Market Size of Asia-Pacific Agricultural Tractors Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

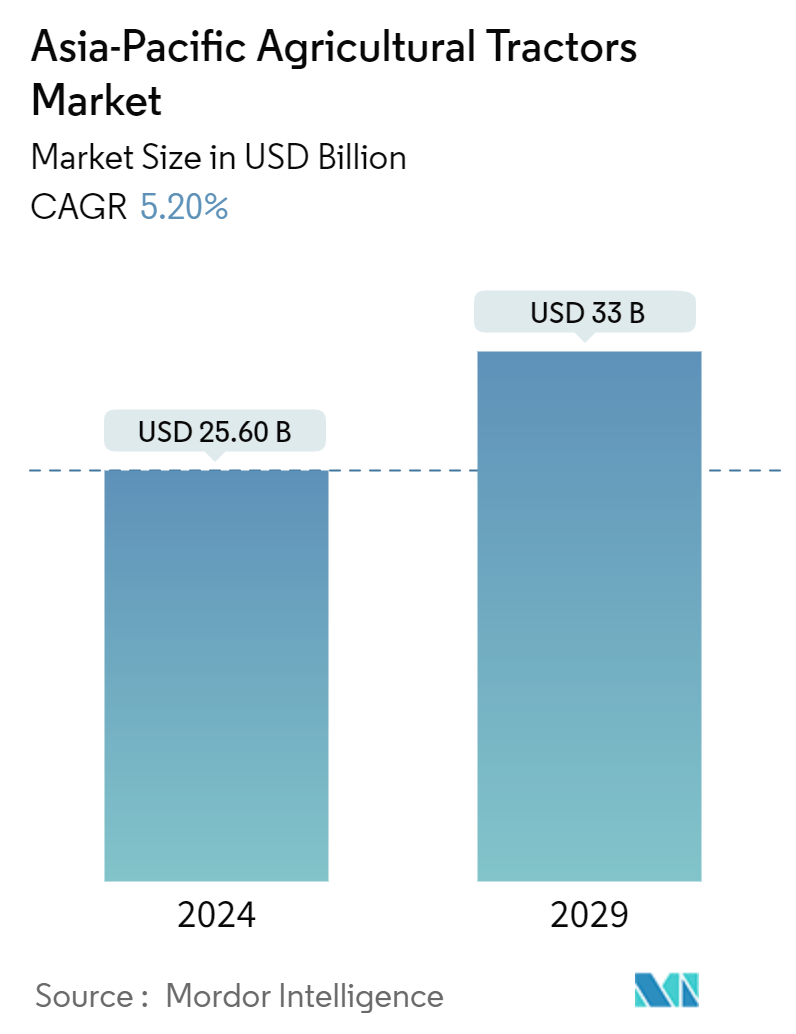

| Market Size (2024) | USD 25.60 Billion |

| Market Size (2029) | USD 33 Billion |

| CAGR (2024 - 2029) | 5.20 % |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Asia-Pacific Agricultural Tractors Market Analysis

The Asia-Pacific Agricultural Tractors Market size is estimated at USD 25.60 billion in 2024, and is expected to reach USD 33 billion by 2029, growing at a CAGR of 5.20% during the forecast period (2024-2029).

- Farming remains a crucial occupation in many Asian countries, deeply rooted in their cultural and economic fabric. As urbanization and technological advancements progress, the adoption of agricultural machinery, including tractors, is increasing. The tractor market in Southeast Asia is driven by factors such as growing farm labor shortages, rising wages, and government support for farm mechanization. In 2023, the Indonesian government allocated USD 538 million for machinery development, which includes tractor production. Similarly, In Thailand, government support is a primary driver of significant market growth. Initiatives like the Thailand 20-Year Strategic Plan 2017-2036 and Thailand 4.0, which focus on developing Smart Farmers, Smart Enterprises, and Smart Offices, include agricultural investment strategies and supportive policies that encourage new tractor acquisitions.

- The agricultural tractor machinery market in the region is propelled by the preference for farm mechanization in developing countries, which is necessary to meet increased agricultural production and food security demands. Government initiatives providing sufficient credit facilities also contribute to this growth. In Bangladesh, the Department of Agricultural Extension (DAE) reported that in 2022, approximately 95% of the land would be cultivated using pedestrian and wheeled tractors, with a notable increase in demand for higher horsepower tractors. Thus, these factors are anticipated to drive the market growth.

Asia-Pacific Agricultural Tractors Industry Segmentation

A tractor is an industrial vehicle with one or two small wheels in front and two large wheels at the back for agricultural and other functions. It is used to move the attached implement that plows the field or performs different activities. For this report, tractors used in agricultural operations have been considered. The report does not cover other farm machinery and attachments to tractors. Tractors used for industrial and construction purposes are also excluded from the study.

Asia-Pacific agricultural tractor market is segmented by horsepower (less than 25 HP, 25-100 HP, and above 100 HP), type (orchard tractors, row crop tractors, and other types), and Geography ( China, India, Japan, Australia, and rest of Asia-Pacific). The report offers market size and forecasts for all the above segments in terms of value (USD).

| Horse Power | |

| Below 25 HP | |

| 25 HP to 100 HP | |

| Above 100 HP |

| Type | |

| Orchard Tractors | |

| Row Crop Tractors | |

| Other Types |

| Geography | |

| China | |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific |

Asia-Pacific Agricultural Tractors Market Size Summary

The Asia-Pacific agricultural tractor market is experiencing growth driven by increased farm mechanization efforts in developing countries, aimed at enhancing agricultural production and ensuring food security. Government initiatives, such as credit facilities and subsidies, are further propelling the market. Countries like China and India are at the forefront of this growth, with China implementing policies like the 'Agricultural Mechanization Promotion Law' and the 'Made in China 2025' scheme to boost domestic production of high-end agricultural equipment. In India, the government is promoting 'Balanced Farm Mechanization' through subsidies and support for bulk purchases, which is expected to strengthen the tractor market. Bangladesh is also witnessing a shift towards automation, with a significant portion of land being tilled using tractors, supported by government-subsidized sales.

The market is characterized by a consolidated landscape with major players such as Mahindra & Mahindra Ltd, AGCO Corporation, Deere & Company, and others holding significant shares. These companies are actively engaging in strategies like partnerships, mergers, acquisitions, and product launches to expand their market presence. For instance, the collaboration between Escorts Ltd and Kubota Corporation has facilitated technology sharing and joint manufacturing of tractors in India. Additionally, innovative product offerings, such as Mahindra & Mahindra's ARJUN NOVO 605 DI-I, are being introduced to meet regional demands. These developments are expected to further augment tractor sales across the Asia-Pacific region during the forecast period.

Asia-Pacific Agricultural Tractors Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.2.1 Increasing Farm Mechanization Rates

-

1.2.2 Growing Government Support to Enhance Farm Mechanization

-

1.2.3 Rising Trend of Custom Hiring of Tractors

-

-

1.3 Market Restraints

-

1.3.1 Lack of Awareness and Skilled Manpower

-

1.3.2 High Initial Cost for Purchase of Tractor

-

-

1.4 Industry Attractiveness - Porter's Five Forces Analysis

-

1.4.1 Bargaining Power of Suppliers

-

1.4.2 Bargaining Power of Buyers

-

1.4.3 Threat of New Entrants

-

1.4.4 Threat of Substitutes

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION

-

2.1 Horse Power

-

2.1.1 Below 25 HP

-

2.1.2 25 HP to 100 HP

-

2.1.3 Above 100 HP

-

-

2.2 Type

-

2.2.1 Orchard Tractors

-

2.2.2 Row Crop Tractors

-

2.2.3 Other Types

-

-

2.3 Geography

-

2.3.1 China

-

2.3.2 India

-

2.3.3 Japan

-

2.3.4 Australia

-

2.3.5 Rest of Asia-Pacific

-

-

Asia-Pacific Agricultural Tractors Market Size FAQs

How big is the Asia-Pacific Agricultural Tractors Market?

The Asia-Pacific Agricultural Tractors Market size is expected to reach USD 25.60 billion in 2024 and grow at a CAGR of 5.20% to reach USD 33 billion by 2029.

What is the current Asia-Pacific Agricultural Tractors Market size?

In 2024, the Asia-Pacific Agricultural Tractors Market size is expected to reach USD 25.60 billion.