Asia-Pacific Electronics Manufacturing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

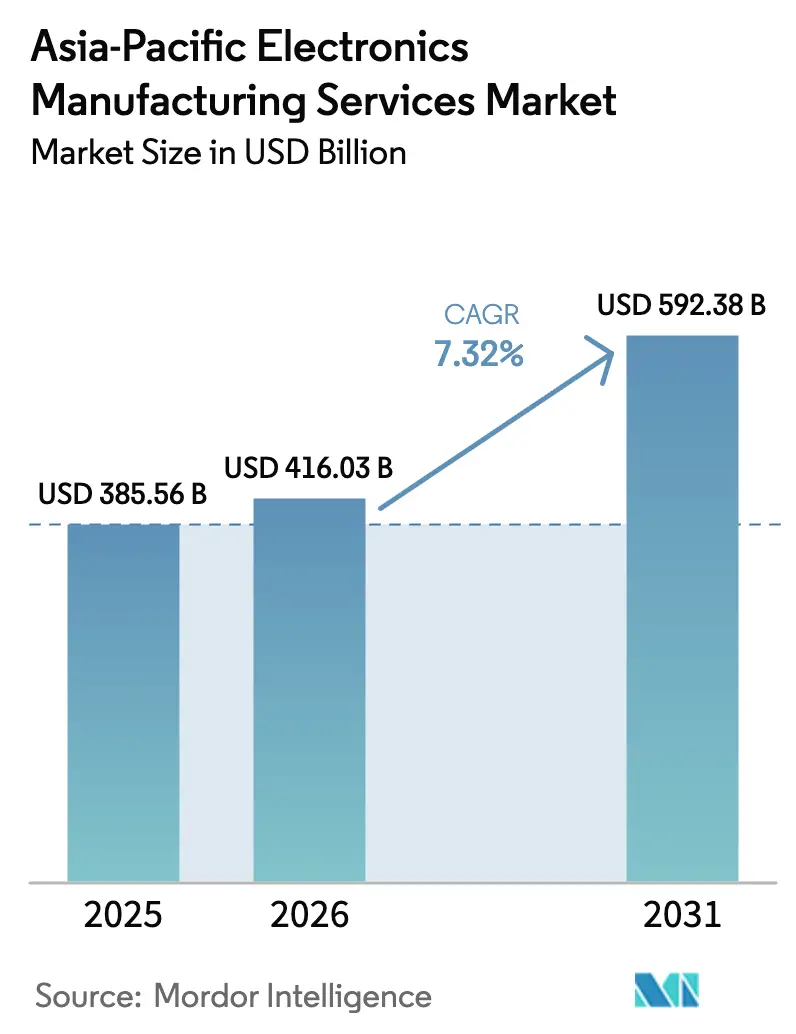

| Base Year Market Size (2025) | USD 385.56 Billion |

| Market Size (2026) | USD 416.03 Billion |

| Market Size (2031) | USD 592.38 Billion |

| Growth Rate (2026 - 2031) | 7.32% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Electronics Manufacturing Services Market Analysis by Mordor Intelligence

The Asia-Pacific Electronics Manufacturing Services Market size in 2026 is estimated at USD 416.03 billion, growing from 2025 value of USD 385.56 billion with projections showing USD 592.38 billion, growing at 7.32% CAGR over 2026-2031. The expansion reflects a structural shift toward multi-country production footprints, aggressive automation, and deeper process know-how rather than a short-term rebound. Sovereign-technology mandates are compelling original equipment manufacturers to place new lines in India, Vietnam, and Thailand, while funding upgrades for advanced packaging and heterogeneous integration in China and South Korea. Intensifying automotive electrification is boosting demand for power modules and battery-management-system assembly, and the rapid roll-out of 5G infrastructure is sustaining high-frequency board demand. Meanwhile, supply-chain resilience considerations are pushing global brands to insist on geographically dispersed final-assembly sites, forcing contract manufacturers to re-engineer logistics, inventory, and compliance programs. Competitive differentiation is shifting away from price alone toward a blend of vertical integration, intellectual property safeguards, and design-for-sustainability capabilities.

Key Report Takeaways

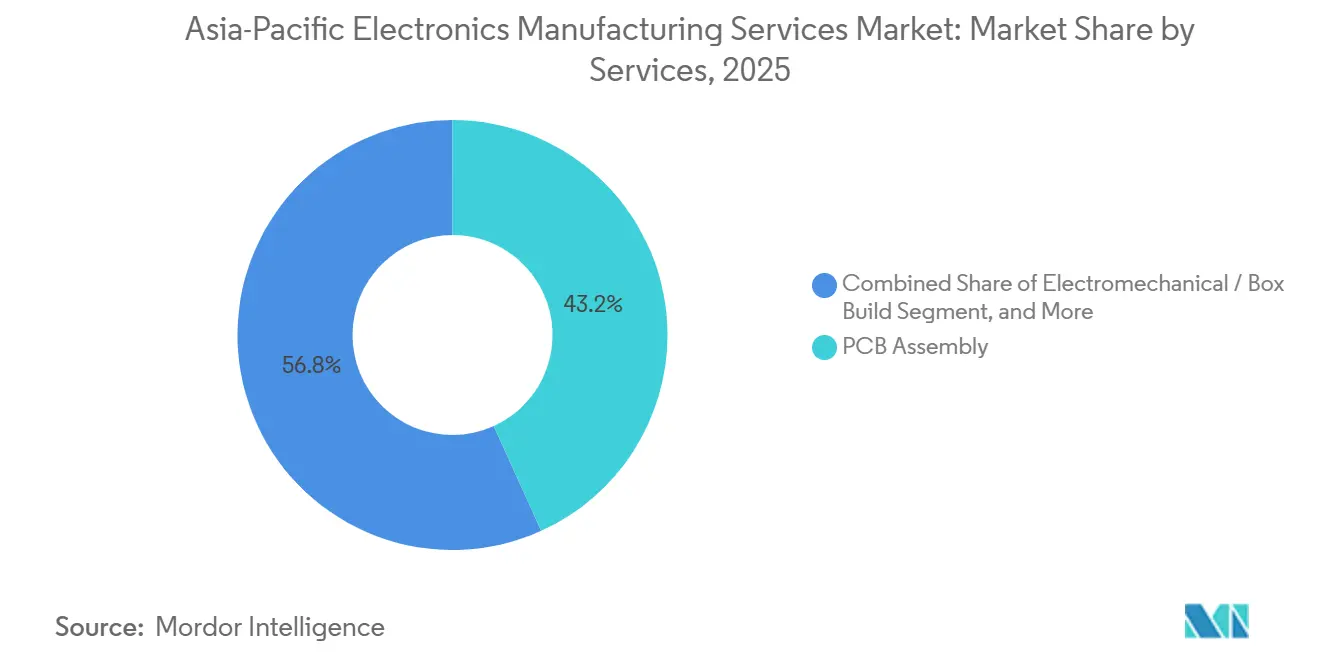

- By service category, printed-circuit-board assembly led with 43.23% of the Asia-Pacific electronics manufacturing services market share in 2025; electromechanical and box-build integration is forecast to grow at an 8.21% CAGR through 2031.

- By business model, contract manufacturing held 62.39% of the Asia-Pacific electronics manufacturing services market in 2025, while hybrid and turnkey arrangements are projected to expand at a 7.94% CAGR through 2031.

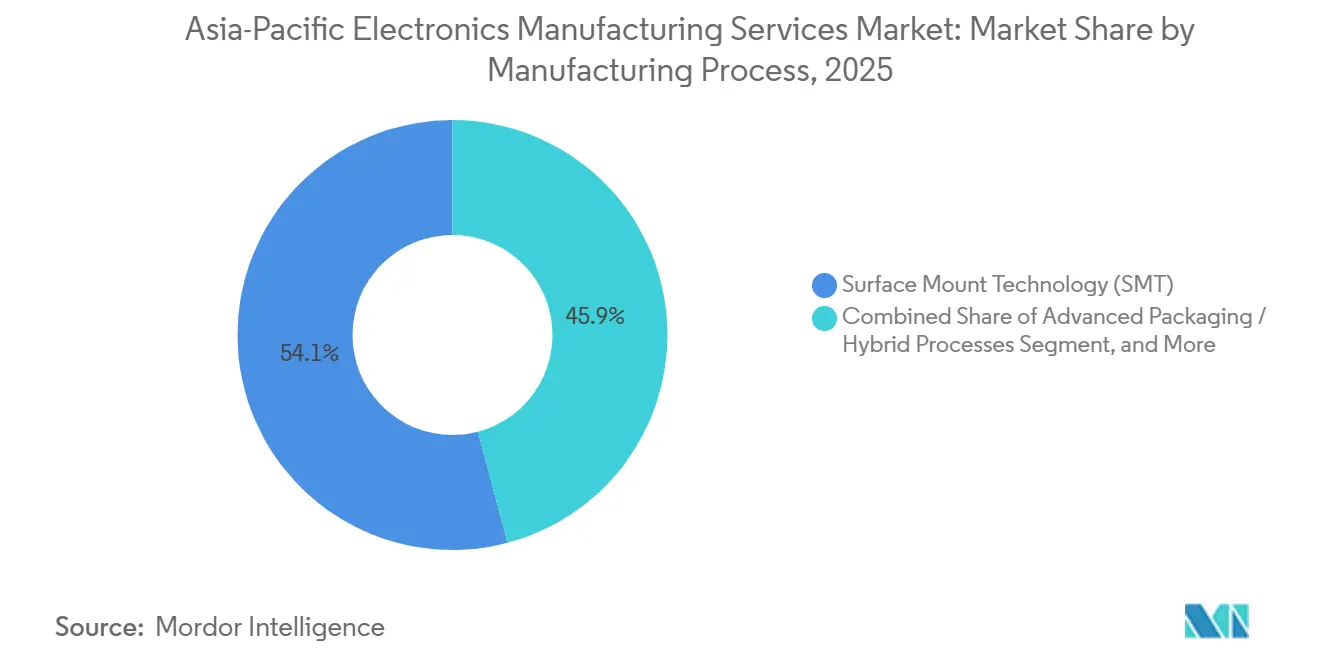

- By manufacturing process, surface-mount technology accounted for 54.12% of the Asia-Pacific electronics manufacturing services market in 2025; advanced packaging and hybrid processes are advancing at an 8.01% CAGR through 2031.

- By end-user, consumer electronics captured 36.78% revenue share in 2025, whereas automotive applications are advancing at a 9.11% CAGR through 2031.

- By geography, China commanded 52.87% of the Asia-Pacific electronic manufacturing services market share in 2025, and India records the fastest projected CAGR at 8.43% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Relative standing becomes clear only when regional contributions are evaluated alongside one another at a global level. Mordor Intelligence's electronics manufacturing services market share coverage captures this comparative structure.

Asia-Pacific Electronics Manufacturing Services Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Outsourcing of Non-Core Manufacturing | +1.5% | China, India, Malaysia, Thailand | Medium term (2-4 years) |

| Rapid Expansion of 5G and IoT Devices | +1.8% | China, South Korea, Japan, India | Short term (≤ 2 years) |

| Electrification of Vehicles | +1.6% | China, Japan, South Korea, India | Medium term (2-4 years) |

| Scaling of Smartphone and Wearable Volumes | +1.2% | India, Vietnam, Thailand, Indonesia | Short term (≤ 2 years) |

| Near-Shoring Within Asia | +0.9% | Vietnam, Thailand, Malaysia, India | Long term (≥ 4 years) |

| Rise of Design-for-Sustainability Contracts | +0.4% | Japan, South Korea, export-oriented Chinese clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Outsourcing of Non-Core Manufacturing Activities by OEMs

Original equipment makers in computing, telecom, and industrial segments are channeling scarce capital into product design while assigning routine PCB population, functional testing, and shipping to specialist partners. Foxconn and Pegatron have replicated full iPhone lines in India and Vietnam, proving that multi-gigawatt campuses can come online within 2 years when backed by tax holidays and zone infrastructure.[1]Press Information Bureau, “Production Linked Incentive Scheme for Electronics Manufacturing,” Government of India, pib.gov.in Similar moves are visible in enterprise servers, where sites in Malaysia and Thailand handle motherboard burn-in at labor costs roughly 20% below those in coastal China. Automotive brands are offloading inverter and charger assembly to EMS suppliers, who now absorb inventory risk and warranty liability, freeing carmakers to shape software-defined platforms. India’s production-linked incentive program disbursed INR 35 billion (USD 420 million) in fiscal 2025, underwriting new capacity from Dixon Technologies and Foxconn that serves both domestic orders and export consignments.

Rapid Expansion of 5G and IoT Device Production

China installed 3.68 million operational 5G base stations by December 2025, creating sustained demand for radio units, baseband cards, and low-loss RF boards.[2]Ministry of Industry and Information Technology, “5G Base Station Deployment Statistics 2025,” MIIT, miit.gov.cn South Korean carriers are upgrading to standalone 5G source millimeter wave antenna modules from EMS firms with proven RF tuning expertise. Consumer wearables and smart home sensors flow off automated lines in Vietnam and Southern China, while industrial IoT gateways are built in Japan and Taiwan, where engineering support shortens design turns. Private 5G networks in factories and ports add a fresh revenue stream for ruggedized edge devices assembled in Thailand and Malaysia. With pandemic-era semiconductor allocation largely resolved, order backlogs have normalized, and EMS providers can now align capacity with OEM forecasts.

Electrification of Vehicles Boosting Power Electronics Demand

China produced 9.59 million new energy vehicles in 2025, elevating orders for onboard chargers, DC-DC converters, and traction inverter modules that require automotive-grade soldering and conformal coating.[3]China Association of Automobile Manufacturers, “New Energy Vehicle Production Data 2025,” caam.org.cn Japanese facilities in Nagoya and Osaka have pivoted to silicon carbide power modules compliant with IATF 16949 and ISO 26262 standards. South Korean battery management system boards are now outsourced to local EMS contractors that run AOI and X-ray suites tailored to automotive reliability metrics. Indian players such as Dixon Technologies and Amber Enterprises are adding high-voltage bays capable of 800-volt insulation testing to serve Tata Motors and Mahindra Electric. As voltage platforms climb, only contractors with validated insulation processes pass customer audits, limiting competitive entry.

Scaling of Smartphone and Wearable Volumes in India and Asia-Pacific

India manufactured 330 million smartphones in 2025, feeding its home market while exporting to the Middle East and Africa. Foxconn, Pegatron, and Wistron operate megacampuses that together employ more than 400,000 workers across Tamil Nadu, Karnataka, and Uttar Pradesh. Vietnam shipped USD 148 billion in electronics during 2025, 35% of which were phones and wearables produced by Samsung and LG in Bac Ninh and Hai Phong. Thailand’s Eastern Economic Corridor now hosts smartwatch lines that integrate display bonding, sensor calibration, and water ingress testing. OEMs are shifting programs not only for cost but also to hedge tariff and geopolitical risk while tapping incentive pools that subsidize capital expenditure and working capital.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Margin Pressure from Intense Price Competition | -1.1% | China, India, Southeast Asia | Short term (≤ 2 years) |

| Supply-Chain Disruptions and Component Shortages | -0.8% | Global, spillover felt in Japan and South Korea | Medium term (2-4 years) |

| Heightened IP-Security Concerns | -0.5% | China, Vietnam, India | Medium term (2-4 years) |

| Skilled-Labor Gap for Advanced Packaging | -0.4% | Vietnam, Thailand, Malaysia, India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Margin Pressure from Intense Price Competition

Gross margins in the Asia-Pacific EMS sector compressed to the 4-7% range in 2025 as smartphone brands and hyperscale cloud operators imposed annual price downs that outpaced productivity gains. Chinese contractors face crowded local competition that curtails pricing discipline, while Taiwanese majors defend utilization at new sites in India and Vietnam by conceding on price. Turnkey deals let EMS firms mark up components while exposing them to commodity price swings and end-of-life inventory losses. Automotive contracts embed quality penalties that can erode profitability when defect rates exceed thresholds, a risk heightened by silicon carbide modules that demand tighter process windows. Leading providers respond by automating assembly, acquiring PCB shops, and pursuing integration with metals and plastics to recoup lost margins.

Supply Chain Disruptions and Component Shortages

Localized shortages persist for automotive-grade microcontrollers and high-frequency RF chips, where foundry capacity remains tight and lead times exceed 26 weeks. Late-2025 allocation of multilayer ceramic capacitors pushed EMS firms to qualify Japanese and Taiwanese alternates, adding testing cost and inventory complexity. Port congestion in Southeast Asia and sporadic airfreight gaps have stretched component transit times by up to 2 weeks, squeezing just-in-time schedules and elevating working capital needs. Export control policies on advanced semiconductors complicate planning for contractors that serve both Chinese and non-Chinese brands. Mitigation now relies on buffer stocks, multisourcing, and data-driven demand sensing to reduce the likelihood of line stoppages.

Segment Analysis

By Services: Box-Build Integration Redefines Value Capture

The Asia-Pacific EMS market continues to derive its largest share of revenue from PCB assembly, yet the electromechanical and box-build segment is expanding faster as OEMs relinquish final integration overhead. PCB assembly’s 43.23% slice in 2025 underscores its volume dominance, but commoditization pressures margins, prompting contractors to differentiate through yield leadership, NPI agility, and secure data handling. The electromechanical segment, advancing at an 8.21% CAGR, bundles cable harnessing, firmware flashing, and packaging, allowing OEMs to shift inventory liability and accelerate time-to-market. Engineering services are gaining strategic relevance, especially where design-for-manufacturability reviews help reduce field-failure rates and warranty costs. Test implementation, spanning environmental stress screening and EMC validation, is a rising revenue contributor in automotive and medical projects.

Box-build demand aligns with circular-economy imperatives that require contractors to design for easy disassembly and material recovery. Prototyping services flourish among IoT start-ups that favor partners capable of sub-week iterations. Logistics services, once an ancillary offering, have become core, with EMS firms orchestrating component kitting and direct-to-consumer drop-ship models. Repair and refurbishment are also growing, reflecting sustainability clauses in European and Japanese contracts. These dynamics collectively sustain healthy order pipelines and reinforce the role of full-service providers in the Asia-Pacific EMS market.

By Business Model: Hybrid Engagements Gain Strategic Momentum

Contract manufacturing maintained a 62.39% share in 2025, confirming its dominance in high-volume consumer devices. Yet hybrid and turnkey constructs are rising at a 7.94% CAGR as brand owners demand single-throat-to-choke accountability across design, sourcing, and assembly. Original design manufacturing maintains traction in white-label notebooks and servers, where speed beats deep differentiation. Hybrid partnerships now dominate automotive electronics and regulated medical devices, leveraging EMS firms’ component procurement and regulatory know-how while allowing OEMs to retain final IP control.

The appeal of hybrid models is amplified by the need for rapid design tweaks to accommodate component substitutions during shortages. Contractors with design benches embedded in customer campuses accelerate debug cycles and reduce engineering change order costs. VTech’s global manufacturing network exemplifies a blended approach, combining design support with distributed fulfillment to insulate clients from single-region shocks. As the Asia-Pacific EMS market evolves, business-model flexibility becomes a decisive differentiator, tilting volume toward firms able to toggle between pure build-to-print and value-added engagements.

By Manufacturing Process: Advanced Packaging Accelerates on Chiplet Architectures

Surface-mount technology retained 54.12% of assembly revenue in 2025, underlining its status as the workhorse for component placement at throughputs above 100,000 parts per hour. However, the shift to chiplet and heterogeneous integration is propelling advanced packaging and hybrid flows at an 8.01% CAGR. System-in-package, fan-out wafer-level packaging, and through-silicon via technologies offer denser interconnects, reduced latency, and smaller footprints, all of which are vital for AI accelerators and mmWave radios. Cleanroom capital intensity and sub-10-micron alignment requirements raise barriers to entry, but contractors making the leap command premium pricing and multiyear volume commitments.

ASE Technology reported USD 1.6 billion in advanced packaging revenue in 2025, showcasing the upside for early movers. Japanese and South Korean EMS firms are piloting system-in-package lines tailored for automotive radar and data-center optics, while Malaysian sites focus on fan-out assembly for 5G modems. Hybrid lines that blend SMT, through-hole, and advanced packaging address use cases such as high-current EV power modules, where mechanical robustness and thermal performance trump miniaturization. Collectively, these investments position the process segment as a critical profit engine within the Asia-Pacific EMS market.

By End-User: Automotive Electronics Surges Past Consumer Staples

Consumer electronics accounted for 36.78% of 2025 revenue, led by smartphones, tablets, and smart appliances. Yet automotive content is scaling faster, posting a 9.11% CAGR as battery-electric platforms push electronics spend per vehicle above USD 2,000. Advanced driver-assistance systems, high-voltage inverters, and vehicle-to-everything modules collectively redefine volume profiles and quality expectations. Industrial electronics maintain mid-single-digit growth, propelled by factory-automation drives that embed connectivity into programmable logic controllers and edge gateways. Communication equipment demand benefits from ongoing 5G rollouts and data center expansions supporting AI workloads.

Medical devices, lighting, and niche aerospace programs contribute smaller but margin-rich streams that favor EMS providers with ISO 13485 and AS9100 certifications. Automotive growth is disproportionately influencing capital-expenditure plans, with Chinese, Japanese, and Indian contractors dedicating new bays to silicon-carbide power devices and 800-volt architectures. These shifts reinforce the structural diversification of revenue inside the Asia-Pacific electronics manufacturing services market, reducing historical over-reliance on consumer-device refresh cycles.

Geography Analysis

China held 52.87% of the Asia-Pacific electronics manufacturing services market share in 2025 thanks to unmatched supplier clustering, robust logistics, and massive skilled-labor pools. Coastal provinces such as Guangdong and Jiangsu house lines for high-value automotive electronics and 5G radios, while inland hubs absorb labor-intensive consumer-device builds. The presence of 3.68 million operational 5G base stations underpins sustained board demand. Nonetheless, export-control concerns and rising wages are prompting multinationals to diversify assembly footprints, often adopting a China-plus-one playbook that shifts incremental capacity to India and Southeast Asia.

India is the region’s fastest grower, recording an 8.43% CAGR through 2031. Production-linked incentives reimburse up to 6% of incremental sales, while tariff structures shield domestic assemblers from low-cost imports. Annual output reached 330 million smartphones in 2025, illustrating the country's ascent in the Asia-Pacific electronics manufacturing services market. Dixon Technologies and Wistron are expanding into servers, wearables, and LED lighting, aided by a talent pool graduating 1.5 million engineers each year. Challenges remain around component-ecosystem depth and logistics bottlenecks, yet policy momentum continues to attract marquee investors.

Southeast Asia serves as the preferred near-shoring corridor. Vietnam attracted USD 36.6 billion in foreign direct investment in 2025, of which 28% was directed to electronics manufacturing. Samsung, Pegatron, and Luxshare ICT operate multi-product campuses in Bac Giang and Ho Chi Minh City. Thailand’s Board of Investment approved THB 82 billion (USD 2.3 billion) in electronics projects for 2025, focusing on automotive modules and medical devices. Malaysia’s Penang and Johor continue to specialize in high-mix, low-volume programs, leveraging quality systems certified to AS9100 and ISO 13485. Japan and South Korea occupy premium niches, supporting medical, defense, and high-precision semiconductor assembly under rigorous environmental and safety standards. Elsewhere, Australia and New Zealand host limited defense-electronics work, underscoring the concentration of volume in the continent’s northern arc.

Analysis of the electronics manufacturing services market by Mordor Intelligence spans multiple other regional evaluations across Europe and North America, supported by country-level insights for South Korea, Japan, Malaysia, China, Taiwan, Vietnam, and India, wherein local market conditions keep varying from one country to another.

Competitive Landscape

The Asia-Pacific electronics manufacturing services landscape shows moderate concentration, with the 10 largest providers accounting for about 55% of regional revenue in 2025. Foxconn, Pegatron, and Wistron dominate smartphone and computing lines through giant campuses and long-standing client lock-in. Flex, Jabil, and Sanmina differentiate by focusing on higher margin automotive, medical, and industrial programs that reward engineering depth and global quality systems. Chinese challengers BYD Electronics, Luxshare ICT, and Goertek are moving up the value chain by pairing proximity to domestic brands with rapid design-for-manufacturability support, while Indian contractors such as Dixon Technologies scale under production-linked incentives yet still lack deep exposure to regulated segments.

Automation and analytics now set the performance bar across leading facilities. Foxconn operates more than 100,000 industrial robots across plants in China, India, and Vietnam, using them to improve first-pass yields and reduce direct labor costs. Jabil and Pegatron deploy AI-driven defect detection on inline optical inspection tools, trimming rework rates and shortening new-product-introduction cycles. Data security has become a bid-winning criterion, pushing contractors to adopt the IPC 1791 trusted designer framework, segmented networks, and strict badge access controls.

Strategic moves in 2025 included Jabil’s USD 450 million advanced packaging plant in Penang, Pegatron’s entry into automotive battery-management systems, and Flex’s medical-device acquisition in Malaysia. These investments signal a shift toward value-added niches like fan-out wafer-level packaging, system-in-package assembly, and surgical robotics, where margins exceed those of commodity board work. Several majors are pursuing vertical integration by buying PCB fabricators, metal-stamping shops, and plastics-molding lines to secure supply and capture extra value. Smaller Vietnamese and Thai entrants are pursuing mid-volume, quick-turn IoT device programs, leveraging geographic proximity and agile engineering to offset their scale disadvantage. Taken together, these dynamics foster vigorous rivalry while raising the technical threshold for remaining relevant in the Asia-Pacific electronics manufacturing services market.

Asia-Pacific Electronics Manufacturing Services Industry Leaders

Hon Hai Precision Industry Co., Ltd.

Pegatron Corporation

Flex Ltd.

Jabil Inc.

Wistron Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Foxconn committed USD 1.2 billion to expand smartphone and wearable assembly in Tamil Nadu, India, creating 30,000 jobs and installing advanced SMT lines.

- December 2025: Pegatron secured a multi-year contract to assemble automotive battery-management systems for a European EV maker, marking its entry into 800-volt architectures.

- November 2025: Flex acquired a Malaysia-based medical-device EMS firm for USD 320 million, adding ISO 13485-certified capacity for surgical robotics.

- October 2025: Jabil opened a USD 450 million advanced packaging plant in Penang equipped for fan-out wafer-level packaging and system-in-package assembly.

Asia-Pacific Electronics Manufacturing Services Market Report Scope

The Asia-Pacific Electronics Manufacturing Services Market Report is Segmented by Service Type (Electronics Manufacturing Services, Engineering Services, Test and Development Implementation Services, Logistics Services, Other Service Types), Business Model (Contract Manufacturing (CM), Original Design Manufacturing (ODM), Hybrid / Turnkey / Other Business Models), Manufacturing Process (Surface Mount Technology (SMT), Through-Hole Technology (THT), Advanced Packaging / Hybrid Processes), End-user (Mobile Devices, Consumer Electronics, Computer, Industrial, Automotive, Communication, Lighting, Medical, Other End-users), and Geography (Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | |

| Prototyping | |

| Other Electronic Manufacturing Services | |

| Engineering Services | |

| Test and Development Implementation Services | |

| Logistics Services | |

| Other Service Types |

| Contract Manufacturing (CM) |

| Original Design Manufacturing (ODM) |

| Hybrid / Turnkey / Other Business Models |

| Surface Mount Technology (SMT) |

| Through-Hole Technology (THT) |

| Advanced Packaging / Hybrid Processes |

| Mobile Devices (Smartphones and Tablets) |

| Consumer Electronics |

| Computer (PCs/Desktop/Laptops) |

| Industrial |

| Automotive |

| Communication |

| Lighting |

| Medical |

| Other End-users |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| South-east Asia | |

| Rest of Asia-Pacific |

| By Service Type | Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | ||

| Prototyping | ||

| Other Electronic Manufacturing Services | ||

| Engineering Services | ||

| Test and Development Implementation Services | ||

| Logistics Services | ||

| Other Service Types | ||

| By Business Model | Contract Manufacturing (CM) | |

| Original Design Manufacturing (ODM) | ||

| Hybrid / Turnkey / Other Business Models | ||

| By Manufacturing Process | Surface Mount Technology (SMT) | |

| Through-Hole Technology (THT) | ||

| Advanced Packaging / Hybrid Processes | ||

| By End-user | Mobile Devices (Smartphones and Tablets) | |

| Consumer Electronics | ||

| Computer (PCs/Desktop/Laptops) | ||

| Industrial | ||

| Automotive | ||

| Communication | ||

| Lighting | ||

| Medical | ||

| Other End-users | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| South Korea | ||

| India | ||

| South-east Asia | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

How large is the Asia-Pacific electronics manufacturing services market in 2026?

The market stands at USD 416.03 billion in 2026 and is forecast to grow to USD 592.38 billion by 2031.

Which segment is expanding fastest inside the market?

Automotive electronics leads growth, advancing at a 9.11% CAGR as electric-vehicle production scales.

Why are hybrid and turnkey business models gaining popularity?

OEMs prefer single-accountability partners that combine design, sourcing, and assembly, driving hybrid and turnkey models to a 7.94% CAGR.

Which geography shows the highest growth rate?

India records the fastest trajectory at an 8.43% CAGR, propelled by production-linked incentives and competitive labor costs.

What drives investment in advanced packaging lines?

The shift to chiplet architectures and heterogeneous integration requires fan-out wafer-level packaging and system-in-package assembly, expanding that process segment at an 8.01% CAGR.

How are EMS firms addressing margin pressure?

Leading contractors deploy automation, vertical integration, and AI-based yield analytics to counter annual price-down clauses and compressed gross margins.

Page last updated on: