Market Trends of Asia-Pacific CDMO Industry

The Demand For Injectable Dose Formulation is Rising in the Market

- The CDMO market is poised for growth, driven by increasing demand for injectable drugs, notably in cancer research. With a strong emphasis on oncology and other potent medications (including antibody conjugates, steroids, and fast-acting IV fluids), cytotoxics are anticipated to spearhead the growth in the injectable dose formulation segment.

- Injectable drugs are poised to outperform other drug formulations, offering superior returns. This is primarily attributed to their higher ROI, enhanced therapeutic efficacy, and quicker onset of action. The surge in demand for diabetes drugs has led to shortages for many patients reliant on these medications. The increased demand for injectable diabetes drugs in the region significantly boosted the segment's growth.

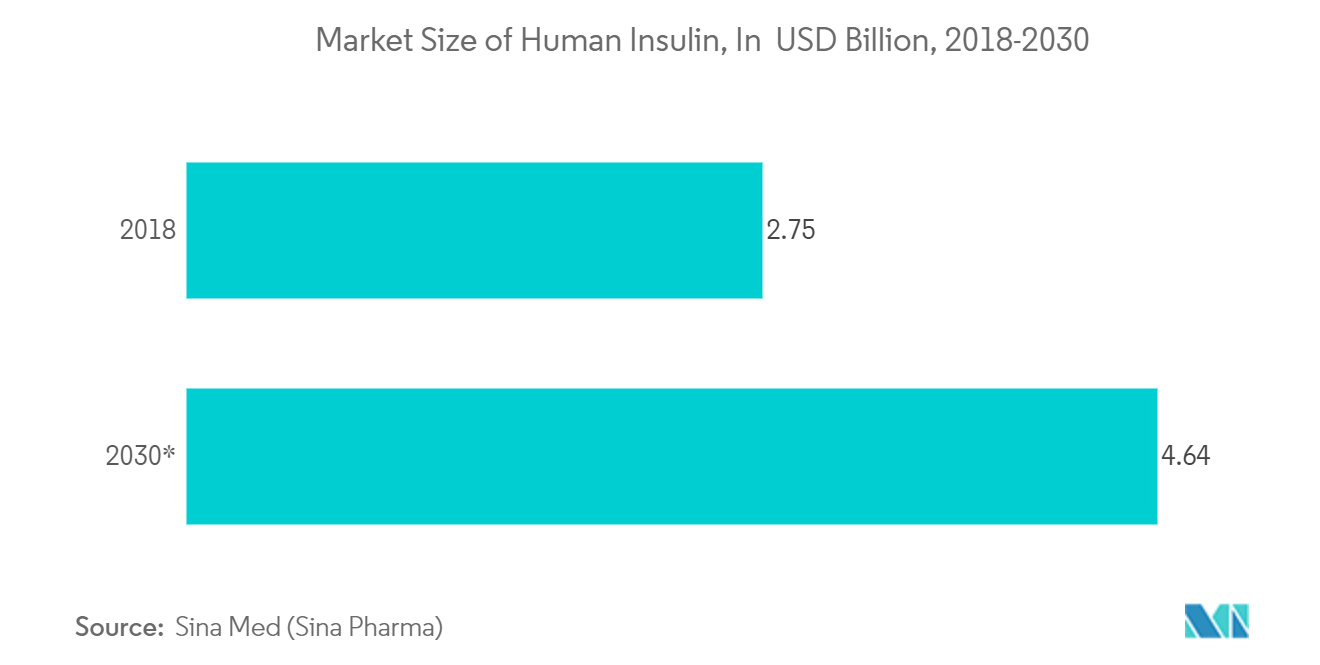

- According to Sina Med, the value of the human insulin market in China is expected to increase from USD 2.75 billion in 2018 to around USD 4.63 billion in 2030. The increasing prevalence of diabetes is a key driver expected to propel the growth of the injectable antidiabetic drugs market in the coming years.

- Further, the rising demand for cell and gene therapies is propelling the growth of the sterile injectable contract manufacturing sector. These therapies, tailored for genetic and chronic diseases, offer personalized and often curative treatments. Given their nature, manufacturing sterile injectables for these therapies necessitates specialized processes to meet stringent regulatory standards.

- In September 2023, India-based Strides introduced a separate branch of specialty pharma CDMO. The newly established company manufactures a wide array of products, spanning from biologicals to intricate injectables and oral soft-gelatin capsules. Such constants are expected to bolster the segmental growth in the region during the forecast period.

Understand The Key Trends Shaping This Market

Download PDF

India is Expected to Witness Robust Growth in the Upcoming Years

- The Indian pharmaceutical sector predominantly focuses on producing bulk pharmaceuticals, the foundational ingredients for formulations. While bulk pharmaceuticals constitute roughly 20% of the sector's output, formulations make up the remaining 80%. India's prowess extends to active pharmaceutical ingredients (APIs), with the country manufacturing over 500 APIs and serving as the origin for 60,000 generic brands spanning 60 therapeutic categories.

- The global CDMO market is expanding, propelled by the cost-effective resources found in emerging markets. India is the top choice for CDMOs, boasting over 100 manufacturing facilities approved by the US FDA, with this number rising. The biologics CDMO market in India's pharmaceutical sector is gaining ground, bolstered by the robust presence of key players like Zydus Cadila and LUPIN.

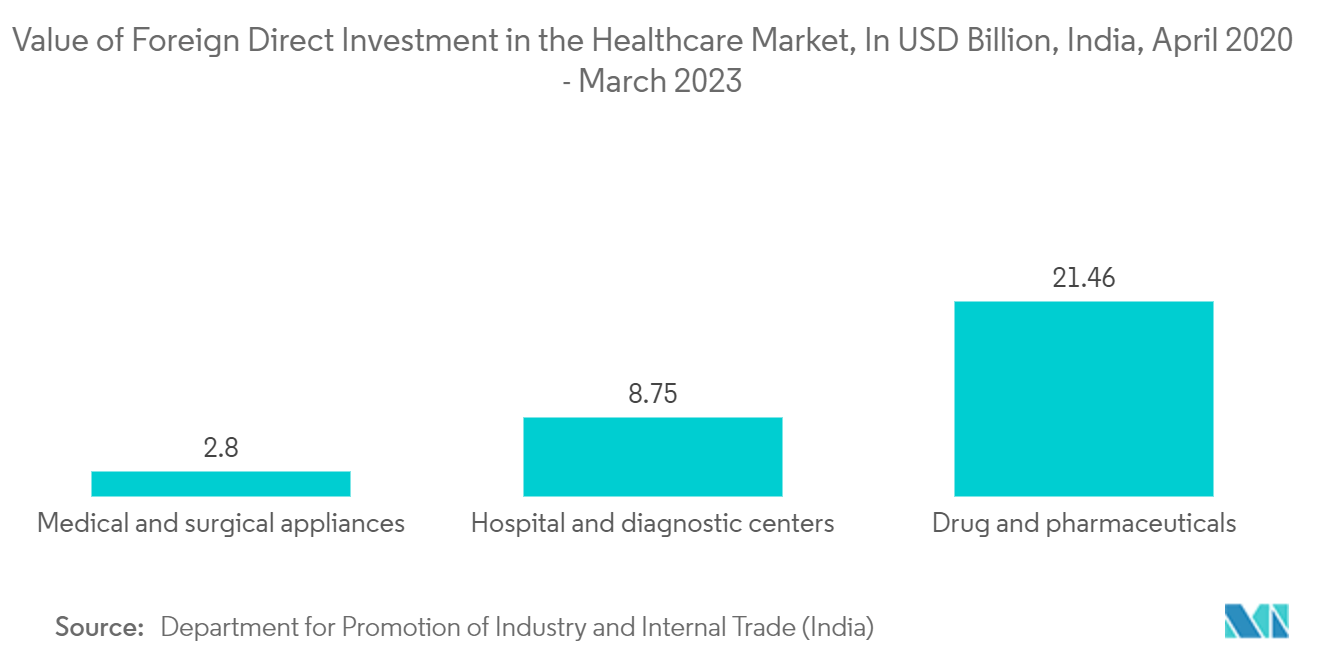

- The pharmaceutical sector in India has become a prime target for foreign investors, ranking among the nation's top ten industries for foreign investment. The Indian government has implemented an investor-friendly Foreign Direct Investment (FDI) policy to further bolster investments in this sector. According to the Department for Promotion of Industry and Internal Trade (India), across the entire healthcare sector, the amount invested in drugs and pharmaceuticals witnessed the highest foreign investment of USD 21.46 billion between April 2020 and March 2023. Such consistent investment in the pharmaceutical sector may propel the market for pharmaceutical contract manufacturing during the forecast period.

- The Indian pharmaceutical sector experienced a surge in growth, propelled by the COVID-19 pandemic. Post-pandemic, there was a notable uptick in demand and production for anti-viral and anti-bacterial drugs within India. Consequently, companies in this sector notched up rising revenues. The increased trade tensions between the US and China underscored the global pharmaceutical supply chain's need for geo-diversification. China's cost structure shifted, making it a pricier outsourcing hub, while India's appeal grew.

Get Analysis on Important Geographic Markets

Download PDF