Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 1.01 Trillion |

| Market Size (2030) | USD 1.39 Trillion |

| Growth Rate (2025 - 2030) | 6.58% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Fashion Accessories Market Analysis by Mordor Intelligence

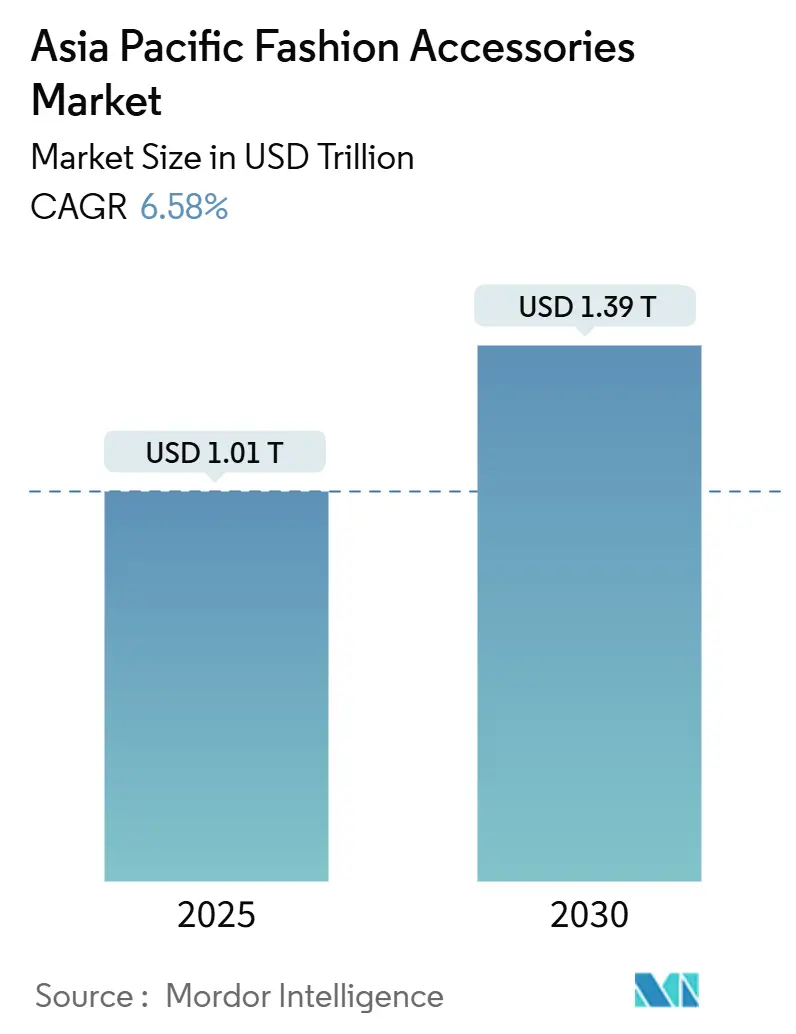

The Asia-Pacific fashion accessories market size stands at USD 1.01 trillion in 2025 and is projected to climb to USD 1.39 trillion by 2030, reflecting a 6.58% CAGR over the forecast period. Rising income levels, urbanization, and smartphone usage are making branded accessories more accessible in urban and semi-urban areas. Premiumization is growing as wealthier consumers prefer high-end brands, while the mass-market segment dominates in volume by catering to cost-conscious buyers. E-commerce platforms, supported by mobile payments and social-commerce features, are expediting purchases and boosting international transactions. Companies are attracting environmentally conscious consumers, especially in developed Asia-Pacific metros, through supply-chain transparency and circular-economy practices. The market is highly competitive, with global players like Nike, Adidas, and PUMA competing against regional brands. Companies are tailoring products to local preferences, as seen with Nike’s R&D center in Shenzhen.

Key Report Takeaways

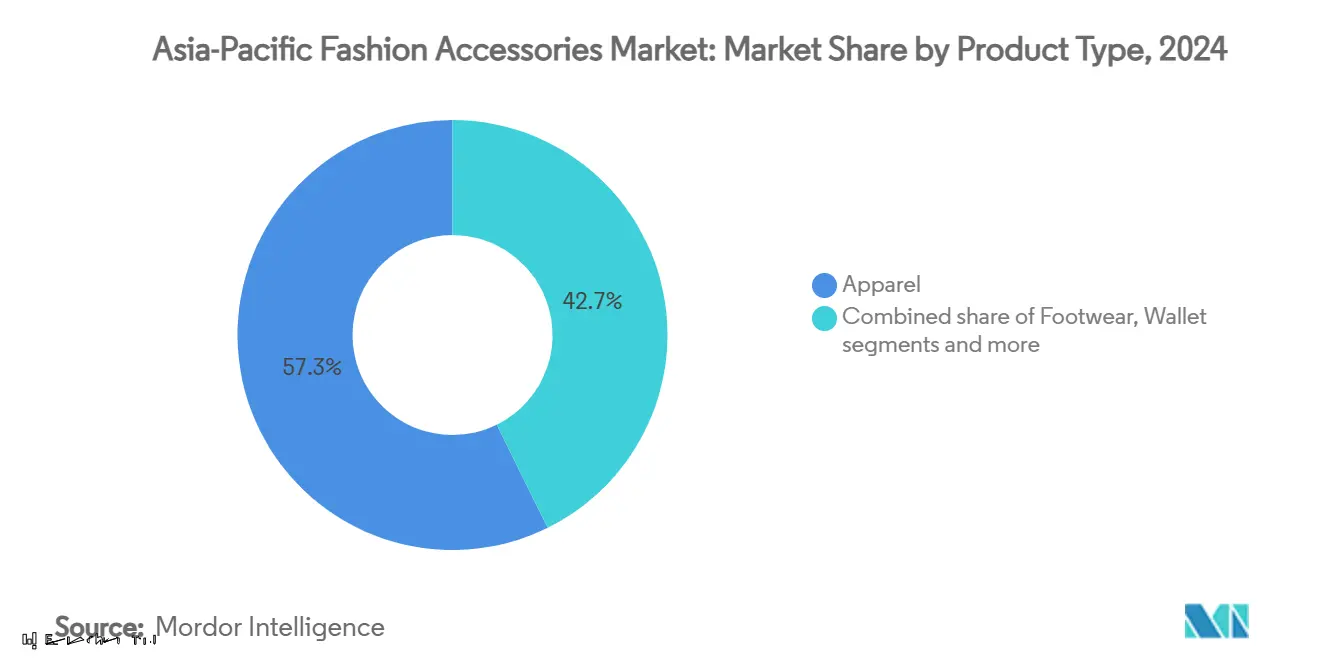

- By product type, apparel accessories commanded 57.35% of the Asia-Pacific fashion accessories market share in 2024, while watches are forecast to post the fastest 6.98% CAGR through 2030.

- By end user, women-led purchases with a 54.35% share in 2024; the kids segment is advancing at a 7.24% CAGR to 2030.

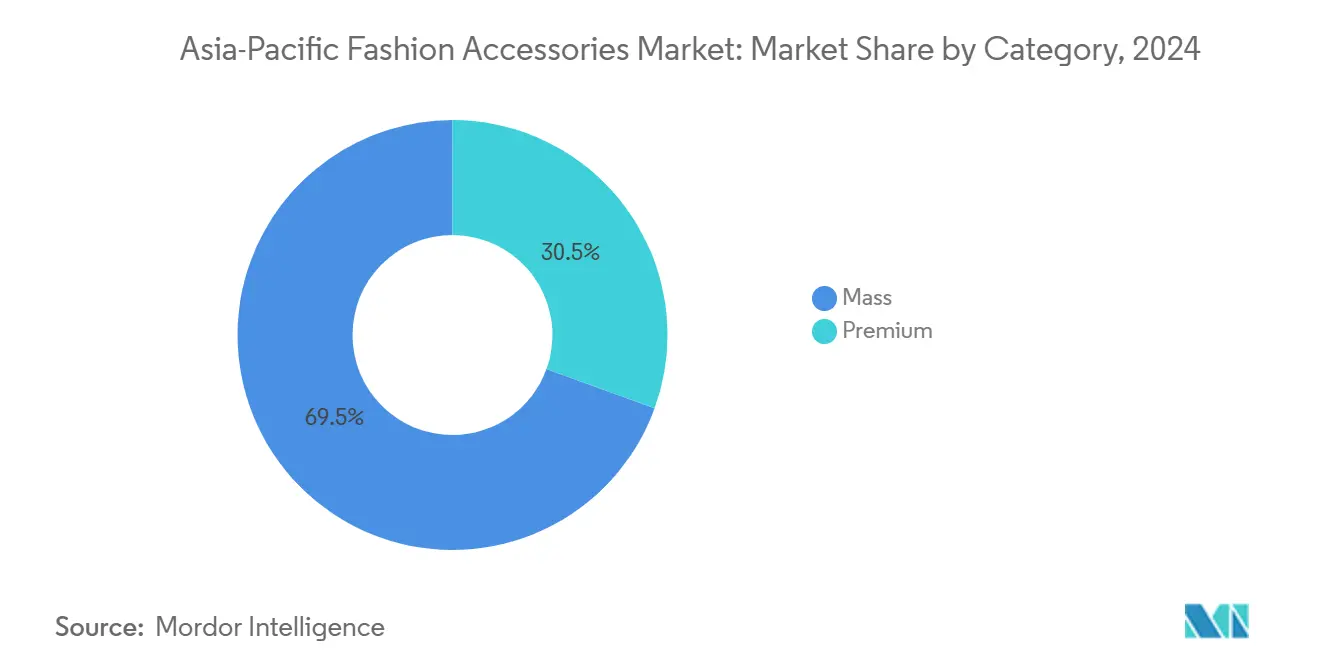

- By category, mass-market goods held 69.46% of the Asia-Pacific fashion accessories market size in 2024; premium lines are set to grow at 7.65% CAGR during 2025-2030.

- By distribution channel, offline stores retained a 64.77% share in 2024, whereas online channels are expanding at an 8.12% CAGR to 2030.

- By geography, China contributed 39.58% revenue in 2024, whereas Thailand is projected to rise at an 8.55% CAGR through 2030.

Asia-Pacific Fashion Accessories Market Trends and Insights

Drivers Impact Table

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Technological advancements in terms of design and raw material | +1.2% | concentration in China, Japan, South Korea | Medium term (2-4 years) |

| Strong demand from inbound tourists | +0.8% | China, Japan, Thailand, Singapore | Short term (≤ 2 years) |

| Growing preference for luxury and branded fashion accessories | +1.5% | China, India, Australia, Singapore | Long term (≥ 4 years) |

| Changing consumer behavior toward fitness and athleisure | +1.1% | early adoption in Australia, South Korea | Medium term (2-4 years) |

| Sustainability and ethical sourcing awareness | +0.7% | Australia, Japan, South Korea, urban China | Long term (≥ 4 years) |

| Influence of social media and celebrity endorsements | +0.9% | China, India, Thailand, Indonesia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Strong demand from inbound tourists

The Asia-Pacific fashion accessories market is growing rapidly, driven by a strong recovery in tourism. The Pacific Asia Travel Association estimates international visitor arrivals to the region will reach 813.7 million by 2027, up from 648.1 million in 2024 [1]Source: International Visitors Arrival in Asia-Pacific, "PATA Forecasts Strong Asia Pacific Visitor Rebound and Growth Through 2027," pata.org. Similarly, the Japan National Tourism Organization (JNTO) and Japan Tourism Agency (JTA) report that 36.9 million foreign tourists visited Japan in 2024 [2]Source: Foreign Tourists Arrival in Japan, " Tourism in Japan: A look at the Numbers from 2024 and the Outlook for 2025," jittiusa.org. Luxury brands and boutiques are offering exclusive collections and collaborating with local artisans to attract tourists seeking unique, culturally inspired items. Retailers are also using dynamic pricing strategies to address currency fluctuations, such as the weaker yen, ensuring competitiveness and profitability. These trends highlight tourism's direct influence on product offerings and retail strategies in key shopping destinations across the Asia-Pacific.

Changing consumer behavior toward fitness and athleisure

The growing focus on fitness and active lifestyles is reshaping the Asia-Pacific fashion accessories market. More people are choosing products like gym-friendly bags, smartwatches, and multi-purpose accessories as part of their daily routines. For example, backpacks with special compartments for gym shoes and water bottles are becoming popular among professionals who juggle work and exercise. Smartwatches are another favorite, as they help track fitness activities like steps, heart rate, and calories burned, while also offering a stylish look. Brands are also using advanced materials, such as moisture-wicking and quick-dry fabrics, to meet consumer needs. For instance, breathable sneakers are now used not only for workouts but also for casual outings, making them a versatile choice. In March 2025, ASICS India released the GEL-K1011, a retro-inspired sneaker combining GEL-KAYANO aesthetics with modern breathable mesh and FF BLAST cushioning, making it suitable for both running and streetwear. Similarly, gym bags with modern, sleek designs are being used as office bags, appealing to consumers who value both style and practicality.

Growing preference for luxury and branded fashion accessories

In the Asia-Pacific region, rising demand for luxury and branded accessories is driven by a growing middle class and increasing purchasing power. The IMF projects the region's PPP-adjusted GDP per capita to reach USD 96.43 thousand by 2025, highlighting strong consumer spending potential [3]Source: Purchasing Power Parity, " GDP, current prices, Purchasing power parity; billions of international dollars, " imf.org. This economic growth enables more consumers to invest in premium products valued for craftsmanship and cultural relevance. Global brands are localizing offerings, such as Tod’s collaboration with Indian designer Rahul Mishra in September 2024 and LVMH’s "Crafted World" exhibit at the 2025 Osaka Expo, which featured collaborations with Japanese artisans, showcasing traditional craftsmanship while appealing to local consumers. Regional brands like Singapore-based Aupen are also merging local identity with global luxury appeal. These strategies reflect how brands align with regional tastes and economic momentum to thrive in Asia–Pacific’s evolving luxury market.

Technological advancements in terms of design and raw material

Technological advancements in design and raw materials are transforming the Asia-Pacific fashion accessories market. Nike, for example, launched its Shenzhen Technology Hub and Sport Research Lab in 2024, focusing on eco-friendly materials like recyclable fibers and plant-based alternatives. These innovations cater to Chinese consumers, accelerate product development, and reduce waste. Similarly, TAL Apparel in Hong Kong introduced its first Regenagri-certified garment, made from regenerative cotton, renewable energy, and designed to cut greenhouse gas emissions, showcasing its commitment to sustainability. On the retail side, smart technologies like item-level RFID tags are gaining traction. These tags improve product tracking, prevent counterfeits, and enable authenticated resale, helping brands build trust, support premium pricing, and meet stricter regulations while enhancing supply chain transparency.

Restraints Impact Analysis

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Proliferation of counterfeit products | -1.8% | China, Southeast Asia, India | Short term (≤ 2 years) |

| Supply chain disruptions | -1.2% | concentration in Vietnam, China, Bangladesh | Medium term (2-4 years) |

| Fluctuating raw material prices | -0.9% | affecting textile-dependent countries like China, India | Short term (≤ 2 years) |

| Rising trade barriers and tariffs | -1.4% | Vietnam, China, Indonesia, Thailand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of counterfeit products

Counterfeit fashion accessories are a growing challenge in the Asia-Pacific market, damaging brand reputations and diverting revenue. In 2025, authorities in the Philippines seized fake Crocs worth PHP 152 million, highlighting the region's rampant counterfeit trade. The National Committee on Intellectual Property Rights reported PHP 40.99 billion worth of counterfeit goods seized in February 2025, a 52% increase from the previous year [4]Source: Counterfeit Products Seized, "NCIPR seizes record P40.99 billion counterfeit goods in 2024," ipophil.gov.ph. Counterfeit designer items are often seen as affordable alternatives in Southeast Asia, complicating consumer education efforts. Regulatory bodies in countries like Vietnam are tightening customs checks, driven by international trade agreements, raising exporters' costs. For example, in June 2025, a clothing store in Pitampura, northwest Delhi, was raided, and over 200 counterfeit items, including shorts and t-shirts, were seized. Global brands are adopting measures like blockchain-based authentication and tamper-proof packaging, but implementing these technologies across fragmented supply chains remains costly and complex.

Rising trade barriers and tariffs

Rising trade barriers and tightening regulations are disrupting fashion accessories consumption across Asia-Pacific. The removal of low-value import exemptions in countries like Australia, India, and Indonesia has increased duties on cross-border purchases, making international fast-fashion and accessory products more expensive for everyday consumers. Governments are also stepping up enforcement on foreign e-commerce platforms. For instance, Indonesia banned Temu in 2024 for non-compliance with local trade rules, while India has imposed stricter norms on platforms like Shein and AliExpress, curbing their operations. These measures are raising prices, reducing product variety, and limiting access to affordable international brands, especially in markets where consumers increasingly rely on cross-border digital channels for trendy, low-cost accessories.

Segment Analysis

By Product Type: Apparel Dominance Faces Watch Innovation

In 2024, apparel accessories accounted for 57.35% of the Asia-Pacific fashion accessories market. Items like belts, scarves, and costume jewelry remain essential due to changing fashion trends and social media influence. Retailers boost sales through bundled deals and private-label collections, while sourcing hubs in China and Vietnam enable quick restocking. Sustainability demands are driving the use of eco-friendly materials like recycled polyester and low-impact dyes. Personalized products, such as monogrammed items, are also gaining popularity, fostering stronger customer connections and reducing price sensitivity.

Watches are the fastest-growing category, with a 6.98% CAGR projected through 2030. Wealthy millennials favor Swiss mechanical watches as investments, while mainstream consumers prefer smartwatches for features like health tracking and contactless payments. Collaborations between tech firms and fashion brands accelerate wearable technology integration. Local manufacturers in Shenzhen and Seoul reduce costs and enable regional customization. Brands enhance loyalty by offering complementary products like interchangeable straps and charging docks, increasing value for Asia-Pacific consumers.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End User: Women Lead While Children Accelerate

In 2024, women contributed 54.35% of the revenue, reflecting their frequent purchases and diverse preferences for accessories like handbags, jewelry, and hair ornaments. Retailers are engaging female shoppers through exclusive collections, influencer collaborations, and buy-now-pay-later options. Advanced customer management tools enable life stage-based segmentation, allowing targeted promotions like bridal jewelry for brides-to-be. Women’s preference for ethically sourced products is driving demand for traceable gold and lab-grown diamonds, aligning with sustainability and ethical values.

The kids' segment is projected to grow at a 7.24% CAGR from 2025 to 2030, making it the fastest-growing demographic. Dual-income households are increasing spending on children’s accessories, often inspired by adult fashion trends. Safety concerns drive manufacturers to use non-toxic dyes and child-safe designs. Licensing agreements with entertainment franchises boost brand appeal, while educators influence functional features like ergonomic backpack straps. Online shopping is rising, offering parents convenience and easy returns.

By Category: Mass-Market Stability Meets Premium Acceleration

In 2024, mass-market products captured a dominant 69.46% market share, largely attributed to their affordability and widespread accessibility. Manufactured in bulk with standardized designs, these products enable producers to maintain lower costs. Retailers, leveraging efficient logistics like just-in-time inventory management, ensure product availability while sidestepping overstocking. Furthermore, predictive analytics empower retailers to forecast demand, averting stock shortages in major discount outlets. Despite intense price competition, certain brands carve out a niche by introducing sustainability certifications and offering inclusive sizing, broadening their customer appeal. Moreover, flexible return policies in both online and brick-and-mortar stores bolster trust and loyalty among mass-market shoppers.

On the other hand, premium products are set to expand at a 7.65% CAGR until 2030, fueled by consumers' desire for exclusivity and distinctive shopping experiences. Highlighting traditional craftsmanship, limited-edition collections, and bespoke services, these products command their elevated price tags, even in markets where spending is typically restrained. Premium brands are streamlining their supply chains for transparency and quality, ensuring materials are both top-notch and ethically sourced. Some are even venturing into the digital realm, utilizing non-fungible tokens (NFTs) as a modern stamp of authenticity. By straddling both mass-market and premium segments, major players can diversify their portfolios, ensuring resilience against economic shifts in the Asia-Pacific fashion accessories arena. This dual approach empowers them to pivot production and offerings in tune with evolving consumer tastes and market dynamics.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Digital Transformation Accelerates

Physical stores accounted for 64.77% of sales in 2024, showing that many customers still prefer to see and touch accessories before buying them. To improve the shopping experience, retailers are upgrading their store layouts with better visual displays, adding QR codes that provide more product details, and offering click-and-collect services. These services allow customers to order online and pick up their purchases in-store, which helps reduce delivery costs. Department stores remain a popular choice because they attract a lot of shoppers, but the rising cost of rent is pushing retailers to try new approaches. Many are experimenting with temporary pop-up stores and shop-in-shop setups, which help them stay visible to customers without committing to long-term leases.

Online sales are expected to grow at a strong 8.12% CAGR, driven by the convenience of mobile payments, high-quality visuals, and the growing influence of social-commerce platforms. In countries like China and Southeast Asia, live-stream shopping events are gaining momentum, allowing consumers to watch product demos and make purchases instantly. Retailers are also investing in seamless omnichannel strategies, integrating physical and online inventory systems to offer faster fulfillment, flexible delivery options, and real-time product availability. These innovations are reshaping the customer journey and fueling continued growth in the region’s online fashion accessories market.

Geography Analysis

In 2024, China commands a dominant 39.58% share of the regional market. This leadership position stems from its sophisticated e-commerce platforms, adeptly serving both luxury aficionados and budget-savvy accessory shoppers. Local brands swiftly pivot to trends surfacing on social media, while international luxury names infuse their marketing with Chinese zodiac symbols and culturally resonant themes. Initiatives to thwart counterfeit products and establish verification systems have bolstered consumer trust, leading to heightened purchases of premium luxury items. Yet, the market grapples with fierce competition, escalating the costs of acquiring new clientele. In response, brands are pivoting to private channels like WeChat groups, fostering direct consumer engagement, loyalty, and bespoke shopping experiences.

Thailand emerges as the region's fastest-growing market, boasting a projected CAGR of 8.55%. This surge is buoyed by a resurgence in international tourism, ushering more visitors into luxury malls and boutiques. Retailers, in turn, are curating exclusive travel-themed collections and launching pop-up stores tailored for tourists. The broader Southeast Asia region is witnessing a digital commerce boom, with projections from the Asian Development Bank indicating it will represent 61% of global B2C e-commerce transactions by 2025. Meanwhile, Vietnam enhances its export edge through blockchain-driven supply chain transparency, and Singapore solidifies its position as a logistics nexus, providing same-day cross-border deliveries and streamlined payment systems for its mobile-centric shoppers.

India's market expansion is fueled by urbanization, increasing disposable incomes, and a burgeoning retail infrastructure in smaller towns. With a rising middle class splurging on fashion accessories, both local and global brands find fertile ground for expansion. In neighboring Indonesia, celebrity endorsements wield considerable influence, underscoring the region's shared and adapted marketing strategies. Enhanced logistics, like freight routes linking India and Southeast Asia, are slashing delivery times, allowing retailers to swiftly replenish trendy accessories. This agility ensures brands cater to a growing consumer base eager for fashionable yet affordable choices.

Competitive Landscape

The competition in the Asia-Pacific fashion accessories market is fragmented. Global brands like LVMH, Hermes, and Kering, along with companies such as Nike, Adidas, and PUMA, are competing against regional and niche players. Each brand is tailoring its products to suit local cultural preferences. For example, in 2024, Nike’s research and development center in Shenzhen focused on designing products specifically for the Chinese market, showcasing a strategy known as “in-market, for-market” innovation. This approach allows global brands to stay relevant by addressing the unique needs of local consumers. At the same time, regional brands are leveraging their deep understanding of local tastes to strengthen their market presence and compete effectively with global players.

Opportunities in sustainable accessories and smart wearables are growing, with start-ups using social media platforms for marketing instead of traditional advertising. For instance, in 2024, several start-ups in Southeast Asia introduced eco-friendly bags and jewelry made from recycled materials. These products gained significant attention through Instagram and TikTok campaigns, which helped them reach a large audience without requiring high marketing budgets. Luxury brands are also adopting blockchain technology to provide authenticity certificates, which help prevent counterfeit products and build consumer trust. A notable example is LVMH’s acquisition of Chrome Hearts in 2024, which allowed the company to expand its portfolio with niche brands that have strong online followings. This highlights the increasing importance of digital engagement and sustainability in the fashion accessories market.

Global brands are increasingly collaborating with local artisans to craft culturally authentic products that meet environmental standards. Renowned names such as Hermès, Louis Vuitton, and Gucci are sourcing from Indian artisans, infusing their collections with a touch of handmade elegance. This move not only safeguards traditional craftsmanship but also resonates with eco-conscious consumers. Furthermore, contract manufacturers are expanding their operations from China to nations like Cambodia and India, mitigating risks tied to tariffs and trade restrictions. This strategic shift bolsters stable supply chains and lessens reliance on any single region. In the Asia-Pacific fashion accessories market, businesses are harnessing advanced technologies like predictive analytics and immersive product visualization. These innovations enhance efficiency, refine demand forecasting, and ensure product alignment with consumer preferences, granting companies a competitive advantage.

Asia-Pacific Fashion Accessories Industry Leaders

-

Titan Company Limited

-

LVMH Moët Hennessy Louis Vuitton SE

-

Kering SA

-

Prada SpA

-

Hermès International

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Bagzone Lifestyles Pvt. Ltd. introduced Akiki London, a new luxury handbag brand designed for modern, style-savvy women. This launch represents a significant move for the company as it steps into the premium market segment.

- November 2024: Singapore-based luxury bag brand Aupen, famous for celebrity carry-ons, formed a manufacturing partnership with LVMH Métiers d’Art. This enables Aupen to produce handbags in French ateliers while maintaining independent ownership.

- September 2024: French accessible-luxury group SMCP (Sandro, Maje, Claudie Pierlot) signed distribution deals with SSI Group in the Philippines and Map Group in Indonesia.

- March 2024: Bulgari introduced Bulgari Studio in Seoul, a creator platform showcasing digital artists, DJs, and choreographers, and used the launch to reinforce its iconic accessories through cultural storytelling in a key Asia-Pacific market.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Asia-Pacific fashion accessories market as all new consumer products classified under footwear, apparel-related add-ons (belts, scarves, caps), wallets, handbags, watches, sunglasses, and jewelry sold across physical and digital retail channels to men, women, and children in 15 regional economies.

Scope Exclusion: Digital skins/NFT accessories and second-hand or rental sales sit outside this scope.

Segmentation Overview

-

By Product Type

- Footwear

- Apparel

- Wallets

- Handbags

- Watches

- Sunglasses

- Jewelery

-

By End User

- Men

- Women

- Kids/Children

-

By Category

- Mass

- Premium

-

By Distribution Channel

- Offline Stores

- Online Stores

-

By Geography

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview sourcing managers at regional brand owners, merchandisers at department stores, and marketplace category heads across China, India, Japan, Australia, and ASEAN. These discussions validate average selling prices, online share shifts, premium-line penetration, and promotional calendars, allowing us to reconcile secondary indicators with ground realities.

Desk Research

We start by mapping the spending pool through public sources such as UN Comtrade shipment codes, World Bank household-consumption tables, National Bureau of Statistics of China retail series, India's MOSPI Consumer Expenditure Survey, and tourism arrival figures from UNWTO, which together establish category demand patterns. Trade bodies, for example, the Japan Fashion Association and China Leather Association, clarify segment shares, while corporate filings retrieved via D&B Hoovers and news flows on Dow Jones Factiva shed light on brand revenues and launch prices. Macroeconomic baselines, including exchange rates, inflation, and urban disposable-income trends, come from IMF and respective central-bank bulletins. This list is illustrative; many additional open datasets underpin our desk work.

Market-Sizing & Forecasting

A top-down build begins with household outlay on clothing and footwear, allocating accessory wallet shares by country, then adjusting with production and trade data to reflect cross-border tourist purchases. Results are stress-tested through selective bottom-up checks, including supplier roll-ups and sampled ASP × volume estimates in footwear, handbags, and watches, which are then used to fine-tune totals. Key model inputs include urban disposable-income growth, e-commerce penetration, luxury-tourist footfall, counterfeit-seizure trends, and average replacement cycles. Forecasts rely on multivariate regression that links category sales to those variables and consensus expectations gathered from our expert panel; gaps in manufacturer disclosures are bridged using channel mark-up heuristics derived from interviews.

Data Validation & Update Cycle

Outputs pass three-layer variance checks against historical series, peer ratios, and fresh news events before senior analyst sign-off. Reports refresh every twelve months, with interim updates triggered by material events such as tariff shifts or pandemic waves, so clients receive a current, balanced view.

Why Mordor's Asia-Pacific Fashion Accessories Baseline Inspires Confidence

Published estimates often vary because firms draw different product baskets, geographic cuts, and price assumptions.

Key gap drivers here include narrower product menus, omission of tourist demand, aggressive or conservative ASP progressions, and refresh cadences that lag fast-moving channels like cross-border e-commerce.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.01 trillion (2025) | Mordor Intelligence | |

| USD 154.6 billion (2024) | Regional Consultancy A | Excludes footwear and sporty apparel add-ons; relies on historical import data without online sales adjustments |

| USD 125.2 billion (2024) | Trade Journal B | Covers only five major economies; counts formal retail receipts and updates biennially, overlooking price re-indexing |

The comparison shows that when accessory breadth, online channel capture, and timely economic signals are fully considered, Mordor's disciplined approach delivers a transparent, reproducible baseline that decision-makers can rely on.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the Asia-Pacific fashion accessories market?

The market is valued at USD 1.01 trillion in 2025 and is forecast to reach USD 1.39 trillion by 2030.

Which product category is growing fastest?

Watches, including smartwatches and luxury timepieces, are projected to grow at a 6.98% CAGR through 2030.

How important is China within the regional market?

China contributed 39.58% of 2024 revenue, making it the single largest national market.

What share do online channels hold?

Offline stores still dominate with 64.77% share in 2024, but online channels are advancing at an 8.12% CAGR.