Asia-Pacific Industrial Communication Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

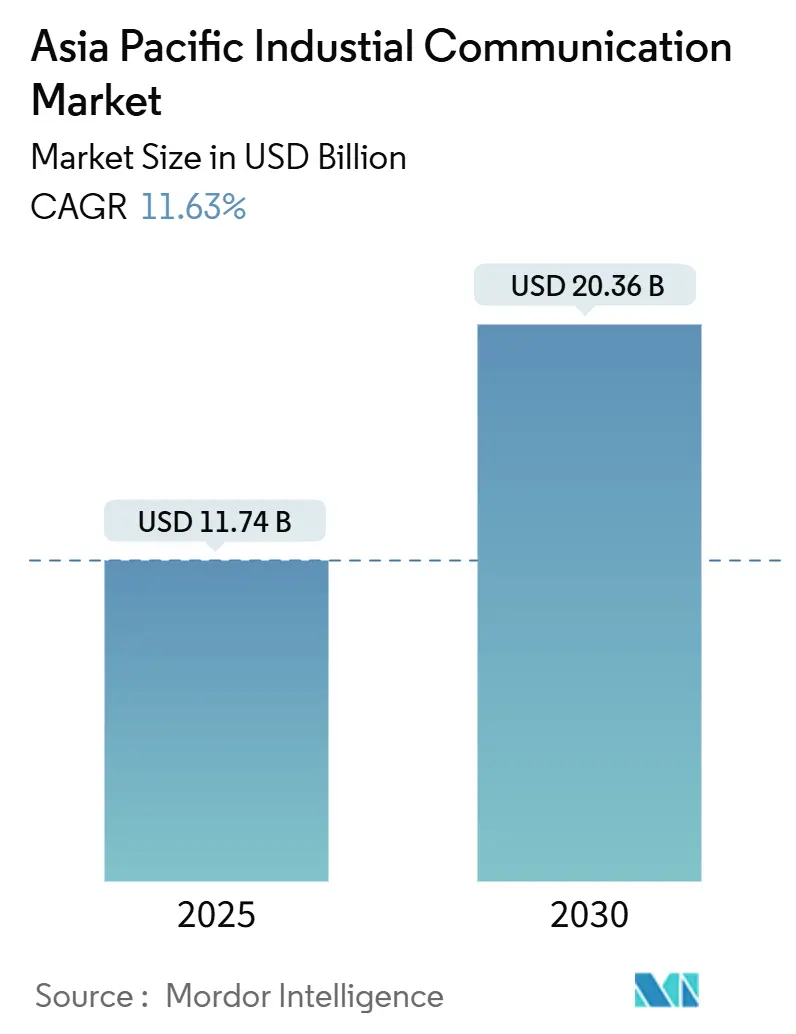

| Market Size (2025) | USD 11.74 Billion |

| Market Size (2030) | USD 20.36 Billion |

| Growth Rate (2025 - 2030) | 11.63% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Industrial Communication Market Analysis by Mordor Intelligence

The Asia-Pacific industrial communication market size is estimated at USD 11.74 billion in 2025 and is projected to reach USD 20.36 billion by 2030, representing a 11.63% CAGR. The acceleration stems from manufacturers retiring legacy fieldbus infrastructure and moving toward converged Ethernet and wireless platforms that support real-time control, edge analytics, and cloud connectivity. China and India together represent the bulk of new node installations as government-supported smart-manufacturing programs broaden electrification across utilities, automotive lines, and semiconductor fabs. Hardware continued to dominate revenue in 2024; however, the shift toward subscription-based remote monitoring and over-the-air updates positions services as the fastest-growing component. Wireless momentum is equally strong, with private-5G campuses and Wi-Fi 6E replacing costly cable runs in hazardous or mobile settings.[1]Siemens Smart Infrastructure, “Infrastructure Transition Monitor 2025,” siemens.com Meanwhile, competitive intensity is heightening as telecom suppliers partner with automation vendors to combine software-defined networking and deterministic industrial control capabilities, forcing smaller protocol providers either to embrace open-source stacks or exit.

Key Report Takeaways

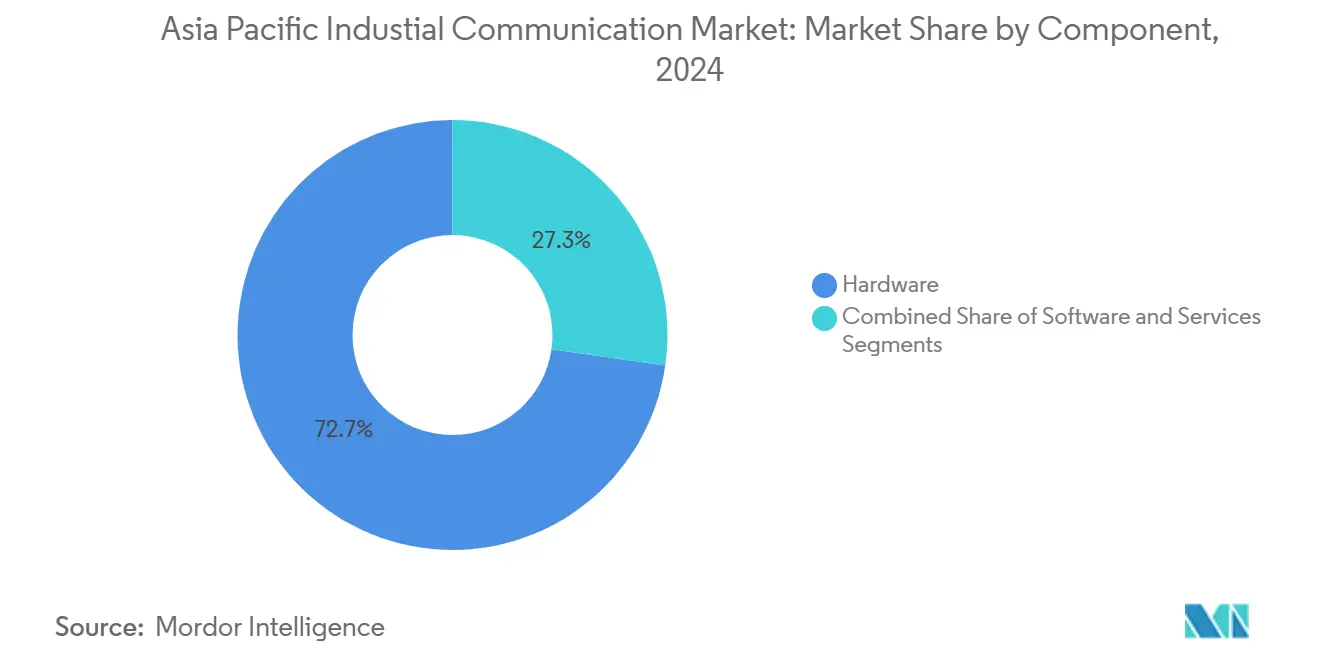

- By component, hardware held 72.73% of Asia-Pacific industrial communication market share in 2024, whereas services are projected to expand at a 12.99% CAGR through 2030.

- By communication type, wired networks accounted for 63.75% of Asia-Pacific industrial communication market size in 2024, while wireless is advancing at a 12.56% CAGR to 2030.

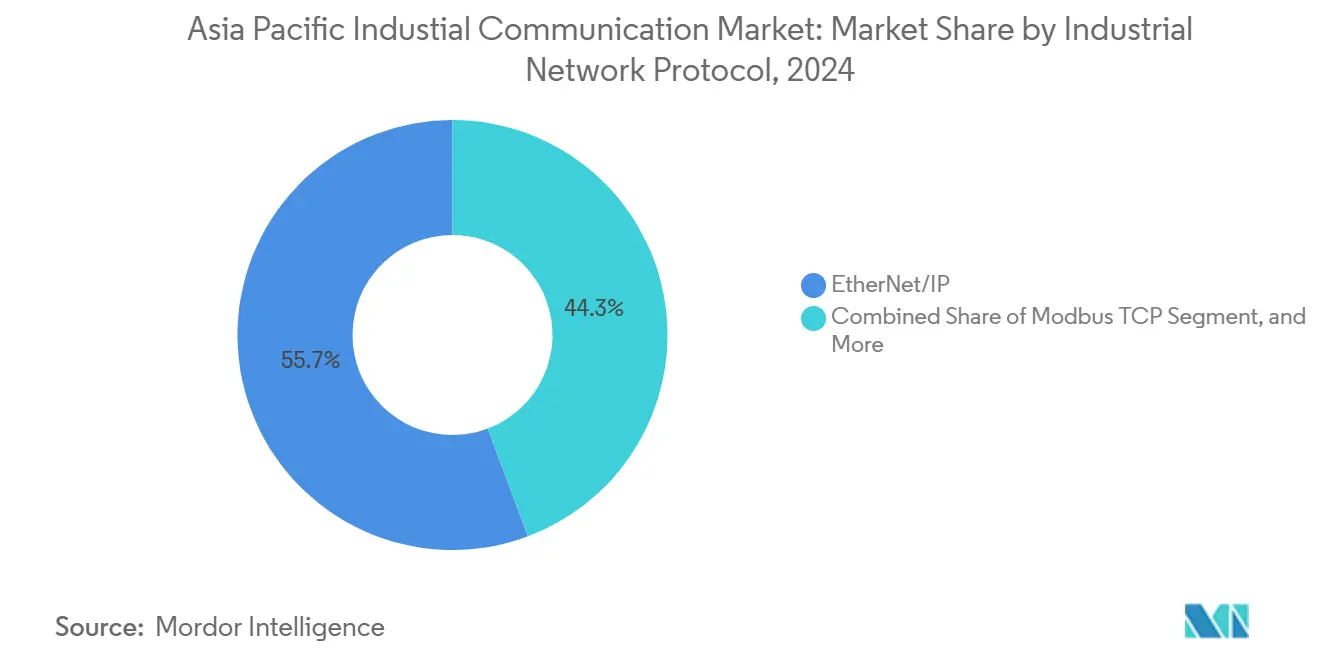

- By protocol, EtherNet/IP commanded 55.72% of Asia-Pacific industrial communication market size in 2024; 5G and private-LTE lead with a 12.44% CAGR through 2030.

- By end-user, automotive led with 28.95% Asia-Pacific industrial communication market share in 2024, yet electronics and semiconductors exhibit the highest growth, at a 12.07% CAGR.

- By geography, China dominated with about 34.68% of Asia-Pacific industrial communication market size in 2024, whereas India records the fastest expansion at a 12.87% CAGR to 2030.

Asia-Pacific Industrial Communication Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of Industry 4.0-driven automation | +2.3% | China, India, Japan, South Korea, Vietnam, Thailand | Medium term (2-4 years) |

| Expansion of 5G and private-LTE industrial campuses | +2.1% | Japan, South Korea, Singapore, Australia, China | Medium term (2-4 years) |

| Proliferation of IIoT edge devices demanding low-latency links | +1.9% | Asia-Pacific core (China, India, Japan, South Korea), spill-over to ASEAN | Short term (≤ 2 years) |

| Government-backed smart-manufacturing initiatives | +1.8% | India, China, Philippines, Indonesia, Malaysia | Long term (≥ 4 years) |

| Rising uptake of Time-Sensitive Networking (TSN) Ethernet | +1.5% | Japan, South Korea, Taiwan, Singapore | Medium term (2-4 years) |

| Shift toward open-source, software-defined industrial protocols | +1.2% | Global, with early adoption in China, India, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Industry 4.0-Driven Automation

Manufacturers across the region lifted smart-technology capital allocations to a range of 11%–15% in 2024, a step-change from sub-5% pre-pandemic levels. Investments extend beyond programmable logic controllers to digital twins and predictive-maintenance platforms, all of which require deterministic multi-protocol backbones. An Industry 4.0 pilot factory in the Philippines, funded by Siemens and Union Bank, showcases interoperability between legacy Modbus devices and next-generation OPC UA servers and lowers adoption barriers for small manufacturers. Such regional demonstrators are accelerating proof-of-value cycles and spurring follow-on orders for converged networks.

Expansion of 5G and Private-LTE Industrial Campuses

Private 5G deployments have transitioned from trials to production, replacing legacy Wi-Fi in electromagnetically noisy environments and supporting mobile robots that require seamless, microsecond-class handovers. Cisco, Mitsui, and KDDI opened a dedicated 5G laboratory in Japan to validate ultra-reliable low-latency applications for automotive assembly and pharmaceutical cleanrooms.[2]Rockwell Automation, “The State of Smart Manufacturing Report,” rockwellautomation.com Japan’s communications ministry reported 23,363 millimeter-wave base stations online in 2024, with a target of 50,000 by 2027, laying the groundwork for pervasive industrial IoT. Licensed spectrum and deterministic quality-of-service policies make private-LTE particularly attractive for mission-critical control.

Proliferation of IIoT Edge Devices Demanding Low-Latency Links

The installed base of wireless field devices is doubling roughly every four years as plants replace 4–20 mA loops in hazardous or mobile equipment. Emerson, for example, surpassed 10 million WirelessHART pressure-transmitter shipments, many of which serve offshore platforms where cable runs are uneconomical.[3]Emerson, “WirelessHART installations milestone,” emerson.com Predictive-maintenance algorithms running at the edge now require sensor refreshes every 50 milliseconds, deterministic wireless options, combining ISA100 and Wi-Fi 6, lower latency, and reduce the bill of materials, thereby accelerating adoption.

Government-Backed Smart-Manufacturing Initiatives

India’s fiscal-2024 budget earmarked INR 11.11 trillion (USD 132.3 billion) toward infrastructure, including dedicated allocations for semiconductor fabs and electric-vehicle supply chains that rely on cleanroom-grade Ethernet and redundant ring topologies. Similar programs in China and Indonesia provide tax holidays and fast-track permitting for factories adopting carbon-efficient automation. The resulting demand for hybrid wired-wireless architectures is fueling integrator pipelines across Southeast Asia.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of retrofitting legacy equipment | -1.4% | China, India, Indonesia, Thailand, Malaysia | Short term (≤ 2 years) |

| Lack of protocol standardisation across vendors | -1.1% | ASEAN (Vietnam, Indonesia, Philippines, Thailand), India | Medium term (2-4 years) |

| Escalating OT-IT cyber-security vulnerabilities | -0.9% | Japan, South Korea, Singapore, Australia | Short term (≤ 2 years) |

| Semiconductor supply-chain disruptions in comms chipsets | -0.8% | Global, acute in China, Taiwan, South Korea | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Retrofitting Legacy Equipment

Plants built before 2010 rely on Modbus-RTU or PROFIBUS networks that cannot natively carry Ethernet traffic, forcing operators to install gateways or entirely new cabling. Siemens’ Infrastructure Transition Monitor surveyed 1,400 executives and found 48% view decarbonization and digitalization as cost-prohibitive. Small enterprises across Indonesia and Thailand face higher financing hurdles, slowing upgrades despite modular retrofit kits entering the market.

Lack of Protocol Standardization Across Vendors

More than 20 Industrial-Ethernet variants persist, each with unique real-time extensions, complicating tool-chains and sparing-parts inventory. HMS Networks confirmed no single protocol exceeds 23% of new nodes, illustrating major fragmentation. Although OPC UA over TSN promises unification, mass firmware updates across millions of devices remain years away.

Segment Analysis

By Component: Services Surge as Operators Shift to Subscription Models

Hardware dominated 72.73% of Asia-Pacific industrial communication market size in 2024. Capital outlays covered industrial switches, gateways, and ruggedized field devices essential for greenfield plants and retrofits. Nevertheless, the migration to cloud-hosted analytics and cybersecurity overlays lifts services revenues at a 12.99% CAGR, the highest among component segments. Rockwell Automation’s State of Smart Manufacturing survey revealed that 79% of facilities operate connected devices, yet only 63% utilize artificial intelligence for efficiency, underscoring a latent appetite for managed analytics.

A parallel pivot toward software-defined networking compresses hardware margins. Vendors are increasingly bundling device management, threat monitoring, and firmware patching into tiered subscription plans, thereby widening their recurring revenue streams. Mitsubishi Electric’s BRIDGE remote-maintenance service and newly launched Serendie industrial-cloud platform exemplify a strategy to decouple earnings from hardware refresh cycles. Over the forecast horizon, services composition will likely shift toward outcome-based guarantees, such as “zero unplanned downtime” contracts tied to performance metrics.

Note: Segment shares of all individual segments available upon report purchase

By Communication Type: Wireless Gains as Factories Replace Cable Runs

Wired networks accounted for 63.75% of Asia-Pacific industrial communication market size in 2024, with Industrial Ethernet supporting high-precision motion control and protective relaying. Fieldbus protocols continued a secular decline, losing 2% of absolute installations. Safety-critical applications, governed by IEC 61508, still favor deterministic wired links that deliver microsecond-class jitter.

Wireless usage, however, is rising at a 12.56% CAGR. Private-5G campuses and Wi-Fi 6E now serve mobile autonomous vehicles, wearables, and hazardous-area sensors where cabling costs or vibration risks are prohibitive. WirelessHART retains niche strength in process plants, but IP-based wireless options are expanding rapidly as spectrum-sharing frameworks mature. Factories adopting licensed private-LTE report paybacks under three years due to reduced downtime and faster line re-configuration. As regulatory clarity around 6 GHz and mm-wave bands spreads beyond Japan and South Korea, adoption is expected to accelerate across ASEAN.

By Industrial Network Protocol: 5G and Private-LTE Disrupt EtherNet/IP Hegemony

EtherNet/IP captured 55.72% Asia-Pacific industrial communication market share in 2024 because of its deep penetration in automotive body-in-white lines and discrete assembly. Rockwell Automation’s live showcase of EtherNet/IP over 5G reveals efforts to extend wired determinism into wireless domains. PROFINET, EtherCAT, and CC-Link IE address regional or performance niches, yet none threatens EtherNet/IP’s installed base before 2030.

The headline challenger is private-5G. Licensed spectrum ensures predictable latency, and built-in network slicing supports segregation of safety and enterprise traffic. The Ministry of Internal Affairs and Communications' target of 50,000 millimeter-wave base stations by 2027 underpins capacity for mobile robotics. As equipment costs fall, greenfield plants may bypass cable-heavy topologies altogether, allowing 5G to chip away at wired leadership positions in flexible production cells.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Electronics and Semiconductors Outpace Automotive

Automotive held 28.95% of Asia-Pacific industrial communication market size in 2024. The pivot to electric vehicles ushers in zonal electrical architectures requiring multi-gigabit Ethernet backbones and battery-cell gigafactories with cleanroom-grade deterministic networks. India’s customs-duty relief on critical minerals and fast-track permits for battery plants intensify regional demand.

Electronics and semiconductors register a 12.07% CAGR, the fastest among verticals. Government incentive schemes across India and Malaysia are driving 300 mm wafer fab projects that demand sub-microsecond synchronization between wafer-handling robots and metrology tools. Cleanroom ISO 14644 standards enforce stainless-steel enclosed switches and fiber-optic cabling; as fabs expand, communication suppliers offering contamination-free hardware gain an edge. Utility, oil and gas, food and beverage, and metals and mining complete the landscape, each with specific latency, bandwidth, and hardening requirements that reward solution tailoring over one-size-fits-all approaches.

Geography Analysis

In 2024, China held a commanding lead in the Asia-Pacific industrial communication market, accounting for approximately 34.68% of the market size. Nationwide 5G coverage reached 96.6% by year-end, and Schneider Electric cites China as its largest automation market, highlighting two-way innovation flows between R&D hubs in Shenzhen and Western plants. ABB’s acquisition of Siemens’ wiring-accessory business in May 2024, adding revenue of more than USD 150 million, underscores confidence despite property-sector volatility.

India is the fastest-growing geography, supported by Production-Linked Incentive schemes and a capital-expenditure envelope topping INR 11.11 trillion in fiscal 2024. The Confederation of Indian Industry reports that manufacturers now direct up to 15% of budgets toward digital-automation initiatives. Hitachi Energy’s USD 4.5 billion R&D expansion elevates India as a global hub for grid-automation technology.

Japan and South Korea exhibit high Industrial-Ethernet penetration and lead private-5G rollouts. The Japanese target of 50,000 millimeter-wave sites by 2027 enables pervasive AR maintenance and mobile robotics in automotive plants. In South Korea, demographic shifts push manufacturers toward full-scale automation to counter labor shortages.

Australia, Taiwan, Singapore, Malaysia, Thailand, and Indonesia constitute smaller but strategic markets. Australia’s mining sector is trialing private-LTE controlled autonomous haulage; Taiwan’s semiconductor dominance demands bleeding-edge deterministic Ethernet; and ASEAN’s annual grid-digitalization budget of USD 22 billion through 2035 fuels utility communication investments.

Competitive Landscape

The Asia-Pacific industrial communication market is moderately concentrated. The top 10 suppliers captured a significant portion of 2024 revenue, leaving ample space for regional specialists. Global leaders, Siemens, ABB, Schneider Electric, Rockwell Automation, Mitsubishi Electric, compete on vertically integrated portfolios and long-term service contracts. Rockwell’s November 2024 integration of Azure IoT Operations within FactoryTalk exemplifies a pivot toward hybrid edge-cloud orchestration, securing recurring subscription revenue.

Telecom incumbents such as Cisco and Nokia are entering factory floors via private-5G solutions that promise deterministic performance. Smaller players, such as Advantech, Moxa, and HMS Networks, focus on protocol gateways and embedded modules that support multi-protocol stacks, enabling machine builders to globalize equipment without redesign. The rise of open-source software is eroding proprietary lock-ins; vendors lacking cloud-native capabilities risk fast commoditization, as Chinese hardware competitors price Industrial-Ethernet switches 30%–40% below those of incumbents.

Asia-Pacific Industrial Communication Industry Leaders

-

Advantech Co., Ltd.

-

Sick AG

-

Moxa Inc.

-

Schneider Electric SE

-

ABB Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Rockwell Automation and Telstra completed a 1 Gbps private-LTE deployment across six Australian iron-ore mines, enabling remote haul-truck control and predictive drill-rig maintenance under a 10-year managed-services contract

- June 2025: ABB launched a subscription-based cybersecurity service for Asia-Pacific utilities, bundling IEC 62443 compliance audits and 24/7 threat monitoring through its Singapore Cybersecurity Operations Center

- March 2025: China’s Ministry of Industry and Information Technology activated its first nationwide TSN interoperability lab in Suzhou, partnering with Schneider Electric and Huawei to certify deterministic-Ethernet devices for smart-manufacturing projects

- January 2025: Mitsubishi Electric opened a USD 200 million industrial-5G test center in Nagoya to validate EtherNet/IP and OPC UA over private-5G for automotive body-in-white lines

Asia-Pacific Industrial Communication Market Report Scope

The Asia-Pacific industrial communication market report is segmented by Component (Hardware, Software, Services), Communication Type (Wired, and Wireless), Industrial Network Protocol (EtherNet/IP, PROFINET, Modbus TCP, EtherCAT, CC-Link IE, OPC UA, Other Industrial Network Protocols), End-User Industry (Automotive, Oil and Gas, Utilities, Food and Beverage, Aerospace and Defense, Metals and Mining, Chemicals and Pharmaceuticals, Electronics and Semiconductors, Other End-User Industries) and Country (China, India, Japan, South Korea, Australia, Taiwan, Singapore, Malaysia, Thailand, Indonesia, Rest of Asia-Pacific). Market Forecasts are Provided in Terms of Value (USD).

| Hardware |

| Software |

| Services |

| Wired Communication | Industrial Ethernet | |

| Fieldbus | ||

| Wireless Communication | Wireless Industrial Communication by Technology | Wi-Fi |

| WirelessHART | ||

| ISA100.11a | ||

| Bluetooth/BLE | ||

| 5G / Private-LTE | ||

| Wireless Industrial Communication by Frequency Band | ||

| EtherNet/IP |

| PROFINET |

| Modbus TCP |

| EtherCAT |

| CC-Link IE |

| OPC UA |

| Other Industrial Network Protocols |

| Automotive |

| Oil and Gas |

| Utilities (Power Generation and Distribution) |

| Food and Beverage |

| Aerospace and Defense |

| Metals and Mining |

| Chemicals and Pharmaceuticals |

| Electronics and Semiconductors |

| Other End-User Industries |

| China |

| India |

| Japan |

| South Korea |

| Australia |

| Taiwan |

| Singapore |

| Malaysia |

| Thailand |

| Indonesia |

| Rest of Asia-Pacific |

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Communication Type | Wired Communication | Industrial Ethernet | |

| Fieldbus | |||

| Wireless Communication | Wireless Industrial Communication by Technology | Wi-Fi | |

| WirelessHART | |||

| ISA100.11a | |||

| Bluetooth/BLE | |||

| 5G / Private-LTE | |||

| Wireless Industrial Communication by Frequency Band | |||

| By Industrial Network Protocol | EtherNet/IP | ||

| PROFINET | |||

| Modbus TCP | |||

| EtherCAT | |||

| CC-Link IE | |||

| OPC UA | |||

| Other Industrial Network Protocols | |||

| By End-User Industry | Automotive | ||

| Oil and Gas | |||

| Utilities (Power Generation and Distribution) | |||

| Food and Beverage | |||

| Aerospace and Defense | |||

| Metals and Mining | |||

| Chemicals and Pharmaceuticals | |||

| Electronics and Semiconductors | |||

| Other End-User Industries | |||

| By Country | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Taiwan | |||

| Singapore | |||

| Malaysia | |||

| Thailand | |||

| Indonesia | |||

| Rest of Asia-Pacific | |||

Key Questions Answered in the Report

How fast is spending on communication networks growing in Asia Pacific factories?

Expenditure is climbing at an 11.63% CAGR, taking the Asia Pacific industrial communication market from USD 11.74 billion in 2025 to USD 20.36 billion in 2030.

Which component category is expanding the quickest?

Services, including remote monitoring and cybersecurity subscriptions, are increasing at a 12.99% CAGR as manufacturers favor outcome-based contracts.

Are wireless links ready for mission-critical control on factory floors?

Private-5G and Wi-Fi 6E deployments now provide sub-10-millisecond latency and deterministic quality-of-service, allowing them to replace cables in hazardous or mobile applications.

Why are electronics fabs demanding deterministic Ethernet?

Cleanroom semiconductor tools must synchronize robotic wafer handling and metrology equipment within 1 microsecond, a requirement met by Time-Sensitive Networking switches and fiber links.

What is the main supply-chain risk for communication hardware?

Extended lead times for multi-protocol ASICs remain a bottleneck, prompting vendors to invest in silicon-carbide capacity and diversify sourcing away from single-region dependence.

Page last updated on: