Asia-Pacific Fitness Rings Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

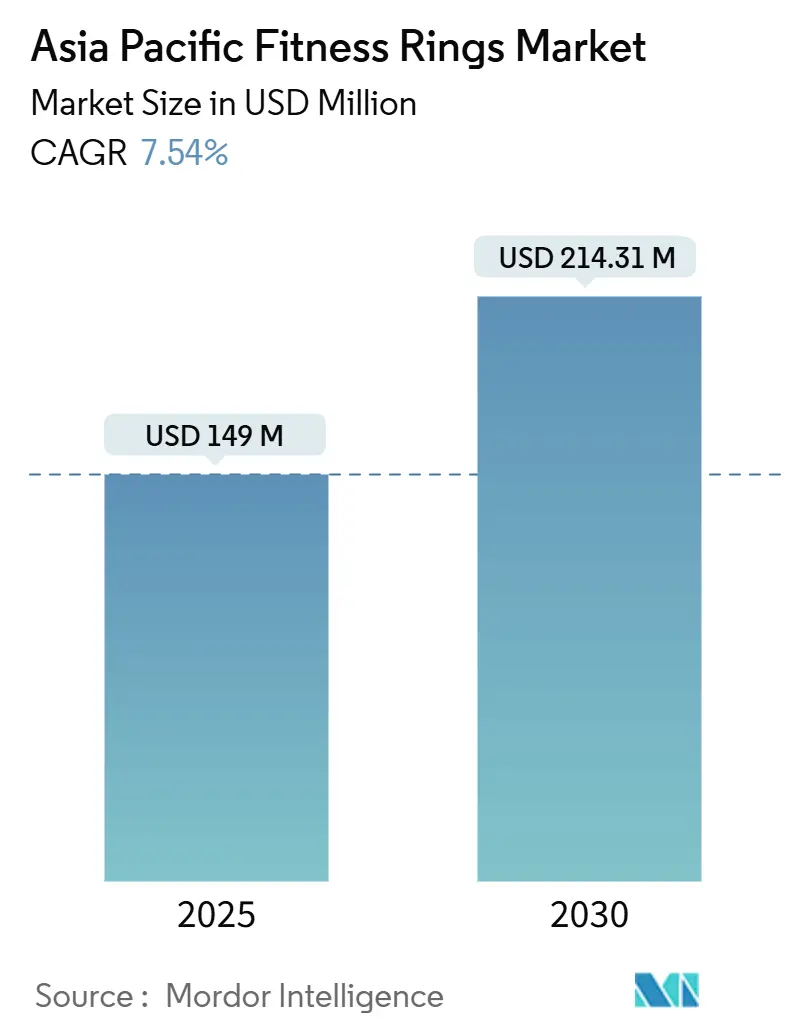

| Market Size (2025) | USD 149 Million |

| Market Size (2030) | USD 214.31 Million |

| Growth Rate (2025 - 2030) | 7.54% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Fitness Rings Market Analysis by Mordor Intelligence

The Asia-Pacific fitness rings market size stands at USD 149 million in 2025 and will reach USD 214.31 million by 2030, reflecting a 7.54% CAGR. Demand is shifting from conspicuous wrist-worn wearables to discreet finger-based sensors that deliver clinical-grade heart-rate variability, SpO₂, skin temperature, and soon glucose readings with higher accuracy than watches. Samsung’s October 2024 launch in Australia and April 2025 launch in New Zealand confirmed that technology majors see rings as core health platforms rather than niche accessories. Medical-device firms are validating this trajectory; Dexcom’s USD 75 million investment in Oura Health is poised to merge continuous glucose monitoring with sleep and recovery dashboards, expanding the fitness ring market into metabolic health management. Parallel gains in regional e-commerce logistics, buy-now-pay-later adoption, and mobile-wallet penetration reduce purchase friction. However, tariff regimes in India and Indonesia, data localization mandates in China and Singapore, and heat management limits within 7 mm shells temper near-term growth.

Key Report Takeaways

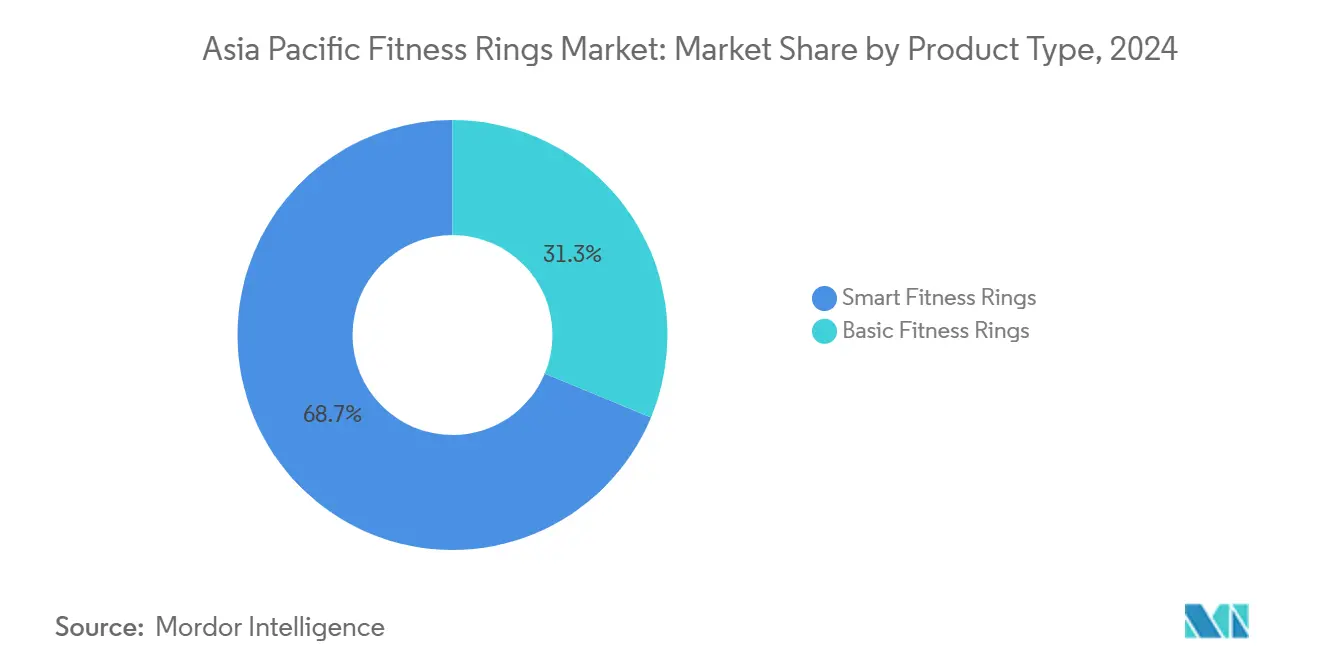

- By product type, smart variants held 68.73% of the Asia-Pacific fitness rings market share in 2024 and are forecast to advance at a 9.02% CAGR through 2030.

- By parameter monitored, activity and calories tracking captured 34.73% share of the Asia-Pacific fitness rings market size in 2024, while continuous glucose monitoring is projected to grow at 8.22% CAGR to 2030.

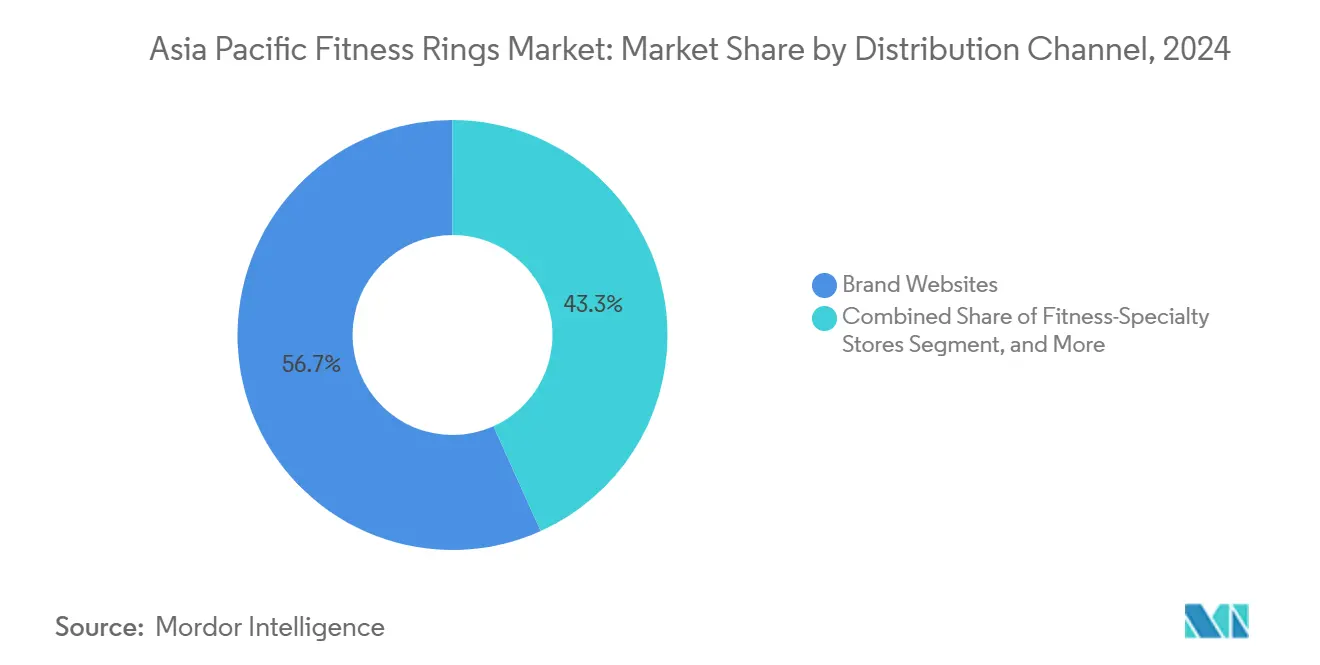

- By distribution channel, brand websites accounted for 56.73% of the revenue in the Asia-Pacific fitness rings market in 2024; e-commerce marketplaces are projected to expand at a 8.67% CAGR by 2030.

- By price band, mid-range devices accounted for 48.92% of the 2024 Asia-Pacific fitness rings market size, whereas premium rings above USD 250 are expected to grow at a 8.55% CAGR through 2030.

- By country, China accounted for 40.16% of the 2024 Asia-Pacific fitness rings market size and is expected to grow at an 8.69% CAGR through 2030.

Asia-Pacific Fitness Rings Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging smartphone-linked health consciousness | +1.2% | Global, with peaks in China, India, South Korea | Medium term (2-4 years) |

| Integration of advanced biometric sensors | +1.5% | Japan, South Korea, Singapore, Australia | Medium term (2-4 years) |

| Boom in corporate wellness and insurance partnerships | +0.9% | Singapore, Malaysia, Japan, Australia | Long term (≥ 4 years) |

| Rapid expansion of Asia-Pacific e-commerce logistics | +1.3% | China, India, Indonesia, Vietnam, Thailand | Short term (≤ 2 years) |

| Emergence of ring-based continuous glucose monitoring | +1.8% | Global, early adoption in Australia, Singapore, Japan | Long term (≥ 4 years) |

| Rise of digital gifting culture in South-East Asia weddings | +0.4% | Indonesia, Malaysia, Thailand, Philippines | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Smartphone-Linked Health Consciousness

More than 1.2 billion residents in the Asia-Pacific used smartphones in 2024, and health apps have become embedded utilities rather than experimental add-ons. Samsung’s Galaxy Ring relies on Android 11 and above, cementing users within Samsung Health’s ecosystem and extending lifetime value.[1]Samsung Electronics New Zealand, “Samsung Galaxy Ring Coming to New Zealand: Experience Simplified Wellness at Your Fingertips,” SAMSUNG.COM Oura’s GBP 5.99 monthly subscription for AI insights demonstrates that many consumers are willing to pay recurring fees when the analytics are tangible and relevant.[2]Anglia Ruskin University, “Smart Rings v Smart Watches – How Do They Compare?” ARU.AC.UK Indian buyers, however, often reject subscriptions; boAt’s one-time hardware model at Rs 8,999 (USD 108) quickly gained traction by matching local price expectations. Gen Z shoppers rely heavily on social commerce, which demands influencer-ready product positioning and omnichannel availability.

Integration of Advanced Biometric Sensors

Finger placement near the radial arteries yields cleaner photoplethysmography signals than wrist placement, enabling the capture of accurate SpO₂ and heart-rate variability that meets clinical thresholds. South Korea’s Sky Labs CART-I earned FDA Breakthrough Device status for continuous blood pressure and ECG functions, proving the ring’s medical potential. Oura and Dexcom are on track to overlay CGM data on top of sleep and activity metrics, addressing the Asia-Pacific’s 537 million adults with diabetes. Sony’s 2024 patent for gesture-control rings suggests future convergence with augmented-reality interfaces.[3]IT Professionals NZ, “What We Know So Far About the Rumoured Apple Smart Ring,” ITP.NZ

Boom in Corporate Wellness and Insurance Partnerships

Insurers across Singapore and Malaysia now experiment with wearable-driven underwriting models that reward sustained activity and quality sleep. Cigna’s tie-up with PAI Health and Alexandra Hospital’s 1,700-person Fitbit trial show a willingness to subsidize devices that curtail claims costs. Employers view rings as less intrusive than watches, as users typically wear them overnight, allowing for continuous biometric capture.

Rapid Expansion of Asia-Pacific E-Commerce Logistics

Asia-Pacific e-commerce reached USD 3.5 trillion GMV in 2023 and is scaling fast on mobile-wallet rails. Same-day fulfillment in tier-1 cities and buy-now-pay-later penetration above 40% in China, Japan, and Indonesia reduces the psychological hurdle of paying USD 300-plus for a ring. Direct-to-consumer brands benefit from lower acquisition costs, provided they localize checkout flows.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Device miniaturization raising thermal-management issues | -0.8% | Global, acute in tropical climates (Southeast Asia) | Short term (≤ 2 years) |

| Data-privacy compliance costs under evolving Asia-Pacific laws | -0.6% | China, Singapore, South Korea, India | Medium term (2-4 years) |

| Customs duties on Bluetooth-enabled wearables in India and Indonesia | -0.5% | India, Indonesia | Short term (≤ 2 years) |

| Limited battery cycles due to ultrathin form-factor | -0.7% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Device Miniaturization Raising Thermal-Management Issues

Sensors and radios crammed into 7 mm titanium shells generate heat that must stay below 41 °C to avoid discomfort. Samsung caps heart-rate sampling during daytime to conserve power and reduce heat. It is expected that lithium-polymer cells will degrade faster when core temperatures exceed 45 °C, thereby shortening ring lifespans. Firmware-level sensor duty cycling, as adopted by RingConn’s 12-day battery Gen 2 device, mitigates heat but limits continuous monitoring.

Data-Privacy Compliance Costs Under Evolving Asia-Pacific Laws

China’s Personal Information Protection Law forces any vendor with more than 1 million users to localize servers and submit annual audits, adding USD 1-3 million in compliance overhead. Singapore’s Personal Data Protection Act and the upcoming South Korean AI Act require granular consent and algorithm explainability, which increases onboarding friction but rewards brands that build trust early.

Segment Analysis

By Product Type: Smart Variants Capture Premium Buyers

Smart models represented 68.73% of 2024 revenue and will post a 9.02% CAGR, underscoring consumer preference for AI-enabled insights. This dominance cements smart devices as the anchor of the fitness rings market. Samsung’s Galaxy Ring, priced at AUD 699, layers sleep, HRV, and temperature data into a single Energy Score that encourages daily use. Oura’s subscription model targets long-term health enthusiasts who value longitudinal analytics.

Basic rings remain relevant in economies where ASPs hover near USD 120. boAt’s no-fee model and Noise’s mid-priced Luna Ring capitalize on one-time payment preferences. Cross-selling tactics, such as Amazfit bundling its Helio Ring with smartwatches, broaden reach while consolidating ecosystems. Regional specialists, such as Ultrahuman, demonstrate how localized service and fast warranty turnaround can outperform global brands on their own turf.

By Parameter Monitored: CGM Integration Redefines Use Cases

Activity and calories tracking accounted for 34.73% of 2024 demand, reflecting baseline expectations among buyers. Yet, continuous glucose monitoring is expected to accelerate at an 8.22% CAGR, repositioning the broader fitness rings market from fitness tracking toward metabolic health. Oura-Dexcom fusion will let users correlate nocturnal glucose dips with sleep interruptions.

Sleep and recovery metrics remain core, as rings are comfortable overnight. Heart, SpO₂, and stress sensing appeal to users managing cardiovascular conditions. Sky Labs’ FDA-recognized blood-pressure ring signals a pipeline of prescription-grade parameters set to enter consumer channels, further expanding the clinical relevance of the fitness rings industry.

By Distribution Channel: Marketplaces Gain on Brand Sites

Brand websites accounted for 56.73% of sales in 2024, thereby protecting margins and owning customer data. Samsung’s sizing-kit workflow illustrates how direct channels manage fit-sensitive SKUs. Marketplaces, however, are expected to outpace the growth rate at 8.67% CAGR, due to Lazada and JD.com’s one-day delivery promises, which broaden the fitness rings market’s reach.

Offline touchpoints still matter. RingConn’s Yiwu showroom enables bulk buyers to verify build quality, while Samsung Experience Stores in Bangkok and Singapore create a premium brand theater. Successful vendors blend direct channels for data ownership with marketplaces for discovery.

Note: Segment shares of all individual segments available upon report purchase

By Price Range: Premium Tier Accelerates on CGM Demand

Mid-range rings, priced between USD 100 and USD 250, generated 48.92% of the 2024 fitness ring market size, aligning with disposable-income bands in India and Indonesia. Premium devices above USD 250, led by Samsung, Oura, and Sky Labs, are expected to log an 8.55% CAGR, driven by titanium builds, glucose integration, and subscription-based AI.

Economy devices under USD 100 attract first-time buyers but face wafer-thin margins. Sustainability credentials offset price gaps; consumers in Indonesia and the Philippines pay premiums for recyclable casings, allowing brands to justify higher ASPs without sacrificing volume.

Geography Analysis

China controls the largest slice of the regional fitness rings market, forecast at CNY 660 million (USD 96 million) in 2025 and CNY 1.6 billion (USD 233 million) by 2031. RingConn’s Yiwu flagship demonstrates how domestic brands utilize wholesale hubs to scale without incurring heavy advertising expenses. Mandatory data localization raises barriers for foreign entrants, but integration with Alipay and WeChat Pay is essential, given their 90% wallet share.

Japan and South Korea form a high-value corridor where aging populations and insurance subsidies drive adoption. Oura’s launch in Japan positions the ring as a quasi-medical device, while Samsung capitalizes on its dominant smartphone share at home. South Korean innovator Sky Labs illustrates the country’s edge in medical-grade wearables.

India offers steep growth potential, shipping 72,000 units in Q2 2024 with a USD 205 ASP. Tariffs incentivize domestic assembly; Ultrahuman’s 48.4% share underscores first-mover advantage. Unified Payments Interface’s ascendancy to 42% of e-commerce transactions simplifies direct checkout integration and boosts conversion. Australia and New Zealand validate willingness to pay premium pricing, with Samsung’s Galaxy Ring debuting at AUD 699 and NZD 699 respectively. Corporate wellness pilots across Singapore and Malaysia hint at enterprise channels where insurers offset device costs for long-term claim reduction.

Emerging markets in Indonesia, Vietnam, and the Philippines combine 70% smartphone penetration with sub-15% wearable adoption, suggesting runway once local payment rails and installment plans mature. Import duties in Indonesia echo India’s, nudging brands toward regional assembly partnerships.

Competitive Landscape

The Asia-Pacific fitness rings market remains fragmented, with no vendor exceeding a 20% regional share; however, consolidation is underway. Ultrahuman controls nearly half of India through aggressive localization, warranty support, and domestic production. Samsung pursues sequential country launches to align with regulatory approvals and retailer partnerships, preserving margin.

Oura’s USD 75 million tie-up with Dexcom elevates rings into the regulated medical territory, setting a high bar for data accuracy and compliance. Sony’s gesture-control patent signals broader use cases beyond health, potentially linking rings to XR headsets and smart-home ecosystems.

Disruptors such as RingConn emphasize 12-day battery life and sleep-apnea detection, while Sky Labs focuses on hypertension care. Competitive advantage now rests on AI insights derived from longitudinal datasets, favoring firms that combine hardware with cloud analytics rather than relying on one-off device sales.

Asia-Pacific Fitness Rings Industry Leaders

Oura Health Oy

Ringly Inc.

Sky Labs Inc.

Jakcom Technology Co., Ltd.

Google LLC (Fitbit Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: RingConn opens its inaugural brick-and-mortar flagship in Yiwu, China, giving bulk buyers a physical venue to test the Gen 2 ring with 12-day battery life and sleep-apnea detection before placing wholesale orders.

- June 2025: Oura Health and Dexcom complete the first over-the-air update that syncs real-time Stelo continuous-glucose readings with Oura Ring Gen 3 sleep and readiness dashboards across Australia, Singapore, and Japan.

- April 2025: Galaxy Ring officially ships to New Zealand customers on April 2, marking the device’s first retail availability in Oceania outside Australia.

- March 2025: Samsung Electronics New Zealand confirmed that Galaxy Ring pre-orders open on March 11 at NZD 699 (USD 425), bundling an 11-size fitting kit and full Samsung Health integration.

Asia-Pacific Fitness Rings Market Report Scope

The Asia-Pacific fitness rings market report is segmented by Product Type (Basic Fitness Rings, Smart Fitness Rings), Parameter Monitored (Activity and Calories, Sleep and Recovery, Heart and SpO₂, Stress and HRV, Body Temperature), Distribution Channel (Brand Websites, E-commerce Marketplaces, Consumer-Electronics Stores, Fitness-Specialty Stores), Price Range (Economy Below USD 100, Mid-range USD 100–250, Premium Above USD 250), and Country (China, Japan, South Korea, India, Australia, New Zealand, Singapore, Indonesia, Malaysia, Thailand, Vietnam, Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD Million).

| Basic Fitness Rings |

| Smart Fitness Rings |

| Activity and Calories |

| Sleep and Recovery |

| Heart and SpO₂ |

| Stress and HRV |

| Body Temperature |

| Brand Websites |

| E-commerce Marketplaces |

| Consumer-Electronics Stores |

| Fitness-Specialty Stores |

| Economy ( Below USD 100) |

| Mid-range (USD 100–250) |

| Premium ( Above USD 250) |

| China |

| Japan |

| South Korea |

| India |

| Australia |

| New Zealand |

| Singapore |

| Indonesia |

| Malaysia |

| Thailand |

| Vietnam |

| Rest of Asia-Pacific |

| By Product Type | Basic Fitness Rings |

| Smart Fitness Rings | |

| By Parameter Monitored | Activity and Calories |

| Sleep and Recovery | |

| Heart and SpO₂ | |

| Stress and HRV | |

| Body Temperature | |

| By Distribution Channel | Brand Websites |

| E-commerce Marketplaces | |

| Consumer-Electronics Stores | |

| Fitness-Specialty Stores | |

| By Price Range | Economy ( Below USD 100) |

| Mid-range (USD 100–250) | |

| Premium ( Above USD 250) | |

| By Country | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| New Zealand | |

| Singapore | |

| Indonesia | |

| Malaysia | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How big is the Asia Pacific fitness rings market in 2025?

The fitness rings market size is USD 149 million in 2025.

Which segment holds the largest revenue share?

Smart variants lead with 68.73% of 2024 revenue.

What growth rate is expected for premium-priced rings?

Premium devices above USD 250 are forecast to grow at an 8.55% CAGR through 2030.

Which parameter is the fastest growing in upcoming models?

Continuous glucose monitoring is projected to expand at an 8.22% CAGR.

How do tariffs affect international brands in India?

India’s 10-20% customs duties push foreign brands to consider local assembly to remain price-competitive.