Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

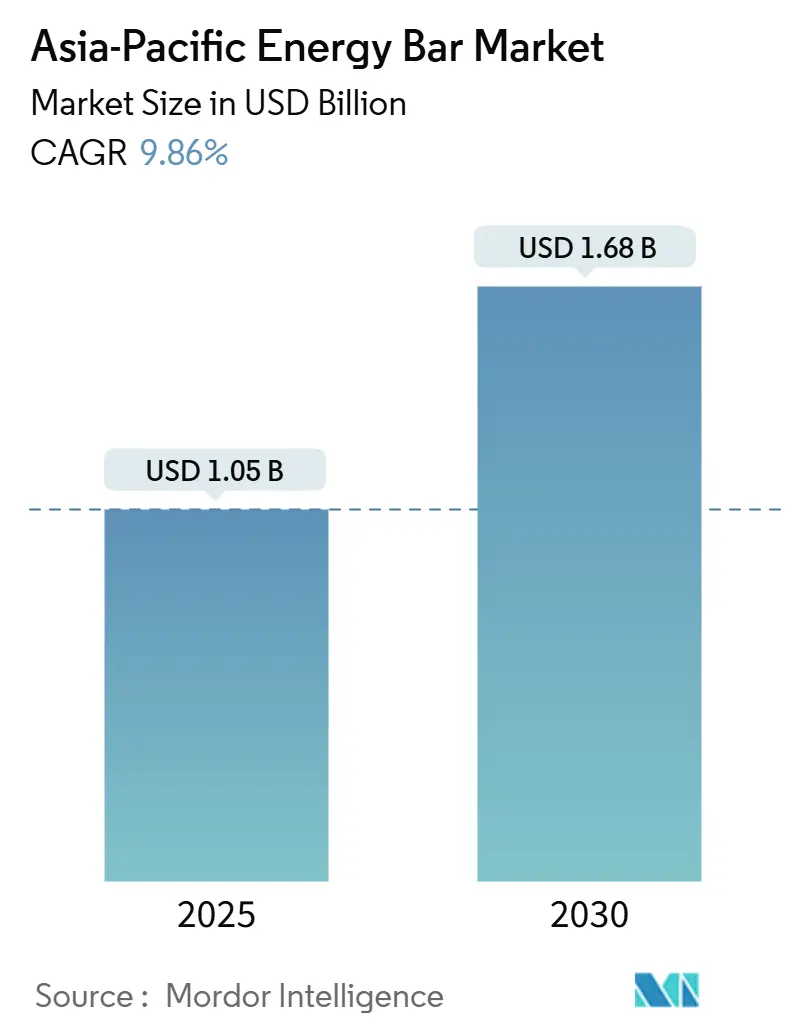

| Market Size (2025) | USD 1.05 Billion |

| Market Size (2030) | USD 1.68 Billion |

| Growth Rate (2025 - 2030) | 9.86% CAGR |

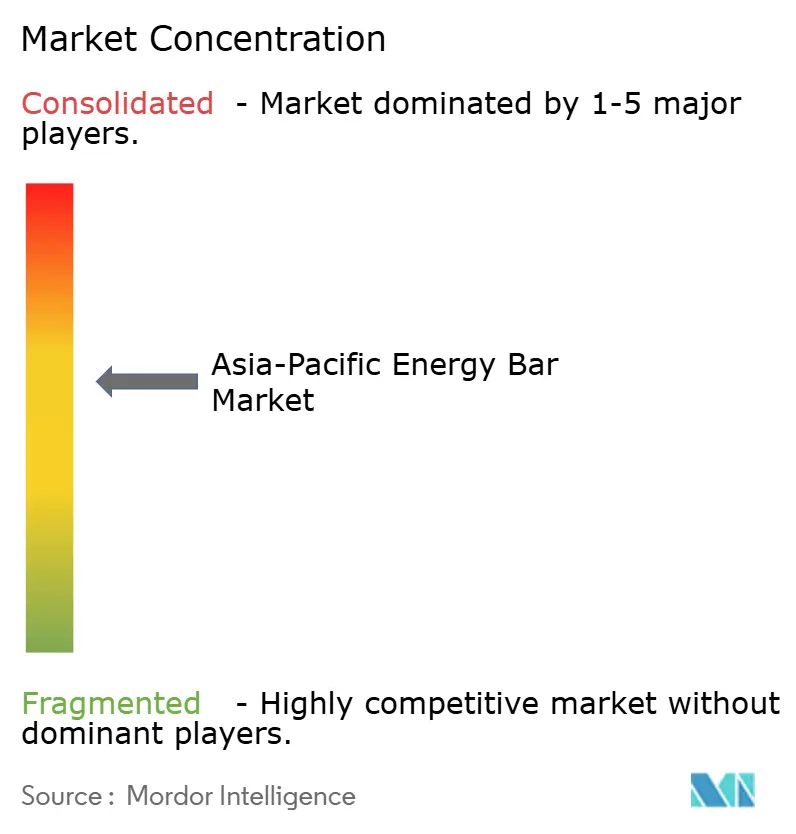

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Energy Bar Market Analysis by Mordor Intelligence

The Asia-Pacific energy bar market, valued at USD 1.05 billion in 2025, is projected to grow significantly, reaching an estimated USD 1.68 billion by 2030. This represents a strong CAGR of 9.86%, which surpasses the growth rates of many other packaged-food segments in the region. The market's rapid expansion is driven by several key factors, including the increasing urban population, longer working hours, the rising disposable income of the middle class, growing health consciousness, and a heightened demand for convenient and nutritious food options. The market benefits from a surge in fitness participation across the region, which has led to greater demand for energy bars as a quick and healthy snack option. Additionally, companies are actively reformulating their products to align with consumer preferences for low-sugar and protein-rich snacks, while regulatory frameworks are increasingly favoring such healthier alternatives. These factors collectively create a favorable environment for market growth. Multinational corporations are demonstrating confidence in the market's potential by investing in automated manufacturing facilities in key countries such as China, India, and Indonesia. These investments not only enhance production efficiency but also indicate a long-term commitment to scaling operations in the region. Furthermore, the integration of regionally sourced ingredients, such as soy isolates from Japan and nuts from Southeast Asia, helps reduce supply-chain risks and ensures a steady supply of raw materials. The trend of premiumization is unlocking additional revenue streams, as consumers in markets like Japan, South Korea, and urban China are increasingly willing to pay a premium for energy bars that feature clean-label claims, organic ingredients, and functional health benefits. This willingness to invest in high-quality products supports sustained profitability for manufacturers, even in the face of fluctuating commodity prices. Overall, these dynamics position the Asia-Pacific energy bar market for robust growth and long-term success.

Key Report Takeaways

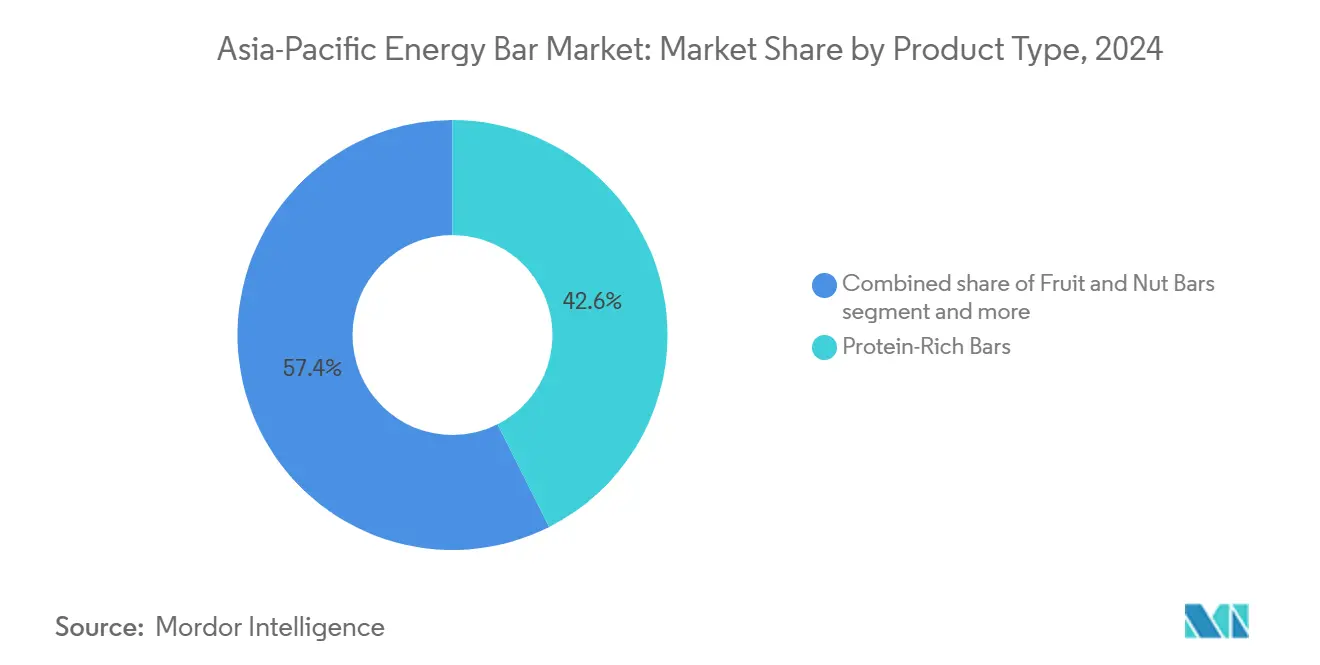

- By product type, protein-rich bars held 42.57% of the energy bar market share in 2024, and fruit-and-nut bars are forecast to expand at a 9.98% CAGR to 2030.

- By flavor profile, chocolate-based variants accounted for 52.35% of 2024 revenue, while fruit flavors are on course for the fastest 10.28% CAGR through 2030.

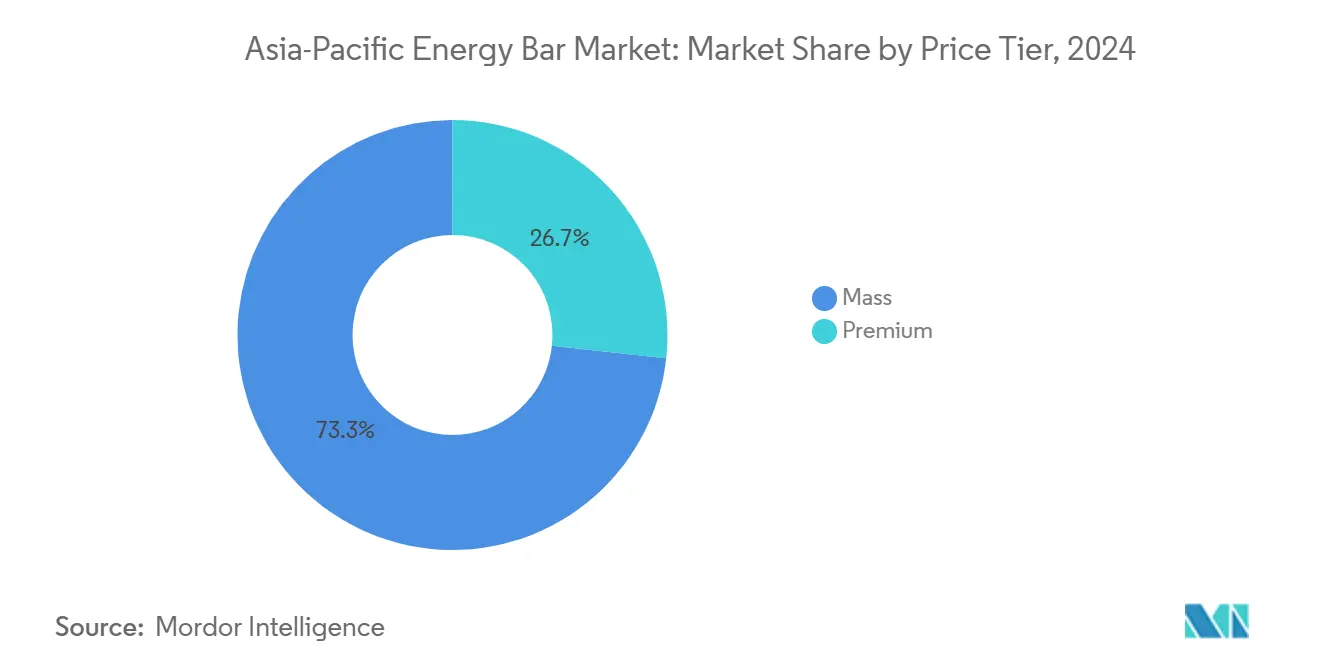

- By price tier, the mass segment represented 73.28% of 2024 sales, and the premium segment is projected to grow at a 10.39% CAGR to 2030.

- By distribution channel, supermarkets and hypermarkets delivered 42.27% of the 2024 value, yet online retail is projected to lead with a 10.72% CAGR to 2030.

- By geography, China commanded 35.28% revenue in 2024, whereas India is set for the highest 10.97% CAGR over the forecast horizon.

Asia-Pacific Energy Bar Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health consciousness and demand for convenient nutrition | +2.5% | Global, with strongest uptake in urban China, India, Japan, South Korea | Medium term (2-4 years) |

| Surge in sports and fitness participation and gym memberships | +1.8% | India, China, Southeast Asia core markets; spillover to Australia, New Zealand | Medium term (2-4 years) |

| Surge in on-the-go snacking aligns with busy urban routines | +1.5% | Urban centers across China, India, Japan, South Korea, Singapore, Thailand | Short term (≤ 2 years) |

| Preference for clean-label, natural, and organic ingredients | +1.2% | Japan, South Korea, Australia, urban China and India | Medium term (2-4 years) |

| Growth of plant-based energy bars with regional ingredients | +1.0% | India, Southeast Asia, with early adoption in Japan, Australia | Long term (≥ 4 years) |

| Government initiatives promoting healthy eating habits | +0.8% | Thailand, India, China (national nutrition programs and school feeding schemes) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising health consciousness and demand for convenient nutrition

Urban professionals are increasingly relying on energy bars as convenient meal replacements during their hectic work schedules, prioritizing functional benefits over taste. These health-conscious consumers are not merely looking for any energy bar; they are actively seeking products that align with their health goals and are willing to pay a premium for such offerings. Specifically, 75% of these consumers are prepared to spend more on energy bars that emphasize high-protein content or promote digestive health. This willingness to invest in health-focused products has driven significant changes in the industry. According to the Asia Food and Beverage Alliance (AFBA), as of 2024, an overwhelming 96% of food and beverage companies are reformulating their products to cater to these evolving health demands[1]Source: Asia Food & Beverage Alliance (AFBA), "The Reformulation Challenge", afba.co. Furthermore, consumers are demonstrating a readiness to pay 10-20% higher prices for products with enhanced nutritional profiles. The growing demand for functional foods, particularly those fortified with vitamins, minerals, and bioactive compounds, underscores this trend. This convergence of consumer willingness to invest in health, regulatory support for health claims, and proactive reformulation efforts by manufacturers is creating a sustained demand trajectory. Unlike short-lived health fads, this momentum reflects a deeper, long-term shift in consumer preferences and industry practices.

Surge in sports and fitness participation and gym memberships

The growing fitness culture across the Asia-Pacific region is significantly boosting the demand for protein-rich energy bars. In India, brands such as MuscleBlaze, RiteBite, and Yoga Bar are expanding their presence in the direct-to-consumer nutrition market by utilizing digital-first distribution strategies and influencer partnerships. Gen Z and Millennials are increasingly prioritizing protein content over other nutritional factors. The expansion of fitness centers, health clubs, gyms, and yoga studios across the Asia-Pacific is directly driving the need for portable pre- and post-workout nutrition options, including energy and protein bars. For example, the Australian Bureau of Statistics reported that Australia had 7,313 operational health and fitness centers and gyms in 2024[2]Source: Australian Bureau of Statistics, "Counts of Australian Businesses, including Entries and Exits", abs.gov.au. Energy bars, positioned as key sports nutrition products, offer benefits such as sustained energy, muscle-repairing protein, added fiber, and essential micronutrients, aligning with the performance goals of gym users and athletes. Additionally, gyms and fitness studios serve as crucial retail points for energy bars, often displaying them at reception areas or vending machines, effectively converting gym traffic into impulse purchases. The tech-savvy fitness community also favors e-commerce and subscription models for sports nutrition, driving online sales of energy and protein bars through various platforms and brand-specific websites.

Surge in on-the-go snacking aligns with busy urban routines

The Asia-Pacific energy bar market is experiencing growth as busy urban lifestyles drive demand for portable, nutritious, and time-saving food options. Energy bars, known for being compact and shelf-stable, are increasingly perceived as healthier alternatives to traditional impulse snacks. With demanding work schedules and the rise of hybrid work models, many consumers in Asia are adopting snacks to replace or supplement meals, a trend referred to as “snackification.” In this scenario, energy and nutrition bars serve as convenient choices for breakfast, mid-morning, or late-afternoon consumption, offering satiety and energy without requiring preparation. Urban consumers are favoring grab-and-go formats that are easy to consume during transit, at desks, or between meetings. Energy bars, designed with single-serve packaging and minimal mess, meet this need effectively. They provide portion-controlled calories and macros, appealing to individuals focused on managing weight and energy intake while snacking more frequently. According to the World Bank, 66% of China's population lived in urban areas in 2024[3]Source: World Bank, "Urban population (% of total population) - China", worldbank.org. As working hours increase in tier-1 and tier-2 cities, meal preparation time is becoming more limited. This trend makes nutrient-dense, shelf-stable bars a practical solution for commuters and office workers.

Preference for clean-label, natural, and organic ingredients

Consumers are increasingly examining ingredient lists with unprecedented scrutiny, driving manufacturers to reformulate their products to align with these elevated expectations or risk losing relevance in the competitive market. This behavioral shift is further supported by significant regulatory developments across major markets. In 2024, Thailand's FDA introduced updated health claim guidelines designed to enhance transparency and ensure accurate product labeling. Likewise, Indonesia's BPOM enforced stricter labeling requirements to build consumer confidence, while China's GB 2760-2024 standard imposed more stringent restrictions on permissible food additives to prioritize safety and compliance. The rising demand for clean-label products has fueled the premiumization of this category, creating a distinctly bifurcated market. Mass-tier brands are struggling with margin pressures as they adapt to these changes, while premium brands and new entrants are leveraging this trend to secure a disproportionate share of the market's value, further intensifying competition.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer concerns over artificial ingredients and preservatives | -0.5% | Japan, South Korea, and Australia | Short term (≤ 2 years) |

| Lack of awareness about energy bar benefits in rural areas | -0.3% | Rural India, Indonesia, Thailand, Philippines | Medium term (2-4 years) |

| Fluctuating raw material prices disrupt supply chain stability | -0.6% | Singapore, Hong Kong | Short term (≤ 2 years) |

| Stringent health and safety regulations increase operational complexity | -0.4% | India (FSSAI), China (GB standards), Thailand (FDA), Indonesia (BPOM) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer concerns over artificial ingredients and preservatives

Manufacturers are under pressure as regulatory tightening and consumer opposition to artificial additives compel them to reformulate. These adjustments increase costs, squeezing margins and delaying product launches. China's GB 2760-2024 standard imposes stricter limits on permissible food additives, requiring manufacturers to replace synthetic preservatives with natural alternatives that are often more expensive and have shorter shelf lives. In 2024, Hong Kong revised its preservatives regulation, introducing stricter labeling requirements and maximum residue limits for benzoates and sorbates, commonly used in energy bars. The FAO's 2024 State of Commodity Markets report highlighted Asia's status as a net importer of ultra-processed foods. This finding, along with concerns about additive exposure, has prompted governments to enforce stricter import controls. Consumers are increasingly scrutinizing ingredient lists, and products containing artificial additives face immediate rejection, particularly among health-conscious buyers. This trend is especially evident in Japan and South Korea, where transparency is highly valued. Manufacturers in these markets face significant reputational risks if synthetic ingredients are detected. However, the reformulation challenge disproportionately impacts small and mid-sized producers, who lack the R and D resources and supply chain advantages of multinational corporations. This situation creates a competitive advantage for established players in the market.

Fluctuating raw material prices disrupt supply chain stability

Commodity price volatility continues to compress profit margins, compelling manufacturers to make difficult decisions, either absorb the rising costs themselves or pass them on to consumers who are highly sensitive to price changes. According to the OECD-FAO Agricultural Outlook 2024-2033, the demand for nuts and protein ingredients in India and Southeast Asia is projected to grow at a pace that exceeds domestic production capabilities. This imbalance is expected to increase reliance on imports, thereby exposing these markets to greater risks associated with currency fluctuations. Additionally, the prices of soybean oil and palm oil have experienced significant increases, primarily driven by biodiesel mandates in countries such as Brazil, Indonesia, and the United States. These mandates redirect edible oils from food production to fuel production, further tightening supply. Manufacturers that adopt diversified sourcing strategies and implement effective hedging mechanisms are likely to manage this volatility more effectively compared to those that depend heavily on spot markets and single-origin ingredient sources.

Segment Analysis

By Product Type: Protein Bars Dominate but Fruit-Nut Variants Gain Ground

In 2024, protein-rich bars secured a dominant 42.57% share of the market, driven by fitness enthusiasts, meal-replacement users, and sports nutrition fans who prioritize nutrient density over flavor. Pulmuone's Tofu Bar, a whole-soy protein offering from Japan, achieved a milestone of 70 million units sold by July 2024. With a presence in over 30,000 stores, it underscores the potential for protein bars to penetrate the mass market, especially when marketed as everyday wellness items rather than exclusive sports supplements. The protein bar segment benefits from a halo effect as sports nutrition gains mainstream acceptance, further solidifying its position in the market. This normalization of sports nutrition beyond dedicated athletes has expanded the consumer base for protein bars, making them a staple for individuals seeking convenient, nutrient-dense options in their daily routines.

However, cereal and granola bars, which cater to breakfast replacements and children's snacks, are facing margin pressures as consumers increasingly opt for protein-rich or fruit-based alternatives. Fruit and nut bars are forecast to grow at a brisk 9.98% CAGR from 2025 to 2030, driven by their clean-label positioning and plant-based ingredients. These attributes resonate with health-conscious consumers who value perceived naturalness over protein concentration. While protein bars dominate the market, fruit and nut bars are capturing a different segment of consumers seeking indulgence without guilt. This dynamic creates a bifurcated growth path, spotlighting innovation on both ends of the functional spectrum. The evolving preferences of consumers highlight opportunities for brands to innovate and cater to diverse needs within the functional bar market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Flavor Profile: Chocolate Leads but Fruit Variants Surge

Chocolate-based bars commanded a 52.35% share of the market in 2024, underscoring a consumer inclination towards indulgent flavors that not only mask the bitterness of protein isolates but also deliver sensory satisfaction. However, fruit-based bars are set to outpace chocolate counterparts, boasting a projected growth rate of 10.28% CAGR from 2025 to 2030. This growth is attributed to their clean-label appeal and natural sweetness, which resonate strongly with health-conscious consumers. Nut and seed-based bars, though positioned at a premium due to higher ingredient costs, cater to the growing demand for whole-food nutrition. Meanwhile, flavors like savory and regional variants remain experimental but present brands with opportunities to break free from the chocolate-fruit dominance. At FBIF 2024, Angel Yeast, in collaboration with ffit8, unveiled a nougat protein bar, setting itself apart by incorporating yeast protein, a departure from the usual whey or soy isolates.

Flavor preferences are dictated more by consumption occasions rather than absolute preference. Chocolate dominates impulse buys and children's snacks, while fruit-based bars are favored for health-centric snacking. Nut and seed options cater to those seeking premium meal replacements. This segmentation suggests that manufacturers would benefit from maintaining a diverse multi-SKU portfolio rather than focusing on a singular flavor platform. By addressing varied consumer needs and occasions, brands can better position themselves in a competitive market landscape.

By Price Tier: Mass Dominates but Premium Captures Disproportionate Growth

In 2024, mass-tier products dominated the market, accounting for a 73.28% share. This trend highlights the significant price sensitivity in developing Asia-Pacific markets, where per-capita incomes remain below those of developed economies. Premium-tier bars are projected to grow at a 10.39% CAGR from 2025 to 2030, surpassing mass-tier growth by 153 basis points. This growth is driven by the expansion of the middle class and an increasing willingness to pay for functional benefits. A 2024 European consumer study revealed that consumers are willing to pay premiums for functional snack bars with health attributes. This willingness is mirrored in Asia-Pacific markets, where disposable incomes are rising at a faster pace compared to mature economies. In the Philippines, the snack market recorded listing fees of approximately USD 100 per SKU per store, creating entry barriers that favor established brands with scale. However, these barriers also incentivize premium positioning to justify retailer margins.

The premiumization trend, however, is not uniform across the region. Markets such as Japan, South Korea, and urban China exhibit the strongest willingness to pay for premium products. In contrast, price-sensitive markets like Indonesia, Thailand, and rural India require mass-tier offerings to achieve volume penetration. This disparity suggests that multinational entrants may benefit from adopting a dual-brand strategy to cater to the diverse market dynamics within the region. By leveraging premium-tier products in affluent markets and mass-tier offerings in price-sensitive areas, companies can optimize their market presence and address varying consumer preferences effectively.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Supermarkets Lead but E-Commerce Disrupts

In 2024, supermarkets and hypermarkets commanded a 42.27% share of the market, capitalizing on shelf visibility, the dynamics of impulse purchases, and ingrained consumer shopping habits. Convenience stores, catering to on-the-go consumers, effectively tap into commuter traffic. Specialty stores, on the other hand, focus on health-food aficionados, offering curated selections and expert guidance. Other channels, such as gyms, pharmacies, and vending machines, though niche, provide targeted access to consumers with specific intents. These diverse distribution channels reflect the evolving preferences of consumers and their varied shopping behaviors.

From 2025 to 2030, online retail is projected to lead with a robust 10.72% CAGR, spurred by the rise of quick commerce platforms, the allure of social commerce, and direct-to-consumer models that sidestep traditional retail hurdles. The distribution landscape is fragmenting: while supermarkets drive volume, they also demand slotting fees and promotions that can squeeze margins. E-commerce platforms foster direct relationships with consumers but necessitate significant digital marketing investments. Convenience stores excel in high-margin impulse sales but offer a limited range of SKUs. This dynamic environment compels manufacturers to adopt omnichannel strategies, moving away from reliance on any single dominant channel.

Geography Analysis

In 2024, China accounted for 35.28% of the global snack market, maintaining its position as the leading geography by revenue. However, the market is slowing down as urbanization stabilizes and health regulations become stricter. The growing urban population and increasing health awareness in China are driving demand for protein-rich and low-calorie snacks, with consumers favoring products with natural claims. Domestic companies are expanding rapidly: In November 2024, Qiaqia Food launched its 11th plant in Baotou, Inner Mongolia, increasing its annual production capacity to 39,000 metric tons of sunflower seeds and 6,000 metric tons of nuts. At the same time, regulatory challenges are intensifying: China's GB 2760-2024 standard imposes stricter limits on food additives, with compliance costs creating advantages for larger players over startups.

India is projected to grow at a strong 10.97% CAGR from 2025 to 2030, making it the fastest-growing geography among major markets. This growth is driven by the increasing adoption of sports nutrition, the rise of direct-to-consumer distribution, and the expansion of the middle class. In December 2024, Zydus Wellness acquired Naturell India (RiteBite Max Protein), marking a consolidation in a previously fragmented market. Key players in the market now include Yoga Bar, RiteBite, The Whole Truth, EAT Anytime, MuscleBlaze, and HealthKart. The rapid growth of quick commerce platforms in India has transformed energy bars from planned purchases into impulse buys, with delivery times as short as 10-15 minutes. India's Food Safety and Standards Authority (FSSAI) enforces labeling and licensing requirements for nutraceuticals, ensuring product quality and fostering consumer trust, though these regulations tend to favor established players due to the associated compliance costs.

Japan and South Korea are mature markets that focus on premium products, where innovation and functional claims are key differentiators. In May 2024, South Korea's Otsuka Pharmaceutical introduced SOYJOY, distributing it through online platforms and health-and-beauty retail outlets to appeal to health-conscious consumers seeking low-glycemic-index options. Southeast Asia, including countries like Thailand, Indonesia, and Singapore, shows fragmented growth trends. Meanwhile, Australia and New Zealand, though smaller markets, feature high-value segments. These regions benefit from well-established health-food retail channels and consumers willing to pay a premium for clean-label and organic products, even though specific market size data for these geographies remains limited.

Competitive Landscape

The Asia-Pacific energy bar market is moderately consolidated, with multinational food corporations competing against agile local players across various price tiers and distribution channels. Strategies differ based on market maturity: in China and India, multinationals prioritize local manufacturing and flavor adaptation, while in Japan and South Korea, differentiation is driven by innovation in functional ingredients and premium positioning. PepsiCo's USD 1.3 billion investment in a Shaanxi food production base and its partnership with Jiangsu Rilong Food to enhance the Quaker brand in China's cereal nutrition segment highlight this focus on capacity building.

Opportunities for growth include rural markets in India, Indonesia, and the Philippines, where awareness of energy bar benefits remains limited, and premiumization in Japan, South Korea, and urban China, where consumers are willing to pay for functional claims and clean-label ingredients. Emerging disruptors are leveraging direct-to-consumer models, social commerce, and influencer partnerships to bypass traditional retail challenges. The Asia-Pacific energy bar market is highly competitive, with key players including Clif Bar and Company, Abbott Laboratories, General Mills, Inc., Kellanova, and PROBAR LLC. Companies are employing strategies such as new product development and mergers and acquisitions to meet consumer demands.

Technology is reshaping competition through e-commerce platforms, rapid logistics, and data-driven personalization. Manufacturers are adopting automation to mitigate raw material price volatility. Regulatory compliance is becoming a competitive advantage: China's GB 2760-2024 additive restrictions, India's FSSAI licensing requirements, and Thailand's FDA health claim regulations create barriers that favor established players with strong regulatory expertise over startups. The competitive landscape is dividing into two segments: scale players focusing on distribution reach and cost efficiency, and premium disruptors emphasizing innovation, functional claims, and direct consumer engagement, leaving minimal space for undifferentiated brands.

Asia-Pacific Energy Bar Industry Leaders

-

General Mills, Inc.

-

Probar LLC

-

Clif Bar and Company

-

Kellanova

-

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- August 2025: Phab introduced India's first Savory Protein Bar, inspired by the iconic Street Snack, Bhel. This addition to Phab's new Street Collection reimagines one of the country's most cherished snacks as a portable, protein-packed, and healthier alternative.

- October 2024: Zydus Wellness Limited has acquired Naturell India Pvt. Ltd., the manufacturer of RiteBite Max Protein energy bars. This acquisition strengthens the fragmented protein bar market in India and enables Zydus to expand its distribution network through modern trade and e-commerce channels.

- July 2024: Angel Yeast, a global leader in yeast production, has partnered with the health-focused brand ffit8 to introduce two innovative products: the nougat protein bar and the protein nougat snack, both enriched with Angel Yeast's high-quality protein.

Asia-Pacific Energy Bar Market Report Scope

By Product type

| Cereal/Granola Bars |

| Protein-Rich Bars |

| Fruit and Nut Bars |

By Flavor Profile

| Chocolate-based Bars |

| Fruit-based bars |

| Nut and Seed-based bars |

| Other Flavors |

By Price Tier

| Mass |

| Premium |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail |

| Specialty Stores |

| Other Distribution Channels |

By Country

| China |

| Japan |

| India |

| Thailand |

| Singapore |

| Indonesia |

| South Korea |

| Australia |

| New Zealand |

| Rest of Asia-Pacific |

| By Product type | Cereal/Granola Bars |

| Protein-Rich Bars | |

| Fruit and Nut Bars | |

| By Flavor Profile | Chocolate-based Bars |

| Fruit-based bars | |

| Nut and Seed-based bars | |

| Other Flavors | |

| By Price Tier | Mass |

| Premium | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail | |

| Specialty Stores | |

| Other Distribution Channels | |

| By Country | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large will the Asia-Pacific energy bar market be by 2030?

It is projected to reach USD 1.68 billion, up from USD 1.05 billion in 2025, reflecting a 9.86% CAGR.

Which product type is growing fastest?

Fruit-and-nut bars show the highest 9.98% CAGR as consumers seek clean-label and plant-based snacks.

Why is India considered the key growth arena?

India combines the region’s fastest 10.97% CAGR, rapid e-commerce adoption, and regulatory frameworks that now favor fortified foods.

What is driving premium-tier expansion?

Urban consumers in Japan, South Korea, and China pay up for organic certification, plant protein, and functional claims, pushing premium bars to a 10.39% CAGR.

Page last updated on: