Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

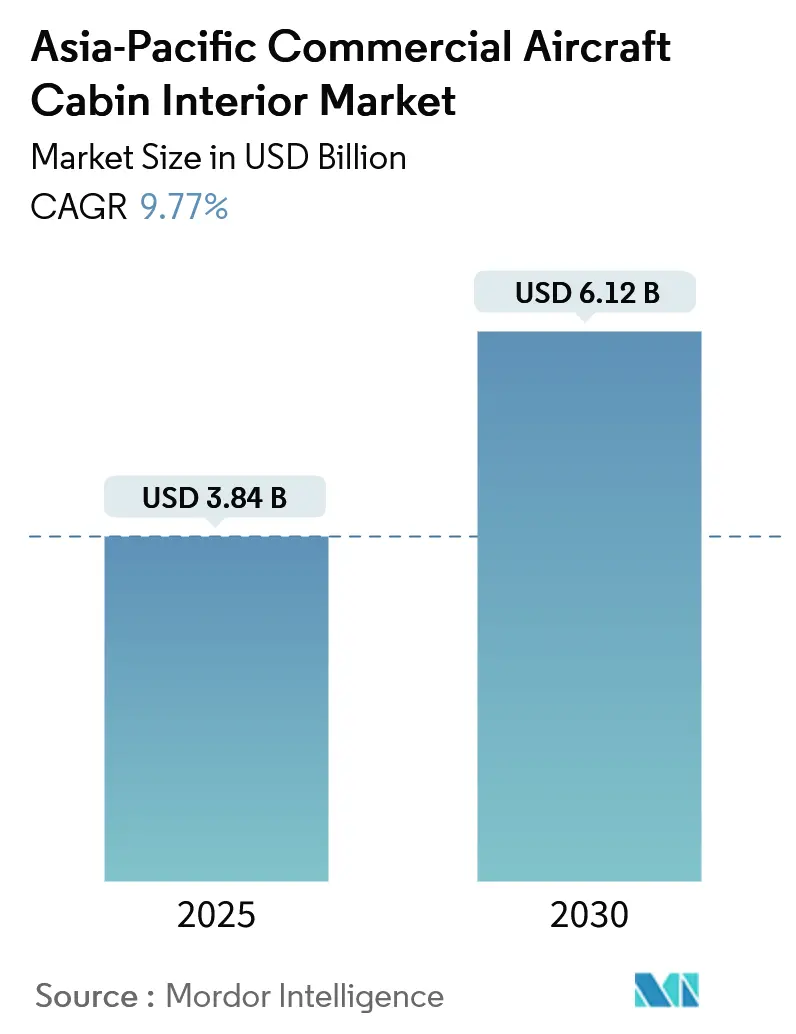

| Market Size (2025) | USD 3.84 Billion |

| Market Size (2030) | USD 6.12 Billion |

| Growth Rate (2025 - 2030) | 9.77% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Commercial Aircraft Cabin Interior Market Analysis by Mordor Intelligence

By 2025, the Asia-Pacific commercial aircraft cabin interior market is set to hit USD 3.84 billion, with projections showing a robust CAGR of 9.77%, pushing it to USD 6.12 billion by 2030. This growth trajectory is underpinned by several pivotal factors: a swift rebound in passenger traffic at regional hubs, aggressive delivery timelines for both narrow- and wide-body aircraft, and airlines opting for extensive retrofit programs to prolong fleet life. While steady fleet restoration bolsters short-term retrofit demand, a forecasted 19,500 aircraft deliveries by 2043 guarantee a sustained backlog for line-fit orders.

Airline strategies are evolving, reshaping the priorities for cabin interiors. Low-cost carriers (LCCs) are gravitating towards high-density, cost-effective cabin designs. In contrast, premium carriers are swiftly integrating LED mood lighting and premium economy seating, emphasizing brand distinction. Concurrently, China and India are ramping up production capacities through localized supply chain efforts. Yet, suppliers grapple with challenges such as raw material price swings and foreign exchange fluctuations, which squeeze their margins. As airlines intensify their focus on ESG (Environmental, Social, and Governance) objectives, there's a notable shift towards composite-rich monuments and seating, aiming to curtail fuel consumption and operational expenses.

These developments underscore the dynamic evolution of the Asia-Pacific commercial aircraft cabin interior market, driven by a blend of innovation, sustainability, and astute fleet management.By 2025, the Asia-Pacific commercial aircraft cabin interior market is set to hit USD 3.84 billion, with projections showing a robust CAGR of 9.77%, pushing it to USD 6.12 billion by 2030. This growth trajectory is underpinned by several pivotal factors: a swift rebound in passenger traffic at regional hubs, aggressive delivery timelines for both narrow- and wide-body aircraft, and airlines opting for extensive retrofit programs to prolong fleet life. While steady fleet restoration bolsters short-term retrofit demand, a forecasted 19,500 aircraft deliveries by 2043 guarantee a sustained backlog for line-fit orders.

Airline strategies are evolving, reshaping the priorities for cabin interiors. Low-cost carriers (LCCs) are gravitating towards high-density, cost-effective cabin designs. In contrast, premium carriers are swiftly integrating LED mood lighting and premium economy seating, emphasizing brand distinction. Concurrently, China and India are ramping up production capacities through localized supply chain efforts. Yet, suppliers grapple with challenges such as raw material price swings and foreign exchange fluctuations, which squeeze their margins. As airlines intensify their focus on ESG (Environmental, Social, and Governance) objectives, there's a notable shift towards composite-rich monuments and seating, aiming to curtail fuel consumption and operational expenses.

These developments underscore the dynamic evolution of the Asia-Pacific commercial aircraft cabin interior market, driven by a blend of innovation, sustainability, and astute fleet management.

Key Report Takeaways

- In 2024, seating claimed a 43.75% share of the Asia-Pacific commercial aircraft cabin interior market.

- Narrow-body models took the lead, holding a 65.38% share of the Asia-Pacific commercial aircraft cabin interior market in 2024. Wide-body interiors, however, are set to experience a growth spurt, with a projected CAGR of 6.84% through 2030.

- Economy class dominated the scene, seizing 52.46% of the Asia-Pacific commercial aircraft cabin interior market in 2024. Meanwhile, the premium economy segment is on track for a notable surge, with a forecasted CAGR of 8.46% by 2030.

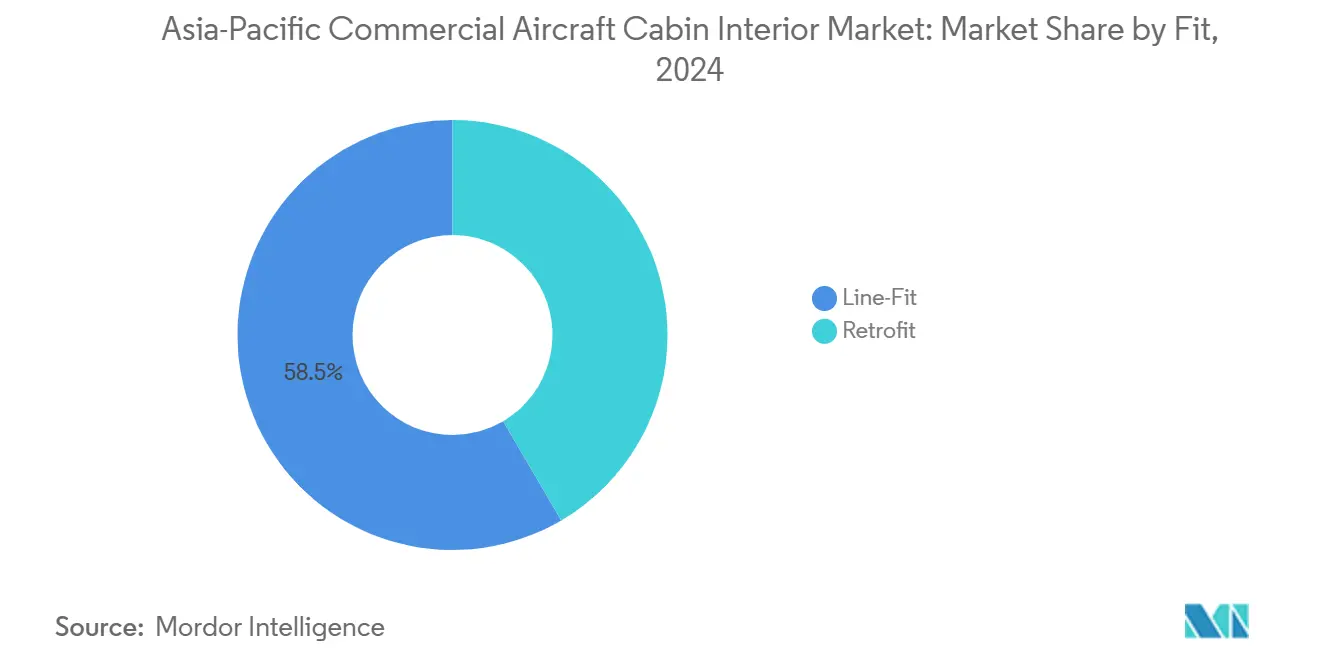

- Line-fit installations captured 58.45% of the Asia-Pacific commercial aircraft cabin interior market in 2024. On the other hand, retrofit spending is gearing up for a notable expansion, with an anticipated CAGR of 7.25% through 2030.

- Composites took the lead with a 46.92% share of the Asia-Pacific commercial aircraft cabin interior market in 2024. Advanced thermoplastics, however, are eyeing a notable rise, with a projected CAGR of 9.61% through 2030.

- China stood tall, accounting for 42% of the regional revenue in 2024. Yet, it's India that's set to steal the spotlight, boasting the fastest growth rate with a projected CAGR of 11.2% through 2030.

Asia-Pacific Commercial Aircraft Cabin Interior Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging low-cost-carrier fleet expansion | +2.8% | Southeast Asia and India | Medium term (2-4 years) |

| Mandatory 16g/21g seat-safety retrofits | +2.2% | China and India | Short term (≤ 2 years) |

| LED mood-lighting adoption for brand and fuel savings | +1.9% | Premium carriers across APAC | Medium term (2-4 years) |

| Premium-economy cabin reconfiguration boom | +1.7% | Japan, Singapore, South Korea | Long term (≥ 4 years) |

| Government incentives for indigenous interior supply chains | +0.6% | China, India, Indonesia | Long term (≥ 4 years) |

| Airline ESG targets driving lightweight-composite demand | +1.4% | Region-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Low-Cost-Carrier Fleet Expansion

In 2024, low-cost carriers (LCCs) ordered over 280 single-aisle jets, each requiring innovative interior solutions such as lighter seats, slim galleys, and high-capacity bins to facilitate 25-minute turnaround times.[1]"Akasa Air announces its three-digit aircraft order of 150 Boeing 737 MAX aircraft at WINGS India 2024," Akasa Air, akasaair.com [2]"China Southern Airlines orders 100 C919 aircraft for $9.9bn, last of China's big 3 to order C919s," Aviation Economics, aviationnews-online.com

In response, interior vendors have introduced ultra-light 16g seat frames, reducing aircraft weight by approximately 300 kg. This weight reduction translates to notable fuel savings, a metric of paramount importance to LCC managers. Furthermore, driven by the ancillary revenue model, there's a growing adoption of full-row seatback device holders and power outlets, tailored for short-haul passengers. This emphasis on cabin density also means more frequent refurbishments, ensuring soft materials adhere to visible-wear compliance standards. Additionally, with LCC hubs expanding in Cebu, Chiang Mai, and Ho Chi Minh City, the service network has been strengthened, incorporating smaller domestic MRO (Maintenance, Repair, and Overhaul) shops into the regional cabin retrofit landscape.

Mandatory 16g/21g Seat-Safety Retrofits

The requirement to upgrade cabin interiors, with seats costing USD 150,000 each, is projected to drive a USD 450 million retrofit initiative in China. This effort aims to ensure compliance with evolving safety standards while maintaining the full operational status of the Guangzhou and Xiamen facilities through 2026.

In a parallel move, Air India set aside USD 400 million in August 2025 for a comprehensive fleet overhaul, targeting upgrades for 200 aircraft.[3]“Air India Launches $400M Retrofit Program for B787-8 Dreamliner Fleet,” AeroTime, aerotime.aero These retrofits encompass not only seat replacements but also enhancements to rail tracks, floor panels, and galley monuments, all of which are upgraded to meet stringent dynamic load standards. This presents a lucrative opportunity for integrated suppliers, enabling them to offer a broader range of solutions beyond just seat shells, thereby paving the way for potential upselling.

LED Mood-Lighting Adoption for Brand and Fuel Savings

In November 2024, Singapore Airlines (SIA) unveiled a SGD 1.1 billion (USD 814 million) investment, targeting upgrades for the cabin products of 41 Airbus A350-900 long-haul and ultra-long-range (ULR) aircraft. This move is set to elevate the premium travel experience. Among the upgrades, seven A350-900ULR aircraft will debut a new First Class cabin, poised to redefine comfort and luxury on the globe's longest routes. The retrofit introduces state-of-the-art LED lighting systems, boasting customizable color zones. These not only boost energy efficiency and cut fuel consumption but also prioritize passenger well-being.[4]“Singapore Airlines Announces Fleet Retrofit Program,” Singapore Airlines, singaporeair.com

Lighting scenarios, programmed for dawn, meals, and rest, aim to mitigate the jet lag process, especially on extended journeys like Seoul to Sydney. By mimicking natural light shifts, these enhancements promise a more comfortable flight.

Original Equipment Manufacturer (OEM) kits now seamlessly blend light strips with cutting-edge cabin-management software. Additionally, plug-and-play harnesses have slashed installation downtime to a mere three days. Yet, in markets such as China or India, certification hurdles can stretch the timeline by half a year. This challenge nudges airlines to either book installation slots early or opt for off-the-shelf color presets, streamlining the regulatory approval process.

Premium-Economy Cabin Reconfiguration Boom

Just six months after their debut, Japan Airlines' domestic premium economy seats boasted an impressive 85% load factor. This achievement underscores the trend: middle-class travelers, often price-sensitive, are opting for the added legroom of premium economy, steering clear of the heftier business class fares.

In a strategic move, Cathay Pacific and Thai Airways have revamped their A350 and A330 aircraft. They've sacrificed 10-15 rows of economy seating, making way for wider premium economy seats that now accommodate a generous 38-inch pitch and calf rests. Such a reconfiguration isn't just about seating; it necessitates adjustments in galley layouts to fit in extra hot-meal carts and dedicated beverage supplies. To streamline this process, monument suppliers are incorporating modular chillers and oven racks into their designs. The surging popularity of premium economy isn't just a trend; it's prompting airlines to invest more in retrofitting their fleets. With these enhancements, airlines can expect to boost revenue per flight by as much as 20% on select routes, while reducing the overall seat count by only 5-7%.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Certification bottlenecks at CAAC and DGCA | -1.1% | China and India | Short term (≤ 2 years) |

| Raw-material and forex volatility squeezing margins | -0.8% | Region-wide | Medium term (2-4 years) |

| Limited MRO slot capacity in APAC hubs | -0.6% | Singapore, Hong Kong, Bangkok | Short term (≤ 2 years) |

| Fragmented regional compliance standards | -0.4% | Multi-country operators | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Certification Bottlenecks at CAAC and DGCA

Due to post-MAX caution, the Civil Aviation Administration of China (CAAC) has extended approval timelines for non-local seating and In-Flight Entertainment and Connectivity (IFEC) vendors to 12-18 months. As a result, many Western firms are now partnering with local engineering centers, skilled in navigating the regulatory paperwork in Mandarin and the intricacies of government bureaucracy. In a parallel move, the Directorate General of Civil Aviation (DGCA) has imposed similar hurdles, mandating system-level integration tests that mirror those of the Federal Aviation Administration (FAA). This requirement has pushed back cabin Wi-Fi approvals by an additional two quarters. Smaller suppliers, often lacking dedicated in-house regulatory teams, incur additional consultancy fees to navigate these challenges.

On the other hand, larger players can more easily absorb these delays thanks to their scale. Additionally, Chinese carriers sometimes opt for domestically certified components, such as LED strips or seat power outlets, even when global standards exceed local ones. This choice is primarily influenced by the faster six-week clearance for locally certified products.

Raw-Material and Forex Volatility Squeezing Margins

In 2024, a resurgence in aerospace demand propelled aluminum prices up by 28% and carbon-fiber weaves by 30%. These surges notably increased costs for components such as seat frames and sidewalls. Concurrently, Asian currencies, notably the Indonesian Rupiah (IDR) and Indian Rupee (INR), saw a depreciation of 6-8% against the US Dollar. This currency shift further squeezed margins for suppliers reliant on imports. In response, contract clauses have evolved to include quarterly pass-through indices for precise pricing adjustments. Yet, airlines push back against escalator provisions exceeding a 4% limit. On another front, initiatives for composite recycling are gaining momentum. Recovered carbon sheets, available at 75% of the cost of virgin fiber, present a promising solution to mitigate cost volatility and support sustainability goals.

Segment Analysis

By Product Type: Seating Dominance Faces IFEC Innovation Challenge

In 2024, the seating segment captured 43.75% of the revenue, underscoring its pivotal role in fleet expansion bills. Yet, as airlines push for composite frames under 8 kg, unit prices have dipped due to weight reduction demands. On the other hand, IFEC revenue is on an upswing, boasting a 7.97% CAGR. Projections suggest it could reach USD 1.45 billion by 2030, driven by innovations such as seatback 4K displays, satellite broadband, and advertising models that yield an additional USD 3 per passenger. Galley and monument packages, once exclusive to business class, now feature additions like espresso modules and fresh-food chillers, thanks to the burgeoning premium economy segment. Cabin-lighting vendors are capitalizing on LED retrofits, synchronizing them with D-checks to curtail downtime.

By 2030, the Asia-Pacific market for commercial aircraft cabin interiors is expected to see the seating segment reach USD 2.67 billion, accounting for approximately 40% of the total expenditure, despite a decelerated growth rate. Meanwhile, the IFEC segment is poised to expand its share from 12% to 17% of the overall market value in aircraft. In the face of intensifying competition, suppliers are streamlining their offerings, bundling seats, lighting, and IFEC into cohesive packages that expedite integration tests. Operators driven by ESG considerations are willing to pay a premium for composite-skin side-walls with thermoplastic laminated to reduce the weight, shaving off 45 kg per narrow-body. Additionally, stowage bins, with a 70-liter capacity per passenger, strike a balance, accommodating carry-on surges without surpassing hinge-moment loads.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Aircraft Type: Narrow-Body Supremacy Challenged by Wide-Body Recovery

In 2024, single-aisle platforms dominated the revenue landscape, securing 65.38% of the total. This surge was fueled by an explosion of LCC networks and robust demand for domestic city-pair travel in China, India, and the ASEAN region. The Asia-Pacific market for narrow-body aircraft cabin interiors reached a valuation of USD 2.5 billion in 2024. This segment is poised for a 6.5% annual growth rate through 2030, bolstered by backlogs in the A320neo and 737 MAX. Meanwhile, widebody interiors are set to outpace their narrow-body counterparts, with a projected CAGR of 6.84%. This higher growth rate of widebody aircraft is attributed to airlines reactivating long-haul seats and introducing premium-heavy configurations, complete with suites and enclosed business pods. Notably, strategies like Emirates' A380 refresh highlight the lucrative potential of cabin retrofitting. An investment of USD 30 million in an interior refresh can rejuvenate an asset's life by a decade, all while being significantly less capital-intensive than new-build deliveries.

Single-aisle economics remain influenced by cabin-density imperatives, which have led lavatory suppliers to dispatch units, each weighing under 400 kg, in sets of three. On the other hand, widebody innovators are pushing boundaries. They require tailored load-path analyses, a necessity given the aircraft's size and weight. Their offerings include self-contained bar units, onboard spas, and ceiling-mounted projection screens, all designed to curate a unique onboard experience. However, as aircraft size increases, so does the complexity of certification. The presence of multiple Class 2 monuments and bunks demands meticulous load-path analyses. In response, suppliers have adapted by deploying dual engineering teams. One team focuses on volume narrow-body turnkey kits, while the other concentrates on high-margin, low-rate customizations for widebody aircraft.

By Cabin Class: Economy Scale Meets Premium Growth Acceleration

Economy cabins, with their sheer seat count, still account for 52.46% of total revenue. While concerns about airborne pathogens linger, premium-economy bookings, boasting load factors of 80% or higher, yield 25-30% more revenue, leading to an 8.46% CAGR for the segment in the forecast period. To address concerns about airborne pathogens on 10-hour routes, premium-class retrofits now feature sliding doors, wireless charging, and seat-directed vent airflow. By 2030, the Asia-Pacific market for premium economy fittings in commercial aircraft cabins is projected to exceed USD 900 million. OEMs are noticing a shift, with soft-goods refresh cycles tightening to five years, driven by rapidly changing textile fashion trends.

First-class seating remains a rarity, with only 11 carriers maintaining full cabins. However, these suites command a public relations value that far exceeds their spatial footprint. Upgrades in economy class now include slimline cushions, USB-C power ports, and ultra-light meal tables, collectively saving 2 kg per triple seat. Airlines are now repositioning class splits every two to three years based on yield analytics, making seat-rail flexibility and quick-change kits key selling points for engineers.

By Fit: Line-Fit Leadership Faces Retrofit Acceleration

Line-fit held 58.45% of the revenue as of 2024, mainly because the Asia-Pacific order book delivered 431 aircraft that year. Yet, retrofit activity is rising at a 7.25% CAGR, and annual spend is expected to surpass line-fit outlays by 2028 as airlines batch 16 G seat upgrades with premium-economy installs during heavy maintenance. Retrofit suppliers must stage mobile teams in Singapore and Hong Kong MRO zones to minimize ferry time. Airlines pay a 15-20% premium for night-stop turnaround kits that enable them to restore aircraft to schedule after 72 hours, rather than the conventional two-week hangar stay.

Line-fit advantages include factory-level wiring and cabin-pressure qualification, resulting in 30% lower labor hours per ship-set compared to retrofit installations. However, interior specification changes freeze 18 months before delivery, forcing airlines to lock in a cabin design well before competitive pressures may shift. Retrofit flexibility thus remains a strategic asset, even for operators with extensive new-build pipelines.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Material: Composites Lead Sustainability Drive

In 2024, composites accounted for 46.92% of the revenue, highlighting their pivotal role in premium seating frames, overhead bins, and side-wall panels. Here, weight savings result in reduced fuel consumption and lower emissions. Advanced thermoplastics, growing at a 9.61% CAGR, are reaping benefits from airlines' ESG targets and heightened regulatory pressures to minimize operating weight. While aluminum alloys are experiencing a dwindling market share in the Asia-Pacific commercial aircraft cabin interior sector due to carriers' push for lighter retrofit substitutes, aluminum still plays a crucial role in galley structures that demand high heat tolerance. Steel finds its niche in high-stress fixtures, such as lavatory mounts, prioritizing durability over weight. Material choices are increasingly influenced by recyclability clauses, as seen with Singapore Airlines and Cathay Pacific, who embed these in contracts to achieve 2030 carbon-neutral goals, urging suppliers to validate closed-loop composite recycling lines.

Following the Boeing 787 and Airbus A350 programs, which demonstrated a 15-20% reduction in cabin weight over aluminum designs, the adoption of thermoplastics surged. Flame-retardant resin systems, which meet the FAA's vertical burn and heat-release standards, have expanded cabin applications from seat shells to window shrouds. Local composite producers in China, responding to EASA and CAAC audits, are striving for global quality benchmarks before securing long-term supply deals with airlines. Consequently, Chinese manufacturers are channeling investments into autoclave and out-of-autoclave curing lines, targeting both domestic C919 cabins and Southeast Asian retrofits. Their supply-chain strategies favor the use of virgin carbon fiber for primary load-bearing components. At the same time, secondary panels utilize recycled fibers, aligning with airline ESG evaluations that now prioritize circularity alongside cost considerations.

Geography Analysis

Regional Aviation Interior Market Trends and Growth Insights

China maintained approximately 42% of the 2024 regional aviation spending, solidifying its position by committing to 460 new jets for both state and private carriers in 2023. The domestic C919 program has prompted OEMs to dual-source cabin components locally, leading to seat and galley production in Jiangsu and Sichuan that now achieves CAAC compliance in as little as six weeks. The growth of secondary-city routes, such as those in Harbin, Uruthe mqi, and Haikou, is fueling demand for narrow-body interiors, particularly for dense 195-seat configurations. Additionally, retrofit demand spikes when carriers synchronize interior upgrades with mandatory seat-safety compliance, aligning CAAC enforcement cycles with predictable parts demand.

India recorded the fastest growth in the region, with an impressive 11.2% CAGR. This growth is driven by key developments, including IndiGo’s 500-aircraft Airbus deal, Go First’s relaunch application, and Air India’s comprehensive fleet interior overhaul backed by Tata.[5]“IndiGo Orders 500 Airbus A320 Family Aircraft,” IndiGo, goindigo.in Domestic routes under two hours dominate the traffic mix; however, rising middle-class demand is prompting the deployment of 787 and A350 aircraft on nonstop international routes, such as Delhi-San Francisco. This shift is increasing, which in turn influences the demand for premium economy and IFEC (In-Flight Entertainment and Connectivity) specifications. Furthermore, India’s Production-Linked Incentive (PLI) program is incentivizing supply chain localization, encouraging investments in subassemblies and clusters in Hyderabad.

In the ASEAN region, countries such as Indonesia, in turn, influence Southeast Asia. The Philippines is leveraging tourism recovery and LCC (Low-Cost Carrier) fleet expansions to drive domestic demand. Cebu Pacific’s introduction of the A330neo with expanded premium economy seating validates the hybrid model approach, encouraging carriers like Lion Air and AirAsia to explore similar strategies. Singapore continues to set cabin trends in the region, with Singapore Airlines’ USD 300 million retrofit of 50 wide-body aircraft establishing high standards for fit and finish, influencing neighboring airlines that aim to remain competitive. Meanwhile, South Korea and Japan act as technology pioneers, often being the first to adopt innovations such as AI-driven seat-temperature management systems and AR-assisted cabin inspection technologies, which subsequently spread, encouraging investments across the region.

Competitive Landscape

China maintained approximately 42% of the 2024 regional aviation spending, solidifying its position by committing to 460 new jets for both state and private carriers last year. The domestic C919 program has prompted OEMs to dual-source cabin components locally, leading to seat and galley production in Jiangsu and Sichuan that now achieves CAAC compliance in as little as six weeks. The growth of secondary-city routes, such as those in Harbin, Urumqi, and Haikou, is fueling demand for narrow-body interiors, particularly for dense 195-seat configurations. Additionally, retrofit demand spikes when carriers synchronize interior upgrades with mandatory seat-safety compliance, aligning CAAC enforcement cycles with predictable parts demand.

India recorded the fastest growth in the region, with an impressive 11.2% CAGR. This growth is driven by key developments, including IndiGo’s 500-aircraft Airbus deal, Go First’s relaunch application, and Air India’s comprehensive fleet interior overhaul, backed by Tata. Domestic routes under two hours dominate the traffic mix; however, rising middle-class demand is prompting the deployment of 787 and A350 aircraft on nonstop international routes, such as Delhi-San Francisco. This shift is increasing demand for premium-economy and IFEC (In-Flight Entertainment and Connectivity) specifications. Furthermore, India’s Production-Linked Incentive (PLI) program incentivizes supply chain localization, encouraging investments in supply chain clusters such as Nagpur and Hyderabad.

In the ASEAN region, countries such as Indonesia Philippines are leveraging tourism recovery and LCC (Low-Cost Carrier) fleet expansions to drive internal demand. Cebu Pacific’s introduction of the A330neo with expanded premium economy seating validates the hybrid model approach, encouraging carriers like Lion Air and AirAsia to explore similar strategies. Singapore continues to set cabin trends in the region, with Singapore Airlines’ USD 300 million retrofit of 50 wide-body aircraft establishing high standards for fit and finish, which in turn influences neighboring airlines that aim to remain competitive. Meanwhile, South Korea and Japan act as technology pioneers, often being the first to adopt innovations such as AI-driven seat temperature management systems and AR-assisted cabin inspection technologies, which subsequently spread across the region.

Asia-Pacific Commercial Aircraft Cabin Interior Industry Leaders

-

Collins Aerospace

-

JAMCO Corporation

-

Safran S.A.

-

Panasonic Holdings Corporation

-

Expliseat S.A.S.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- August 2025: Cathay Pacific finished equipping every aircraft with seat-back 4K displays and full-fleet Wi-Fi, offering free connectivity to premium passengers.

- August 2025: All Nippon Airways (ANA) is implementing free Viasat in-flight connectivity across all international classes on its 767-300ER aircraft. The airline aims to install Wi-Fi services on more than 80% of its international fleet by 2030.

- June 2025: VietJet Thailand partnered with Bluebox Aviation Systems to introduce an in-flight entertainment (IFE) service powered by the Blueview digital platform.

- April 2025: Riyadh Air selected Safran's Unity Business Class Suite for installation across its Boeing 787-9 fleet. The airline's decision aligns with its commitment to deliver premium passenger comfort and modern cabin amenities.

Asia-Pacific Commercial Aircraft Cabin Interior Market Report Scope

Cabin Lights, Cabin Windows, In-Flight Entertainment System, Passenger Seats are covered as segments by Product Type. Narrowbody, Widebody are covered as segments by Aircraft Type. Business and First Class, Economy and Premium Economy Class are covered as segments by Cabin Class. China, India, Indonesia, Japan, Singapore, South Korea are covered as segments by Country.

By Product Type

| Seating |

| Cabin Lighting |

| In-Flight Entertainment and Connectivity (IFEC) |

| Galley and Monument |

| Lavatory Systems |

| Cabin Windows and Windshields |

| Overhead Stowage Bins |

| Interior Panels and Floorboards |

| Others |

By Aircraft Type

| Narrowbody |

| Widebody |

| Regional Jet |

By Cabin Class

| Economy |

| Premium Economy |

| Business |

| First |

By Fit

| Line-Fit |

| Retrofit |

By Material

| Composites |

| Aluminum Alloys |

| Steel and Other Alloys |

| Advanced Thermoplastics |

By Country

| China |

| India |

| Indonesia |

| Japan |

| Singapore |

| South Korea |

| Rest of Asia-Pacific |

| By Product Type | Seating |

| Cabin Lighting | |

| In-Flight Entertainment and Connectivity (IFEC) | |

| Galley and Monument | |

| Lavatory Systems | |

| Cabin Windows and Windshields | |

| Overhead Stowage Bins | |

| Interior Panels and Floorboards | |

| Others | |

| By Aircraft Type | Narrowbody |

| Widebody | |

| Regional Jet | |

| By Cabin Class | Economy |

| Premium Economy | |

| Business | |

| First | |

| By Fit | Line-Fit |

| Retrofit | |

| By Material | Composites |

| Aluminum Alloys | |

| Steel and Other Alloys | |

| Advanced Thermoplastics | |

| By Country | China |

| India | |

| Indonesia | |

| Japan | |

| Singapore | |

| South Korea | |

| Rest of Asia-Pacific |

Need A Different Region or Segment?

Customize Now

Market Definition

- Product Type - Commercial Aircraft cabin interior products such as passenger seats, cabin lighting, inflight entertainment system, cabin windows, lavatories, galley, and stowage bins have been included under the product type in this study.

- Aircraft Type - All the passenger aircraft such as narrowbody and widebody which are single-aisle and twin-aisle are included in this study.

- Cabin Class - Business and First Class, economy and premium economy are classes of air travel provided by the airlines that offer various services to the passengers.

| Keyword | Definition |

|---|---|

| Gross domestic product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| High Dynamic Range (HDR) | Dynamic range describes the ratio between the brightest and darkest parts of an image. HDR is used to capture a greater dynamic range than SDR. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| European Aviation Safety Agency (EASA) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| 4K Display | 4K resolution refers to a horizontal display resolution of approximately 4,000 pixels. |

| Organic Light Emitting Diode (OLED) | It is the light-emitting diode (LED) in which the emissive electroluminescent layer is a film of organic compound that emits light in response to an electric current. |

| Mean Time Between Failures (MTBF) | The mean time between failures is the predicted elapsed time between inherent failures of a mechanical or electronic system, during normal system operation. |

| (Low-Cost Carrier (LCCs) | It is an airline that is operated with an especially high emphasis on minimizing operating costs and without some of the traditional services and amenities provided in the fare |

| Electronically Dimmable Windows (EDW) | It is a type of window that blocks up to 99.96% of all visible light and provide full opacity, integrated into the window cassette of the sidewall panel. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step 1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step 2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step 3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF