Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

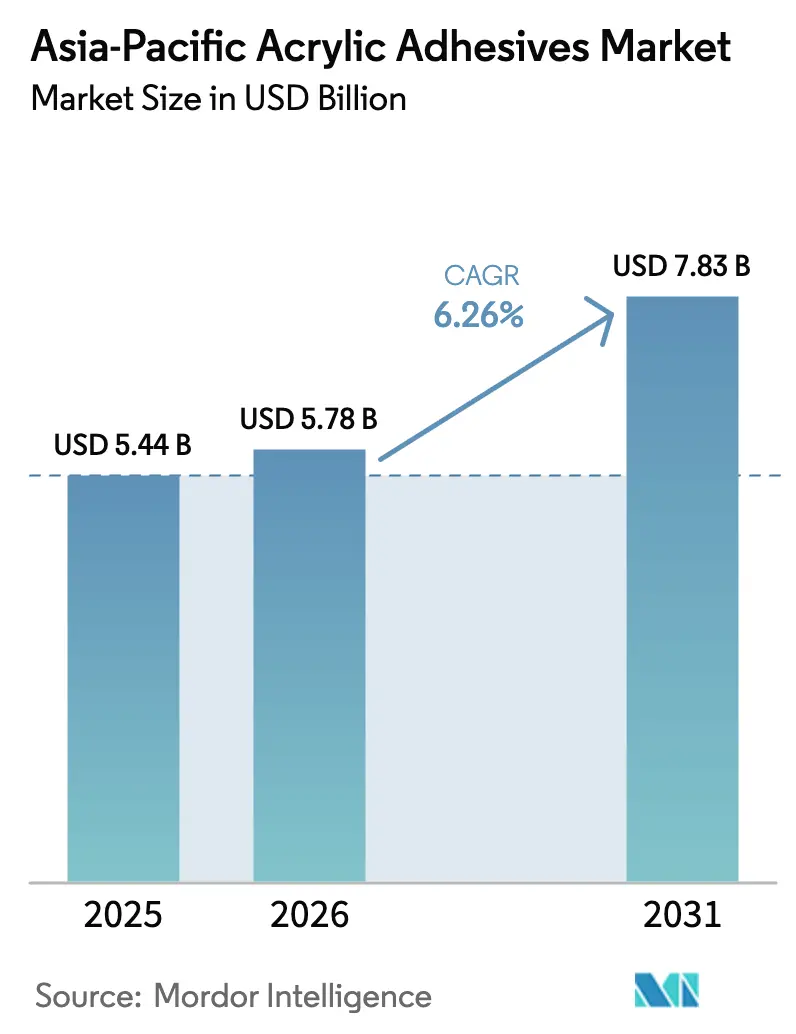

| Base Year Market Size (2025) | USD 5.44 Billion |

| Market Size (2026) | USD 5.78 Billion |

| Market Size (2031) | USD 7.83 Billion |

| Growth Rate (2026 - 2031) | 6.26% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Acrylic Adhesives Market Analysis by Mordor Intelligence

The Asia-Pacific Acrylic Adhesives Market size is projected to expand from USD 5.44 billion in 2025 and USD 5.78 billion in 2026 to USD 7.83 billion by 2031, registering a CAGR of 6.26% between 2026 and 2031. Expanding e-commerce packaging, accelerating electric-vehicle component assembly, and tighter regional VOC (Volatile Organic Compound) regulations underpin steady volume growth. Packaging lines continue to specify water-borne acrylic chemistries because they meet recyclability targets and deliver rapid peel-seal performance, while battery makers adopt thermally conductive acrylic hybrids that dissipate heat in cell-to-pack designs. Producers are also relocating capacity toward Thailand, Malaysia, and Vietnam to capture double-digit tax incentives that lower effective capex on new reactors. Feedstock cost swings, however, still compress margins, with 2025 methyl methacrylate prices falling 21% before rebounding in early 2026 on Middle-East supply shocks.

Key Report Takeaways

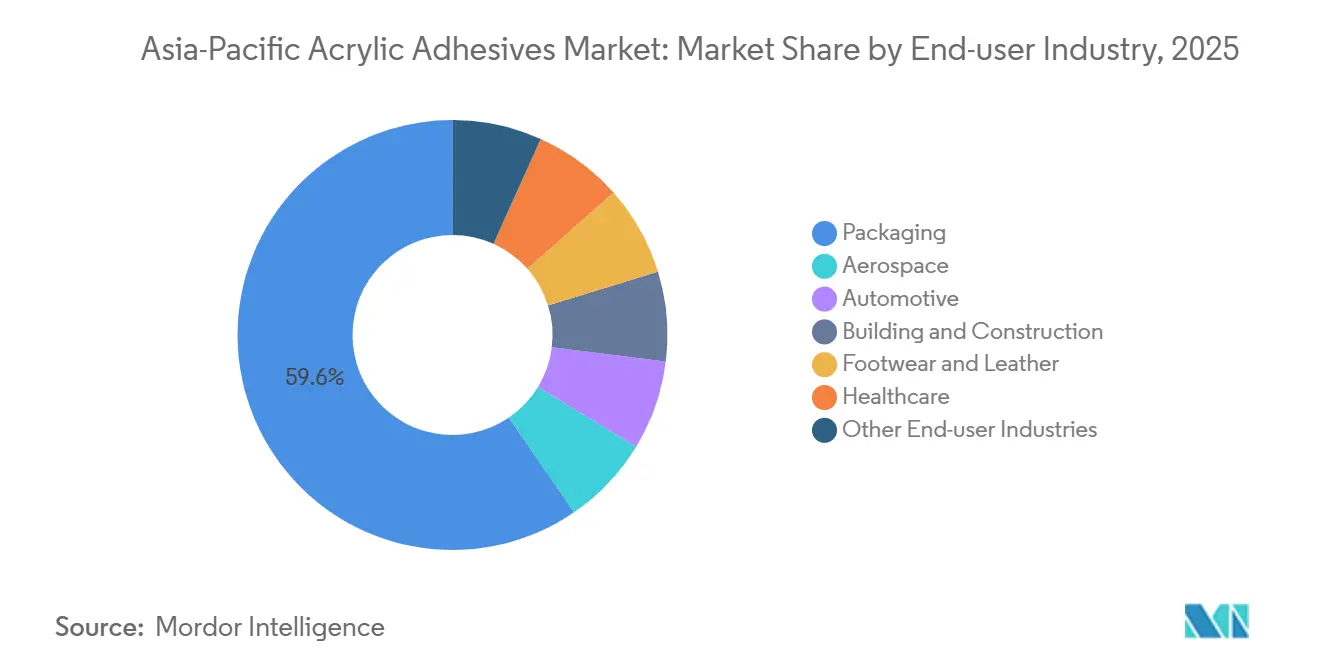

- By end-user industry, packaging led with 59.56% revenue share in 2025; automotive is advancing at a 6.72% CAGR through 2031.

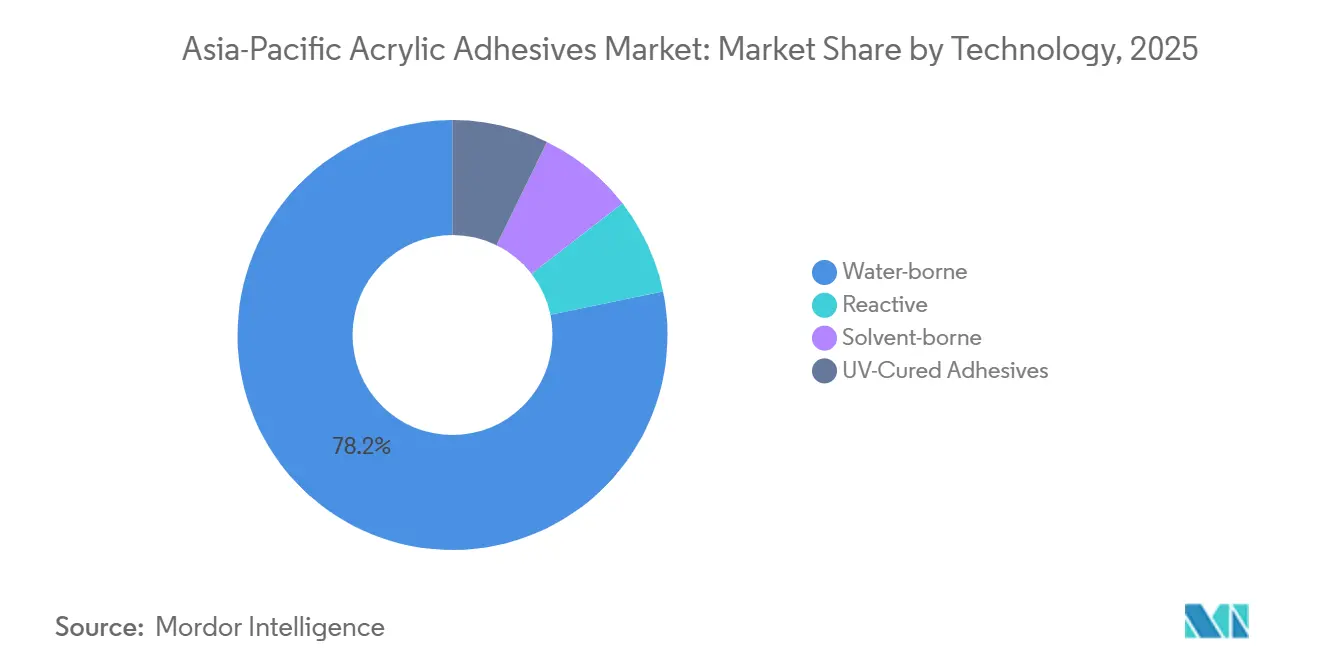

- By technology, water-borne formulations held 78.24% share in 2025 and are expanding at 7.15% CAGR to 2031.

- By country, China commanded 48.27% share in 2025, while India is projected to post the fastest 7.48% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Acrylic Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Electric Vehicle and electronics manufacturing in China-led hubs | +1.8% | China, South Korea, Japan; spillover to ASEAN battery-assembly hubs | Medium term (2-4 years) |

| Regulatory push toward low-VOC, water-borne systems | +1.5% | China, Singapore, Malaysia; EU export-compliance alignment | Long term (≥ 4 years) |

| Expansion of flexible packaging for e-commerce fulfillment | +1.3% | APAC-wide, concentrated in China, India, Southeast Asia logistics corridors | Short term (≤ 2 years) |

| Mega construction projects across India and ASEAN | +1.0% | India, Vietnam, Philippines, Indonesia, Malaysia | Medium term (2-4 years) |

| ASEAN tax-holiday schemes catalyzing local adhesive output | +0.7% | Thailand, Malaysia, Vietnam, Indonesia (EEC, SEZs, BOI zones) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Electric Vehicle and Electronics Manufacturing

Battery-cell production remains the principal catalyst for specialty acrylic demand. CATL shipped 661 GWh of lithium-ion batteries in 2025 at 96.9% utilization, prompting adhesive developers to supply thermally conductive, vibration-resistant acrylic hybrids that bond cells directly to pack enclosures[1]Battery-Tech Network, “CATL Expands Overseas Battery Footprint,” battery-technetwork.com. Hubei Huitian invested RMB 97.68 million (USD 13.59 million) in 2025 for a new latex binder line and partnered with Tailan New Energy on solid-state battery adhesives that will reach commercial scale after 2027. Semiconductor localization amplifies the pull; NANPAO formed a 2025 joint venture to formulate ultra-low outgassing chip-package adhesives suited to advanced nodes. South Korea’s market for silicon-carbide power-chip adhesives is projected to triple to KRW 850 billion (USD 598.4 million) by 2030, sustaining demand for nano-silver and acrylic-based die attach solutions.

Regulatory Push Toward Low-VOC, Water-Borne Systems

China’s GB 33372-2020 limits solvent-borne acrylics to 510 g/L VOC, whereas water-borne analogs must stay below 50 g/L in indoor uses, forcing widespread line conversions to emulsion polymerization and longer oven zones[2]State Administration for Market Regulation, “GB 33372-2020 Architectural Coatings VOC Limits,” samr.gov.cn. Singapore’s Super Low-Energy building program and Malaysia’s Green Technology Investment Allowance reinforce similar thresholds, encouraging formulators to certify products under ISO 14024 ecolabels. The European Union Packaging and Packaging Waste Regulation, effective 2025, adds an external compliance lever because Asia-made flexible packs must hit 30% recycled content by 2030. BASF’s Acrodur resins showcased at CHINAPLAS 2025 demonstrate the commercial pivot, offering thermally crosslinkable, formaldehyde-free water-borne acrylics compatible with 75% regenerated fibers.

Expansion of Flexible Packaging for E-Commerce Fulfillment

Laminate converters favor acrylic emulsions that provide tamper-evident seals across polyethylene and paper without sacrificing recyclability. Arkema’s December 2024 acquisition of Dow’s flexible-packaging adhesive assets signaled a consolidation wave centered on water-based and solvent-free chemistries. Quick-commerce grocery services, expanding at a high CAGR, demand moisture-resistant paper mailers where acrylic emulsions deliver barrier performance yet repulp cleanly at mill re-entry.

Mega Construction Projects Across India and ASEAN

India’s National Infrastructure Pipeline, paired with relaxed FDI caps, underpins rising consumption of tile-bonding and façade adhesives. Pidilite recorded 11% year-on-year sales growth in Q3 FY26 and plans a 200,000-ton Punjab plant by December 2027, primarily for water-based acrylics. Malaysia’s 10.3% jump in non-residential building during 2025 and Vietnam’s 6.9% average construction growth fuel demand for rapid-cure acrylic formulations suited to robotic panel assembly. ASEAN tax holidays, such as Thailand’s 15-year CIT exemption, cut effective project costs up to 50%, accelerating local reactor build-outs

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acrylic-monomer price volatility and feedstock risk | -1.20% | APAC-wide, acute in China, Japan, South Korea dependent on Middle East naphtha/methanol | Short term (≤ 2 years) |

| Intensifying PU and epoxy substitution in high-strength joints | -0.80% | Japan, South Korea aerospace/automotive; China composite manufacturing | Medium term (2-4 years) |

| Compliance cost of solvent-borne VOC abatement | -0.60% | China, Singapore, Malaysia, ASEAN export-compliance markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Acrylic-Monomer Price Volatility and Feedstock Risk

Methyl methacrylate prices fell to USD 1,275 per ton by December 2025, 21% below January, before Mitsubishi Chemical announced a price rise in March 2026 as Middle-East tensions disrupted naphtha flows that supply over 60% of regional cracker feedstock. BASF followed with USD 100 per ton acrylate increases in March 2026, citing higher logistics and energy outlays. Such whipsaw movements erode forward-pricing visibility and drive formulators toward dual sourcing and higher safety stocks.

Intensifying PU and Epoxy Substitution in High-Strength Joints

Permabond’s ET5422 epoxy, launched in March 2026, delivers 320 N/25 mm peel strength, twelvefold more than typical acrylics, while maintaining thixotropic gap-fill properties critical to aerospace seat-track bonding. Huntsman’s EPIBOND 315 reaches 5,500 psi lap shear and 204°C service temperature, eating into acrylic share in composite fuselage assembly. Unless formulators adopt urethane-modified or silicone-acrylic hybrids, high-stress applications will continue to migrate to PU and epoxy systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-user Industry: Packaging Retains Leadership While Automotive Accelerates

Packaging commanded 59.56% of the Asia-Pacific acrylic adhesives market share in 2025. Rising parcel volumes from cross-border e-commerce and retailer commitments to curb single-use plastics sustain high-volume water-borne consumption in carton sealing and flexible laminations. The Asia-Pacific Acrylic Adhesives market size tied to automotive uses is expanding at the fastest CAGR of 6.72% duirng the forecast period (2026-2031) because lightweight multi-material bodies and silicon-carbide inverters need heat-resistant joints. Building and construction demand is diverging: China’s adhesive volumes soften with its 1.8% uptick in residential starts, but India, Vietnam, and Malaysia deliver mid-single-digit gains through data-center and semiconductor-fab work. Footwear exporters in India gain from the EU FTA tariff removal, spurring incremental acrylic purchases for PU-lined leather uppers.

By Technology: Water-Borne Dominates and UV-Cure Gains Niche Traction

Water-borne acrylics held 78.24% share in 2025 and will outpace the overall Asia-Pacific Acrylic Adhesives market at 7.15% CAGR through 2031. Their low-VOC profile aligns with GB 33372-2020 and similar ASEAN thresholds, and modern surfactant packages now deliver bond strengths comparable to solvent-based grades.

Reactive two-part acrylics and moisture cures continue to address structural assemblies where rapid fixture and toughness override cost. UV-cured grades, although below 4% volume, are rising fastest in medical and electronics lines because instant, on-demand curing slashes dwell time and facilitates inline optical inspection. BASF’s Acrodur family shows how thermally crosslinkable water-borne resins can also meet semi-structural requirements in automotive trim, compressing the performance gap with traditional reactive chemistries.

Geography Analysis

China’s scale anchors the Asia-Pacific acrylic adhesives market, yet the country contends with slowing residential builds and raw-material oversupply. BASF’s 400,000-ton butyl acrylate unit in Zhanjiang, commissioned in 2025, lowers import reliance and stabilizes pricing for domestic formulators. Enforcement of GB 33372-2020 accelerates a pivot toward water-borne lines, favoring large firms that can afford reactor upgrades.

India sustains the fastest trajectory, driven by the National Infrastructure Pipeline and confirmed by Pidilite’s INR 300 crore (USD 34.5 million) Punjab greenfield project slated for 2027 start-up. Tariff-free leather exports to the EU widen addressable volume for footwear glues, and customs duty exemptions on input chemicals through March 2028 ease cost pressures.

Japan and South Korea leverage high-margin electronics and automotive niches. LG Chem and Noritake target KRW 850 billion (USD 598.4 million) SiC power-chip adhesive sales by 2030, lifting regional demand for hybrid acrylics with superior thermal conductivity. The broader ASEAN bloc attracts green-field reactors aided by 5% concessionary tax rates in Malaysia’s JS-SEZ and 25-50% cash subsidies under Vietnam’s Investment Support Fund.

Competitive Landscape

The Asia-Pacific Acrylic Adhesives market is moderately fragmented. New entrants leverage fiscal incentives; Toyo Ink India will triple solvent-based output by April 2026 at its Gujarat site and intends to export across the Middle East and Africa. Digital labs and AI-driven quality monitoring give incumbents an operational edge, illustrated by Henkel’s Singapore facility that replicates customer processes for faster formulation cycles.

Asia-Pacific Acrylic Adhesives Industry Leaders

3M

Henkel AG & Co. KGaA

Arkema

Sika AG

H.B. Fuller Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Mitsui Chemicals ICT Materia, Inc. announced that it successfully employed a water-based acrylic adhesive to develop a new surface protective tape for use in fiber laser cutting.

- October 2025: UPM Adhesive Materials, a producer of acrylic adhesives, announced plans to inaugurate a slitting and distribution terminal in Northern Vietnam. This move underscores the company's ambition to bolster its presence in Southeast Asia, promising swift services to its Northern Vietnamese clientele.

Asia-Pacific Acrylic Adhesives Market Report Scope

Acrylic adhesive is a fast-curing, high-strength structural adhesive, often known as methyl methacrylate (MMA), designed for bonding diverse materials, including metals, plastics, and composites. It is known for its resistance to weathering, moisture, UV light, and chemicals, making it ideal for both structural indoor and outdoor applications.

The Asia-Pacific Acrylic Adhesives market report is segmented by end-user industry, technology, and country. By end-user industry, the market is segmented into aerospace, automotive, building and construction, footwear and leather, healthcare, packaging, and other end-user industries. By Technology, the market is segmented into reactive, solvent-borne, UV-cured adhesives, and water-borne. The report also covers market sizes and forecasts for 9 countries across the region. The market sizes and forecasts are provided in terms of value (USD).

By End-user Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Footwear and Leather |

| Healthcare |

| Packaging |

| Other End-user Industries |

By Technology

| Reactive |

| Solvent-borne |

| UV-Cured Adhesives |

| Water-borne |

By Country

| Australia |

| China |

| India |

| Indonesia |

| Japan |

| Malaysia |

| Singapore |

| South Korea |

| Thailand |

| Rest of Asia-Pacific |

| By End-user Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Footwear and Leather | |

| Healthcare | |

| Packaging | |

| Other End-user Industries | |

| By Technology | Reactive |

| Solvent-borne | |

| UV-Cured Adhesives | |

| Water-borne | |

| By Country | Australia |

| China | |

| India | |

| Indonesia | |

| Japan | |

| Malaysia | |

| Singapore | |

| South Korea | |

| Thailand | |

| Rest of Asia-Pacific |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Woodworking & Joinery, Footwear & Leather, Healthcare, and Others are the end-user industries considered under the acrylic adhesives market.

- Product - All acrylic adhesive products are considered in the market studied

- Resin - Under the scope of the study, different kinds of acrylate monomers, like 2-Ethylhexyl acrylate and butyl acrylate are considered

- Technology - For the purpose of this study, Water-borne, Solvent-borne, Reactive, Hot Melt, and UV Cured adhesive technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms