Market Trends of Asia-Pacific LNG Bunkering Industry

This section covers the major market trends shaping the APAC LNG Bunkering Market according to our research experts:

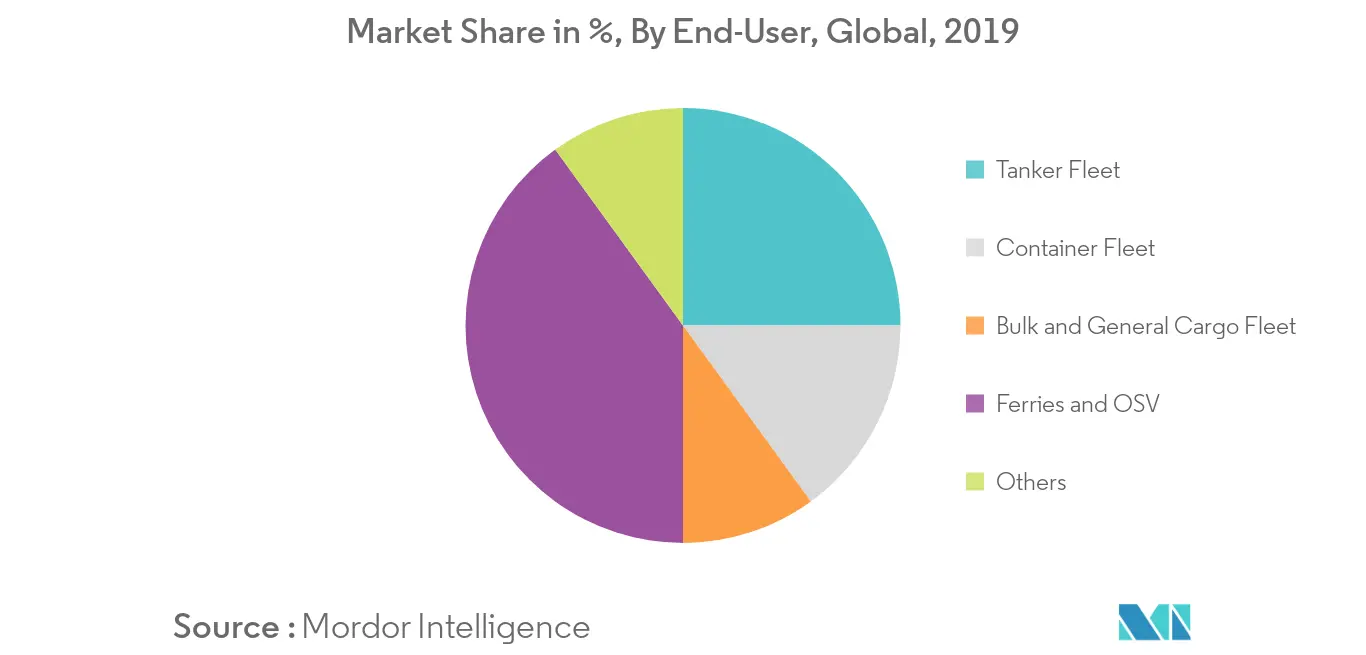

Ferries and OSV Segment to Dominate the Market

- Offshore support vessel segment is expected to dominate in segment, owing to it being relatively cost effective in terms of offshore exploration and production activities. According to Baker Hughes the Asia-Pacific offshore rig count was 92 in May, 2020.

- Rising investments toward FLNG projects including FPSO and FSRU is expected to further complement the industry size. Prelude floating liquefied natural gas (FLNG) project located in the Browse Basin offshore Western Australia represents the world's biggest FLNG facility. Operated by Shell Australia, the Prelude FLNG commenced production in December 2018.

- In November 2019, Japanese shipping firm, Mitsui OSK Lines (MOL) and its group company, Ferry Sunflower revealed their plans to build Japan's first two liquified natural gas - fueled ferries, called Sunflower Kurenai and the Sunflower Murasaki. Ferry Sunflower is expected to charter the vessels and deploy them on its Osaka-Beppu route from the end of 2022 through the first half of 2023.

- Hence, the region is expected to have a positive demand for Ferries and OSV in the LNG bunkering market, during the forecast period.

Understand The Key Trends Shaping This Market

Download PDF

China to Dominate the Market

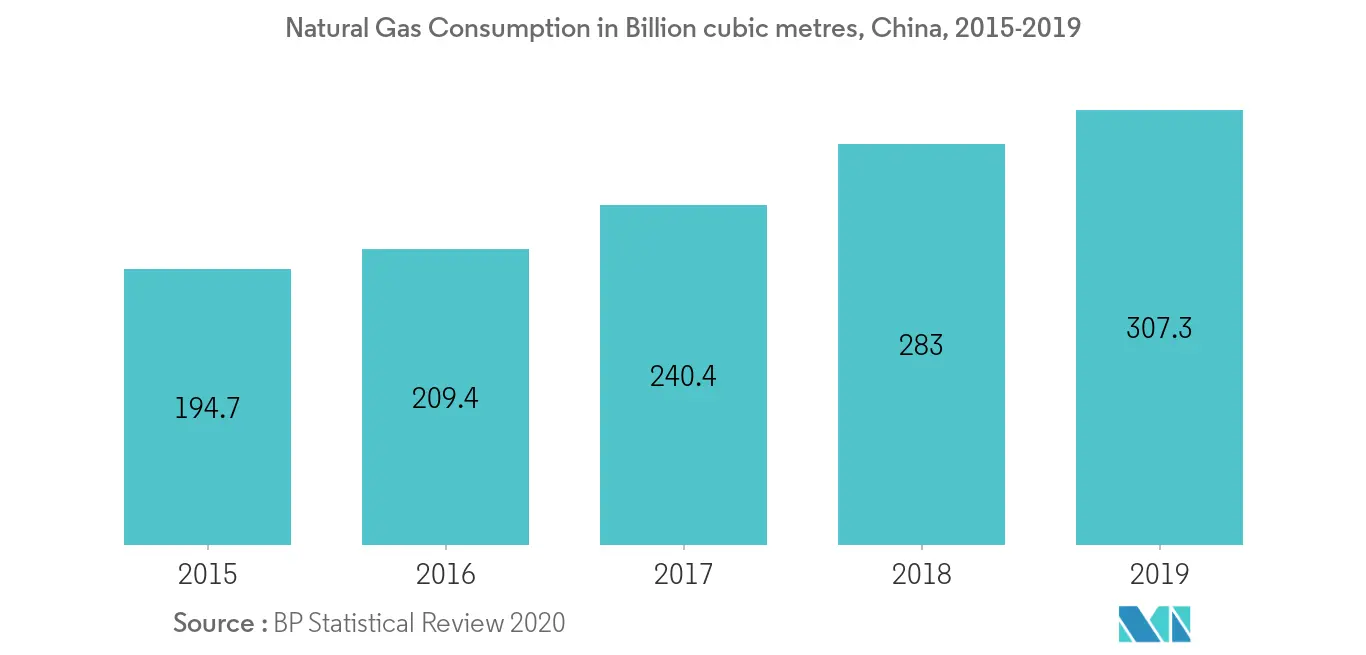

- China's LNG bunkering market maintained its growth momentum in 2019. With coal-to-gas conversion policies, GDP expansion, and industrial recovery, the country's gas consumption is increasing year-on-year. However, domestic output and pipeline imports are unable to keep up and LNG is needed to bridge this gap.

- China's natural gas consumption was about 307.3 billion cubic meters with a growth rate of 8.6% when compared to the previous year owing to the increased demand for natural gas in the country.

- In June 2019, ENN Energy Holdings, which is one of the largest LNG users in China, ordered the first LNG bunkering vessel in China. The ship is being built by Dalian Shipbuilding Industry Corporation. The bunkering vessel will have 8,500 cubic meters of capacity and is expected to begin operation by early 2020 in China's eastern Zhejiang province.

- The country has been investing in LNG bunkering facilities, and LNG as a fuel is already available in many major ports, such as Hong Kong and Shanghai port, and areas impacted by emissions regulations. Furthermore, during the forecast period, Asian LNG prices are not expected to increase significantly. Owing to the above factors, the Chinese LNG bunkering market has a potential for growth in the future.

Get Analysis on Important Geographic Markets

Download PDF