Asia-Pacific Electric Vehicle Battery Manufacturing Equipment Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

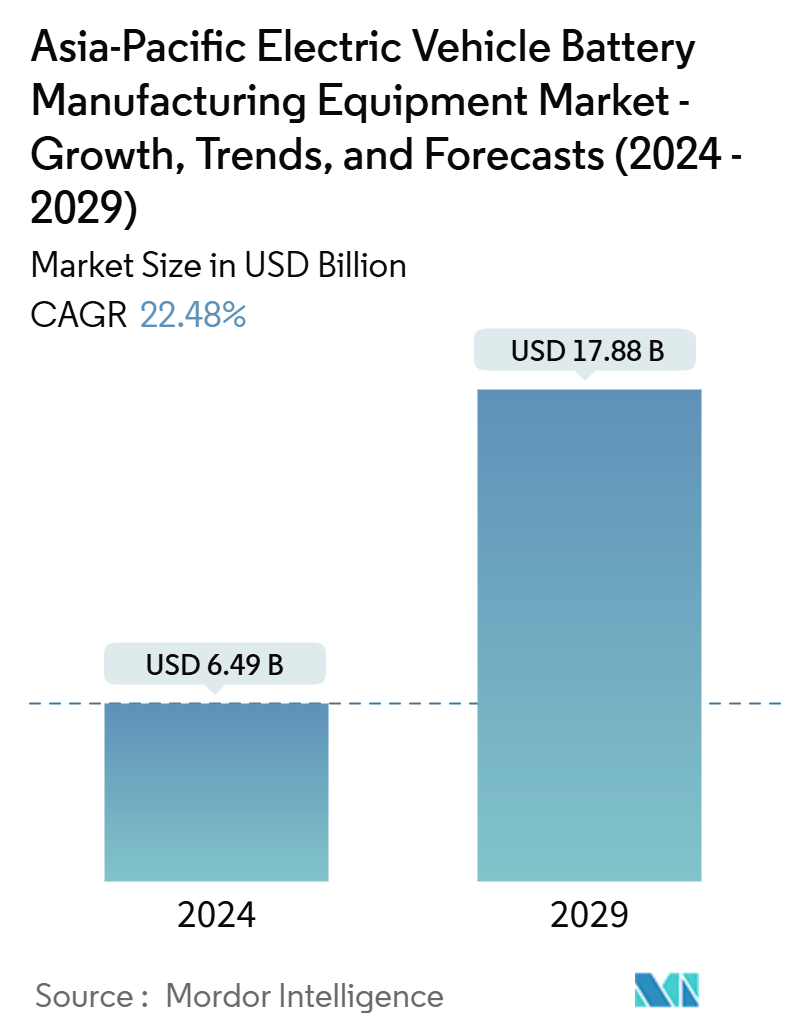

| Market Size (2024) | USD 6.49 Billion |

| Market Size (2029) | USD 17.88 Billion |

| CAGR (2024 - 2029) | 22.48 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Asia-Pacific Electric Vehicle Battery Manufacturing Equipment Market Analysis

The Asia-Pacific Electric Vehicle Battery Manufacturing Equipment Market - Growth, Trends, And Forecasts Industry is expected to grow from USD 6.49 billion in 2024 to USD 17.88 billion by 2029, at a CAGR of 22.48% during the forecast period (2024-2029).

- Over the medium term, the growing adoption of electric vehicles (EV) and supportive government initiatives and investments towards EV battery manufacturing are expected to drive the demand for the Asia-Pacific electric vehicle battery manufacturing equipment market during the forecast period.

- On the other hand, the requirement of high initial investments and setup costs are expected to hinder the market's growth during the forecast period.

- Nevertheless, the expansion of local EV battery production is expected to create vast opportunities for the Asia-Pacific electric vehicle battery manufacturing equipment market in the future.

- Among all the countries in the region, India is expected to have significant growth in the electric vehicle battery manufacturing industry during the forecast period.

Asia-Pacific Electric Vehicle Battery Manufacturing Equipment Market Trends

Lithium-ion Battery to be the Fastest Growing

- Lithium-ion (Li-ion) batteries have transformed the electric vehicle (EV) industry, spurring notable advancements in battery manufacturing across the Asia-Pacific region. Their high energy density, long cycle life, and rapid charging capabilities have solidified their dominance in the EV market.

- What distinguishes lithium-ion batteries is their superior capacity-to-weight ratio. Even though they come at a premium, top players in the Asia-Pacific are channeling investments into R&D and ramping up production. This surge in activity is intensifying competition and driving prices down, broadening the accessibility of lithium-ion batteries.

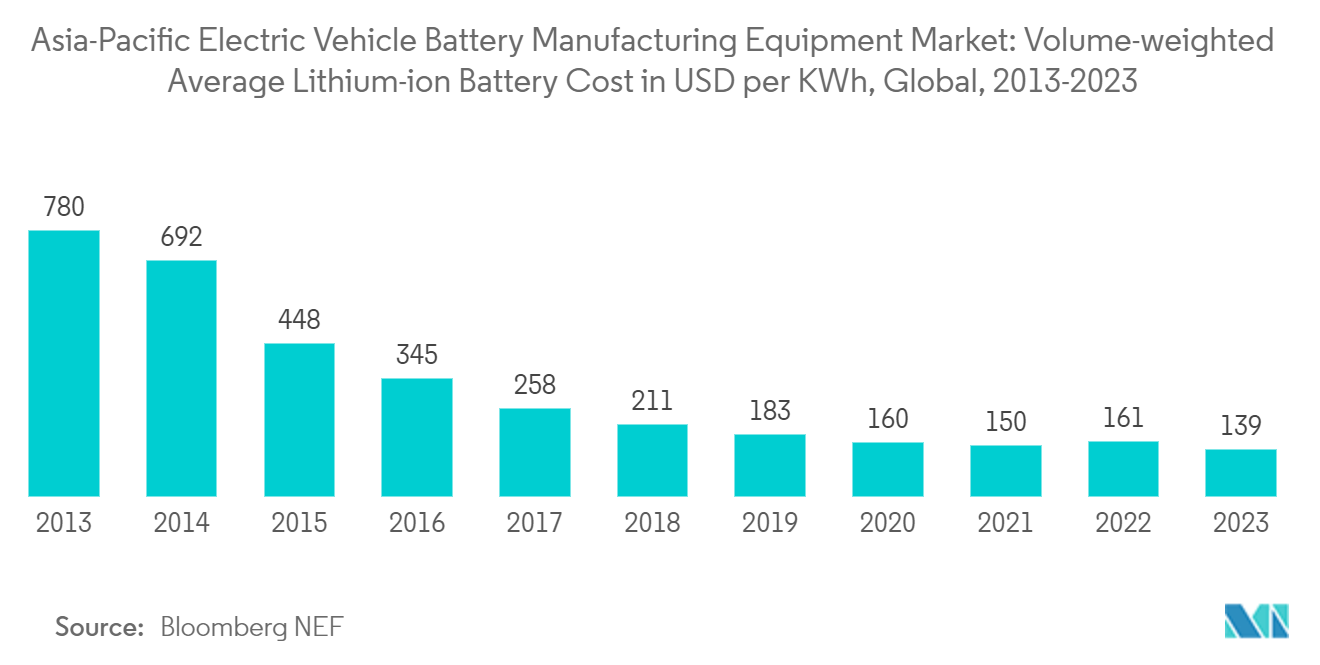

- In 2023, the average price of EV battery packs fell to USD 139/kWh, marking a significant 13% drop. Projections indicate this downward momentum will persist, with prices anticipated to reach USD 113/kWh by 2025 and plummet further to USD 80/kWh by 2030. These price reductions, spurred by advancements in technology and manufacturing, are likely to amplify the demand for specialized manufacturing equipment for lithium-ion batteries in the region.

- Asia-Pacific governments are actively championing the electric vehicle movement and bolstering lithium-ion battery production through favorable policies and incentives. Central to these initiatives is R&D, particularly in identifying cost-effective material substitutes for expensive components like cobalt. This strategy not only reduces manufacturing expenses but also strengthens a sustainable supply chain, heightening the demand for cutting-edge manufacturing tools.

- For instance, in May 2024, China announced a substantial investment of approximately CNY 6 billion (USD 845 million) aimed at pioneering next-generation battery technologies for EVs, including solid-state batteries. Given their enhanced energy density and safety over traditional lithium-ion batteries, these innovations are poised to drive up the demand for advanced manufacturing equipment in the region.

- Furthermore, in December 2023, South Korea’s Ministry of Finance committed KRW 38 trillion (~USD 28.5 billion) in policy financing to the lithium battery sector over the next five years, with official rollout set for 2024. Their strategy encompasses a KRW 1 trillion (~USD 750 million) promotion fund for the lithium battery industry, a KRW 73.6 billion (~USD 55.2 million) R&D investment, and strengthening critical mineral reserves for local battery production. These moves, alongside efforts to cultivate a battery reuse and recycling ecosystem, are set to energize the lithium-ion battery sector and, consequently, the market for EV battery manufacturing equipment.

- Additionally, the rising appetite for lithium-ion batteries has catalyzed the emergence of Gigafactories throughout the Asia-Pacific. These colossal production hubs play a crucial role in ensuring a steady supply of battery cells to cater to the surging EV demand. Key players in the region are embarking on multiple projects, positioning themselves for a flourishing EV battery market.

- As an illustration, in February 2024, BMW announced its plans for an EV battery factory in Rayong, Thailand, with ambitions to establish the country as a key export center for Asia-Pacific's EV batteries. Given the facility's aggressive targets for lithium-ion battery production, this venture is bound to stimulate demand for state-of-the-art manufacturing tools.

- With these advancements, lithium-ion battery production capacity is on the rise, driving the need for sophisticated EV battery manufacturing tools. The continuous expansion of production facilities and the adoption of cutting-edge technologies are crucial in shaping the future of the Asia-Pacific EV battery manufacturing equipment landscape.

India To Witness Significant Growth

- India's electric vehicle (EV) battery manufacturing industry is rapidly expanding as the nation embraces greener mobility solutions. This growth is fueled by government initiatives, surging demand for electric vehicles, and substantial investments from both domestic and international entities.

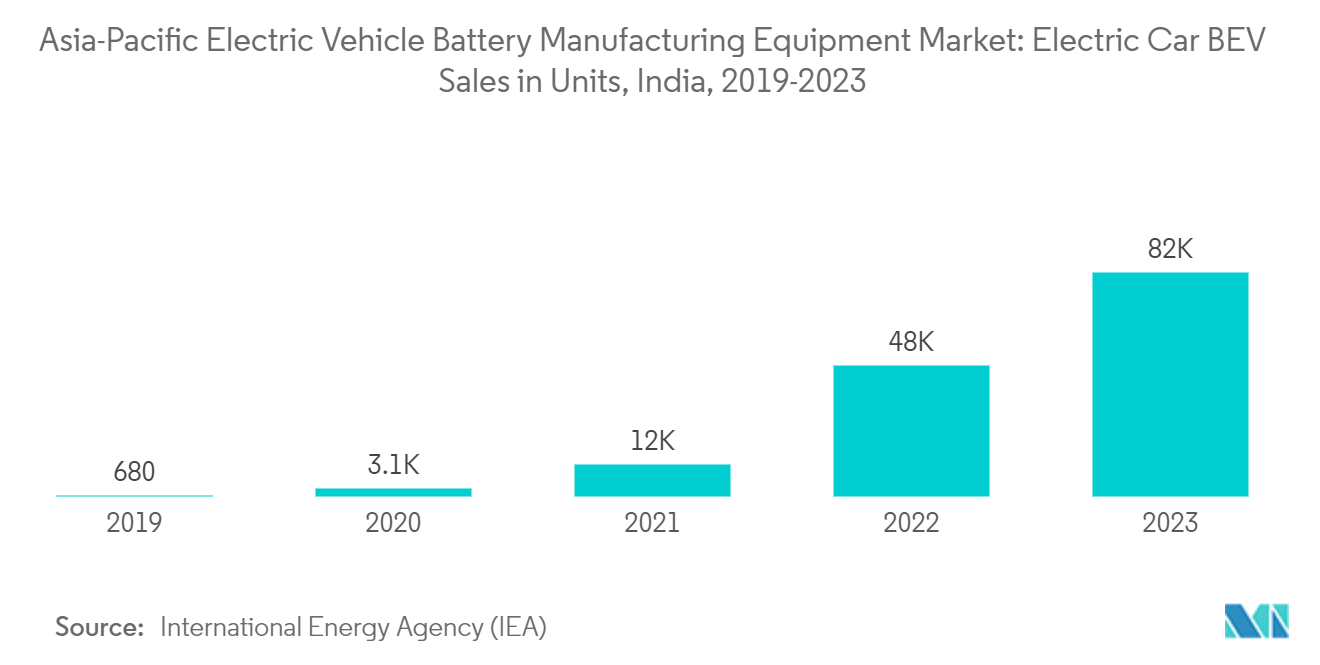

- As India pivots towards clean energy, the emphasis on electric vehicles has become paramount for numerous companies. EV sales in the region have surged dramatically. For example, the International Energy Agency (IEA) reported that battery electric vehicle (BEV) sales in India hit approximately 82,000 units in 2023, marking a staggering 70% increase from 2022. With such a robust uptick in EV adoption, the demand for EV battery manufacturing is poised to skyrocket. Furthermore, the Indian Government has set ambitious targets for 2030: aiming for 30% of newly registered private cars, 40% of buses, 70% of commercial vehicles, and a striking 80% of two-wheelers and three-wheelers to be electric. Such targets underscore a burgeoning demand for batteries, especially lithium-ion, and signal a thriving market for EV battery manufacturing and related production equipment.

- India has emerged as a magnet for investments in EV battery manufacturing, attracting both domestic and international players. This capital influx is strategically aimed at strengthening the nation's electric vehicle infrastructure, curbing reliance on fossil fuels, and championing sustainable transportation. Bolstered by supportive government policies and incentives, these investments are cementing India's stature in the global EV arena.

- For instance, in July 2024, Ola Electric unveiled a USD 100 million investment for the initial phase of its gigafactory in Tamil Nadu, India. This facility is set to produce indigenous lithium-ion batteries. Ola Electric plans to transition to its battery cells for its electric vehicles by early next year, moving away from current imports from Korea and China. Such moves are set to catalyze a surge in battery production equipment demand in the coming years.

- Moreover, the Indian government has rolled out a suite of initiatives to amplify electric vehicle (EV) adoption and stimulate local battery manufacturing. These measures encompass subsidies for EV purchasers, tax breaks for manufacturers, and bolstered investments in charging infrastructure.

- As an illustration, in 2023, the Indian government reiterated its ambitious targets: 30% of private cars, 70% of commercial vehicles, and 80% of two and three-wheelers are to be electric by 2030. Additionally, the government has introduced subsidy incentives ranging from INR 10,000 per kWh (USD 120) to INR 15,000 per kWh (USD 180). These concerted efforts are set to not only boost EV production and sales but also amplify the demand for battery manufacturing and related equipment.

- In early 2022, industry giant Exide Industries unveiled plans for a USD 718 million investment to establish a lithium-ion cell manufacturing plant in Karnataka. The facility, starting with a 6 GWh capacity, is slated to commence operations by 2024, with ambitions to double its capacity to 12 GWh in subsequent years.

- In April 2023, Log9 Materials, a battery technology startup, inaugurated India's maiden lithium-ion cell manufacturing facility in Jakkur, Bengaluru. Starting with a 50 MWh capacity, Log9 is eyeing an ambitious expansion to 1 GWh for cell manufacturing and 2 GWh for battery packs by Q1 2025. Such developments are fueling a robust demand for EV battery manufacturing equipment in India.

- Given these dynamics, India is poised to emerge as a significant market for EV battery manufacturing equipment in the coming years.

Asia-Pacific Electric Vehicle Battery Manufacturing Equipment Industry Overview

The Asia-Pacific Electric Vehicle Battery Manufacturing Equipment market is semi-fragmented. Some of the key players in the market (not in any particular order) include Hitachi Ltd., Duerr AG, Schuler AG, Komatsu NTC Ltd., and Wuxi Lead Intelligent Equipment Co Ltd.

Asia-Pacific Electric Vehicle Battery Manufacturing Equipment Market Leaders

-

Hitachi Ltd.

-

Duerr AG

-

Schuler AG

-

Komatsu NTC Ltd.

-

Wuxi Lead Intelligent Equipment Co Ltd.

*Disclaimer: Major Players sorted in no particular order

Asia-Pacific Electric Vehicle Battery Manufacturing Equipment Market News

- March 2024: Indian Oil Corporation Ltd (IOCL), a state-owned entity, has teamed up with Japan's Panasonic Energy to manufacture cylindrical lithium-ion cells in India. After signing a head of agreement in January 2024, the two companies have finalized a binding term sheet, outlining the framework for their joint venture. A head of agreement is a non-binding document that underscores key issues related to a potential sale, partnership, or other agreements. At present, both companies are delving into the significance of battery technology in India's transition to clean energy.

- February 2024: In a strategic move, JSW Group, in partnership with MG Motor India, is set to establish electric vehicle and battery manufacturing projects in Odisha. The ambitious project comes with a hefty price tag of approximately INR 400 billion (USD 4.82 billion). This endeavor is poised to amplify the demand for battery manufacturing equipment.

Asia-Pacific Electric Vehicle Battery Manufacturing Equipment Market Report - Table of Contents

1. INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2. EXECUTIVE SUMMARY

3. RESEARCH METHODOLOGY

4. MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Growing Adoption of Eelectric Vehicles

4.5.1.2 Supportive Government Policies and Investments Towards EV Battery Manufacturing

4.5.2 Restraints

4.5.2.1 Requirement of High Initial Investments and Setup Costs

4.6 Supply Chain Analysis

4.7 Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

4.8 Investment Analysis

5. MARKET SEGMENTATION

5.1 Process

5.1.1 Mixing

5.1.2 Coating

5.1.3 Calendering

5.1.4 Slitting and Electrode Making

5.1.5 Other Process

5.2 Battery

5.2.1 Lithium-ion Battery

5.2.2 Lead-acid Battery

5.2.3 Nickel Metal Hydride Battery

5.2.4 Other Batteries

5.3 Geography

5.3.1 China

5.3.2 India

5.3.3 Japan

5.3.4 South Korea

5.3.5 Malaysia

5.3.6 Thailand

5.3.7 Indonesia

5.3.8 Vietnam

5.3.9 Rest of Asia-Pacific

6. COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 Duerr AG

6.3.2 Hitachi Ltd.

6.3.3 Schuler AG

6.3.4 Wuxi Lead Intelligent Equipment Co Ltd

6.3.5 Xiamen Tmax Battery Equipments Limited

6.3.6 Xiamen TOB New Energy Technology Co., Ltd.

6.3.7 TC Machinery Co., Ltd.

6.3.8 Komatsu NTC Ltd.

6.3.9 Shenzhen Yinghe Technology Co.,Ltd.

6.3.10 Xiamen Lith Machine Limited

- *List Not Exhaustive

6.4 List of Other Prominent Companies

6.5 Market Ranking Analysis

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Expansion of Local EV Battery Production

Asia-Pacific Electric Vehicle Battery Manufacturing Equipment Industry Segmentation

- EV battery manufacturing equipment refers to the machinery and tools essential for producing batteries tailored for electric vehicles. This encompasses equipment for material handling, electrode production, cell assembly, electrolyte filling, and processes like formation and aging. Key components include specialized machines for coating, drying, and pressing electrodes, as well as equipment for stacking or winding cells. Besides, advanced testing and quality control systems are in place to guarantee that the batteries adhere to stringent safety and performance standards.

- The Asia-Pacific electric vehicle battery manufacturing equipment market is segmented into Process, Battery, and Geography. By process, the market is segmented into mixing, coating, calendaring, slitting and electrode making and other process). By battery, the market is segmented into lithium-ion battery, lead-acid battery, nickel metal hydride battery and other batteries. The report also covers the market size and forecasts for the Asia-Pacific electric vehicle battery manufacturing equipment market across major countries. The report offers the market size and forecasts for the market in revenue (USD) for all the above segments.

| Process | |

| Mixing | |

| Coating | |

| Calendering | |

| Slitting and Electrode Making | |

| Other Process |

| Battery | |

| Lithium-ion Battery | |

| Lead-acid Battery | |

| Nickel Metal Hydride Battery | |

| Other Batteries |

| Geography | |

| China | |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific |

Asia-Pacific Electric Vehicle Battery Manufacturing Equipment Market Research Faqs

How big is the Asia-Pacific Electric Vehicle Battery Manufacturing Equipment Market?

The Asia-Pacific Electric Vehicle Battery Manufacturing Equipment Market size is expected to reach USD 6.49 billion in 2024 and grow at a CAGR of 22.48% to reach USD 17.88 billion by 2029.

What is the current Asia-Pacific Electric Vehicle Battery Manufacturing Equipment Market size?

In 2024, the Asia-Pacific Electric Vehicle Battery Manufacturing Equipment Market size is expected to reach USD 6.49 billion.

Who are the key players in Asia-Pacific Electric Vehicle Battery Manufacturing Equipment Market?

Hitachi Ltd., Duerr AG, Schuler AG, Komatsu NTC Ltd. and Wuxi Lead Intelligent Equipment Co Ltd. are the major companies operating in the Asia-Pacific Electric Vehicle Battery Manufacturing Equipment Market.

What years does this Asia-Pacific Electric Vehicle Battery Manufacturing Equipment Market cover, and what was the market size in 2023?

In 2023, the Asia-Pacific Electric Vehicle Battery Manufacturing Equipment Market size was estimated at USD 5.03 billion. The report covers the Asia-Pacific Electric Vehicle Battery Manufacturing Equipment Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Asia-Pacific Electric Vehicle Battery Manufacturing Equipment Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Asia-Pacific Electric Vehicle Battery Manufacturing Equipment Industry Report

Statistics for the 2024 Asia-Pacific Electric Vehicle Battery Manufacturing Equipment market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Asia-Pacific Electric Vehicle Battery Manufacturing Equipment analysis includes a market forecast outlook for 2024 to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.