Market Trends of Asia-Pacific Bunker Fuel Industry

This section covers the major market trends shaping the APAC Bunker Fuel Market according to our research experts:

VLSFO to Witness Significant Growth

- Marine fuel containing less than 0.5% of sulfur is generally termed as very-low sulfur fuel oil. From January 1, 2020, HSFO can only be used in ships having scrubbers installed to reduce the emissions, which will drive the demand of VLSFO.

- Most of the high-sulfur fuel oil (HSFO) bunker fuel market is expected to be shortly replaced by low-sulfur alternatives. Most of the VLSFO available in the market is blended from residual and distillate components, which are blended with various cutters of varying sulfur and viscosity to create an on-specification product.

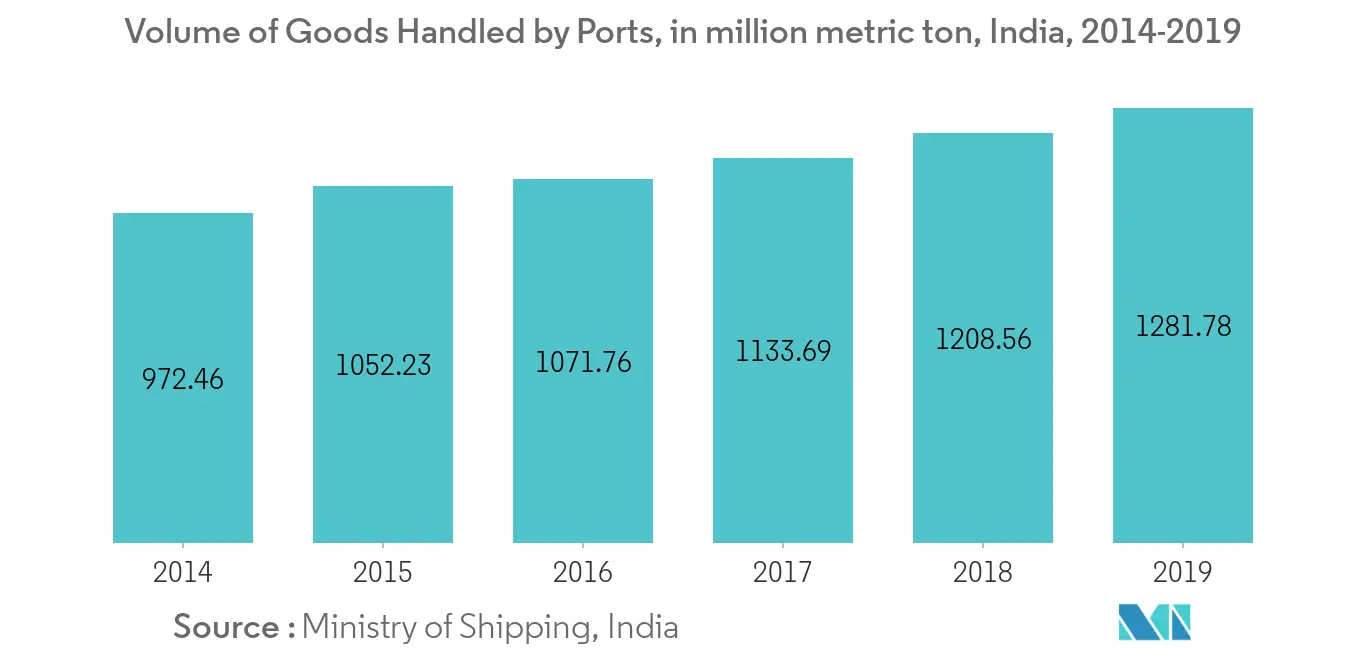

- India is one of the major trading markets is witnessing continuous growth in the volume of goods being handled at ports. In 2019, the nation reported 1281 million metric tons of products through different ports. Post pandemic, the market is likely to boost the demand for VLSFO.

- In India, to meet the demand for VLSFO, Indian Oil Corp. stated its ambition to produce one million metric ton of IMO-complaint very low sulfur fuel oil in 2020.

- The demand for VLSFO declined after January 2020 due to global supply chain disruptions, a decrease in demand for general goods and products, lockdown implementation in most of the countries, and a global economic slowdown.

- The need for VLSFO is likely to recover significantly after mid-2021. Post-2020, the demand is expected to rise on account of the opening of all the trade routes and relative price rise.

Understand The Key Trends Shaping This Market

Download PDF

China to Dominate the Market

- China is the biggest exporter and the second-largest importer of the goods by value. China's major exports are mechanical and electric machinery and equipment, automotive products including vehicle parts, chemicals and plastics, iron and steel articles, and furniture, among others.

- From 2016-2018, the Chinses exports increased from USD 2.12 trillion to USD 2.5 trillion, driven primarily by an increase in imports from the US and Japan. Chinese exports to the United States and Japan increased by 23.6% and 13.74%, respectively, during 2016-2018.

- With the increasing demand for energy, especially in nations like China and India, trading for crude oil and natural gas is likely to get an increase over the forecast period, which in turn is expected to increase the demand for tankers.

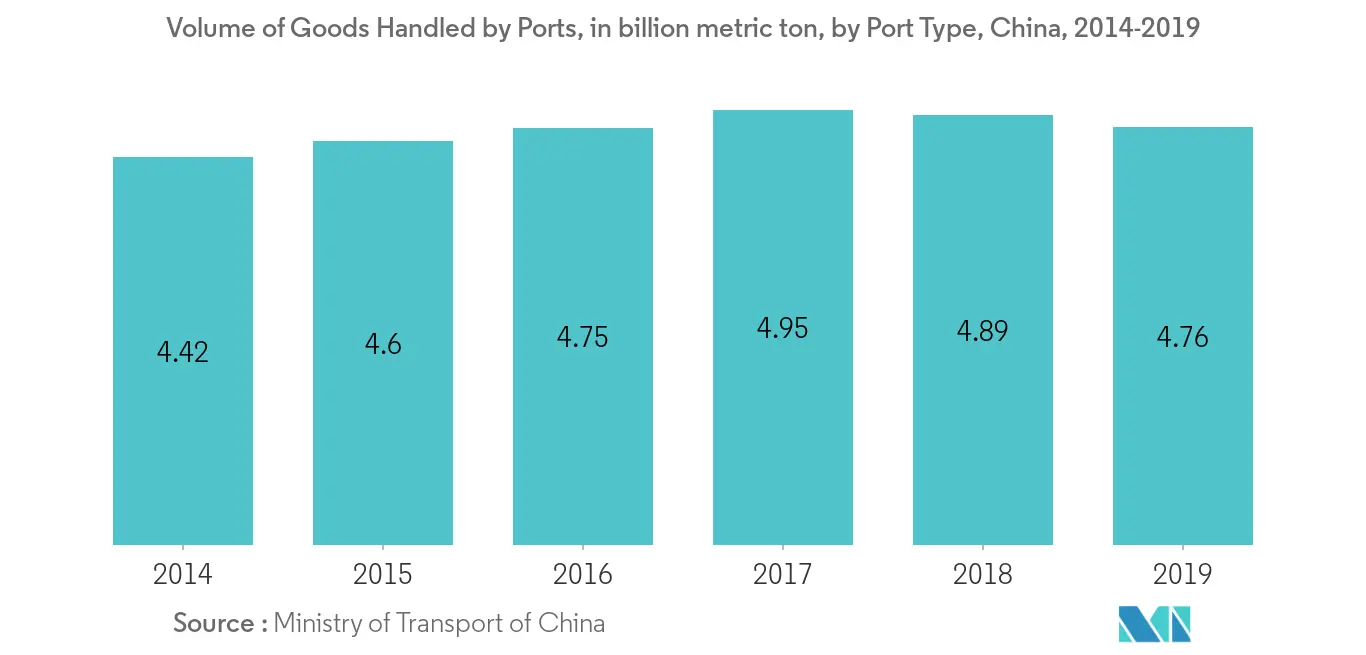

- Despite a slight decline in the volume of goods handled by the river and coastal ports in 2019, China managed more than 13.5 billion metric tons of products. With large export and

- However, the fleet in the country is registering a situation of drastic slowdown and oversupply. During Q1 2020, the container volume at the major Chinese ports has declined by 8.9% compared to 2019. The most significant drop in the traffic was registered by the China-US route and China-Japan/South Korea route.

- Additionally, the trade tension began between the United States and China in 2018 due to the setting of high tariffs and other trade barriers, which is expected to restrain the market. Moreover, the COVID-19 is pushing the market downwards further, restraining the market growth.

Get Analysis on Important Geographic Markets

Download PDF