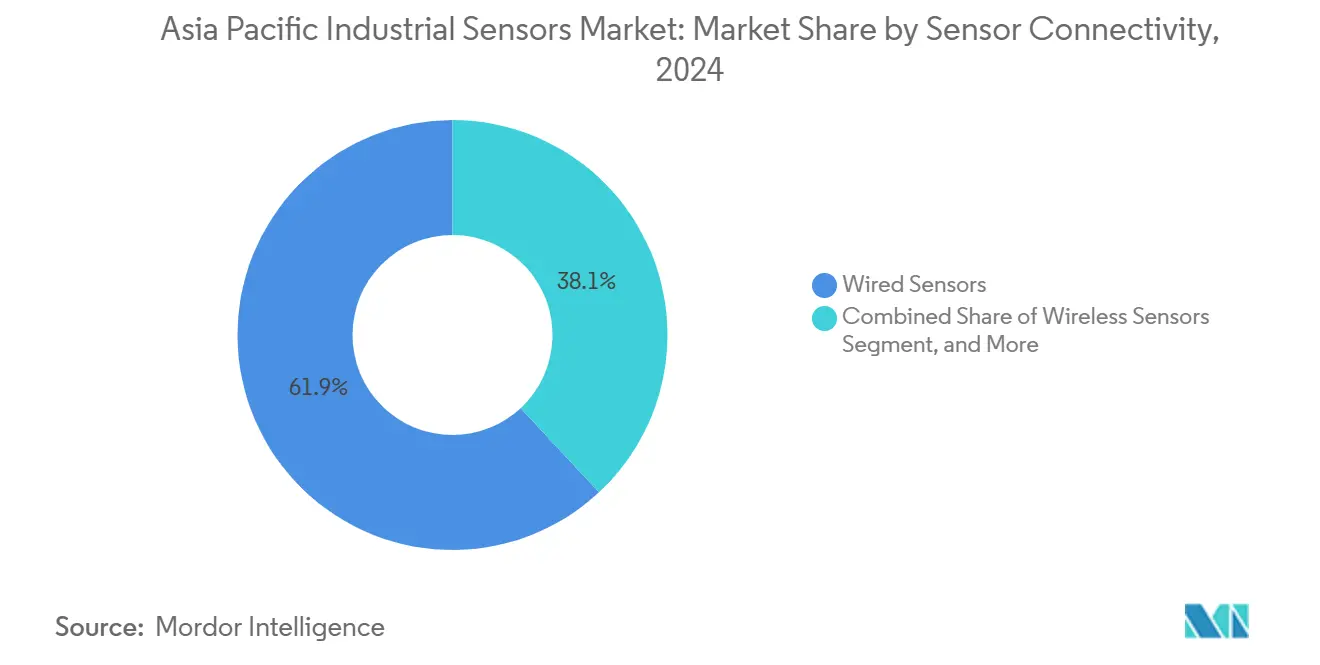

- By sensor connectivity, wired devices accounted for 61.93% of market revenue in 2024 of Asia-Pacific industrial sensors market, but wireless sensors are forecast to register the fastest 15.89% CAGR over the outlook period.

- By sensing technology, MEMS devices captured 42.74% share in 2024 of Asia-Pacific industrial sensors market, yet optical sensors are on track to post a 15.55% CAGR to 2030.

- By country, China captured a 39.28% share of the Asia-Pacific industrial sensors market in 2024. India is projected to record the fastest growth rate at a 15.66% CAGR through 2030.

Asia-Pacific Industrial Sensors Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IIoT and Industry 4.0 penetration | +2.8% | China, Japan, South Korea, with spillover to India and Southeast Asia | Medium term (2-4 years) |

| Rapid automation across Asia-Pacific manufacturing | +2.5% | China, India, Vietnam, Thailand, Indonesia | Short term (≤ 2 years) |

| Government incentives for smart factories | +1.9% | India (PLI), China (Made in China 2025), Japan (Society 5.0) | Medium term (2-4 years) |

| Demand for predictive maintenance solutions | +2.1% | Japan, South Korea, Australia, with adoption spreading to India | Long term (≥ 4 years) |

| IO-Link and edge-configurable sensors adoption | +1.7% | Global, with early traction in Japan and South Korea | Medium term (2-4 years) |

| Private 5G industrial campus roll-outs | +1.6% | China, Thailand, Malaysia, Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

IIoT And Industry 4.0 Penetration

Manufacturers are migrating from point-level automation to fully connected operations where every asset streams time-series data to on-premise or cloud analytics platforms. China’s 94% industrial-AI adoption in 2024 validates the scale of this shift, with sensors underpinning yield optimization in semiconductor fabs and energy management routines in chemical plants. Japan’s Society 5.0 program accelerates adoption in aging-workforce scenarios, as collaborative robots rely on force and proximity sensors to ensure operator safety. South Korea aims to establish 30,000 smart factories by 2025, effectively repositioning sensors from optional hardware to a compliance necessity. Open-protocol devices are proliferating as buyers seek interoperability, fragmenting brand loyalty but enlarging the total hardware pool. Premium vendors now bundle analytics subscriptions with hardware, transforming one-off sensor sales into recurring revenue.

Rapid Automation Across Asia-Pacific Manufacturing

Rising labor costs and the reshoring of supply chains push producers to automate every repetitive task. India’s PLI scheme is expected to generate USD 130.8 billion in additional factory output by 2024 and spur new orders for temperature, pressure, and optical sensors in greenfield electronics and automotive plants. Vietnam’s USD 100 billion electronics output relies on optical sensors for surface-mount accuracy, replacing them every three to five years as component miniaturization tightens tolerances. Thailand’s retrofit of hybrid-vehicle lines demands higher-precision pressure and flow devices, while Indonesia’s food processors are shifting from manual checks to machine-vision quality control. As throughput targets climb, sensor refresh cycles shorten, lifting annual replacement revenue.

Government Incentives For Smart Factories

Fiscal programs are lowering the entry barrier for automation. India refunds 4%–6% of incremental sales, letting manufacturers amortize sensor investments against subsidies. China allocates provincial grants to domestic sensor manufacturers under the Made in China 2025 initiative, strategically reducing import reliance in pressure and flow categories. Japan’s tax credits for ISO 50001 energy-management certification boost demand for energy-monitoring sensors that detect compressed-air leaks. South Korea co-funds 50% of sensor-rich upgrades for SMEs, compressing payback periods to within two years. Such incentives create a self-reinforcing loop: subsidies increase sensor density, which in turn justifies further digital spending.

Demand For Predictive Maintenance Solutions

Rising downtime penalties prompt operators to adopt condition-based strategies. Yokogawa reports that coupling wireless vibration sensors with analytics cuts false alarms by 60%, addressing earlier skepticism over alert quality.[2]Yokogawa Electric Corporation, “Industrial Automation Solutions,” yokogawa.com Australia’s miners mandate sensor monitoring on conveyors because a single failure can idle USD 2 billion operations. South Korea’s chip fabs utilize gas sensors to monitor chamber contamination, thereby preventing scrap worth millions of dollars. As device prices fall and cloud algorithms commoditize, barriers to pilot projects recede, extending uptake into mid-tier plants. The economic case strengthens further when energy savings from optimized runtimes are taken into account.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost and ROI uncertainty | -1.4% | India, Southeast Asia, SME-heavy markets | Short term (≤ 2 years) |

| Legacy-system integration complexity | -1.2% | Japan, South Korea, mature industrial bases | Medium term (2-4 years) |

| Chip-supply volatility for MEMS devices | -0.9% | Global, with acute impact on automotive and consumer electronics | Short term (≤ 2 years) |

| Spectrum regulations limiting industrial wireless | -0.8% | India, Indonesia, fragmented regulatory environments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost And ROI Uncertainty

SMEs often lack the working capital to absorb 12- to 18-month payback periods typical of predictive-maintenance pilots. Indian family-owned mills with annual revenue below USD 10 million prefer machinery that lifts output immediately over sensors offering indirect gains. Slim margins at Southeast Asian auto-component plants demand ROI in under 24 months, whereas wireless deployments may take up to 36 months when integration and learning curves are counted. Leasing models that could spread payments remain scarce, prolonging the investment hurdle. The result is a widening digital gap between cash-rich corporations and resource-constrained suppliers.

Legacy-System Integration Complexity

Brownfield sites laden with 1980s PLCs struggle to ingest data from Ethernet-based sensors. Japan’s chemical complexes using proprietary bus protocols face multimillion-dollar rip-and-replace costs or risk data silos that blunt digital strategies. South Korean steel furnaces cannot accept downtime necessary for rewiring, yet wireless alternatives operate below the 1,200 °C thresholds required. Skill shortages compound the issue; a single engineer fluent in both legacy code and modern IoT can be booked for nine months. Vendors offering plug-and-play bridges gain disproportionate traction in these accounts.

Segment Analysis

By Product Type: Pressure Dominance Meets Wireless Disruption

Pressure sensors commanded 34.74% Asia-Pacific industrial sensors market share in 2024, reflecting their indispensability in process control, hydraulics, and vehicle safety systems. Projections show a strong 15.11% CAGR growth through 2030, driven by private 5G's ability to eliminate latency issues in compressor optimization and steam-distribution loops. Temperature sensors remain the next-largest category, underpinned by semiconductor fabs' pursuit of sub-0.1 °C stability and biologics' requirement for cold-chain integrity below 8 °C. Level-measurement growth is driven by municipal water upgrades replacing corroding mechanical floats with radar units that perform effectively in high-solids effluent. Flow sensors are shifting toward mass-flow technology in custody-transfer transactions, where volumetric variance previously led to inflated billing disputes.

Across the remainder of the portfolio, gas sensors are expanding into indoor-air monitoring for sterile spaces, vibration devices are standard equipment in predictive-maintenance kits, and optical sensors are crucial for label placement accuracy exceeding 300 units per minute. Magnetic-field sensors fulfill niche roles in EV powertrain alignment and current sensing. With each incremental production upgrade, buyers accent hybrid stacks, combining pressure, temperature, and optical sensing, to gain multidimensional visibility, intensifying cross-selling opportunities for multi-product vendors.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User Industry: Automotive Maturity Versus Pharmaceutical Acceleration

Automotive lines accounted for 26.62% of the Asia-Pacific industrial sensors market size in 2024, driven by the embedding of over 100 temperature and voltage nodes per unit in EV battery packs and the integration of radar, lidar, and ultrasonic devices in ADAS suites. In contrast, the pharmaceutical and life sciences segment is on track for a 14.99% CAGR through 2030, as regulators tighten mandates for continuous environmental monitoring within sterile zones.[3]U.S. FDA, “Current Good Manufacturing Practice (CGMP) Regulations,” fda.gov Electronics manufacturing ranks third, as chipfabs often exceed 50,000 installed sensors per site to sustain nanometer-class process stability. Chemical and petrochemical complexes rely on pressure and flow sensing to prevent runaway reactions, while power producers utilize vibration monitoring to maximize the uptime of wind turbine gearboxes and solar inverter strings.

Oil-and-gas operators favor wireless builds on offshore platforms where cabling exceeds USD 1,000 per meter. Food processors are pushing for stainless-steel IP69K sensors that can withstand high-pressure washdowns, resulting in three- to five-year replacement cycles. Water utilities adopt radar level gauges and pH probes to comply with increasingly stringent discharge limits, whereas mining sites rely on proximity and gas sensors to prevent costly evacuations. Aerospace and defense remain specialty niches demanding radiation-hardened, wide-temperature-range devices that command premium pricing.

By Sensor Connectivity: Wired Incumbency Challenged By Wireless Economics

Wired devices maintained 61.93% share in 2024 because brownfield plants see limited ROI in replacing functional 4-20 mA loops. However, wireless nodes will clock a 15.89% CAGR as private 5G meets deterministic performance thresholds once exclusive to wired protocols. IO-Link bridges both worlds, using standard three-wire cables while enabling digital communication and slashing commissioning time by 40%. Edge-smart sensors reduce bandwidth by sending only anomaly alerts, mitigating congestion in offshore and mining operations where satellite backhauls are expensive.

The economic calculus is tilting toward wireless because installation labor on wired retrofits can be three to five times the hardware cost. Energy-harvesting innovations, piezo, thermo, and photoelectric, extend battery-free lifespans past a decade. Hybrid architectures prevail: critical control loops stay wired, while auxiliary monitoring migrates to wireless. Varying national spectrum policies still introduce deployment friction, but incremental harmonization is underway as regulators appreciate the productivity dividends.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Sensing Technology: MEMS Maturity Meets Optical Innovation

MEMS captured 42.74% Asia-Pacific industrial sensors market share in 2024, buoyed by decades of process refinement for pressure, acceleration, and gyroscope functions. Optical sensors are projected to post a 15.55% CAGR to 2030 as fiber-optic devices prove their worth in high-EMI and explosive zones where electronics are prohibited. CMOS image sensors deliver megapixel resolutions to machine vision, enabling defect detection at line speeds previously impossible with analog predecessors. Piezoresistive stacks dominate ultra-high-pressure hydraulic applications, while capacitive designs excel at liquid-level tasks that are confounded by rare-earth particulates optically.

Hybrid devices are emerging, for instance, six-axis MEMS inertial units for autonomous mobile robots, dual-mode temperature-humidity chips for HVAC, and integrated pressure-temperature modules for precise coolant control in EV manufacturing. Supply-chain resilience now influences technology selection; buyers favor vendors with multisite fabs to avoid repeat shortages. Functional-safety and quality-management certifications are increasingly influential during procurement, as end-users prioritize compliance to streamline audits.

Geography Analysis

In 2024, China secured a dominant 39.28% share of the Asia-Pacific industrial sensors market, underpinned by the Made in China 2025 initiative, which redirects spending toward domestic suppliers. A 94% industrial-AI adoption rate means sensor-fed data already drives yield and energy decisions across automotive, electronics, and chemical factories. Large-scale private 5G sites, such as Midea’s 200,000 m² plant, underscore the country’s readiness to operate closed-loop robotic control over wireless networks. Brownfield upgrades characterize Japan’s market, while predictive-maintenance sensors offset labor shortages in plants that are on average 25 years old. Meanwhile, Society 5.0 policies mainstream cyber-physical integration. South Korea’s Smart Factory Initiative reclassifies sensors as compliance expenditures, thereby fast-tracking their adoption in the automotive and semiconductor sectors.

India emerges as the fastest-growing market through 2030, for instance, PLI incentives worth INR 10.9 lakh crore have translated into factory builds across Gujarat, Tamil Nadu, and Uttar Pradesh, which embed sensors from the ground up. Southeast Asia’s growth stems from Vietnam’s USD 100 billion electronics output, Thailand’s 1.8 million annual vehicle production, and Malaysia’s petrochemical expansions, all integrating sensor-heavy automation to match global quality benchmarks.

Indonesia and the Philippines are automating food and beverage lines, creating new demand for vision and NIR spectrometers. Australia and New Zealand deploy wireless sensors in mining and agriculture; cable runs costing USD 1,000 per meter make wireless economics compelling. Emerging economies such as Bangladesh and Pakistan register nascent uptake limited to basic temperature and gas detection in export-oriented textile mills. Regulatory fragmentation in wireless allotments remains a constraint, but gradual alignment on IEC 61508 and ISO 13849 standards is lowering certification costs for regional rollouts.

Competitive Landscape

Competitive intensity is moderate, with global majors ABB, Siemens, and Honeywell protecting their installed bases through proprietary protocols and bundled analytics. Meanwhile, Omron, Keyence, and Yokogawa win a share of the discrete-manufacturing market by shipping edge-configured sensors that bypass separate gateways. IO-Link’s rapid adoption dismantles historic lock-in, shifting competition toward software differentiation and ecosystem services. Niche players thrive where domain know-how outweighs brand heft, vibration sensing for wind, gas detection for chip fabs, magnetic-field sensing for EV drivetrains.

Strategically, semiconductor vendors such as STMicroelectronics and Infineon are expanding captive MEMS capacity to shield themselves from future shortages. Patent races in wireless power harvesting and deterministic networking hint at forthcoming product waves that slash maintenance overhead. Influence within standards bodies, particularly the IEC 61508 and OPC UA working groups, provides early visibility of compliance and shapes buyer specifications. Buying patterns bifurcate: large enterprises prefer single-vendor stacks for lower integration risk, while SMEs favor open-protocol best-of-breed mixes to preserve flexibility.

Asia-Pacific Industrial Sensors Industry Leaders

Texas Instruments Incorporated

STMicroelectronics N.V.

Emerson Electric Co

Rockwell Automation Inc.

ABB Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2025: Keyence released its AP-X series wireless photoelectric sensors featuring on-device AI for defect classification, enabling real-time inspection on high-speed PCB lines without forwarding image data to external servers.

- August 2025: Honeywell launched an energy-harvesting temperature sensor for cold-chain logistics in India, using thermoelectric conversion to achieve a 12-year maintenance-free lifespan, and secured pilot deployments with two major vaccine manufacturers.

- May 2025: Omron began mass production of its MEMS-based differential pressure sensor at the Kyoto plant, increasing regional capacity by 40% and shortening lead times for automotive customers in Japan and South Korea.

- February 2025: ABB unveiled its Gen 4 multi-protocol pressure sensor platform in Shanghai, adding native IO-Link and OPC UA connectivity that enables seamless integration with mixed-vendor control systems across chemical and food-processing plants.

Asia-Pacific Industrial Sensors Market Report Scope

The Asia-Pacific industrial sensors market report is segmented by Product Type (Pressure, Temperature, Level, Flow, Magnetic Field, Acceleration and Yaw Rate, Gas, Vibration, Proximity, Optical/Photoelectric), End-user Industry (Automotive, Electronics and Semiconductor, Chemical and Petrochemical, Power Generation, Oil and Gas, Food and Beverage, Water and Wastewater, Pharmaceuticals and Life Sciences, Metals and Mining, Aerospace and Defense), Sensor Connectivity (Wired, Wireless, IO-Link, Edge-integrated Smart Sensors), Sensing Technology (MEMS-based, CMOS-based, Piezoresistive, Capacitive, Optical, Electromagnetic), and Geography (China, Japan, South Korea, India, Southeast Asia, Australia and New Zealand, Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Pressure |

| Temperature |

| Level |

| Flow |

| Magnetic Field |

| Acceleration and Yaw Rate |

| Gas |

| Vibration |

| Proximity |

| Optical / Photo-electric |

By End-user Industry

| Automotive |

| Electronics and Semiconductor |

| Chemical and Petrochemical |

| Power Generation |

| Oil and Gas |

| Food and Beverage |

| Water and Wastewater |

| Pharmaceuticals and Life Sciences |

| Metals and Mining |

| Aerospace and Defense |

By Sensor Connectivity

| Wired Sensors |

| Wireless Sensors |

| IO-Link Sensors |

| Edge-integrated Smart Sensors |

By Sensing Technology

| MEMS-based |

| CMOS-based |

| Piezoresistive |

| Capacitive |

| Optical |

| Electromagnetic |

By Geography

| China |

| Japan |

| South Korea |

| India |

| Southeast Asia |

| Australia and New Zealand |

| Rest of Asia-Pacific |

| By Product Type | Pressure |

| Temperature | |

| Level | |

| Flow | |

| Magnetic Field | |

| Acceleration and Yaw Rate | |

| Gas | |

| Vibration | |

| Proximity | |

| Optical / Photo-electric | |

| By End-user Industry | Automotive |

| Electronics and Semiconductor | |

| Chemical and Petrochemical | |

| Power Generation | |

| Oil and Gas | |

| Food and Beverage | |

| Water and Wastewater | |

| Pharmaceuticals and Life Sciences | |

| Metals and Mining | |

| Aerospace and Defense | |

| By Sensor Connectivity | Wired Sensors |

| Wireless Sensors | |

| IO-Link Sensors | |

| Edge-integrated Smart Sensors | |

| By Sensing Technology | MEMS-based |

| CMOS-based | |

| Piezoresistive | |

| Capacitive | |

| Optical | |

| Electromagnetic | |

| By Geography | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Australia and New Zealand | |

| Rest of Asia-Pacific |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the expected value of the Asia Pacific industrial sensors market in 2030?

The market is projected to reach USD 19.09 billion by 2030 based on current growth trajectories.

Which product category currently holds the largest revenue share?

Pressure sensors lead with 34.74% of total revenue due to their prevalence in process control and automotive systems.

Why are wireless sensors growing faster than wired alternatives?

Private 5G roll-outs and IO-Link standardization are overcoming latency and reliability concerns, lowering installation costs and driving a 15.89% CAGR for wireless nodes.

Which end-user segment is forecast to expand the quickest?

Pharmaceuticals and life sciences are set for a 14.99% CAGR as regulators demand continuous environmental monitoring in sterile manufacturing.

How do government incentives influence adoption?

Programs such as India’s PLI and China’s Made in China 2025 subsidize smart-factory investments, effectively converting sensor purchases into compliance requirements and shortening payback periods.