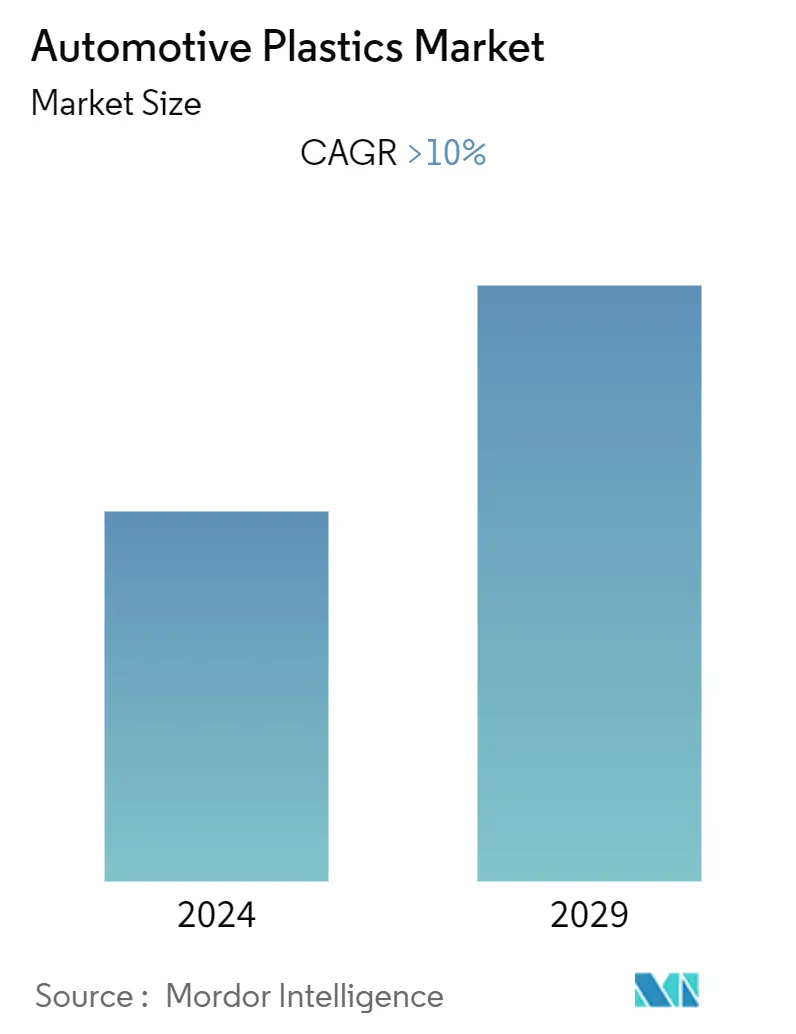

Automotive Plastics Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| CAGR (2024 - 2029) | > 10.00 % |

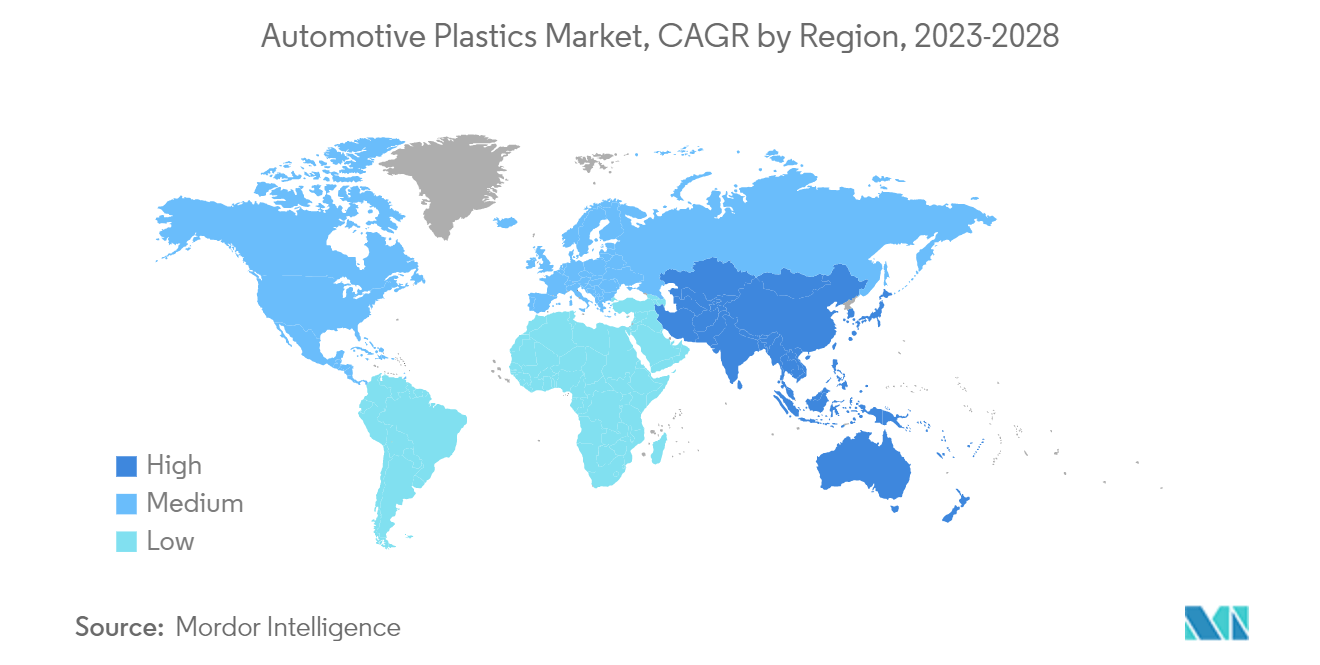

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

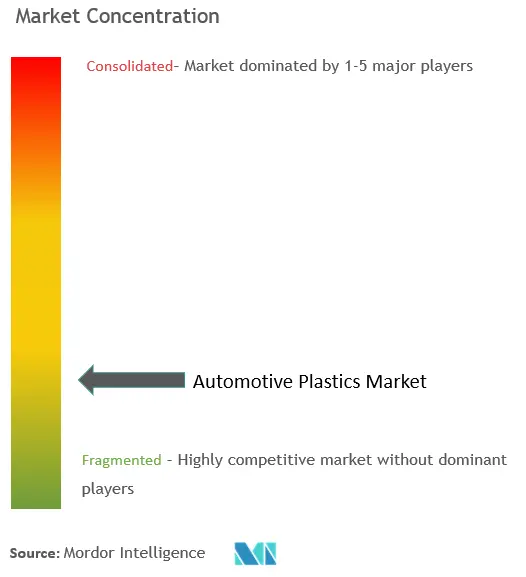

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Automotive Plastics Market Analysis

The Automotive Plastics Market is expected to register a CAGR of greater than 10% during the forecast period.

COVID-19 negatively impacted the market in 2020. However, the market reached pre-pandemic levels in 2022 and is expected to grow steadily in the future.

- The increasing demand for lightweight and electric vehicles is expected to drive the demand for the market during the forecast period. On the flip side, challenges associated with plastic recycling are likely to hinder the market's growth.

- Technological development in electric vehicles is projected to act as an opportunity for the market in the future. The Asia-Pacific region dominates the global market due to increased demand for electric vehicles in the region.

Automotive Plastics Market Trends

High Demand in Automotive Applications

- Plastic can act as an electric conductor and insulator (mainly insulator). It plays a vital role in various under-bonnet applications concerning propulsion, alternative drive systems, and batteries. Plastics make electric and hybrid automotive batteries more affordable and add value by replacing heavy electric cells with compensatory light-weighting.

- The plastic sensors, harnesses, connectors, seals, fuses, and capacitors used in 'under-the-hood' applications in hybrid or electric vehicles help consolidate parts, resist corrosion, and reduce noise. Hybridization (the use of combined gas and electric propulsion system) has already increased the demand for efficiency, battery longevity, weight, space savings, and safety standards in the automotive sector.

- Electric vehicle manufacturers now acknowledge consumers' demand for driving ranges similar to gasoline vehicles. Plastic innovations are already assisting manufacturers with this demand. Lithium-ion battery packs, Ni-MH battery packs, and snap-fit li-ion battery cell packs are all made possible with plastics.

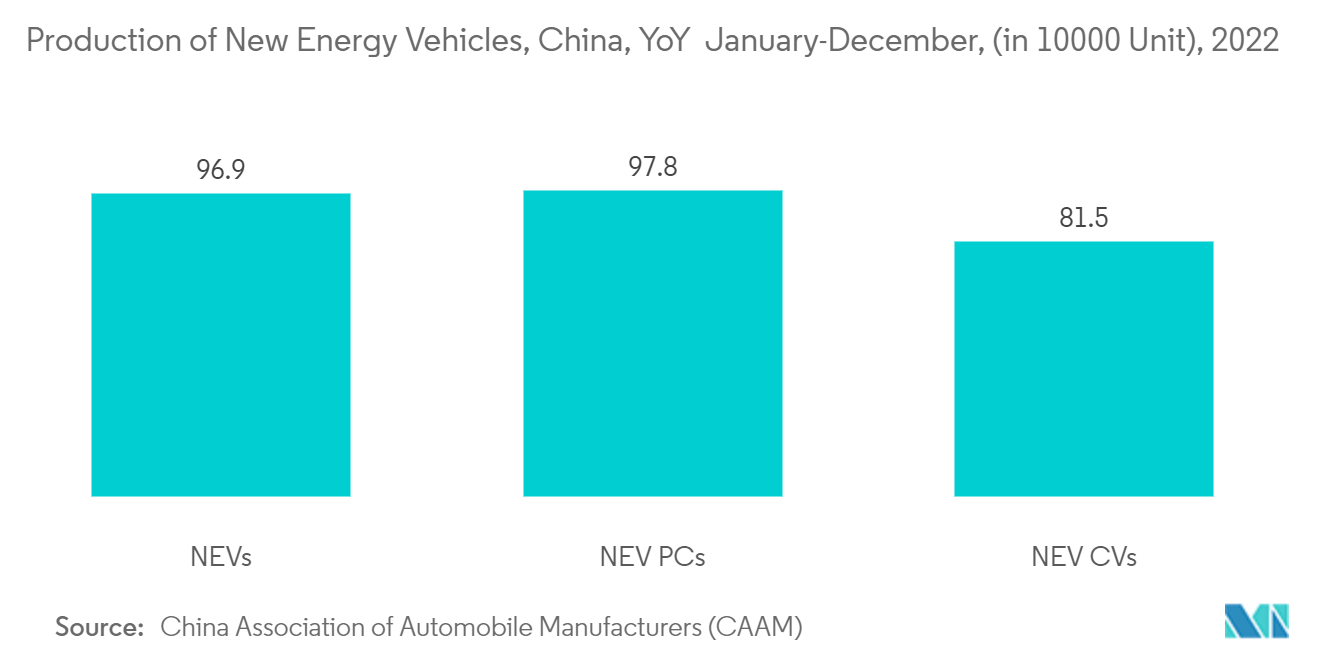

- China is a global leader in the electric car market, with a significant increase in the sales of new electric vehicles. A total of 3.3 million units of electric vehicles (EVs) were sold in China in 2021, registering an increase of 154% compared to 1.3 million units sold in 2020.

- Further, according to the China Association of Automobile Manufacturing (CAAM), the production of new electric vehicles (NEVs) in the country witnessed a year-on-year increase of 96.9 percent in December 2022. Thus, the expanding electric vehicle market is expected to increase the demand for automotive plastics in the country.

- Therefore, from the above-mentioned points, under bonnet application is expected to witness high demand during the forecast period.

Asia-Pacific Region is expected to Dominate the Market

- The Asia-Pacific region is expected to dominate the global market. With the increase in demand for lightweight vehicles and a large automotive production base in countries such as China, India, and Japan, the usage of automotive plastics is increasing in the region.

- China continues to be the world's largest vehicle market by both annual sales and manufacturing output. According to the China Association of Automobile Manufacturers (CAAM) statistical analysis, China produced about 2.9 million battery-electric vehicles in 2021, up 166% from the previous year. Around 601,000 plug-in hybrid vehicles were produced in China in the same year, up 131% from the year before.

- Furthermore, according to the latest data published by the Society of Indian Automobile Manufacturers (SIAM), the country witnessed a significant increase in the production of passenger vehicles. For instance, the production of passenger vehicles reached 3,650,698 for 2021-2022, representing an increase of 19% compared to 2020-21, positively impacting the demand for automotive plastics in the region.

- Moreover, other countries in the region are putting efforts into enhancing the automotive sector by investing heavily in electric cars to achieve net zero emissions. For example, in Japan, over 8,600 of the 20,000 new electric vehicles delivered in 2021 were imported electric vehicles, supporting the market growth significantly.

- Hence, due to the above-mentioned reasons, Asia-Pacific is anticipated to dominate the market studied during the forecast period.

Automotive Plastics Industry Overview

The automotive plastics market is partially fragmented in nature. Some of the major players in the market include BASF SE, Covestro AG, Celanese Corporation, Borealis AG, and DSM, among others.

Automotive Plastics Market Leaders

BASF SE

Covestro AG

Celanese Corporation

Borealis AG

DSM

*Disclaimer: Major Players sorted in no particular order

Automotive Plastics Market News

- September 2022: Citroën and BASF unveiled their all-electric concept car oli [all-ë], a manifesto to how much can be saved by reducing weight and resource usage. BASF has been pursuing an ambitious sustainability strategy for years now. Some of the major cornerstones of this strategy include the ChemCyclingTM project on improving the chemical recycling of plastics, as well as the biomass balance approach, in which fossil resources are replaced with renewables in production.

- March 2022: Covestro AG started two polycarbonate compounding production lines at its Greater Noida plant near New Delhi in India. The new plants are intended to meet the growing demand for compounded plastics, particularly for the automotive, electrical, and electronics industries.

Automotive Plastics Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Demand for Lightweight Materials from Electric and Hybrid Vehicles

4.1.2 Other Drivers

4.2 Restraints

4.2.1 Challenges Associated with Plastic Recycling

4.2.2 Other Restraints

4.3 Industry Value-Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size in Volume)

5.1 Material

5.1.1 Polypropylene (PP)

5.1.2 Polyurethane (PU)

5.1.3 Polyvinyl Chloride (PVC)

5.1.4 Polyethylene (PE)

5.1.5 Acrylonitrile Butadiene Styrene (ABS)

5.1.6 Polyamides (PA)

5.1.7 Polycarbonate (PC)

5.1.8 Other Materials

5.2 Application

5.2.1 Exterior

5.2.2 Interior

5.2.3 Under Bonnet

5.2.4 Other Applications

5.3 Vehicle Type

5.3.1 Conventional/Traditional Vehicles

5.3.2 Electric Vehicles

5.4 Geography

5.4.1 Asia-Pacific

5.4.1.1 China

5.4.1.2 India

5.4.1.3 Japan

5.4.1.4 South Korea

5.4.1.5 Rest of Asia-Pacific

5.4.2 North America

5.4.2.1 United States

5.4.2.2 Canada

5.4.2.3 Mexico

5.4.2.4 Rest of North America

5.4.3 Europe

5.4.3.1 Germany

5.4.3.2 United Kingdom

5.4.3.3 France

5.4.3.4 Italy

5.4.3.5 Rest of Europe

5.4.4 South America

5.4.4.1 Brazil

5.4.4.2 Argentina

5.4.4.3 Rest of South America

5.4.5 Middle-East and Africa

5.4.5.1 Saudi Arabia

5.4.5.2 South Africa

5.4.5.3 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Colaborations and Agreements

6.2 Market Share(%)**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Asahi Kasei Advance Corporation

6.4.2 BASF SE

6.4.3 Borealis AG

6.4.4 Braskem

6.4.5 Celanese Corporation

6.4.6 Covestro AG

6.4.7 Daicel Corporation

6.4.8 DuPont

6.4.9 DSM

6.4.10 Exxon Mobil Corporation

6.4.11 LANXESS

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Technological Development in Electric Vehicles

Automotive Plastics Industry Segmentation

Plastics are majorly processed into automotive components and parts owing to their ease of manufacturing, possible sourcing from renewable raw materials, and relative ease of improved design. Further, automotive plastics play a crucial role in performance and safety innovations in commercial vehicles, heavy motor vehicles (HMVs), modern cars, and sport utility vehicles (SUVs).

The automotive plastics market is segmented by material, application, vehicle type, and geography. By material, the market is segmented into polypropylene, polyurethane, polyvinyl chloride, polyethylene, acrylonitrile butadiene styrene, polyamides, polycarbonate, and other materials. By application, the market is segmented into the interior, exterior, under-bonnet, and other applications. By vehicle type, the market is segmented into conventional/traditional vehicles and electric vehicles. The report also covers the market size and forecasts for automotive plastics in 15 countries across major regions.

For each segment, the market sizing and forecasts have been done based on volume (metric tons).

| Material | |

| Polypropylene (PP) | |

| Polyurethane (PU) | |

| Polyvinyl Chloride (PVC) | |

| Polyethylene (PE) | |

| Acrylonitrile Butadiene Styrene (ABS) | |

| Polyamides (PA) | |

| Polycarbonate (PC) | |

| Other Materials |

| Application | |

| Exterior | |

| Interior | |

| Under Bonnet | |

| Other Applications |

| Vehicle Type | |

| Conventional/Traditional Vehicles | |

| Electric Vehicles |

| Geography | |||||||

| |||||||

| |||||||

| |||||||

| |||||||

|

Automotive Plastics Market Research FAQs

What is the current Automotive Plastics Market size?

The Automotive Plastics Market is projected to register a CAGR of greater than 10% during the forecast period (2024-2029)

Who are the key players in Automotive Plastics Market?

BASF SE, Covestro AG, Celanese Corporation, Borealis AG and DSM are the major companies operating in the Automotive Plastics Market.

Which is the fastest growing region in Automotive Plastics Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Automotive Plastics Market?

In 2024, the Asia-Pacific accounts for the largest market share in Automotive Plastics Market.

What years does this Automotive Plastics Market cover?

The report covers the Automotive Plastics Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Automotive Plastics Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

What are the key trends in the Automotive Plastics Market?

The key trends in the Automotive Plastics Market are: a) Increased demand for lightweight materials, including plastics b) Advancements in plastic material technologies, including high-performance polymers and reinforced composites

Automotive Polymers Industry Report

The global automotive plastics market is witnessing substantial growth, driven by factors such as stringent emission and fuel economy regulations prompting the adoption of lightweight materials, and the rising trend of vehicle electrification. The use of advanced plastic materials in vehicles enhances fuel economy while maintaining safety and performance. The market is further propelled by the growing demand for comfort features in vehicle interiors, with plastics offering impact resistance, dimensional stability, and aesthetic appeal. Additionally, the high capital and infrastructure costs for re-engineering plastics pose a significant challenge. Despite these hurdles, growth opportunities are particularly prevalent in the Asia Pacific region, the largest consumer of automotive plastics. Mordor Intelligence™ Industry Reports provide statistics for the Automotive Polymers market share, size, and revenue growth rate, including a market forecast and historical overview. A sample of this industry analysis is available as a PDF download.