Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

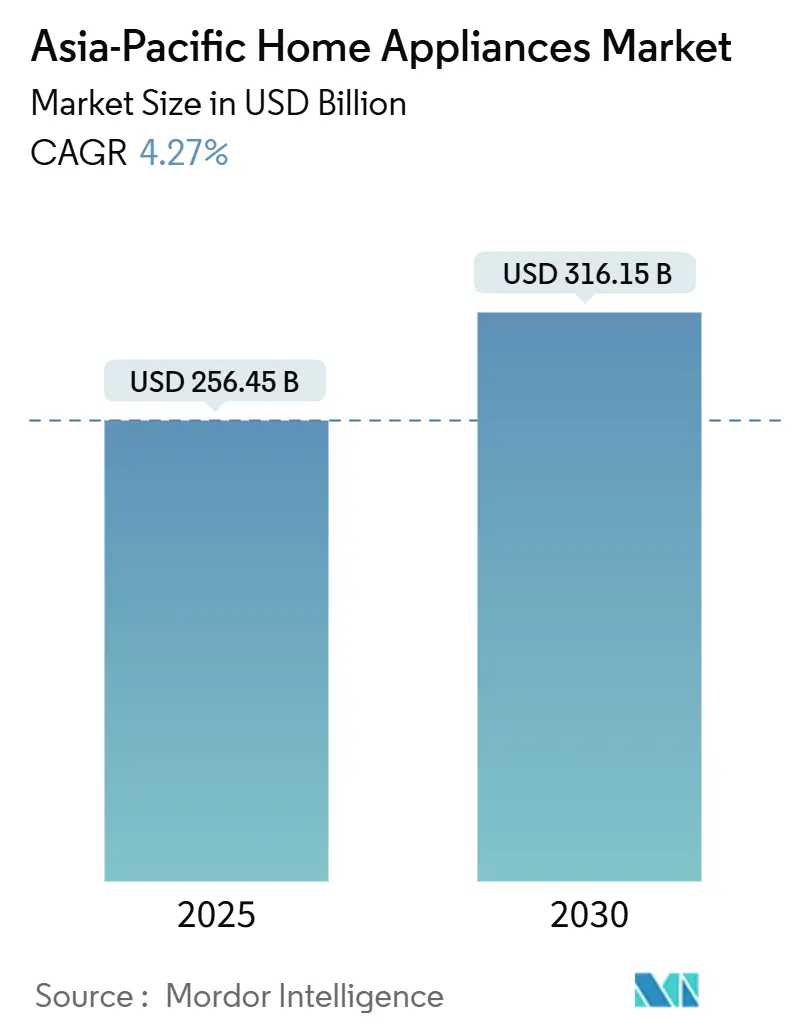

| Market Size (2025) | USD 256.45 Billion |

| Market Size (2030) | USD 316.15 Billion |

| Growth Rate (2025 - 2030) | 4.27% CAGR |

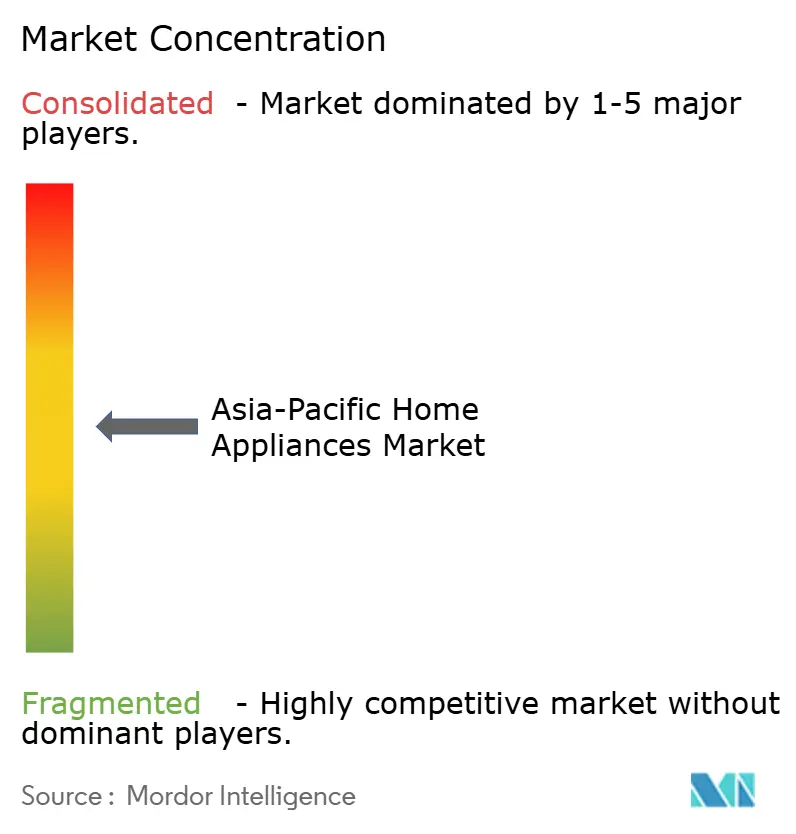

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Home Appliances Market Analysis by Mordor Intelligence

The Asia-Pacific home appliances market size reached USD 256.45 billion in 2025 and is projected to rise to USD 316.15 billion by 2030, reflecting a 4.27% CAGR. Demand growth rests on steady urban migration, larger disposable incomes, and an expanding smart-home ecosystem that lifts penetration of connected refrigerators, air conditioners, and washers. China anchors regional supply through cost-efficient clusters, while India supplies new consumption momentum that balances maturing volumes in Japan and South Korea. Government incentives for high-efficiency models, stronger e-commerce infrastructure, and the appeal of multifunctional designs add further lift. Competitive intensity has sharpened; Chinese brands hold commanding shares in small robotic categories, driving Korean and Japanese leaders to differentiate through artificial-intelligence features. At the same time, raw-material swings and cross-border price wars keep pressure on margins and force ongoing cost management.

Key Report Takeaways

- By product type, refrigerators led with 25.34% of the Asia-Pacific home appliances market share in 2024, while air fryers posted the fastest 6.12% CAGR through 2030.

- By distribution channel, multi-brand stores held 48.77% of the Asia-Pacific home appliances market size in 2024, whereas online sales are set to advance at a 6.54% CAGR to 2030.

- By geography, China commanded 42.83% of Asia-Pacific home appliances market share in 2024, but India records the highest 5.29% CAGR through 2030.

Asia-Pacific Home Appliances Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable incomes in emerging Asia-Pacific economies | +1.2% | India, Southeast Asia, China tier-2/3 cities | Medium term (2-4 years) |

| Rapid urbanisation & new‐housing growth | +0.8% | India, China, Southeast Asia urban corridors | Long term (≥ 4 years) |

| E-commerce expansion & last-mile reach | +0.6% | Indonesia, Philippines, Vietnam, India | Short term (≤ 2 years) |

| Energy-efficiency subsidy programmes | +0.4% | Malaysia, South Korea, Australia, Thailand | Short term (≤ 2 years) |

| AIoT-enabled smart-home ecosystems | +0.5% | China, South Korea, Japan, Singapore | Medium term (2-4 years) |

| Compact-living demand for multifunctional units | +0.3% | Hong Kong, Singapore, major urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Incomes in Emerging Asia-Pacific Economies

Income growth in emerging Asia-Pacific markets creates a consumption upgrade cycle that extends beyond basic appliance penetration to premium feature adoption. India's appliances industry expects 10-15% growth in 2025 driven by premiumisation, with room air conditioners growing 30% in 2024 as rising incomes enable energy-efficient inverter models. This trend reflects a structural shift where middle-class expansion in tier-2 and tier-3 cities generates demand for branded appliances with advanced features, moving beyond the price-sensitive segments that dominated earlier growth phases. The income elasticity effect is particularly pronounced in categories like refrigerators and washing machines, where consumers upgrade to larger capacities and smart connectivity features as household purchasing power increases.

Rapid Urbanization & New-Housing Growth

Urban population growth across developing Asia creates concentrated appliance demand that outpaces rural market development, with city clusters accounting for most absolute increases in household formation. The Asian Development Bank projects urban population rising from 1.84 billion in 2017 to reach 64% urbanization by 2050, with large cities and urban corridors generating agglomeration economies that support higher appliance adoption rates[1]Source: Asian Development Bank, “Asian Development Outlook Update,” adb.org. New housing construction in urban areas drives initial appliance purchases, while apartment-style living increases demand for space-efficient, built-in models that integrate with modern kitchen designs. This urbanization pattern creates geographic concentration of demand that enables efficient distribution networks and after-sales service coverage, supporting market expansion in previously underserved regions.

E-commerce Expansion & Last-mile Reach

Digital sales channels are significantly transforming appliance distribution by enabling manufacturers to establish direct relationships with consumers and substantially expanding their market reach. These channels provide manufacturers with the ability to bypass intermediaries, allowing for more streamlined operations and cost efficiencies. In the Philippines, digital adoption is witnessing remarkable growth, with online sales increasing from a 40.4% share to a projected 48.0% by 2029. This growth is fueled by improved infrastructure, such as enhanced internet connectivity and logistics networks, and rising consumer confidence in making substantial online purchases. The convenience of online platforms has made it easier for consumers to access a wide range of products, including large-ticket items, from the comfort of their homes.

AIoT-enabled Smart-home Ecosystems

Connected appliance adoption accelerates as 5G infrastructure deployment and IoT standardization create seamless integration opportunities across device categories. Samsung's 2025 AI Home lineup demonstrates this convergence, with expanded touchscreens across refrigerators, washers, and ovens enabling voice recognition and personalized automation. Smart appliance market potential could exceed USD 600 billion by 2030, with air conditioners, refrigerators, and washing machines leading AI integration for energy optimization and predictive maintenance. This technological shift enables subscription-based service models that create recurring revenue streams beyond traditional hardware sales, fundamentally altering competitive dynamics and customer relationships.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility | -0.7% | Global, particularly India and Southeast Asia | Short term (≤ 2 years) |

| Saturation in mature APAC countries | -0.5% | Japan, South Korea, Australia, New Zealand | Long term (≥ 4 years) |

| Cross-border e-commerce price wars | -0.4% | Korea, Japan, premium segments globally | Medium term (2-4 years) |

| Stringent e-waste compliance costs | -0.2% | EU-exporting manufacturers, developed APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-material Price Volatility

Commodity cost fluctuations create margin pressure that forces manufacturers to implement price increases or absorb reduced profitability, both of which constrain market growth. Indian appliance manufacturers faced 70% increases in metals and plastics costs during 2024, prompting industry-wide price hikes of 5-10% across air conditioners, refrigerators, and washing machines. This cost inflation particularly affects steel-intensive products like refrigerators and washing machines, where material costs represent 60-70% of manufacturing expenses. Supply chain disruptions and geopolitical tensions exacerbate volatility, forcing manufacturers to maintain higher inventory buffers and implement more frequent pricing adjustments that can dampen consumer demand in price-sensitive segments.

Cross-border E-commerce Price Wars

Digital platform competition enables direct price comparison across brands and geographies, intensifying competitive pressure and compressing margins across all market segments. Chinese manufacturers leverage manufacturing scale and direct-to-consumer models to offer substantial price advantages, with Xiaomi entering Korea at 599,800-649,800 won compared to premium Korean alternatives[2] Source: Shanghai Metals Market, “Home Appliance Sales Hit a Record High in 2024,” news.metal.com. This pricing pressure extends beyond low-end segments as Chinese brands upgrade product quality and design, forcing established players to compete on value rather than brand premium alone. The result is margin compression across the industry as traditional pricing power erodes under transparent digital comparison shopping and direct manufacturer competition.

Segment Analysis

By Product Type: Small Appliances Accelerate, Large Appliances Sustain Core Value

Asia-Pacific home appliances market size for refrigerators stood as the largest slice at 25.34% in 2024. Strong household stock combined with longer replacement intervals secures a stable demand floor, while innovations in compressor efficiency and AI food management keep the category relevant. Conversely, air fryers record a 6.12% CAGR through 2030, demonstrating how small appliances can shift cooking behavior toward healthier, low-oil meal preparation. Robotic vacuum cleaners, multi-cookers, and countertop ovens follow similar momentum, aided by gift purchases and impulse e-commerce deals.

Air conditioners, washing machines, and dishwashers remain value pillars because each unit carries a higher average selling price and requires installation services. Brands inject AI diagnostics and inverter drives to refresh these categories without fundamentally altering core functions. In contrast, vacuum cleaners face cannibalization by robo-variants that tie into smart-home hubs. The clear divide between mature large appliances and fast-growing small appliances calls for portfolio strategies that balance high-value steady segments with nimble growth niches.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Omnichannel Becomes the Default

Multi-brand stores captured 48.77% of the Asia-Pacific home appliances market size in 2024, due to immediate product availability, hands-on demos, and access to financing plans. Their floor space supports comparison across brands, which remains important for higher-ticket items. Online platforms, however, show the strongest trajectory with a 6.54% CAGR. Faster last-mile delivery, richer product content, and easy return policies now persuade consumers to finalize even USD 1,000 refrigerator purchases through mobile apps.

Exclusive brand outlets thrive in premium segments, offering curated ecosystems that highlight design consistency across appliance lines. Department stores and hypermarkets struggle to maintain relevance as specialized retailers and e-commerce both outperform them on assortment depth and price transparency. Most shoppers now begin research online, visit a physical store for validation, and then transact on whichever channel offers the best final price, making seamless inventory and pricing visibility critical.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

China’s 42.83% share anchors the Asia-Pacific home appliances market. Domestic consumption, elevated by trade-in subsidies, pairs with export leadership for a two-engine model that funds continuous R&D investment. At the same time, rising wages and tighter environmental rules move some production to lower-cost neighbors, yet design and component sourcing often remain within Chinese clusters.

India’s 5.29% CAGR reflects under-penetration and rising disposable incomes that emulate China’s earlier trajectory. Production-Linked Incentive schemes attract global OEMs to localize compressor and PCB manufacture, reducing import reliance and improving time-to-market. Japan and South Korea rely on high replacement rates and premium innovations to hold value, whereas Australia and New Zealand benefit from steady immigration and housing completions. Southeast Asia delivers balanced volume and value growth, supported by e-commerce accessibility and a young demographic profile.

Japan and South Korea represent mature markets where replacement demand and premium positioning drive value growth despite volume constraints. South Korea's appliance manufacturers face intensifying competition from Chinese brands, with Roborock capturing 46.5% of the domestic robot vacuum market and Chinese TV makers Hisense and TCL establishing local operations. This competitive pressure forces Korean incumbents Samsung and LG to emphasize technological differentiation through AI integration and premium design, while expanding overseas operations to maintain growth momentum. Southeast Asia shows strong potential driven by urbanization and e-commerce adoption, with Indonesia's household appliances e-commerce reaching USD 5.64 billion and the Philippines achieving 40.4% online penetration ECDB. Regional diversity creates opportunities for tailored strategies that balance local preferences with manufacturing efficiency, though it requires sophisticated market entry and distribution approaches.

Competitive Landscape

The Asia-Pacific home appliances market presents moderate consolidation. In refrigerators and washers, Haier, Samsung, and LG account for more than half of regional shipments, while small appliance segments host dozens of agile competitors. Chinese robot-vacuum makers own 63% of the global supply, prompting Korean and Japanese players to release AI-enabled premium models. Companies pursue scale through vertical integration: compressor plants, PCB assembly, and smartphone-derived display modules remain in-house to secure cost and technology advantages.

Innovation themes converge on connectivity and energy command. Samsung’s 2025 portfolio integrates voice-activated dashboards across most large appliances[3]Source: Samsung Electronics, “Samsung Unveils New Refrigerators with AI Hybrid Cooling Technology,” news.samsung.com. Haier invests in overseas parks in Thailand and Egypt to short-circuit tariff risk and shorten shipping lanes. Circular-economy pilots, such as SCGC’s closed-loop recycling with HomePro, convert returned appliances into recycled polymer feedstock, reducing virgin resin dependence. Direct-to-consumer models gain traction; brands use online configurators to let buyers customize panel colors and receive factory-direct deliveries within one week. Incumbents answer by expanding experience centers that showcase full smart-home suites rather than isolated products.

Pricing battles intensify across borderless digital platforms. A premium Japanese dishwasher can now face a similar-spec Chinese rival priced 20% lower, visible on the same search results page. Profit pools therefore migrate toward aftermarket services, extended warranties, and subscription refill programs. Ecosystem lock-in, powered by proprietary apps and cloud analytics, becomes a strategic shield against pure price comparison.

Asia-Pacific Home Appliances Industry Leaders

-

Haier Smart Home Co., Ltd.

-

Midea Group Co., Ltd.

-

Samsung Electronics Co.

-

LG Electronics Inc.

-

Panasonic Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: Xiaomi has officially unveiled its latest lineup of AI-powered smart appliances, signaling a deeper expansion into the Internet of Things (IoT) market across Southeast Asia.

- March 2025: Samsung Electronics unveiled its 2025 AI Home lineup featuring expanded touchscreens and Voice ID across multiple appliance categories.

- February 2025: AtHome raised KRW 18 billion (USD 13 million) Series A funding to expand global sales of its Minix food-waste dryer

- January 2025: Malaysia launched the NUR@PETRA e-rebate program, offering up to RM 400 for households purchasing five-star refrigerators or air conditioners.

Asia-Pacific Home Appliances Market Report Scope

A home appliance, also known as a domestic appliance assists in household functions such as cooking, cleaning, and food preservation. the Asia Pacific home appliances market is segmented by major appliances, small appliances, distribution channels, and by country. Major appliances are segmented by refrigerators, freezers, dishwashing machines, washing machines, cookers, ovens, and other major appliances. Small appliances are segmented by vacuum cleaners, coffee machines, irons, toasters, grills and roasters, and other small appliances. Distribution channels are segmented by multi-brand stores, exclusive stores, online, and other distribution channels, and by country (China, India, Japan, South Korea, Australia, New Zealand, rest of Asia Pacific. the report offers market size and forecasts for the Asia Pacific home appliances market in value (USD) for all the above segments.

By Product Type

| Major Home Appliances | Refrigerators |

| Freezers | |

| Washing Machines | |

| Dishwashers | |

| Ovens (Incl. Combi & Microwave) | |

| Air Conditioners | |

| Other Major Home Appliances | |

| Small Home Appliances | Coffee Makers |

| Food Processors | |

| Grills & Roasters | |

| Electric Kettles | |

| Juicers & Blenders | |

| Air Fryers | |

| Vacuum Cleaners | |

| Electric Rice Cookers | |

| Toasters | |

| Countertop Ovens | |

| Other Small Home Appliances |

By Distribution Channel

| Multi-Brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

By Geography

| India |

| China |

| Japan |

| Australia |

| South Korea |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) |

| Rest of Asia-Pacific |

| By Product Type | Major Home Appliances | Refrigerators |

| Freezers | ||

| Washing Machines | ||

| Dishwashers | ||

| Ovens (Incl. Combi & Microwave) | ||

| Air Conditioners | ||

| Other Major Home Appliances | ||

| Small Home Appliances | Coffee Makers | |

| Food Processors | ||

| Grills & Roasters | ||

| Electric Kettles | ||

| Juicers & Blenders | ||

| Air Fryers | ||

| Vacuum Cleaners | ||

| Electric Rice Cookers | ||

| Toasters | ||

| Countertop Ovens | ||

| Other Small Home Appliances | ||

| By Distribution Channel | Multi-Brand Stores | |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Asia Pacific home appliances market?

The market stood at USD 256.45 billion in 2025 and is forecast to reach USD 316.15 billion by 2030.

Which product category leads sales in the region?

Refrigerators command the largest share at 25.34% of 2024 revenue.

What channel is growing fastest for appliance purchases?

Online sales posts a 6.54% CAGR through 2030, driven by stronger logistics and consumer confidence.

Which country contributes most to regional revenue?

China accounts for 42.83% of total value, supported by both domestic demand and export output.

Where is the fastest growth expected?

India shows the highest forward CAGR of 5.29% through 2030 as rising incomes spur first-time and replacement purchases.

Page last updated on: