Market Size of Asia-Pacific CDMO Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

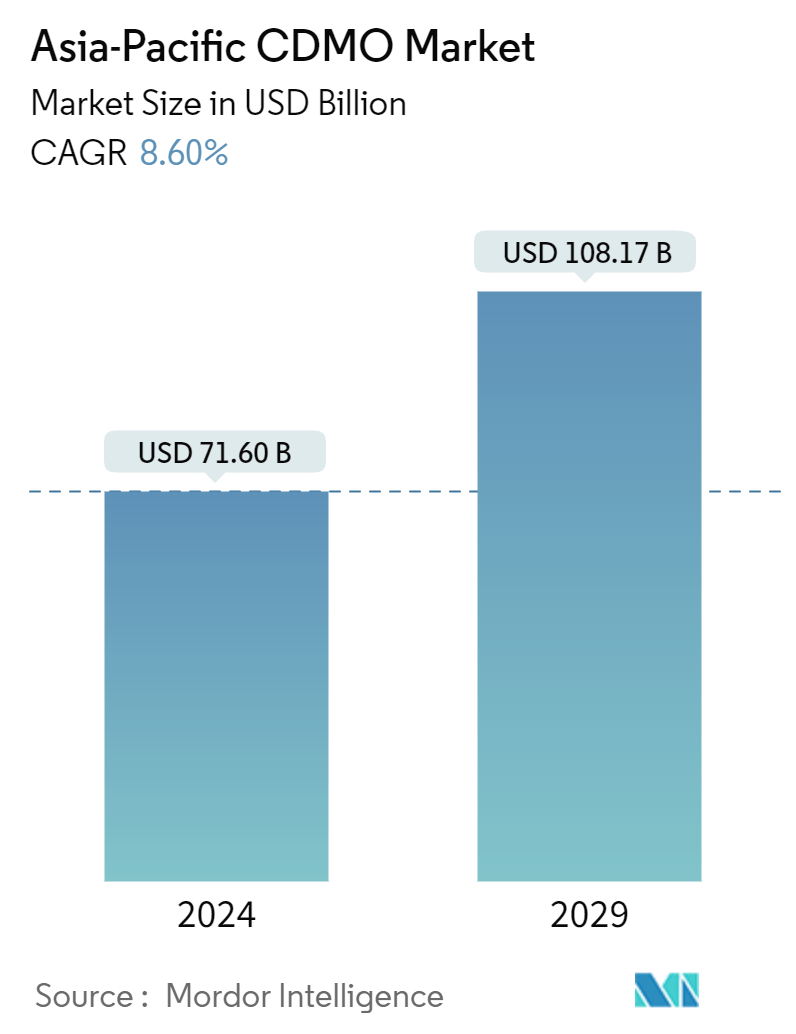

| Market Size (2024) | USD 71.60 Billion |

| Market Size (2029) | USD 108.17 Billion |

| CAGR (2024 - 2029) | 8.60 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Asia-Pacific CDMO Market Analysis

The Asia-Pacific CDMO Market size is estimated at USD 71.60 billion in 2024, and is expected to reach USD 108.17 billion by 2029, growing at a CAGR of 8.60% during the forecast period (2024-2029).

The Asia-Pacific CDMO (contract development and manufacturing organization) market is poised for substantial growth in 2024 and beyond. This growth can be attributed to escalating pharmaceutical demands, increasing emphasis on R&D, and the growing trend of outsourcing drug development and manufacturing.

- The market is set for substantial growth, driven by the escalating trend of pharmaceutical companies outsourcing drug development and manufacturing. This is largely due to robust government backing and enticing incentives that lure foreign investments.

- Emerging markets, including China, India, and South Korea, are poised to maintain their dominance in the market. The rising incidence of chronic diseases and aging demographics in these nations are expected to drive up the need for pharmaceuticals, subsequently boosting the demand for CDMO services.

- China has over 180 million elderly citizens suffering from chronic diseases; of that, 75% has more than one, according to the National Health Commission (NHC). By 2030, cardiovascular diseases are expected to cost the Chinese government USD 1,044 billion. Similar trends for the high prevalence of diabetes are present in Asia-Pacific, including China, South Korea, and Australia.

- While the United States remains the central hub for pharmaceutical development outsourcing, the APAC region stands out as the favored CDMO growth market. This preference is largely attributed to the region's cost-effective manufacturing compared to North America and Europe. Significant funding allocations and the clustering of pharmaceutical research centers around universities contribute to this trend.

- However, the Asia-Pacific CDMO market is grappling with a severe labor shortage, leading to a significant surge in labor costs. This trend has prompted numerous Western CDMOs to relocate their operations back to the United States and Europe. Moreover, national policies, trade dynamics like Brexit and the US-China conflict, and the repercussions of the pandemic are poised to prompt the reshoring of supply chains in numerous nations.

Asia-Pacific CDMO Industry Segmentation

Contract development and manufacturing organizations (CDMOs) in the pharmaceutical sector provide a comprehensive suite of services from drug development to manufacturing. They achieve this by undertaking outsourced projects and leveraging their expertise in development and manufacturing to serve clients. The study tracks and analyzes the demand for outsourcing CMO and CRO activities within the pharmaceutical sector based on the current trends and market dynamics. The market numbers have been derived by tracking the revenue generated by the players operating in the market who provide CRO & CMO services. The study provides a detailed breakdown of the various research phases and service types. This report analyzes the factors based on the prevalent base scenarios, key themes, and end-user vertical-related demand cycles.

The Asia-Pacific CDMO Market is segmented by service type CMO segment (active pharmaceutical ingredient (API) manufacturing [small molecule, large molecule, high potency (HPAPI)], finished dosage formulation (FDF) development and manufacturing [solid dose formulation (tablets and others), liquid dose formulation, and injectable dose formulation], and secondary packaging), research phase CRO Segment (pre-clinical, Phase I, Phase II, Phase III, and Phase IV), and country (Asia-Pacific (China, India, Japan, Australia, and Rest of Asia-Pacific)). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Service Type CMO Segment | ||||||||

| ||||||||

| ||||||||

| Secondary Packaging |

| By Research Phase CRO Segment | |

| Pre-clinical | |

| Phase I | |

| Phase II | |

| Phase III | |

| Phase IV |

| By Country | |

| China | |

| Japan | |

| India | |

| Australia and New Zealand |

Asia-Pacific CDMO Market Size Summary

The Asia-Pacific CDMO market is experiencing significant expansion, driven by the increasing demand for pharmaceutical products and the trend of outsourcing drug development and manufacturing. This growth is supported by strong government incentives and foreign investments, particularly in emerging markets like China, India, and South Korea. These countries are witnessing a rise in chronic diseases and an aging population, which are fueling the demand for pharmaceuticals and, consequently, CDMO services. The region's cost-effective manufacturing capabilities compared to North America and Europe further enhance its appeal as a preferred destination for CDMO activities. However, the market faces challenges such as labor shortages and rising labor costs, which have led some Western CDMOs to reconsider their operational locations.

The demand for injectable drugs, especially in cancer research and diabetes treatment, is a key driver of growth in the Asia-Pacific CDMO market. The region is seeing a surge in the production of sterile injectables, driven by the rising need for cell and gene therapies. India's pharmaceutical sector, with its strong focus on active pharmaceutical ingredients and bulk pharmaceuticals, is a significant player in the global CDMO market. The country is attracting substantial foreign investment, supported by favorable government policies, and is home to numerous FDA-approved manufacturing facilities. The market is characterized by the presence of major players like Catalent Inc., Samsung Biologics, and WuXi Biologics, who are expanding their operations to meet the growing demand for contract development and manufacturing services.

Asia-Pacific CDMO Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Attractiveness - Porter's Five Forces Analysis

-

1.2.1 Porter's Five Forces Analysis for CMO

-

1.2.1.1 Bargaining Power of Suppliers

-

1.2.1.2 Bargaining Power of Buyers

-

1.2.1.3 Threat of New Entrants

-

1.2.1.4 Threat of Substitute Products

-

1.2.1.5 Intensity of Competitive Rivalry

-

-

1.2.2 Porter's Five Forces Analysis for CRO

-

1.2.2.1 Bargaining Power of Suppliers

-

1.2.2.2 Bargaining Power of Buyers

-

1.2.2.3 Threat of New Entrants

-

1.2.2.4 Threat of Substitute Products

-

1.2.2.5 Intensity of Competitive Rivalry

-

-

-

1.3 Industry Policies

-

1.4 Industry Value Chain Analysis

-

1.5 Market Dynamics

-

1.5.1 Market Drivers

-

1.5.1.1 Increasing Outsourcing Volume by Big Pharmaceutical Companies

-

1.5.1.2 Increasing Investment in Research and Development

-

-

1.5.2 Market Restraints

-

1.5.2.1 Increasing Lead Time Owing to Supply Chain Related Constraints in the Region

-

1.5.2.2 Skilled Labour Shortages Across the Region

-

-

-

1.6 Qualitative Coverage on the 3D Printing Developments in the OSD Segment

-

1.6.1 Evolution of 3D Printing in Fabrication Processes and the Key Advantages Over Conventional Processes

-

1.6.2 Analysis of Major Drugs Manufactured Using 3D Printing-based Process

-

1.6.3 Analysis of Key Techniques Deployed (SLS & FDM), Along with their Relative Advantages

-

1.6.4 Key Developments on Stakeholders

-

-

1.7 Technology Snapshot

-

1.7.1 Dosage Formulation Technologies

-

1.7.2 Dosage Forms by Route of Administration

-

1.7.3 Key Considerations for Outsourcing of Pharmaceutical R&D

-

1.7.4 Major Segments in CRO Bio Analytical Testing, Central Laboratory Testing, and cGMP Testing

-

-

-

2. MARKET SEGMENTATION

-

2.1 By Service Type CMO Segment

-

2.1.1 Active Pharmaceutical Ingredient (API) Manufacturing

-

2.1.1.1 Small Molecule

-

2.1.1.2 Large Molecule

-

2.1.1.3 High Potency (HPAPI)

-

-

2.1.2 Finished Dosage Formulation (FDF) Development and Manufacturing

-

2.1.2.1 Solid Dose Formulation

-

2.1.2.1.1 Tablets

-

2.1.2.1.2 Others

-

-

2.1.2.2 Liquid Dose Formulation

-

2.1.2.3 Injectable Dose Formulation

-

-

2.1.3 Secondary Packaging

-

-

2.2 By Research Phase CRO Segment

-

2.2.1 Pre-clinical

-

2.2.2 Phase I

-

2.2.3 Phase II

-

2.2.4 Phase III

-

2.2.5 Phase IV

-

-

2.3 By Country

-

2.3.1 China

-

2.3.2 Japan

-

2.3.3 India

-

2.3.4 Australia and New Zealand

-

-

Asia-Pacific CDMO Market Size FAQs

How big is the Asia-Pacific CDMO Market?

The Asia-Pacific CDMO Market size is expected to reach USD 71.60 billion in 2024 and grow at a CAGR of 8.60% to reach USD 108.17 billion by 2029.

What is the current Asia-Pacific CDMO Market size?

In 2024, the Asia-Pacific CDMO Market size is expected to reach USD 71.60 billion.