Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

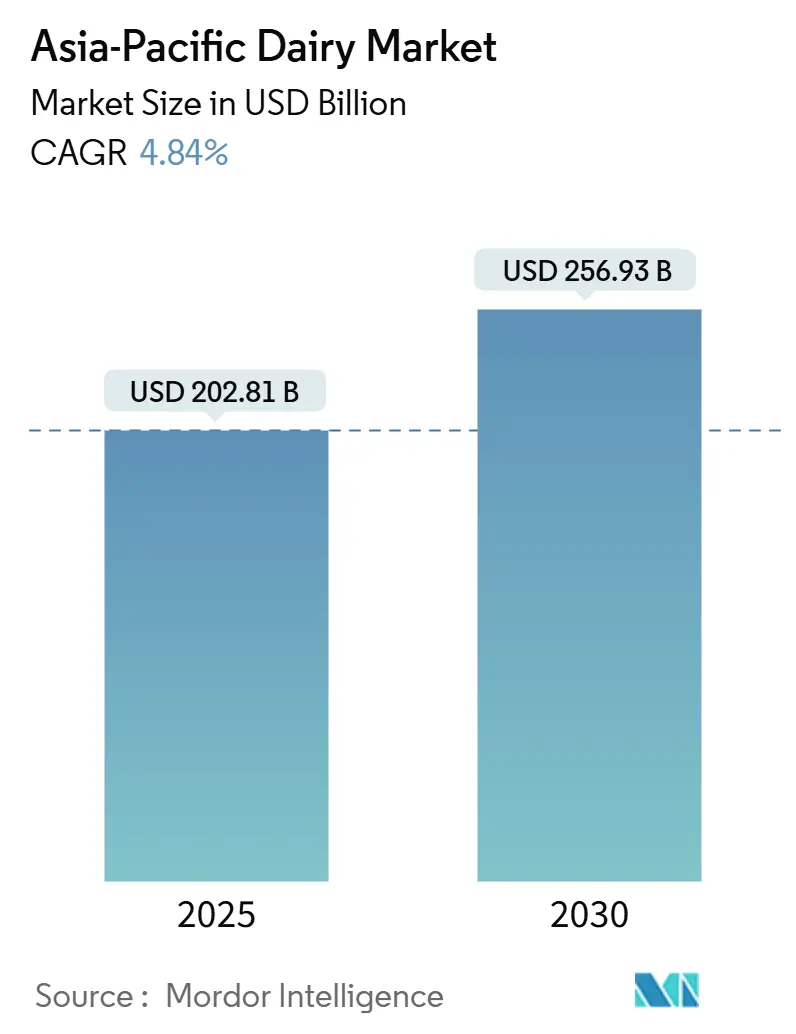

| Market Size (2025) | USD 202.81 Billion |

| Market Size (2030) | USD 256.93 Billion |

| Growth Rate (2025 - 2030) | 4.84% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Dairy Market Analysis by Mordor Intelligence

The Asia-Pacific dairy market size is estimated at USD 202.81 billion in 2025, and is expected to reach USD 256.93 billion by 2030, at a CAGR of 4.84% during the forecast period (2025-2030). This trajectory reflects structural shifts rather than simple volume accumulation, urbanization in China pushed per capita dairy consumption from 36.1 kg in 2019 to 42.3 kg by 2024, while India's production base swelled to 230 million tonnes in 2024, cementing its position as the world's largest milk producer[1]Source: National Dairy Development Board, "ABOUT NDDB", nddb.coop. The region's growth diverges sharply from mature Western markets, where incremental gains hinge on premiumization; here, first-time adoption and category expansion drive the bulk of revenue. Category migration from plain milk to value-added offerings such as drinkable yogurt, lactose-free UHT milk, and high-protein whey concentrates improves average selling prices and cushions producers against input-cost volatility. Meanwhile, omnichannel distribution, particularly e-commerce with temperature-controlled last-mile delivery, converts previously latent demand into repeat purchases. Competitive intensity remains balanced, allowing both cooperatives and multinationals to invest in premium SKUs without triggering destructive price wars.

Key Report Takeaways

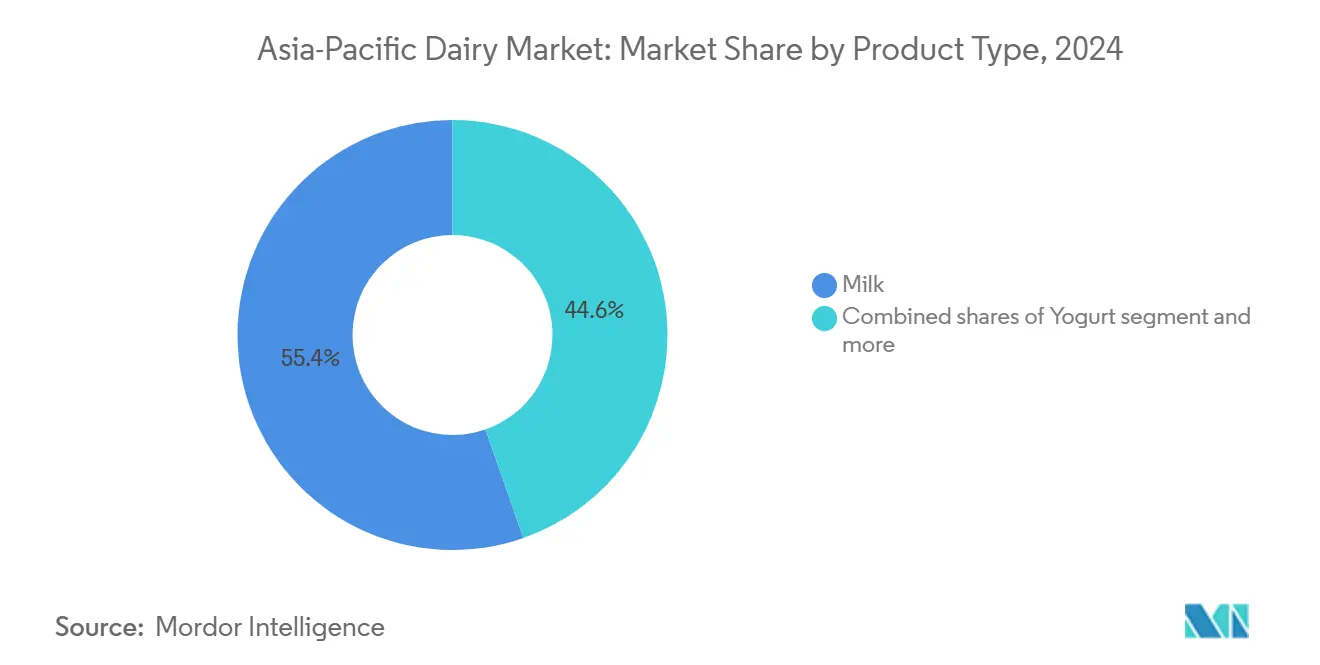

- By product type, milk commanded 55.36% of the Asia-Pacific dairy market share in 2024, while yogurt recorded the fastest 5.77% CAGR through 2030.

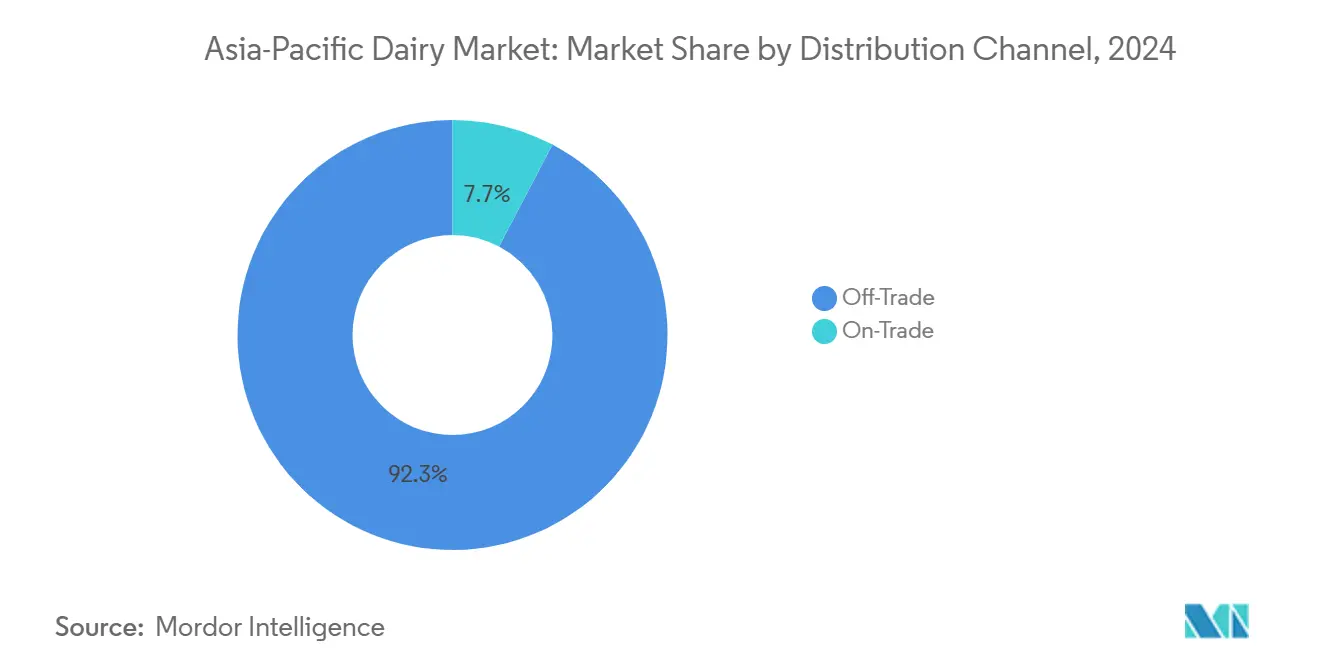

- By distribution channel, off-trade outlets held 92.31% revenue share of the Asia-Pacific dairy market size in 2024, whereas on-trade sales are advancing at a 5.18% CAGR to 2030.

- By geography, India contributed 53.22% of 2024 value, yet China is projected to post a 6.46% CAGR, the highest among major markets.

Asia-Pacific Dairy Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Processing innovation expands sector into high-value categories | +0.8% | China, India, Southeast Asia | Medium term (2-4 years) |

| Organized promotions drive nutritional awareness and sales | +0.7% | India, China, Indonesia | Short term (≤ 2 years) |

| Dairy acceptance achieves widespread staple food status | +0.9% | India, China, Vietnam | Long term (≥ 4 years) |

| Modern retail enhances product accessibility and choice | +0.8% | Urban centers across APAC (Asia-Pacific) | Medium term (2-4 years) |

| Urbanization facilitates lifestyle westernization trends | +0.9% | China, India, Indonesia, Vietnam | Long term (≥ 4 years) |

| Reduced trade barriers enable foreign market entry | +0.5% | ASEAN, India, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Processing Innovation Expands Sector into High-Value Categories

Aseptic packaging and enzyme engineering have unlocked categories once deemed impractical for tropical climates. Tetra Pak's 2024 mascarpone technology extends shelf life to 8 months without refrigeration, enabling Italian-style desserts to reach Indonesian and Philippine markets where cold chains remain patchy. China's Yili introduced lactose-free UHT milk using microbial lactase in 2024, capturing consumers who previously avoided dairy altogether. Membrane filtration now concentrates whey protein to 80% purity at scale, feeding the sports-nutrition boom in Japan and South Korea. These advances do more than preserve product, they redefine what counts as "dairy" in regions where traditional fermentation and fresh consumption dominated for centuries.

Organized Promotions Drive Nutritional Awareness and Sales

Government-backed campaigns and corporate nutrition initiatives are reshaping consumption norms. India's National Dairy Development Board launched school milk programs reaching 12 million children in 2024, embedding dairy as a daily staple rather than a luxury. Nestlé India's "Nestle a+ Nourish" campaign tied fortified milk to cognitive development, leveraging pediatrician endorsements to shift middle-class purchasing. In Vietnam, Vinamilk's partnerships with maternal health clinics positioned yogurt as essential prenatal nutrition, lifting sales in provinces where dairy was historically absent. These efforts work because they address skepticism head-on, many Asian consumers still associate milk with childhood or illness recovery, not adult wellness.

Dairy Acceptance Achieves Widespread Staple Food Status

Dairy's integration into daily diets marks a departure from episodic consumption. India's per capita intake reached 459 grams per day in 2024, surpassing eggs and approaching global norms, while China's urbanization drove consumption from 36.1 kg in 2019 to 42.3 kg by 2024. This shift is structural, not cyclical, breakfast cereal penetration, café culture, and Western fast-food chains normalize milk, yogurt, and cheese as meal components rather than standalone treats. Vietnam's dairy cooperative model, which aggregates smallholder output and guarantees prices, has stabilized supply enough that retailers now stock fresh milk year-round, a feat unthinkable a decade ago. The psychological transition from "foreign food" to "everyday staple" underpins long-term volume growth.

Modern Retail Enhances Product Accessibility and Choice

Supermarkets and e-commerce platforms have dismantled distribution bottlenecks that once confined dairy to urban elites. China's Hema Fresh stores, operated by Alibaba, use real-time inventory systems to restock yogurt within 2 hours, reducing spoilage and enabling SKU proliferation, shoppers in Shenzhen can choose from 47 yogurt variants, up from 12 in traditional grocers. India's Reliance Retail expanded its chilled dairy footprint to 1,200 stores in 2024, bringing branded cheese and butter to tier-2 cities where mom-and-pop shops lacked refrigeration. Online platforms like BigBasket and JD.com now handle temperature-controlled last-mile delivery, making premium imports accessible beyond metro cores. This infrastructure shift matters because it converts latent demand, consumers who wanted dairy but couldn't reliably source it, into realized sales.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lactose intolerance restricts inherent market penetration | -0.6% | East Asia, South Asia, Southeast Asia | Long term (≥ 4 years) |

| Varying regulatory measures generate substantial trade friction | -0.4% | ASEAN, India, China | Medium term (2-4 years) |

| Supply chain maturity challenged by rapid demand pace | -0.5% | India, Indonesia, Vietnam | Medium term (2-4 years) |

| Underdeveloped cold chain hinders product quality maintenance | -0.5% | India, Indonesia, Philippines | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lactose Intolerance Restricts Inherent Market Penetration

Genetic prevalence of lactase non-persistence caps addressable populations, 90% of East Asians, 70% of South Asians, and 60% of Southeast Asians experience discomfort from unmodified dairy [2]Source: International Dairy Federation, "World Dairy Situation Report", fil-idf.org. While enzyme-treated milk and plant-dairy blends offer workarounds, they fragment the market and dilute brand equity; a consumer who switches to oat milk exits the dairy value chain entirely. Japan's aging demographic exacerbates the issue, as lactase production declines further with age, pushing seniors toward calcium-fortified alternatives. Companies must invest in reformulation pipelines and consumer education, costs that erode margins without guaranteeing conversion. The constraint is biological, not behavioral, making it harder to overcome through marketing alone.

Varying Regulatory Measures Generate Substantial Trade Friction

Divergent food-safety standards and import protocols force multinationals to operate parallel supply chains. India's FSSAI mandates specific fat percentages for "cheese," disqualifying European PDO variants that use different milk blends, while China's CFDA requires re-registration for every formulation tweak, delaying launches by 18 months [3]Source: FSSAI, " Mandates on specific fat percentages", fssai.gov.in. ASEAN's mutual recognition agreements remain incomplete, so a yogurt approved in Thailand may still face lab testing in Indonesia. These frictions explain why Fonterra chose to expand its New Zealand UHT cream plant rather than build in Southeast Asia, centralized production under a single regulatory regime reduces compliance overhead, even if it adds shipping costs. Harmonization efforts under RCEP may ease barriers by 2028, but until then, regulatory arbitrage favors incumbents with local lobbying power.

Segment Analysis

By Product Type: Yogurt Outpaces Traditional Milk in Growth

Milk captured 55.36% of product-type value in 2024, anchored by India's vast liquid consumption and China's UHT dominance, yet yogurt's 5.77% CAGR through 2030 signals a premiumization wave. Probiotic strains like Lactobacillus casei and Bifidobacterium lactis have transformed yogurt from a niche health food into a functional beverage, with drinkable formats accounting significant share of China's yogurt sales in 2024. Cheese remains underpenetrated, processed variants hold a significant share of retail cheese sales, reflecting limited culinary integration outside pizza and sandwiches, but foodservice demand is surging, with the majority of China's cheese consumption now occurring in restaurants and quick-service outlets, according to the China Dairy Industry Association. Butter and cream categories grow steadily as bakery chains proliferate, though import dependence persists due to insufficient domestic butterfat supply.

Dairy desserts, led by ice cream, benefit from year-round consumption in tropical climates, with premium single-serve formats gaining traction in convenience stores. Sour milk drinks, traditional in Central Asia, are being repositioned as gut-health beverages in urban China, leveraging kefir and kumis heritage. Condensed and powdered milk serve as pantry staples in rural areas lacking refrigeration, though fresh and UHT variants are gradually displacing them as cold chains extend. Emerging innovations blur category boundaries, Mengniu's 2024 launch of a yogurt-cheese hybrid targets consumers seeking protein density without cooking effort, while flavored milk now includes turmeric and matcha variants tailored to local palates. The shift from commodity milk to value-added formats is irreversible; companies that cling to plain white milk will cede margin to those engineering functional, convenient, and culturally resonant products. Regulatory oversight by FSSAI in India and CFDA in China ensures product safety but also raises entry barriers, as compliance costs favor scale players with in-house testing labs.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: On-Trade Gains as Cafés and QSRs Multiply

Off-trade channels commanded 92.31% of distribution share in 2024, driven by supermarkets, hypermarkets, and e-commerce platforms that offer refrigeration, variety, and price transparency. Yet on-trade's 5.18% CAGR through 2030 reflects structural changes in how Asians consume dairy, coffee shops, bubble tea outlets, and quick-service restaurants now serve as primary touchpoints for younger cohorts. Starbucks China sources 180,000 tonnes of milk annually, introducing millions to lattes and cappuccinos who previously drank tea exclusively. Convenience stores like 7-Eleven and FamilyMart stock chilled yogurt and flavored milk at checkout, converting impulse purchases into habitual consumption. Online retail, a subset of off-trade, grew in 2024 as platforms like JD.com and BigBasket solved last-mile cold-chain logistics, enabling premium imports to reach tier-3 cities.

Specialist retailers, organic grocers, and health-food chains remain niche but influential, curating artisanal cheeses and probiotic yogurts that set quality benchmarks. Warehouse clubs like Metro Cash & Carry cater to foodservice buyers, offering bulk formats that undercut traditional distributors. The on-trade surge matters strategically because it embeds dairy into social rituals, meeting friends at a café, grabbing a smoothie post-gym, rather than relegating it to home consumption. This stickiness insulates demand from economic downturns; consumers may skip a grocery trip but rarely forego their morning coffee. Distribution strategy increasingly hinges on omnichannel integration, where QR codes on retail packs unlock recipes or loyalty points, blurring the line between off-trade purchase and on-trade experience.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

India accounted for 53.22% of the regional market value in 2024, a dominance rooted in both production scale, 230 million tonnes annually, and consumption breadth, with dairy embedded in cuisine, religion, and daily nutrition. The cooperative model pioneered by Amul aggregates 3.6 million smallholder farmers, ensuring stable procurement and rural income, while private players like Nestlé India and Danone leverage branded value-added products to capture urban premiums. Per capita consumption of 459 grams per day in 2024 still trails global averages, suggesting headroom for growth as incomes rise and cold chains penetrate deeper into rural hinterlands. Government initiatives under the National Dairy Plan aim to boost productivity through genetic improvement and feed optimization, targeting 300 million tonnes by 2030. India's challenge lies in fragmentation, over 70% of milk bypasses formal processing, limiting quality control and traceability, though FSSAI's tightening standards are gradually formalizing the sector.

China's 6.46% CAGR through 2030 makes it the fastest-growing major geography, propelled by urbanization, 65% of the population now lives in cities, and rising disposable incomes that enable premiumization. Domestic production reached 41 million tonnes in 2024, yet imports remain substantial, particularly for cheese, butter, and infant formula, reflecting quality perceptions and supply gaps. China's dairy belt in Inner Mongolia and Heilongjiang provinces benefits from mechanized farming and genetics, China Shengmu imported 8,100 Australian Holstein cows in 2024 to upgrade herd quality. The government's push for self-sufficiency, driven by food-security concerns, is spurring investments in large-scale farms and processing infrastructure, though environmental constraints around water and land use may cap expansion.

Japan and Australia represent mature, high-value markets where growth hinges on innovation rather than volume. Japan's aging population and stagnant birth rates compress demand, yet functional dairy, probiotic yogurts, calcium-fortified milk, commands premium pricing, with Meiji and Morinaga leading in R&D intensity. Australia's dairy sector is export-oriented, with AUD 3.2 billion (USD 2.1 billion) in shipments in 2024, primarily to China and Southeast Asia, though drought and labor shortages constrain production according to Dairy Australia. Rest of Asia-Pacific, encompassing Vietnam, Indonesia, Thailand, and the Philippines, exhibits the highest growth potential, driven by young demographics and low baseline consumption. Vietnam's TH Group is constructing a 10,000-hectare dairy farm in Indonesia with 1.8 million tonnes annual capacity, signaling confidence in regional demand. However, infrastructure deficits and regulatory inconsistencies remain binding constraints, requiring patient capital and local partnerships to navigate.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

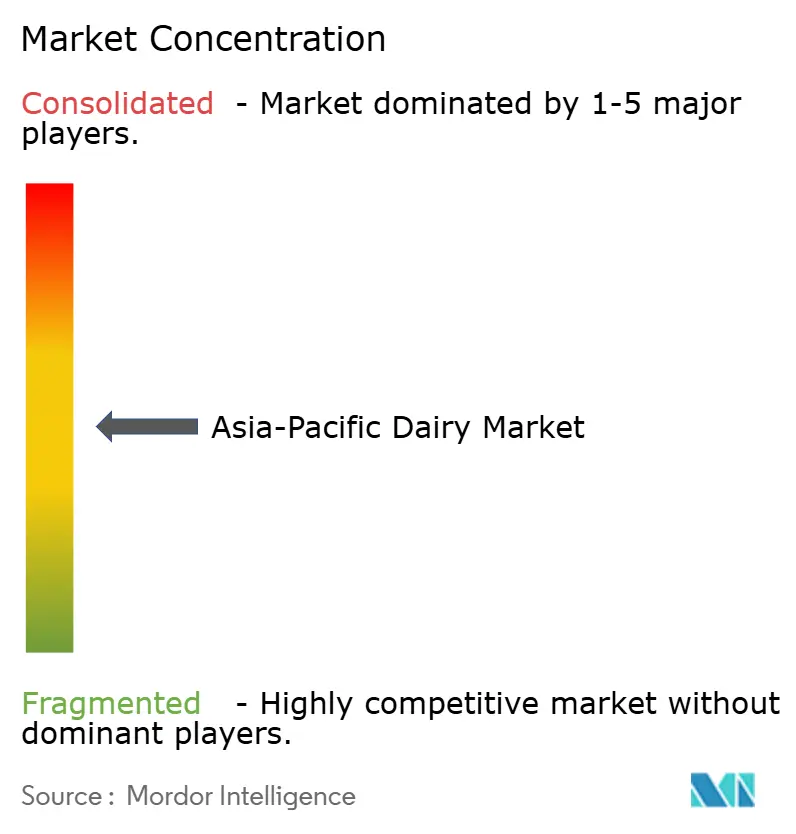

The Asia-Pacific Dairy Market exhibits moderate concentration, indicating a balance between dominant incumbents and agile challengers. Cooperatives like Amul and Fonterra wield structural advantages, farmer networks that ensure raw-milk supply and brand equity built over decades, while multinationals such as Nestlé, Danone, and FrieslandCampina leverage global R&D pipelines and premium positioning. Major market players include Gujarat Co-operative Milk Marketing Federation Ltd, Fonterra Co‑operative Group Limited, Inner Mongolia Mengniu Dairy (Group) Co., Ltd. (Mengniu), Nestlé S.A., and Danone S.A., among others.

Chinese giants Yili and Mengniu have scaled aggressively, with Mengniu's acquisition of Bellamy's Organic for AUD 1.5 billion (USD 1.0 billion) in 2019 securing a foothold in infant formula, a category where trust and traceability command outsized margins. Strategy patterns cluster around three axes: geographic expansion into underpenetrated markets, premiumization through functional ingredients, and vertical integration to control quality from farm to shelf. Opportunities abound in categories like cheese and butter, where per capita consumption remains a fraction of Western levels, and in distribution channels like e-commerce and on-trade, where first-mover advantages persist.

Emerging disruptors include plant-dairy hybrids and enzyme-treated variants that address lactose intolerance without sacrificing taste, as well as direct-to-consumer brands bypassing traditional retail. Technology adoption is accelerating, Fonterra's digital traceability platform, launched in 2024, uses blockchain to verify milk provenance, appealing to quality-conscious Chinese consumers. Regulatory compliance remains a competitive moat; companies with ISO 22000 certification and FSSAI approvals can command shelf space and price premiums that smaller players cannot match. The sector's trajectory favors those who balance scale efficiencies with localized innovation, as homogeneous global brands struggle against regional tastes and purchasing power disparities.

Asia-Pacific Dairy Industry Leaders

-

Gujarat Co-operative Milk Marketing Federation Ltd

-

Fonterra Co‑operative Group Limited

-

Inner Mongolia Mengniu Dairy (Group) Co., Ltd. (Mengniu)

-

Nestlé S.A.

-

Danone S.A.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- August 2025: Meiji, a dairy manufacturer, launched a Spreadable Matured Cheese Blend as an addition to its line of spreadable butters, expanding its product offerings. This product followed the company’s introduction of the milk beverage, Meiji Eye and Sleep W, which was designed to support eye accommodation and enhance sleep quality through its innovative formulation.

- June 2025: France’s No. 1 frozen yogurt brand, Yogurt Factory, officially announced its entry into the Indian market through a strategic partnership with FranGlobal, the international business arm of Franchise India. Yogurt Factory aimed to revolutionize the Indian dessert landscape with its 0% fat, 100% gourmet frozen yogurt and an extensive range of smoothies, milkshakes, waffles, and bubble teas.

- April 2025: In a defining moment for India’s premium dairy segment, Britannia Industries Ltd officially launched its much-anticipated Greek yogurt range, marking a significant step forward in the brand’s innovation journey. Behind the polished packaging and market-ready product lay a story of ambition, collaboration, and an unwavering commitment to excellence. This launch was not just about introducing a new SKU; it was about creating an experience. One that embodied authenticity, bold flavor profiles, nutritional integrity, and a design-led consumer appeal that reflected the evolving tastes of the modern Indian shopper.

Asia-Pacific Dairy Market Report Scope

The dairy market refers to the economic exchange of dairy products, including milk, cheese, yogurt, and butter, as well as the supply and demand dynamics of these products. The Asia-Pacific dairy market is segmented by product type, distribution channel, and geography. By product type, the market is segmented into butter, cheese, cream, dairy desserts, milk, sour milk drinks, and yogurt. By distribution channel, the market is segmented into off-trade and on-trade. By geography, the market is segmented into Australia, China, India, Japan, and the Rest of the Asia-Pacific. The market forecasts are provided in terms of value (USD) and Volume (Tons).

Product Type

| Butter | Salted Butter | |

| Unsalted Butter | ||

| Cheese | Natural Cheese | Cheddar |

| Cottage | ||

| Ricotta | ||

| Parmesan | ||

| Others | ||

| Processed Cheese | ||

| Cream | Fresh Cream | |

| Cooking Cream | ||

| Whippng Cream | ||

| Others | ||

| Dairy Desserts | Ice Cream | |

| Cheesecakes | ||

| Frozen Desserts | ||

| Others | ||

| Milk | Condensed milk | |

| Flavored Milk | ||

| Fresh Milk | ||

| UHT Milk | ||

| Powdered Milk | ||

| Yogurt | Drinkable | |

| Spoonable | ||

| Sour Milk Drinks | ||

Distribution Channel

| On-trade | |

| Off-trade | Convenience Stores |

| Specialist Retailers | |

| Supermarkets and Hypermarkets | |

| On-line Retail | |

| Others |

By Geography

| India |

| China |

| Japan |

| Australia |

| Rest of Asia-Pacific |

| Product Type | Butter | Salted Butter | |

| Unsalted Butter | |||

| Cheese | Natural Cheese | Cheddar | |

| Cottage | |||

| Ricotta | |||

| Parmesan | |||

| Others | |||

| Processed Cheese | |||

| Cream | Fresh Cream | ||

| Cooking Cream | |||

| Whippng Cream | |||

| Others | |||

| Dairy Desserts | Ice Cream | ||

| Cheesecakes | |||

| Frozen Desserts | |||

| Others | |||

| Milk | Condensed milk | ||

| Flavored Milk | |||

| Fresh Milk | |||

| UHT Milk | |||

| Powdered Milk | |||

| Yogurt | Drinkable | ||

| Spoonable | |||

| Sour Milk Drinks | |||

| Distribution Channel | On-trade | ||

| Off-trade | Convenience Stores | ||

| Specialist Retailers | |||

| Supermarkets and Hypermarkets | |||

| On-line Retail | |||

| Others | |||

| By Geography | India | ||

| China | |||

| Japan | |||

| Australia | |||

| Rest of Asia-Pacific | |||

Need A Different Region or Segment?

Customize Now

Market Definition

- Butter - Butter is a yellow-to-white solid emulsion of fat globules, water, and inorganic salts produced by churning the cream from cows’ milk

- Dairy - Dairy product include milk and any of the foods made from milk, including butter, cheese, ice cream, yogurt, and condensed and dried milk.

- Frozen Desserts - Frozen dairy dessert means and includes products containing milk or cream and other ingredients which are frozen or semi-frozen prior to consumption, such as ice milk or sherbet, including frozen dairy desserts for special dietary purposes, and sorbet

- Sour Milk Drinks - Sour milk is thick, curdled milk, with a sour taste, obtained from the fermentation of milk. Sour milk drinks such as kefir, laban, buttermilk have been considered in the study

| Keyword | Definition |

|---|---|

| Cultured Butter | Cultured butter is prepared by having the raw butter go through chemical processing and has been added with certain emulsifiers and foreign ingredients. |

| Uncultured Butter | This type of butter is one which has not been processed in any way |

| Natural Cheese | The type of cheese in its most natural form. It is made from natural and simple products and ingredients, including fresh and natural salts, natural colors, enzymes, and high-quality milk. |

| Processed Cheese | Processed cheese undergoes the same processes as natural cheese; however, it requires more steps and many different forms of ingredients. Making processed cheese involves melting natural cheese, emulsifying it, and adding preservatives and other artificial ingredients or colorings. |

| Single Cream | Single cream contains around 18% fat. It’s a single layer of cream that appears over boiled milk. |

| Double Cream | Double cream contains 48% fat, more than double the amount of fat of single cream. It’s heavier and thicker than single cream |

| Whipping Cream | This has a much higher fat percentage than single cream (36%). Used to top cakes, pies, and puddings and as a thickener for sauces, soups, and fillings. |

| Frozen Desserts | Desserts that are meant to be eaten in frozen condition. E.g., sherbets, sorbets, frozen yogurts |

| UHT Milk (Ultra-high temperature milk) | Milk heated at a very high temperature. Ultra-high-temperature processing (UHT) of milk involves heating for 1–8 sec at 135–154°C. which kills the spore-forming pathogenic microorganism, resulting in a product with a shelf-life of several months. |

| Non-dairy butter/Plant-based butter | Butter made from plant-derived oil such as coconut, palm, etc. |

| Non-dairy Yogurt | Yogurt made from typically made from nuts, like almonds, cashews, coconuts, and even other foods like soybeans, plantains, oats, and peas |

| On-trade | It refers to restaurants, QSRs, and bars. |

| Off-trade | It refers to supermarkets, hypermarkets, on-line channels, etc. |

| Neufchatel cheese | One of the oldest kinds of cheese in France. It is a soft, slightly crumbly, mold-ripened, bloomy-rind cheese made in the Neufchâtel-en-Bray region of Normandy. |

| Flexitarian | It refers to a consumer preferring a semi-vegetarian diet, that is centered on plant foods with limited or occasional inclusion of meat. |

| Lactose Intolerance | Lactose intolerance is a reaction in digestive system to lactose, the sugar in milk. It causes uncomfortable symptoms in response to the consumption of dairy products. |

| Cream Cheese | Cream cheese is a soft and creamy fresh cheese with a tangy taste made from milk and cream. |

| Sorbets | Sorbet is a frozen dessert made using ice combined with fruit juice, fruit purée, or other ingredients, such as wine, liqueur, or honey. |

| Sherbet | Sherbet is a sweetened frozen dessert made with fruit and some sort of dairy product such as milk or cream. |

| Shelf stable | Foods that can be safely stored at room temperature, or "on the shelf," for at least one year and do not have to be cooked or refrigerated to eat safely. |

| DSD | Direct Store Delivery is the process in supply chain management wherein the product is delivered from manufacturing plant directly to the retailer. |

| OU Kosher | Orthodox Union Kosher is a kosher certification agency based in New York City. |

| Gelato | Gelato is a frozen creamy dessert made with milk, heavy cream and sugar. |

| Grass-fed Cows | Grass-fed cows are allowed to graze in pastures, where they eat a variety of grasses and clover. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF