Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

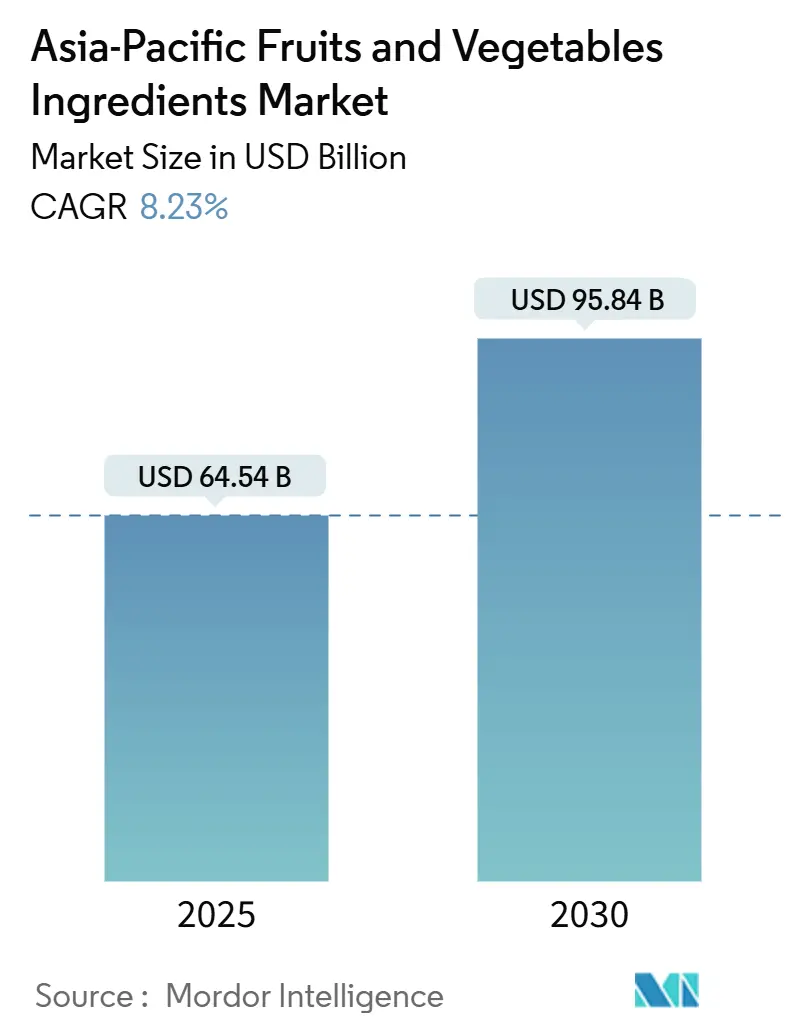

| Market Size (2025) | USD 64.54 Billion |

| Market Size (2030) | USD 95.84 Billion |

| Growth Rate (2025 - 2030) | 8.23% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Fruits And Vegetables Ingredients Market Analysis by Mordor Intelligence

The Asia-Pacific fruits and vegetables ingredients market size reached USD 64.54 million in 2025 and is set to expand to USD 95.84 million by 2030, registering an 8.23% CAGR. Ingredient buyers are shifting their focus from synthetic additives to recognizable fruit and vegetable derivatives in response to tightening regulations and growing consumer demand for cleaner labels. Thailand’s Phase 4 sugar-tax escalation in April 2025 and Indonesia’s draft Nutri-Level rules are forcing beverage makers to reformulate with mango, pineapple, and berry concentrates that help curb added sugars while maintaining taste. Trade blocs, such as the Regional Comprehensive Economic Partnership, are lowering tariffs on processed foods, thereby widening export avenues for Chinese and ASEAN processors that bundle fruits and vegetables into value-added products. At the consumer level, 70% of shoppers now scrutinize ingredient lists, and 58% are willing to accept a price premium for shorter, natural formulations, signaling sustained demand momentum for cleaner ingredient solutions.

Key Report Takeaways

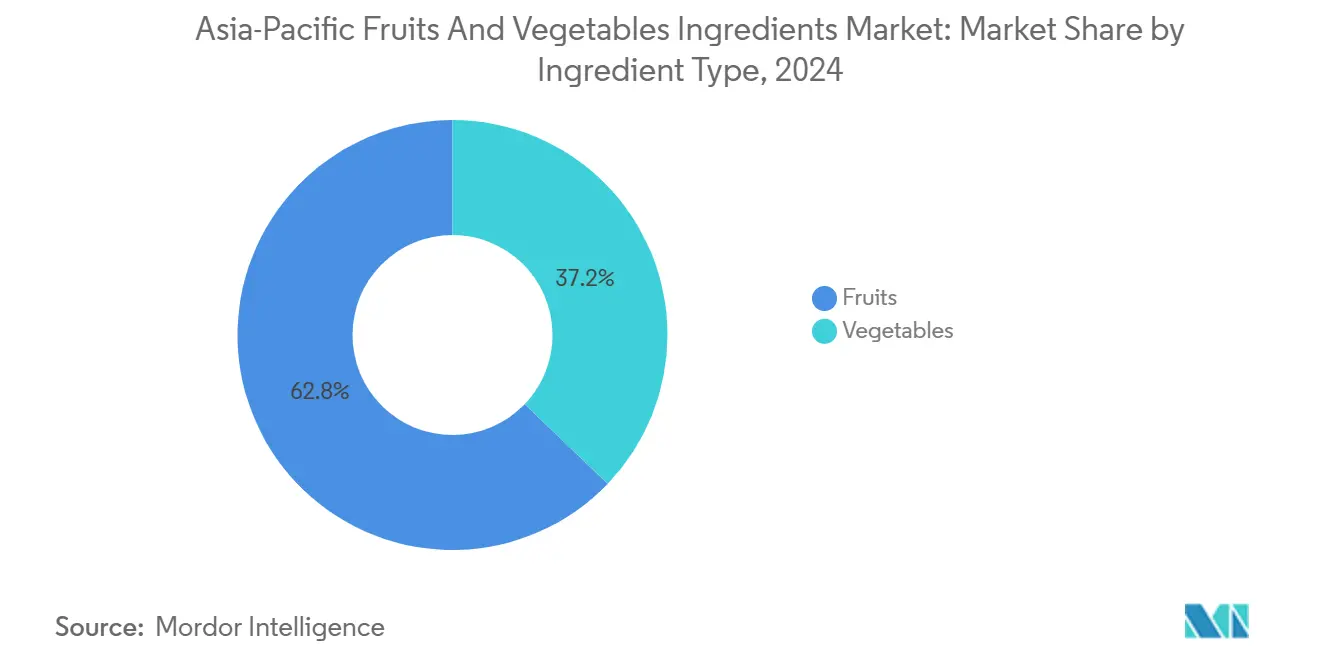

- By ingredient type, fruit derivatives led with a 62.84% Asia-Pacific fruits and vegetables ingredients market share in 2024, while vegetable ingredients are advancing at a 9.28% CAGR through 2030.

- By form, concentrates held 41.26% of the Asia-Pacific fruits and vegetables ingredients market size in 2024, whereas NFC juices are projected to climb at a 10.35% CAGR to 2030.

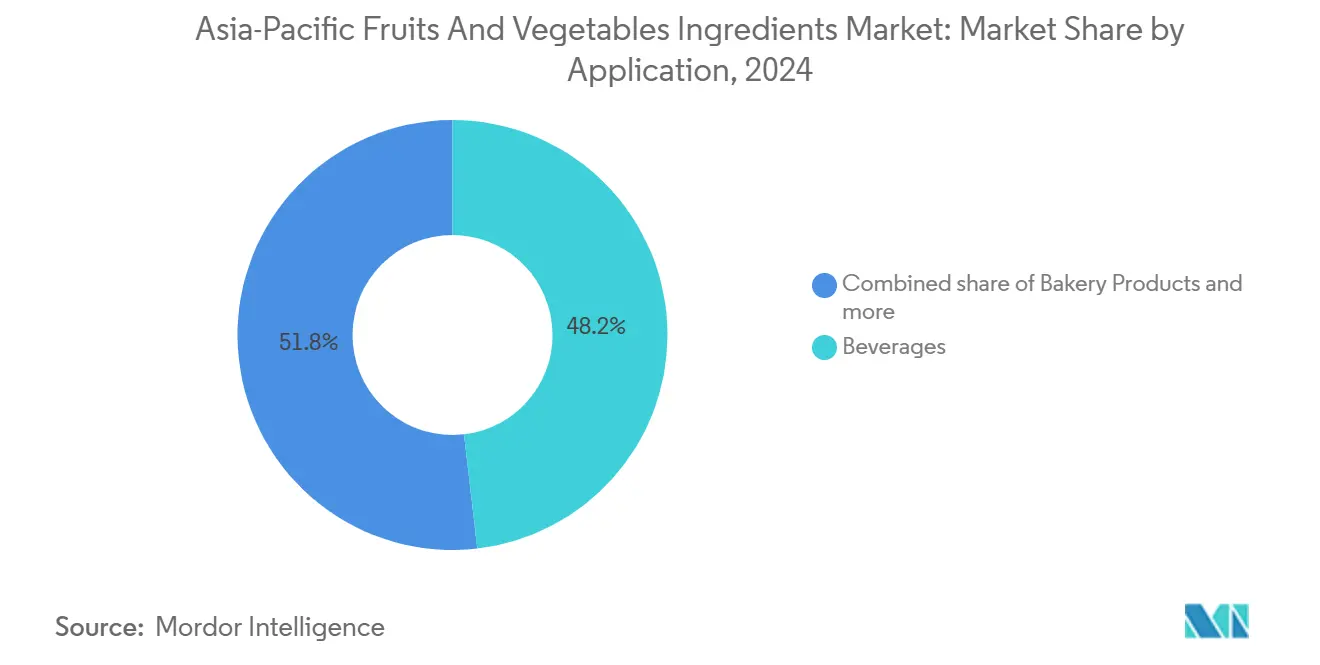

- By application, beverages accounted for 48.17% of demand in 2024, but ready-to-eat formats are expanding at a 10.64% CAGR over the forecast window.

- China controlled 53.62% of the regional value in 2024; however, India is set to grow at a 9.79% CAGR, driven by cold-chain subsidies and production incentives.

Asia-Pacific Fruits And Vegetables Ingredients Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for clean-label and natural ingredients in packaged foods | +1.8% | Global, with peak intensity in China, Thailand, Indonesia, Singapore | Medium term (2-4 years) |

| Growing adoption of fruit-based sugar-replacers by beverage formulators | +1.5% | ASEAN core (Thailand, Indonesia, Vietnam), spill-over to India, Australia | Short term (≤ 2 years) |

| Functional-food launches featuring super-fruit phytonutrients | +1.2% | Japan, South Korea, urban China, Singapore | Medium term (2-4 years) |

| Growth of plant-based and vegan foods | +1.4% | China, India, Australia, urban Southeast Asia | Long term (≥ 4 years) |

| Surge of processed food exports from China and ASEAN | +1.1% | China (Shandong, Shaanxi), Thailand, Vietnam, Indonesia | Medium term (2-4 years) |

| Cold-chain subsidies by APAC governments | +0.9% | India (PMKSY program), China (national logistics plan), Vietnam, Indonesia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Clean-Label and Natural Ingredients in Packaged Foods

Regulatory pressure and rising consumer awareness are driving packaged-food makers to replace synthetic additives with fruit- and vegetable-based ingredients. Indonesia’s 2024 draft Nutri-Level labeling requires front-of-pack warnings for high sugar, salt, or saturated fat, prompting reformulation with natural sweeteners and colorants, such as dragon fruit and beetroot, according to BPOM[1]Source: Indonesia BPOM, “Nutri-Level Draft Regulation,” pom.go.id. Thailand’s Phase 4 sugar tax (effective April 2025) and Singapore’s 2024 Nutri-Grade labeling similarly encourage manufacturers to shift toward fruit concentrates and monk fruit extracts, while Vietnam introduces a new tax on sweetened beverages[2]Source: Thai FDA, “Sugar-Tax Phase 4 Implementation,” fda.moph.go.th . Consumer trends support this shift: Cargill’s 2025 APAC survey reveals that 58% are willing to pay more for recognizable, natural ingredients, and over 70% actively check labels. Global influences, such as the U.S. FDA’s updated “healthy” claim rules, effective as of 2028, are also shaping Asia-Pacific ingredient strategies and increasing the value of clean-label offerings.

Growing Adoption of Fruit-Based Sugar-Replacers by Beverage Formulators

Beverage makers are increasingly replacing refined sucrose with fruit-derived sweeteners to meet sugar tax regulations and tap into the premiumization trend, thereby boosting demand for concentrates, NFC juices, and powdered fruit extracts. Thailand’s April 2025 sugar tax hike targets drinks with more than 10 g/100 ml. The 2018–2023 reformulations saw producers reduce the average sugar content by 18% using blends of cane sugar, monk fruit, stevia, and fruit concentrates, according to the Thai FDA. Innovations like NutraEx Food’s July 2024 BI-Sugar, which combines L-arabinose with sucrose and stevia to reduce glycemic response while maintaining sweetness, exemplify technical advances. Meanwhile, Samyang Corporation’s September 2024 KRW 140 billion specialty plant in Ulsan, South Korea, now produces 13,000 tons per year of allulose, a rare low-calorie sugar gaining traction in APAC beverages. Rising fiscal penalties and consumer demand for “no artificial sweeteners” labels are expected to expand the fruit-based sugar-replacer market by roughly 1.5 percentage points of CAGR through 2030.

Functional-Food Launches Featuring Super-Fruit Phytonutrients

Functional-food brands in the Asia-Pacific region are increasingly utilizing exotic fruit extracts, rich in polyphenols, anthocyanins, and carotenoids, to support immunity, gut health, and cognitive performance, driving demand for freeze-dried powders and concentrated phytonutrients. Thailand’s FDA updated its health-claim guidelines in July 2024, streamlining approval for botanicals like butterfly pea, dragon fruit, and mangosteen. Meanwhile, the WHO’s 2024 safety evaluation of butterfly pea flower extract bolsters cross-border trade and regulatory acceptance in markets such as Japan, South Korea, and Australia[3]Source: WHO JECFA, “Safety Evaluation of Butterfly-Pea Extract,” who.int. Nurasa opened its 3,840 m² Food Tech Innovation Centre in Singapore in April 2024, featuring precision-fermentation labs and bioreactors. The centre collaborates with A*STAR and ScaleUpBio to develop low-sugar, gut-friendly products that leverage fruit-derived prebiotics and polyphenols. Similarly, Kagome’s January 2025 strategy shift from a “tomato company” to a “vegetable company” highlights the move toward functional products using diverse fruit and vegetable phytonutrients. According to the Asian Food and Beverage Alliance, the APAC fortification market is growing at over 18% CAGR (2022–2027), with super-fruit ingredients serving as both functional actives and clean-label marketing assets.

Growth of Plant-Based and Vegan Foods

The plant-based meat, dairy, and snack sectors are growing rapidly across urban Asia, with fruit and vegetable ingredients being used to enhance texture, flavor, and nutrition. In November 2024, Nourish Ingredients partnered with China’s Cabio Biotech to produce Tastilux, a precision-fermentation fat derived from Mortierella alpina, upcycling fruit and vegetable by-products to achieve a meaty aroma at a sub-1% inclusion rate, targeting China’s plant-based meat market in 2025. Similarly, Kinoko-Tech’s October 2024 agreement with Metaphor Foods will scale up fungi-mycelium protein production in Australia, with plans to expand to Malaysia, Singapore, Indonesia, and New Zealand, utilizing legumes and grains to enhance protein and fiber content while maintaining taste. Other launches, including Thammasat University’s GreenTein mung-bean protein drink and Yeo’s immunity-focused soy milk, demonstrate that plant-based formats are going mainstream. Rising health awareness, environmental concerns, and improved taste profiles are adding approximately 1.4 percentage points to the market's CAGR, with long-term growth expected as distribution and pricing approach parity with animal-based products.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility due to climate and pests | -0.8% | Philippines, Thailand, India, Vietnam, Indonesia | Short term (≤ 2 years) |

| Competition from synthetic substitutes | -0.6% | Global, with higher intensity in cost-sensitive segments (confectionery, bakery) | Medium term (2-4 years) |

| High CAPEX for aseptic and freeze-drying lines | -0.7% | China, India, Thailand, Indonesia, Malaysia | Medium term (2-4 years) |

| Complex multi-country regulatory approvals | -0.5% | ASEAN, China, India, Japan, South Korea, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility Due to Climate and Pests

Extreme weather and pest outbreaks are disrupting fruit and vegetable harvests across the Asia-Pacific region, resulting in supply shortages, price spikes, and increased processing costs. In 2024, typhoons and heavy rains in the Philippines damaged leafy greens, tomatoes, and root crops, driving up local prices by 30–50%. Meanwhile, droughts in northern Thailand reduced mango and longan yields, forcing processors to source from India and Pakistan at higher costs, according to the FAO. China’s apple regions in Shaanxi and Shandong also faced lower-than-expected harvests due to temperature extremes and irregular rainfall. Pest pressures, including fruit flies and aphids, further reduce yields and increase post-harvest sorting costs by 12–18%. The FAO Food Price Index showed month-to-month swings of over 10% for tropical fruits and 8% for processed vegetables, complicating long-term contracts. This volatility is expected to reduce short-term market CAGR by 0.8 percentage points, with relief anticipated as climate-resilient crops and better irrigation systems are introduced.

Competition from Synthetic Substitutes

Synthetic flavors, colors, and sweeteners remain popular in price-sensitive markets, such as confectionery, bakery, and mass-market beverages, due to their lower costs and stable supply. For instance, synthetic vanillin costs about 10% of natural vanilla, while synthetic beta-carotene offers a more stable color under heat, extending shelf life. Despite rising demand for clean labels, manufacturers in India, Indonesia, and the Philippines continue to use synthetics to keep retail prices below USD 1, which is crucial for high-volume traditional trade. APAC regulations generally permit GRAS-status synthetics, and inconsistent enforcement results in reduced penalties. With natural ingredient prices expected to remain volatile in 2024–2025, synthetic substitutes are likely to remain attractive, limiting market CAGR by around 0.6 percentage points. However, tighter labeling and sugar tax rules in Thailand, Indonesia, and Singapore are gradually encouraging the use of natural alternatives.

Segment Analysis

By Ingredient Type: Vegetables Outpace Fruits Despite Smaller Base

Vegetable ingredients are projected to grow at the fastest rate, with a 9.28% CAGR from 2025 to 2030, despite fruits holding a 62.84% share in 2024. The rise of plant-based and functional foods is driving demand for vegetable-derived proteins, fibers, and phytonutrients in meat alternatives, dairy substitutes, and fortified snacks. Kagome’s January 2025 pivot from a “tomato company” to a “vegetable company” highlights opportunities to expand beyond pastes and purees into freeze-dried powders, concentrated extracts, and fermented derivatives. Carrots, beets, and tomatoes dominate volumes, with beetroot powder replacing synthetic Red 40 and carmine in plant-based burgers and dairy-free yogurts. Meanwhile, pumpkins and butternuts add natural texture and mild sweetness to bakery and confectionery applications.

Fruits remain the largest ingredient segment due to their entrenched use in beverages, confectionery, and bakery products, with apples, oranges, pineapples, mangoes, and bananas providing both flavor and functional benefits, such as pectin and natural acidity. Berries, including strawberries, blueberries, and raspberries, are the fastest-growing fruit segment, driven by the health benefits of anthocyanins and their positioning as superfoods in functional beverages and dairy products. Exotic fruits like kiwi cater to premium niches in Japan, South Korea, and urban China. Regional launches, such as I.P. Natural Products’ May 2024 Ivy-brand tamarind and plum juices in Thailand packaged in SIG XSlimBloc cartons, showcase on-the-go commercialization of local flavors. Vegetable ingredients also benefit from simpler regulatory approval under FSSAI and ASEAN frameworks, while novel fruit extracts often require toxicology dossiers, influencing innovation and market strategy.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Form: NFC Juices Surge on Premiumization

NFC (not-from-concentrate) juices are expected to grow at the fastest rate among form segments, with a 10.35% CAGR from 2025 to 2030, despite concentrates holding a 41.26% share in 2024. Premiumization is driving this trend, with consumers in Japan, South Korea, Australia, and urban China willing to pay 30–50% more for minimally processed juices that preserve delicate aromatics and heat-sensitive vitamins. NFC production relies on cold-chain logistics, and subsidies for refrigerated transport in India, China, and Vietnam are reducing costs that previously limited adoption to luxury brands. Concentrates remain key for cost-sensitive beverages, confectionery fillings, and bakery glazes, while pastes and purees, led by tomato and mango, serve the dairy, ready-to-eat meals, and sauce markets.

Powders are gaining traction in functional foods and dietary supplements, delivering concentrated phytonutrients and fiber in compact sachets, capsules, and ready-to-mix beverages. Ingredion’s September 2024 APAC launch of FIBERTEX CF 500 and CF 100 citrus fiber, derived from upcycled peel, highlights advances in powder functionality, providing texturizing, gelling, and viscosifying properties that can replace starches, hydrocolloids, and eggs across multiple applications. Consumer research shows 87% of APAC buyers accept citrus fiber on labels, while 79% globally prefer recognizable ingredients, supporting clean-label positioning. Pieces and slices target premium bakery, confectionery, and ready-to-eat meals for visual and textural appeal. Processing innovations such as aseptic packaging and freeze-drying are shaping form segmentation, enabling broader NFC distribution and new powder applications in e-commerce and export markets.

By Application: RTE Products Lead Growth

Ready-to-eat (RTE) products are projected to grow at the fastest rate among applications, with a 10.64% CAGR from 2025 to 2030, despite beverages accounting for 48.17% of 2024 sales. Urban Asia’s rising dual-income households, e-commerce growth, and demand for convenient, nutritious options are driving RTE meals, snack bars, and meal kits. Fruit and vegetable ingredients provide flavor, texture, and nutrition, with freeze-dried vegetables, fruit purees, and concentrated extracts enabling the creation of shelf-stable, clean-label products. Examples include Wantian’s October 2024 partnership with Hin Sang to open 100 health soup chain stores and co-develop premium herbal-green ingredient gift sets, and Cremer Sustainable Foods and Lim Kee’s April 2024 launches of plant-based RTE items like chilli crab pau, black pepper chicken, and laksa in Singapore.

Beverages remain the largest segment, with fruit concentrates, NFC juices, and vegetable extracts used in soft drinks, functional beverages, dairy products, and plant-based milks. Soups and sauces rely on tomato paste, carrot puree, and beetroot concentrate for color, viscosity, and umami. Meanwhile, dairy products incorporate fruit purees and vegetable fibers to enhance texture and support clean-label claims, such as in yogurt, ice cream, and cheese analogs. Confectionery and bakery use fruit pieces, pastes, and powders for fillings and toppings, with berries and tropical fruits driving premium innovation. Distribution channels increasingly shape application trends: e-commerce and modern trade favor convenient, transparent RTE formats, whereas traditional trade emphasizes beverages and confectionery with longer shelf life and lower price points.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

China dominated the Asia-Pacific fruit and vegetable ingredient market in 2024, accounting for 53.62% of regional revenue, supported by vertically integrated processing clusters in Shandong and Shaanxi that supplied apple concentrate, tomato paste, and vegetable powders for both domestic and export markets. Scale advantages, such as Haisheng Juice’s large apple concentrate facility, and government-backed export zones under the RCEP, underpin this dominance. Strategic investments highlight the importance of local production. Samyang Foods’ December 2024 KRW 64.7 billion (USD 45.18 million) China plant will serve Southeast Asia and Malaysia to address projected domestic shortfalls. Meanwhile, Thai Wah’s April 2025 joint venture with Fuji Nihon in Thailand leverages ASEAN trade benefits and Japanese starch expertise. China’s updated 2024 cold-chain logistics plan further strengthens temperature-controlled warehousing and last-mile delivery, enabling processors to source from remote regions like Xinjiang, Gansu, and Yunnan.

India is expected to grow at the fastest rate, with a 9.79% CAGR from 2025 to 2030, driven by the Ministry of Food Processing Industries’ Production Linked Incentive scheme and cold-chain subsidies under the Pradhan Mantri Kisan Sampada Yojana. Key expansions include Jain Irrigation Systems’ mango puree and concentrate capacity, OB Holdings’ RM 30.5 million (USD 7 million) Serendah factory in Malaysia for fortified foods (production starting H1 2026), and Yenher Holdings’ September 2024 joint venture with Denmark’s Fermentationexperts to produce 25,000 t/year of plant proteins via fermentation for Vietnam, Indonesia, the Philippines, and Taiwan starting Q4 2025.

High-value markets like Japan, South Korea, and Australia emphasize clean-label, traceability, and functional benefits, supporting premium pricing. Kagome’s January 2024 acquisition of a 70% stake in California’s Ingomar Packing strengthens tomato processing for Japan, while Samyang’s September 2024 allulose plant in Ulsan (13,000 t/year) targets Japan, Southeast Asia, and Australia/New Zealand amid growing demand for low-calorie sweeteners. Kinoko-Tech’s October 2024 partnership with Metaphor Foods to produce fungi-based products in Australia, expanding into Malaysia, Singapore, Indonesia, and New Zealand from 2025, illustrates the region’s role as an innovation hub. Rapid urbanization, rising disposable incomes, and modern trade growth across Thailand, Indonesia, Singapore, and the broader APAC region continue to drive demand for fruit and vegetable ingredients in beverages, RTE meals, and functional foods, supported by Corbion’s July 2024 expanded distribution in Thailand and Kalsec’s June 2024 Singapore finishing and distribution center.

Competitive Landscape

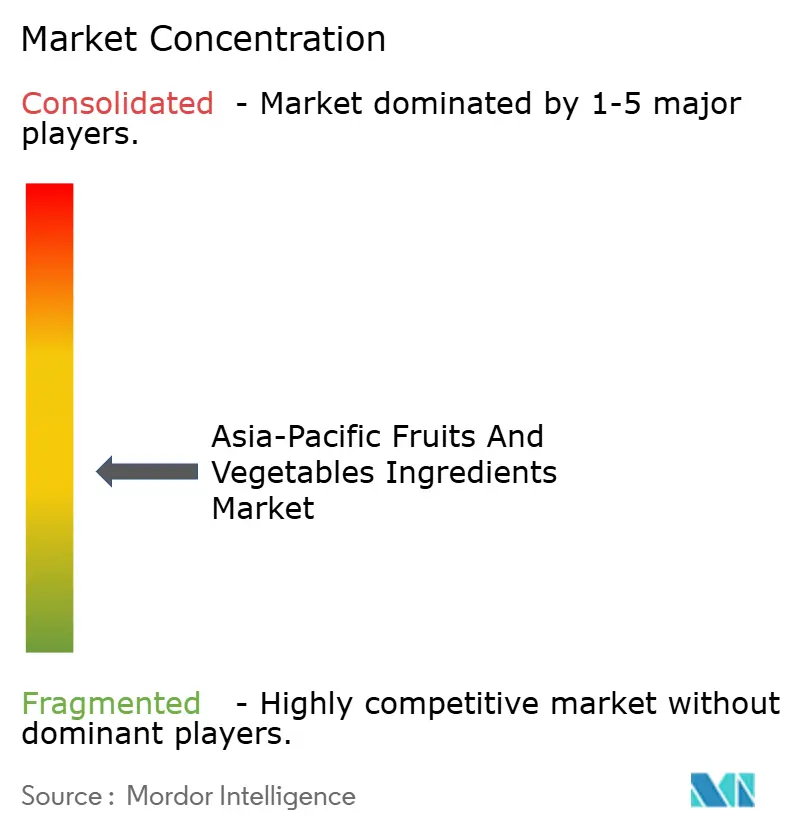

The Asia-Pacific fruit and vegetable ingredients market is moderately fragmented, with supplier networks offering opportunities for regional specialists to capture niche segments through proximity to raw material sources and customized formulations. Major players, Archer Daniels Midland, Cargill, Döhler, AGRANA, and Kerry Group, drive pricing and innovation but with differing strategies: ADM focuses on backward integration into oilseeds and grains, Cargill cross-sells fruit-based sugar replacers via its global sweetener portfolio, Döhler provides turnkey flavor and color systems for beverage and dairy clients, AGRANA specializes in fruit preparations for yogurt and ice cream, and Kerry leverages its taste-and-nutrition platform for plant-based and functional foods. Smaller vertically integrated processors like Haisheng Juice in China, Jain Irrigation in India, and Kagome in Japan reduce supply-chain risk and respond quickly to customer needs.

Givaudan’s October 2024 groundbreaking of a CHF 50 million Indonesia facility, operational by H1 2026, with solar power, recycled water, and rainwater harvesting, highlights the capital intensity required to compete at scale and meet ESG requirements[4]Source: Givaudan, “Indonesia Facility Ground-Breaking,” givaudan.com. White-space opportunities lie in upcycled ingredients, precision fermentation, and culturally resonant, locally sourced flavors. Ingredion’s September 2024 launch of citrus fiber from upcycled peel illustrates cost-effective, clean-label alternatives to synthetic hydrocolloids, while Nourish Ingredients’ November 2024 partnership with Cabio Biotech to produce Tastilux, a precision-fermentation fat from Mortierella alpina, shows how biotechnology can deliver meaty aroma at sub-1% inclusion rates.

Disruptors such as Kinoko-Tech’s fungi-mycelium platform produce protein-rich, zero-waste ingredients with lower carbon footprints, and dsm-firmenich’s September 2024 FutureBites Food Design Studio in Singapore accelerates plant-based innovation in collaboration with NUS and A*STAR. Technology adoption varies across the region: multinationals deploy automation, AI-driven quality control, and blockchain traceability, while mid-tier processors in India, Thailand, and Vietnam rely on semi-automated lines and manual sorting. This performance gap is expected to widen unless government Production-Linked Incentive schemes and joint ventures accelerate technology transfer, shaping the competitive landscape for APAC fruit and vegetable ingredient suppliers.

Asia-Pacific Fruits And Vegetables Ingredients Industry Leaders

-

Archer Daniels Midland Company

-

AGRANA Beteiligungs-AG

-

Döhler GmbH

-

Kerry Group plc

-

Cargill, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Thai Wah Public Company and Fuji Nihon Corporation finalized the formation of Thai Wah Fuji Nihon Company Limited, a joint venture with Thai Wah holding 51% and Fuji Nihon Thailand 49%, to develop high-quality tapioca starch products with novel functionalities and expand global footprint across APAC, reinforcing supply-chain resilience and driving innovation in agri-food ingredients.

- December 2024: Samyang Foods announced a KRW 64.7 billion (USD 45.18 million) investment to establish a Singapore holding company and a China production plant, with final investment planned by December 31, 2025, to localize production and resolve future supply shortages as exports reached 77% of sales through Q3 2024, serving the United States, Japan, China, Indonesia, and Southeast Asia.

- November 2024: Nourish Ingredients and China's Cabio Biotech have signed a joint commercial agreement to manufacture and distribute Tastilux, a precision-fermentation plant-based fat, across the Asia-Pacific. Cabio will lead manufacturing, while China will handle distribution, with Nourish handling global sales. Sales are expected to begin in 2025, targeting China's plant-based meat sector.

- October 2024: Givaudan Taste & Wellbeing broke ground on a CHF 50 million (approximately USD 56 million) production facility in Cikarang, Indonesia, with a 24,000-square-meter footprint and capacity for savoury, sweet, snack powders, and infant nutrition solutions; completion is expected within 18 months, with operations beginning in H1 2026 and approximately 60 jobs created.

Asia-Pacific Fruits And Vegetables Ingredients Market Report Scope

The Asia-Pacific fruit and vegetable ingredient market is segmented by ingredient type, application, product type, and geography. By ingredient type, the market is segmented into fruits and vegetables. By application, the market is segmented into beverages, confectionery products, RTE products, bakery products, soups and sauces, and dairy products. By product type, the market is segmented into concentrates, pastes and purees, NFC juices, and pieces and powders. The report also provides a country-wise analysis of the region.

By Ingredient Type

| Fruits | Apple |

| Orange | |

| Pineapple | |

| Mango | |

| Banana | |

| Kiwi | |

| Berries | |

| Other Fruits | |

| Vegetables | Carrots |

| Beetroots | |

| Tomato | |

| Butternuts | |

| Pumpkins | |

| Other Vegetables |

By Form

| Concentrates |

| Pastes and Purees |

| Pieces and Slices |

| Powders |

| NFC Juices |

| Others |

By Application

| Beverages |

| Confectionary Products |

| Bakery Products |

| Soups and Sauces |

| Dairy Products |

| RTE Products |

| Others |

By Geography

| China |

| India |

| Japan |

| Australia |

| South Korea |

| Indonesia |

| Thailand |

| Singapore |

| Rest of Asia-Pacific |

| By Ingredient Type | Fruits | Apple |

| Orange | ||

| Pineapple | ||

| Mango | ||

| Banana | ||

| Kiwi | ||

| Berries | ||

| Other Fruits | ||

| Vegetables | Carrots | |

| Beetroots | ||

| Tomato | ||

| Butternuts | ||

| Pumpkins | ||

| Other Vegetables | ||

| By Form | Concentrates | |

| Pastes and Purees | ||

| Pieces and Slices | ||

| Powders | ||

| NFC Juices | ||

| Others | ||

| By Application | Beverages | |

| Confectionary Products | ||

| Bakery Products | ||

| Soups and Sauces | ||

| Dairy Products | ||

| RTE Products | ||

| Others | ||

| By Geography | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Asia-Pacific fruits and vegetables ingredients market in 2025?

It stands at USD 64.54 million and is on track for USD 95.84 million by 2030 at an 8.23% CAGR.

Which ingredient type is growing fastest?

Vegetable ingredients are rising at 9.28% as plant-based meat and dairy makers demand natural colors and fibers.

Why are NFC juices gaining popularity?

Cold-pressed positioning, government cold-chain subsidies, and willingness to pay for freshness are propelling NFC juices at a 10.35% CAGR.

Which country offers the strongest growth outlook?

India leads with a 9.79% CAGR, supported by Production Linked Incentives and expanded cold-chain infrastructure.

What is a key restraint for new entrants?

High upfront costs for aseptic and freeze-drying lines, often exceeding USD 10 million, limit entry for mid-sized processors.

Page last updated on: