Artificial Intelligence In Retail Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 18.64 Billion |

| Market Size (2031) | USD 82.72 Billion |

| Growth Rate (2026 - 2031) | 34.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

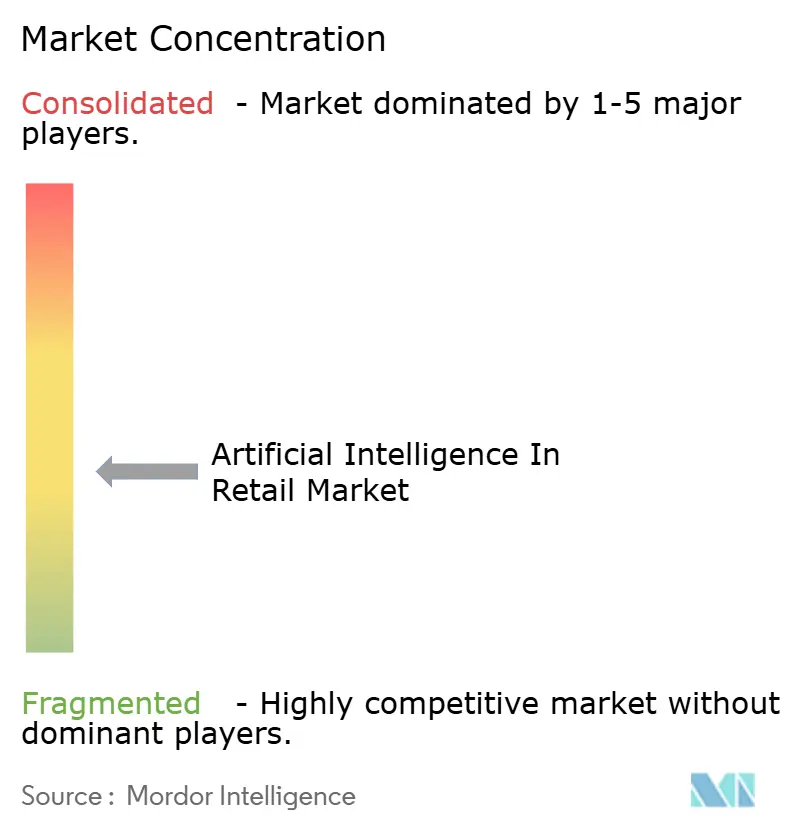

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Artificial Intelligence In Retail Market Analysis by Mordor Intelligence

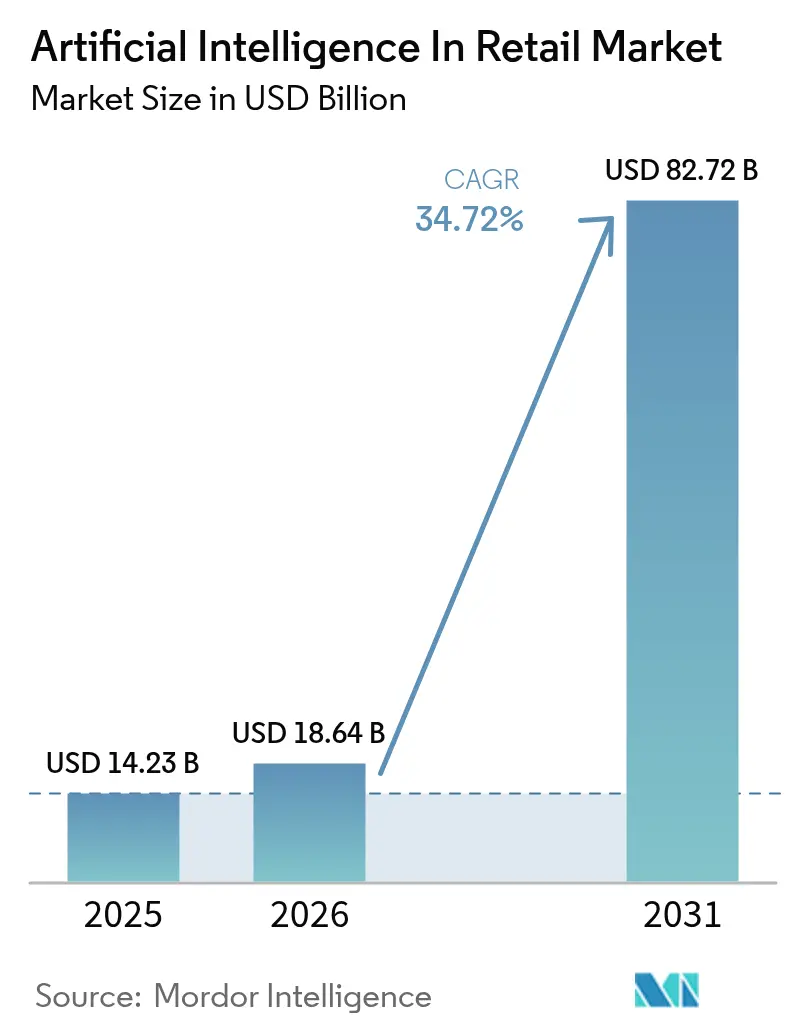

The Artificial Intelligence in Retail market size is expected to grow from USD 14.23 billion in 2025 to USD 18.64 billion in 2026 and is forecast to reach USD 82.72 billion by 2031 at a 34.7% CAGR over 2026-2031. Retailers have moved beyond proofs-of-concept into production deployments that synchronize prices, promotions, and inventory across every channel in real time. Falling cloud-infrastructure pricing, down 22% between 2024 and 2025, has lowered the entry barrier for mid-market chains and accelerated platform migrations that once took years. Omnichannel leaders that already capture unified customer signals are layering large language models on top of existing data pipes, lifting basket sizes by more than 20% when personalizing content and promotions within 50 milliseconds. At the same time, computer-vision checkout and smart-supply-chain initiatives are shrinking labor costs and food waste, while hyperscalers race to bundle pre-trained retail models into pay-as-you-go subscriptions that shrink time-to-value from months to weeks. These forces collectively propel the Artificial Intelligence in Retail market toward double-digit expansion even as privacy rules, energy prices, and talent shortages add cost and execution risk.

Key Report Takeaways

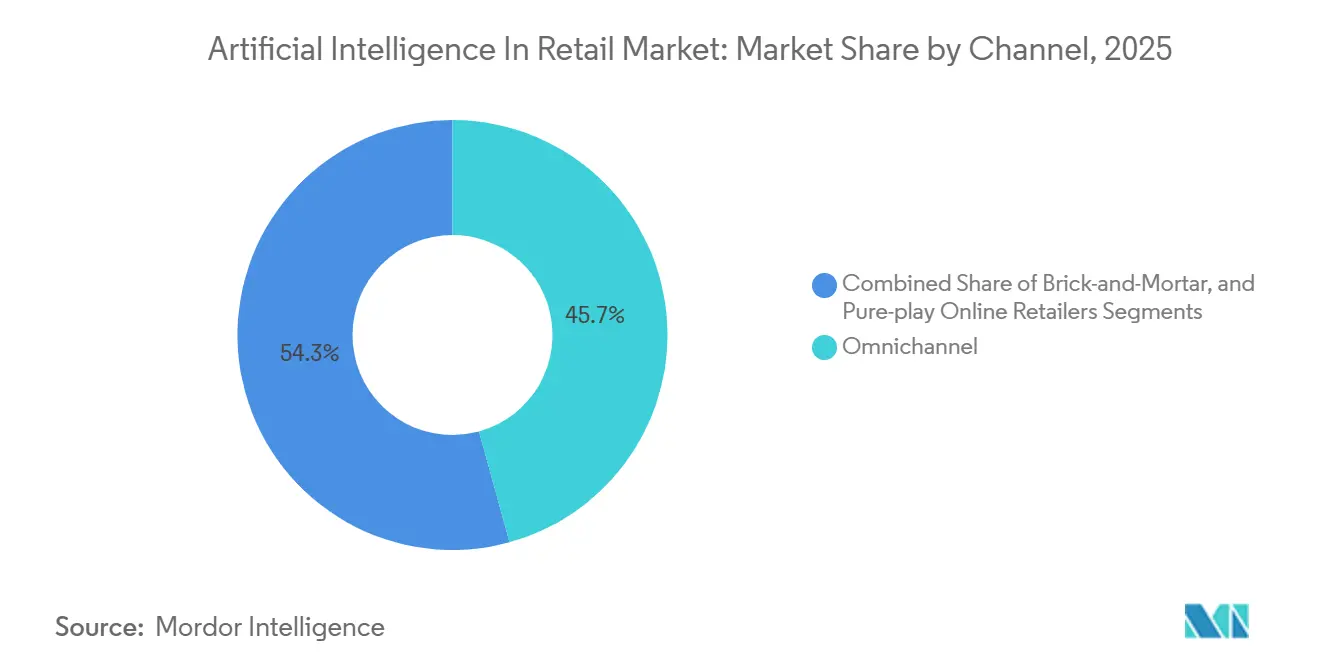

- By channel, omnichannel operators led with 45.73% of Artificial Intelligence in Retail market share in 2025, while pure-play online retailers are expanding at a 35.11% CAGR to 2031.

- By component, software accounted for 60.64% of the 2025 Artificial Intelligence in Retail market size; services represent the fastest growth at 35.32% through 2031.

- By deployment, cloud captured 71.62% of 2025 revenue and is advancing at a 35.05% CAGR, outpacing on-premise alternatives.

- By application, inventory and demand forecasting held a 22.81% share of the Artificial Intelligence in Retail market size in 2025, while vision checkout is projected to expand at a 35.25% CAGR.

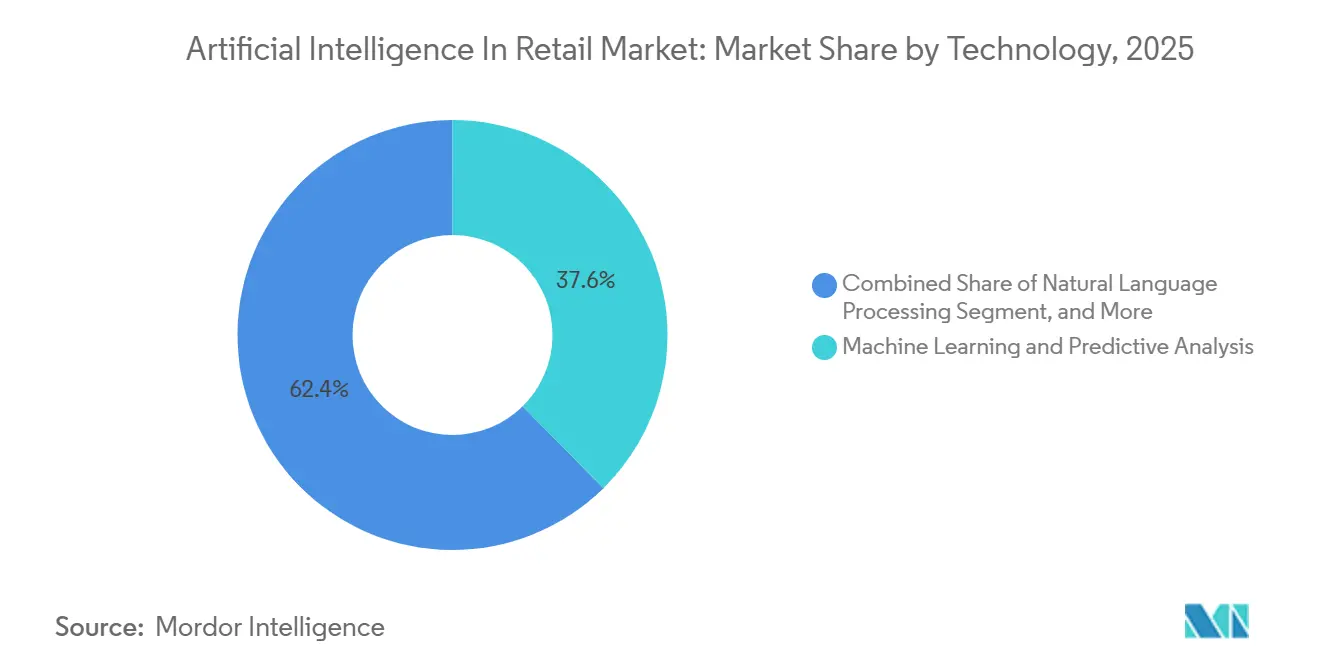

- By technology, machine learning commanded 37.62% share in 2025; generative AI is the fastest mover with a 35.51% CAGR to 2031.

- By geography, North America led with 26.83% of 2025 revenue, whereas Asia Pacific is on track for the highest growth at 36.09% over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Artificial Intelligence In Retail Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of Omnichannel AI for Personalization | +6.2% | Global, with concentration in North America and Western Europe | Medium term (2-4 years) |

| Declining Cost and Accessibility of Cloud-Based AI Stacks | +5.8% | Global, accelerating in Asia Pacific and Latin America | Short term (≤ 2 years) |

| E-Commerce Expansion Demanding Real-Time Analytics | +5.4% | Asia Pacific core, spillover to Middle East and Africa | Medium term (2-4 years) |

| Generative-AI-Powered Vision Checkout | +4.9% | North America and Europe early adopters, Asia Pacific fast followers | Long term (≥ 4 years) |

| Retail Media Networks Monetising First-Party Data | +4.7% | North America and Europe, emerging in Asia Pacific | Medium term (2-4 years) |

| ESG-Driven AI Inventory Carbon Optimisation | +3.8% | Europe leading, North America and Asia Pacific following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Omnichannel AI for Personalization

Retailers embedding neural-network engines into websites, mobile apps, and stores now anticipate intent before shoppers articulate it, raising average order value by more than 20% in 2025. Microsoft and Walgreens proved the model in 8,600 U.S. pharmacies, where Azure Copilot cut wait times 23% and lifted cross-category sales 14%.[1]Microsoft, “Walgreens Expands Strategic Partnership with Microsoft,” news.microsoft.com Despite progress, only 31% of chains operate real-time customer data platforms, leaving clear upside for laggards. Shopify’s Shop Assistant illustrates the democratization path, as mid-market merchants reported 27% higher conversions without custom code. As the Artificial Intelligence in Retail market scales, hyper-personalization remains the clearest lever for immediate revenue lift.

Declining Cost and Accessibility of Cloud-Based AI Stacks

Hyperscaler price wars trimmed AI compute bills 22% year over year, allowing regional grocers to spin up recommendation engines for only the usage hours they need. Pay-as-you-go models reduce capital outlays, while pre-trained vertical models cut data-science lead times from 6 months to 3 weeks on AWS. Oracle’s edge-optimized packages further lowered in-store latency by 40% and computing costs by 22% year over year, allowing regional grocers to spin up recommendation engines for only the hours they use18% via model quantization.[2]Oracle, “Artificial Intelligence Solutions,” oracle.com Data-center operators confirm momentum, retail AI already commands 19% of 2025 colocation demand, up from 11% the prior year. Easier access widens Artificial Intelligence's participation in the Retail market and intensifies price competition across formats.

E-Commerce Expansion Demanding Real-Time Analytics

Asia Pacific platforms now generate billions of data points that feed AI engines optimizing product descriptions, routing, and payment security within milliseconds. Alibaba showed AI-authored listings that increased click-through rates by 34% and reduced returns by 12% in 2025. JD.com used reinforcement learning to steer 1.8 billion parcels through 1,200 hubs during Singles’ Day, shaving delivery times 19%.[3]South China Morning Post, “JD.com Unveils AI-Powered Supply Chain Solution,” scmp.com Visa’s adaptive risk scoring reduced false declines 28% while keeping fraud detection above 99.2%, removing friction at checkout. Tencent’s conversational commerce processes 1.2 billion transactions daily, raising impulse buys by 22% without redirecting users from chat. Such speed and scale cement real-time analytics as a foundational pillar of the Artificial Intelligence in Retail market.

Generative-AI-Powered Vision Checkout

Camera arrays guided by diffusion models now recognize items in under 200 milliseconds, eliminating scanners and slicing queue times by 60% in pilots. Amazon’s Just Walk Out installations across third-party stores lifted peak-hour throughput by 40%. Synthetic images boosted recognition accuracy 18% for products with changing labels, shrinking manual annotation burdens. Consumer openness is rising, 63% of Asia Pacific shoppers would use vision checkout if transactions finish within 30 seconds, though 47% insist on explicit biometric opt-in. NVIDIA’s edge kits now process 120 frames per second locally, enabling autonomous stores even in bandwidth-limited environmentsthe. As retailers quantify queue-time savings against capital cost, vision checkout becomes a high-ROI wedge driving Artificial Intelligence in Retail market adoption.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Privacy Regulations Limiting Data Harvesting | -3.2% | Europe and North America, expanding to Asia Pacific | Short term (≤ 2 years) |

| Shortage of Retail-Specific AI Talent | -2.8% | Global, acute in North America and Western Europe | Medium term (2-4 years) |

| Algorithmic Bias Risk in Dynamic Pricing | -1.9% | North America and Europe, regulatory scrutiny increasing | Medium term (2-4 years) |

| Edge-Compute Energy Cost in Micro-Fulfilment | -1.6% | North America and Europe, emerging in Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy Regulations Limiting Data Harvesting

The European Union collected EUR 2.92 billion (USD 3.19 billion) in retail GDPR fines during 2025, forcing chains to purge biometric and location signals from recommendation models. California’s updated Consumer Privacy Act now requires real-time opt-out for algorithmic pricing, with fines up to USD 7,500 per violation. United Kingdom guidance further cut allowable customer attributes by 34%, degrading model accuracy for 58% of surveyed retailers. Many operators are testing synthetic data and federated learning, but only 19% had pilots underway by late 2025. The rapidly evolving rulebook, therefore, tempers near-term growth of the Artificial Intelligence in Retail market.

Shortage of Retail-Specific AI Talent

Retail AI job listings jumped 47% in 2025, but just 23% were filled within 90 days, reflecting the scarcity of engineers versed in inventory optimization, fraud analytics, and omnichannel orchestration. McKinsey reports 64% of executives cite talent gaps as the top impediment to AI scaling, with median salaries at USD 165,000-22% above other sectors. The World Economic Forum estimates 40% of retail staff will need reskilling by 2027, yet only 18% of chains offered structured programs in 2025. Infosys’ academy certified 3,500 employees in prompt engineering and model tuning, demonstrating a single remediation path. Until such initiatives scale, limited expertise will constrain the full potential of the Artificial Intelligence in Retail market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Channel: Omnichannel Scales, Online Pure-Plays Accelerate

Omnichannel operators captured 45.73% of the 2025 Artificial Intelligence in Retail market share, underpinned by unified data platforms that synchronize inventory, pricing, and promotions across web, mobile, and stores. Basket-building upsides have encouraged grocery and pharmacy chains to expand computer-vision shelf audits and voice ordering, while apparel specialists layer large language models on loyalty data to recommend outfits in real time. Pure-play online retailers, free of legacy point-of-sale constraints, are advancing at a 35.11% CAGR through 2031 as they deploy reinforcement-learning engines that refresh product rankings within 50 milliseconds of a click. Their cloud-native architectures translate directly into lower operating cost per transaction, especially when foundation models can be fine-tuned in three weeks on pay-as-you-go compute.

Omnichannel chains continue to extend edge processing to kiosks and handhelds so employees can surface personalized offers in-aisle, a move that raised cross-category add-ons 14% for Walgreens. Brick-and-mortar incumbents test camera-based checkout in selected stores to defend market share against online rivals; Amazon’s Just Walk Out rollouts in third-party locations lifted peak-hour throughput by 40%. The Artificial Intelligence in Retail market therefore sees a widening performance gap between retailers that can fund omnichannel AI at scale and those still reliant on rule-based segmentation.

By Component: Software Leads, Services Gain Ground

Software accounted for 60.64% of 2025 revenue, spanning recommendation APIs, demand-forecast engines, and fraud-detection modules that sit on retailers’ existing clouds. Fast payback-often within two quarters when out-of-stock incidents fall into double digits- explains why plug-and-play algorithms dominate initial spending. Services, however, are expanding by 35.32% through 2031 as multi-model orchestration becomes more complex and retailers outsource prompt engineering, data labeling, and model retraining.

Generative content operations retain the highest service intensity: Salesforce Einstein GPT increased email conversions by 31% and now requires ongoing tone-tuning to match seasonal campaigns. IBM, Oracle and SAP responded by embedding assistants into enterprise suites, bundling consulting hours that keep models compliant with shifting privacy rules. The Artificial Intelligence in Retail industry increasingly treats full-lifecycle model management as a managed service, driving annuity-style revenue streams for integrators.

By Deployment: Cloud Dominates, Hybrid Architectures Evolve

Cloud captured 71.62% of 2025 spend and is growing at a 35.05% CAGR, propelled by pre-trained retail models that hyperscalers price by usage minutes rather than perpetual licenses. Chains large and small now spin up capacity for flash events- Singles’ Day, Prime Day, Black Friday- then wind down servers minutes later, reducing idle capital.

On-premise installations persist in high-frequency trading aisles such as convenience stores, where transactions are completed in sub-second windows. Oracle’s edge-optimized bundles compressed latency by 40% while syncing with cloud repositories for model refreshes ORACLE. Hybrid blueprints therefore dominate new roll-outs: inference runs locally alongside cameras and handhelds, but retraining and monitoring run in regional clouds connected by 10-gigabit lines. This architecture keeps inference costs low and ensures data residency compliance, enabling the Artificial Intelligence in Retail market to scale without bottlenecks.

By Application: Forecasting Commands Spend, Vision Checkout Surges

Inventory and demand forecasting accounted for 22.81% of 2025 spend, reflecting the acute margin hit from stockouts and markdowns that historically erased up to 12% of gross profit. Carrefour’s Vertex AI project trimmed fresh-produce spoilage 12% by fusing weather, event, and social-signal data. AI-powered vision checkout, though smaller today, is set to grow 35.25% through 2031 as camera arrays replace scanners in small-basket formats where speed drives conversion.

Fraud-and-loss prevention remains a foundational layer that Visa showed can cut false declines 28% while keeping fraud detection above 99.2% VISA. In-store navigation uses computer vision to escort shoppers to items, reducing aisle search time by 41% at Lowe’s. Collectively, these use cases convert narrow point solutions into an integrated stack that deepens Artificial Intelligence penetration in the Retail market.

By Technology: Machine Learning Mature, Generative AI Gains Velocity

Machine-learning algorithms for recommendations, price elasticity, and fraud accounted for 37.62% of 2025 technology revenue; their models refresh monthly using transaction deltas. Generative AI, rising 35.51% CAGR, automates copy, images, and conversational flows, slashing creative cycle times by 40% for Shopify merchants.

Natural-language processing now handles 1.2 billion daily WeChat retail transactions, demonstrating mature throughput at planet-scale. Computer vision fuels autonomous checkout and shelf analytics, while reinforcement learning moves from research to production in JD.com’s 1,200-node fulfilment grid. With synthetic data filling privacy gaps, these technologies together expand Artificial Intelligence in Retail market functionality faster than policy can standardize.

Geography Analysis

North America led with 26.83% of 2025 revenue, anchored by Walmart’s computer-vision shelf audits that cut out-of-stocks 18%. U.S. drugstores, mass merchants and department stores now embed GPT copilots into store systems, while Canadian grocers deploy demand-forecast SaaS to rein in produce waste. Regulatory rigor under California’s privacy act pushes vendors toward real-time consent dashboards, yet investment momentum stays positive as cloud spending diverts from legacy data centers.

Asia Pacific is projected to grow 36.09% through 2031, driven by China’s live-streaming commerce where WeChat AI processes 1.2 billion daily transactions and JD.com’s smart supply chain shaved logistics cost 15% in 2025. India widens access by subsidizing small-merchant AI pilots via the National AI Portal INDIA AI, while Japan’s convenience chains automate replenishment to alleviate labor shortages. South Korea’s ecommerce leaders deploy generative-copy engines that raised conversion 19%, proving that culturally localized language models spur Artificial Intelligence in Retail market adoption.

Europe contributes meaningful volume but stricter GDPR rules slowed data harvesting, resulting in EUR 2.92 billion (USD 3.19 billion) in fines during 2025. Even so, Carrefour and Tesco refine supply-chain AI for carbon and cost, while Spanish apparel retailers trial bias-tested dynamic pricing. South America, the Middle East and Africa collectively trail in spend but register the highest green-field upside as Majid Al Futtaim scales Azure cognitive services across 450 stores in the Gulf MAF. These contrasts confirm that the Artificial Intelligence in Retail market grows fastest where cloud regions, mobile adoption and regulatory clarity intersect.

Competitive Landscape

Concentration remains moderate, the top five vendors held a considerale share of 2025 revenue, yet acquisition velocity climbed as Oracle bought two retail analytics start-ups and SAP embedded Joule into S/4HANA. Hyperscalers differentiate on vertical depth, offering elastic GPUs and retail-tuned models that mid-market chains can activate in hours. For instance, AWS bundled generative frameworks that cut deployment lead times from six months to three weeks, drawing apparel and electronics sellers to its marketplace.

Hardware providers such as NVIDIA supply edge kits that process 120 frames per second, freeing retailers from cloud round-trips and enabling processing in a 24% increase in rural, low-bandwidth locations. Specialized SaaS vendors- including BloomReach in semantic search, Daisy Intelligence in promotion optimization, and Conversica in autonomous outreach- carve profitable niches by outperforming generalists on precision metrics. Early adopters reported 24% higher conversion after deploying BloomReach Clarity AI Search.

Service integrators respond to talent scarcity by certifying thousands of store-level and headquarters staff; Infosys’ academy trimmed time-to-competency to seven months. In 2025 the Artificial Intelligence in Retail market pivoted from pilot proofs to production programs tied to revenue impact, forcing vendors to demonstrate week-one business lift rather than theoretical capability. Competitive battlegrounds therefore center on rapid ROI, privacy-by-design architectures and bundled services that mitigate the skills gap.

Artificial Intelligence In Retail Industry Leaders

IBM Corporation

Microsoft Corporation

Google LLC

NVIDIA Corporation

Amazon Web Services Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Microsoft expanded its Walgreens alliance, rolling out Azure Copilot to 8,600 pharmacies and cutting prescription processing 23%.

- November 2025: Salesforce introduced Agentforce for Retail, lifting email conversions 31% and trimming service response times 27%.

- October 2025: Google Cloud and Carrefour deployed Vertex AI across 12,000 stores, reducing fresh-produce waste 12%.

- September 2025: AWS launched retail-specific generative AI bundles that slashed deployment cycles to three weeks.

Global Artificial Intelligence In Retail Market Report Scope

Artificial intelligence is an approach for teaching a computer, a robot operated by a computer, or software to think critically and creatively like a human mind. AI is achieved by examining the cognitive processes and researching the patterns of the human brain. These research projects produce intelligent systems and software.

The Artificial Intelligence in Retail Market Report is Segmented by Channel (Omnichannel, Brick-and-Mortar, and Pure-play Online Retailers), Component (Software and Services), Deployment (Cloud and On-premise), Application (Supply-Chain and Logistics, Product Optimisation and Merchandising, In-Store Navigation and Experience, Payment, Pricing and Checkout Analytics, Inventory and Demand Forecasting, Customer Relationship Management, and Fraud and Loss Prevention), Technology (Machine Learning and Predictive Analytics, Natural Language Processing, Generative AI and Large Language Models, Computer Vision, Chatbots and Virtual Assistants, and Swarm and Reinforcement Intelligence), and Geography (North America, South America, Europe, Asia Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Omnichannel |

| Brick-and-Mortar |

| Pure-play Online Retailers |

| Software |

| Services |

| Cloud |

| On-premise |

| Supply-Chain and Logistics |

| Product Optimisation and Merchandising |

| In-Store Navigation and Experience |

| Payment, Pricing and Checkout Analytics |

| Inventory and Demand Forecasting |

| Customer Relationship Management |

| Fraud and Loss Prevention |

| Machine Learning and Predictive Analytics |

| Natural Language Processing |

| Generative AI and Large Language Models |

| Computer Vision (Image and Video) |

| Chatbots and Virtual Assistants |

| Swarm and Reinforcement Intelligence |

| North America | United States |

| Canada | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Channel | Omnichannel | |

| Brick-and-Mortar | ||

| Pure-play Online Retailers | ||

| By Component | Software | |

| Services | ||

| By Deployment | Cloud | |

| On-premise | ||

| By Application | Supply-Chain and Logistics | |

| Product Optimisation and Merchandising | ||

| In-Store Navigation and Experience | ||

| Payment, Pricing and Checkout Analytics | ||

| Inventory and Demand Forecasting | ||

| Customer Relationship Management | ||

| Fraud and Loss Prevention | ||

| By Technology | Machine Learning and Predictive Analytics | |

| Natural Language Processing | ||

| Generative AI and Large Language Models | ||

| Computer Vision (Image and Video) | ||

| Chatbots and Virtual Assistants | ||

| Swarm and Reinforcement Intelligence | ||

| By Geography | North America | United States |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast will spending on embedded AI checkout grow?

Vision-based checkout is projected to advance at a 35.25% CAGR through 2031 as retailers replace barcode scanners with camera arrays that recognize products in under 200 milliseconds.

Which channel currently contributes the most revenue?

Omnichannel chains held 45.73% of Artificial Intelligence in Retail market share in 2025, making them the largest revenue contributor.

Why are services revenue rising faster than software?

Multi-model orchestration, privacy compliance and prompt engineering complexity are pushing retailers to rely on integrators, driving services at a 35.32% CAGR.

Which region is expected to post the highest growth to 2031?

Asia Pacific is forecast to expand at a 36.09% CAGR, led by China’s live-streaming commerce and India’s SME AI grants.

Page last updated on: