Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

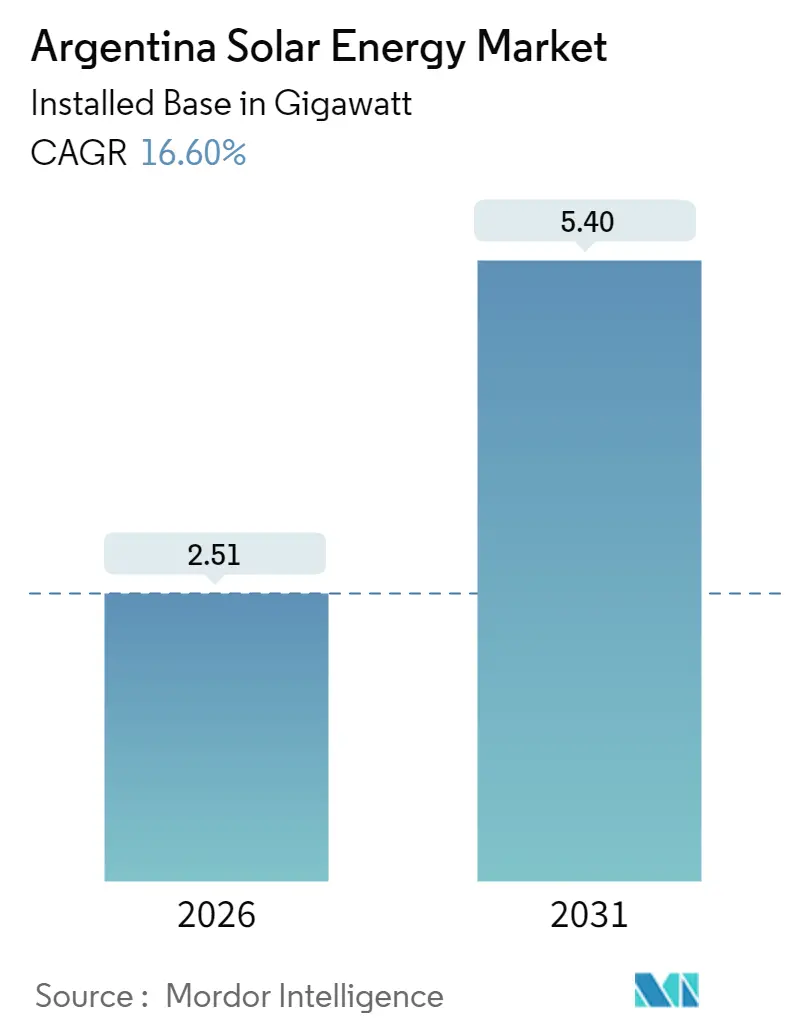

| Market Volume (2026) | 2.51 gigawatt |

| Market Volume (2031) | 5.4 gigawatt |

| Growth Rate (2026 - 2031) | 16.60% CAGR |

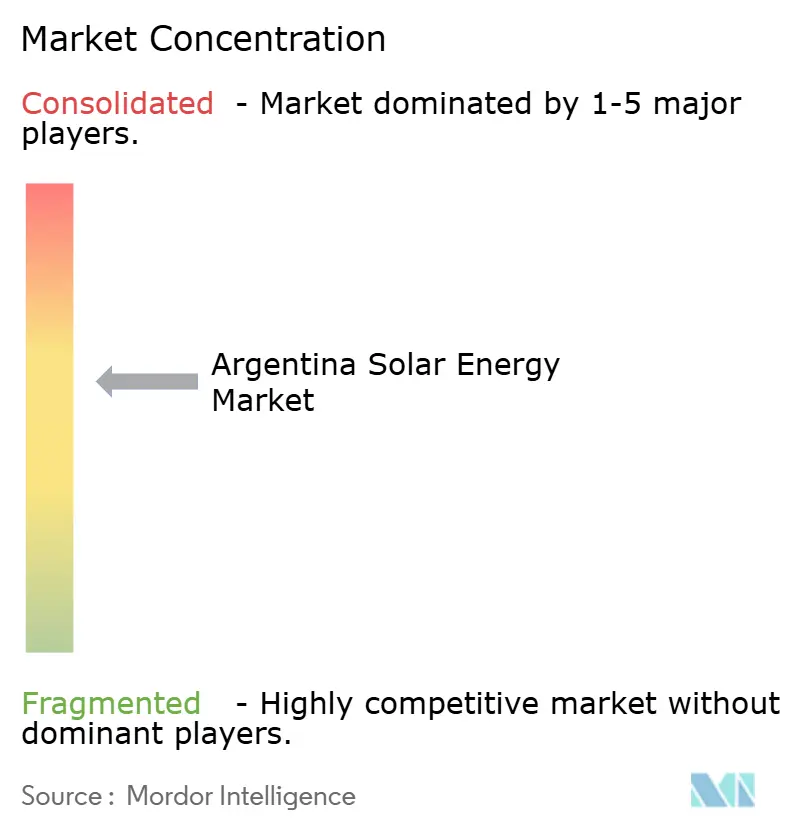

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Solar Energy Market Analysis by Mordor Intelligence

The Argentina Solar Energy Market is expected to grow from 2.15 gigawatt in 2025 to 2.51 gigawatt in 2026 and is forecast to reach 5.4 gigawatt by 2031 at 16.60% CAGR over 2026-2031.

Robust auction pipelines, falling levelized costs in high-irradiation provinces, and fiscal incentives under the RIGI framework are accelerating the Argentine solar energy market, even as currency instability complicates equipment imports. Utility-scale projects continue to dominate new builds because dollar-indexed PPAs insulate revenue from peso depreciation, while peso-linked green bonds are broadening access for commercial rooftops in major cities. Transmission upgrades financed by multilateral lenders are steadily easing bottlenecks between the Northwest and Buenos Aires, opening room for incremental capacity. Hybrid wind-solar complexes tied to Patagonia’s hydrogen roadmap add a parallel demand driver, positioning the Argentine solar energy market for diversified growth across grid-connected and off-grid segments.[1]Inter-American Development Bank, “Argentina: Transmission Network Expansion Loan Approval,” idb.org

Key Report Takeaways

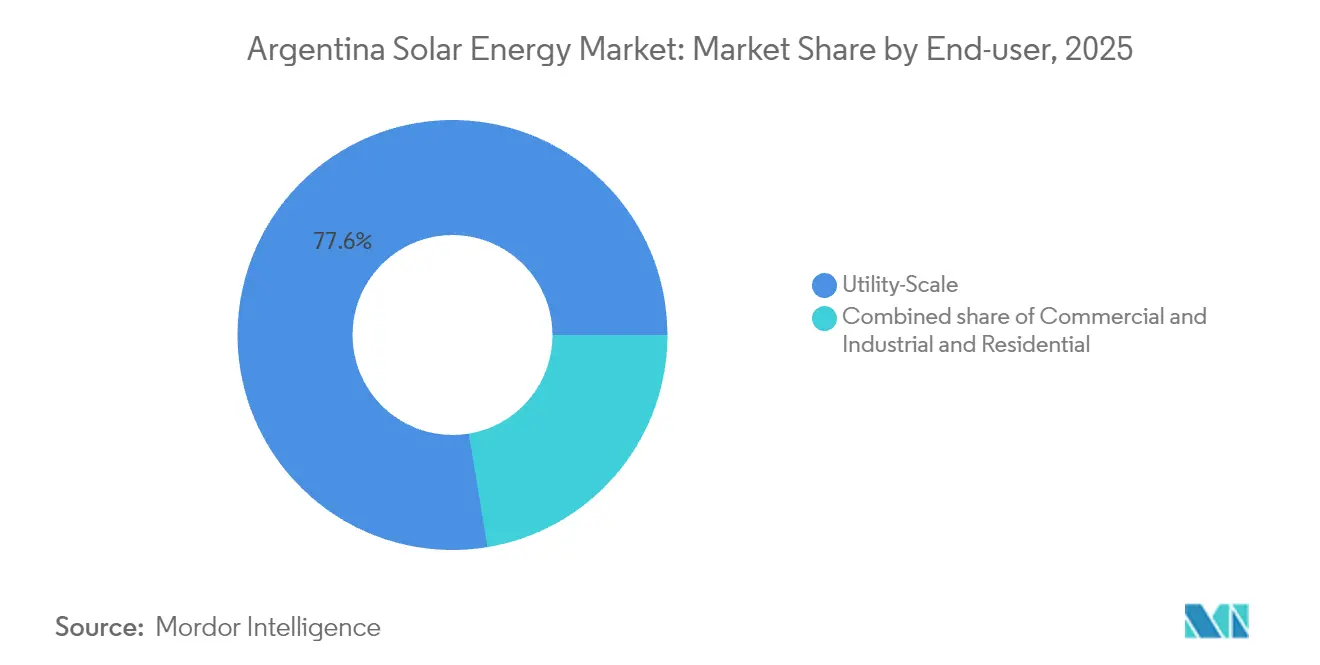

- By end-user, utility-scale projects commanded 77.60% of the Argentine solar energy market share in 2025, while the commercial and industrial segment is forecast to expand at a 20.95% CAGR to 2031.

- By grid type, on-grid systems held 63.15% of the Argentine solar energy market share in 2025; off-grid installations are projected to advance at a 19.45% CAGR during 2026-2031.

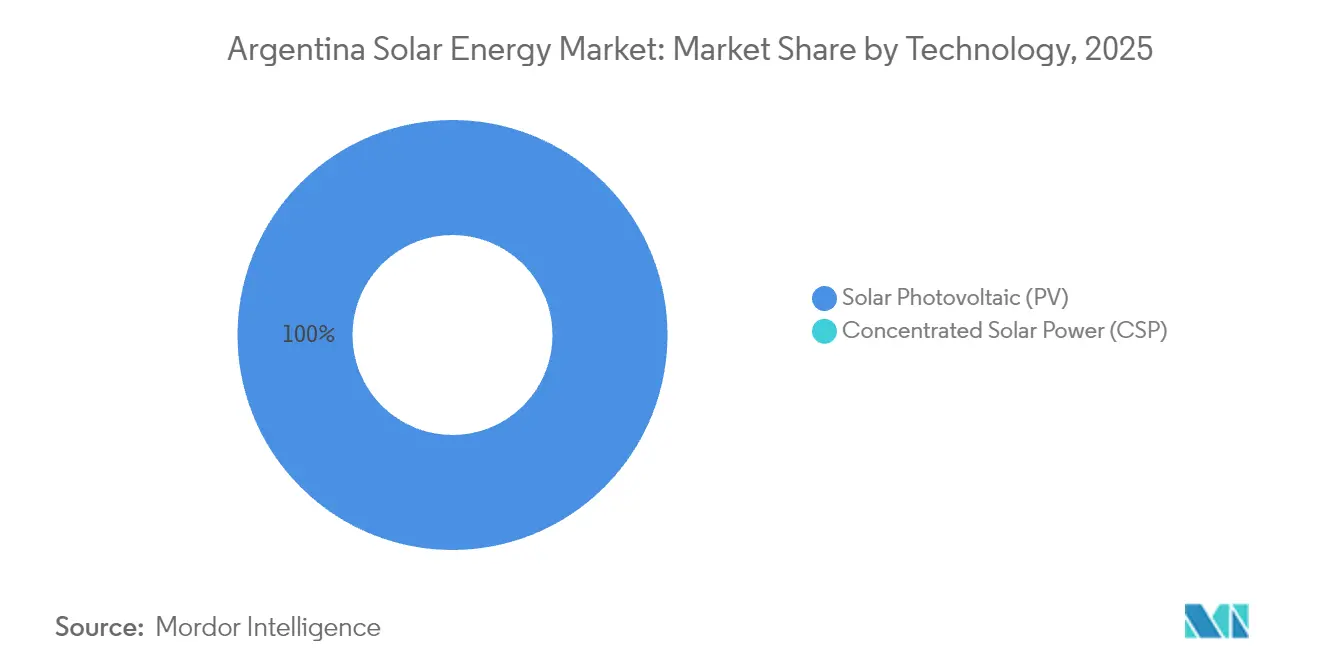

- By technology, solar PV accounted for 100.00% of installed capacity in 2025 and is projected to maintain a 16.28% CAGR through 2031, keeping concentrated solar power commercially sidelined.

- By province, Salta led with an estimated 34.60% share of installed capacity in 2025, while Mendoza is set to post the fastest provincial CAGR through 2031 once new transmission corridors come online.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Argentina Solar Energy Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renewable-energy auctions (RenovAr & MATER) continue to secure bankable PPAs | +3.80% | National, especially Salta, Jujuy, San Juan, Mendoza | Medium term (2-4 years) |

| Declining LCOE of utility-scale PV in high-irradiation regions | +2.90% | Northwest and Cuyo | Short term (≤ 2 years) |

| Corporate PPA demand from mining and agro-exporters | +2.40% | Andean and Pampas provinces | Medium term (2-4 years) |

| Transmission-grid expansion financed by CAF & IDB | +2.10% | Linking Northwest to Buenos Aires | Long term (≥ 4 years) |

| Green hydrogen roadmap spurring large hybrid PV projects | +1.80% | Patagonia and Northwest | Long term (≥ 4 years) |

| Peso-linked green-bond availability for C&I rooftop | +1.20% | Buenos Aires, Córdoba, Rosario | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Renewable-energy Auctions Continue to Secure Bankable PPAs

RenovAr and MATER rounds provide 20-year dollar-indexed contracts that shield revenues from peso swings, enabling developers such as Genneia to reach financial close on 270 MW in Mendoza slated for operation in 2025. The auctions also tendered 500 MW of storage capacity in 2024, allowing older solar assets to add evening-peak flexibility. International lenders favor these structures because CAMMESA assumes payment risk so that auction-backed projects will remain the backbone of the Argentine solar energy market. Merchant projects instead cluster in the C&I space, where creditworthy off-takers negotiate bespoke terms. Priority-dispatch rules further reduce curtailment risk, sharpening the investment case for large solar arrays.

Declining LCOE of Utility-Scale PV in High-Irradiation Regions

Salta and Jujuy record 2,200-2,400 kWh/m²/year of solar resource, pushing utility-scale PV LCOE below USD 30 per MWh and undercutting gas turbines that face intermittent fuel supply. Bifacial modules lift yields by up to 15%, while single-axis trackers now ship with most new projects. Sub-USD 0.30/W module pricing reduces payback periods to below seven years, drawing developers toward a narrow Northwest corridor. However, concentrating too many projects there intensifies congestion, so transmission additions will dictate how far declining costs can stretch provincial pipelines across the broader Argentine solar energy market.

Corporate PPA Demand from Mining & Agro-Exporters

Lithium and copper miners in remote plateaus increasingly sign 10-year dollar PPAs to secure stable electricity outlays, with YPF Luz inking 150 MW of such contracts in 2024. Agro-exporters follow suit as European buyers tighten carbon-border rules. Corporate PPAs now function as a parallel procurement channel, layering growth on top of auction schedules. Projects enjoy higher margins if the off-taker’s balance sheet removes sovereign-risk premiums, yet execution risk rises because each agreement requires tailored credit terms and bespoke curtailment clauses.

Transmission-Grid Expansion Financed by CAF & IDB

A USD 1.14 billion IDB loan finances 500 kV lines connecting Salta and Jujuy to Buenos Aires, expected to cut network losses from 17.1% to below 12% by 2028. CAF funding complements substation upgrades in San Juan and Mendoza. Lower losses raise netback prices for distant facilities, so developer interest is spilling into Río Negro and other provinces once deemed too remote. Over 800 MW of stalled projects now have a path to connection, underscoring transmission as a structural catalyst for the Argentine solar energy market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Macroeconomic volatility and FX restrictions on imported modules | -2.60% | Nationwide, with acute pressure on developers reliant on foreign equipment | Short term (≤ 2 years) |

| Saturation of existing substations in the Northwest | -1.80% | Salta, Jujuy, Catamarca | Medium term (2-4 years) |

| Community opposition delaying permits in ecologically sensitive Puna plateau | -1.30% | Jujuy and Salta high-altitude zones | Short term (≤ 2 years) |

| Policy uncertainty over post-2025 fiscal incentives and tariff structures | -1.00% | Nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Macroeconomic Volatility & FX Restrictions on Imported Modules

Peso depreciation exceeded 100% versus the dollar in 2024, while import permits for modules, inverters, and trackers stalled for months at customs, extending construction windows and jeopardizing PPA milestones. Developers with peso-denominated income face a currency mismatch on dollar debt, while those with dollar PPAs struggle to repatriate dividends through the official FX market. Smaller firms without multi-lateral banking relationships are most exposed, raising risk premiums and weighing on the overall Argentine solar energy market.[2]Banco Central de la República Argentina, “Foreign-Exchange Market Regulations,” bcra.gob.ar

Saturation of Existing Substations in Northwest

Grid-connection queues surpassed 1.2 GW in 2024, and several 132 kV and 220 kV nodes now operate at or above capacity during midday peaks. Developers often fund their own spur lines, adding USD 15-30 million to project budgets. The lack of a clear cost-allocation framework delays commitments, nudging investors toward Mendoza and San Juan, where grid headroom remains. Off-grid microgrids for mining thus gain appeal because they bypass congested substations altogether.[3]Ente Nacional Regulador de la Electricidad, “Substation Capacity Status 2024,” enre.gov.ar

Segment Analysis

By Technology: PV Dominance Reflects Cost and Modularity

Solar PV held 100.00% of installed capacity in 2025, giving it the largest Argentina solar energy market share in absolute terms. With CSP absent, the segment’s 16.28% CAGR to 2031 should lift PV to 5.4 GW, preserving the central role of module and tracker cost curves. The Argentina solar energy market size for PV is projected to increase by a net 2.89 GW over the forecast span, driven by auction-tied builds and corporate PPAs. Module-price declines of 8-10% annually and bifacial penetration above 60% nurture this trajectory, while the Mendoza BESS-linked project highlights how storage adds incremental revenue streams.

Argentina solar energy market developers favor single-axis trackers that raise yields 17-20% in high-albedo soils, making them standard on new utility sites. Battery costs falling below USD 350 per kWh allow evening-peak capture, closing the economic gap with gas-fired reserve plants. CSP remains stranded by high capex and longer construction cycles. Unless a dedicated capacity payment emerges, CSP’s addressable share will stay negligible within the Argentine solar energy industry.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Grid Type: Off-Grid Surge Driven by Mining Isolation

On-grid plants owned 63.15% of the Argentine solar energy market share in 2025, anchored by RenovAr and MATER projects that feed CAMMESA’s wholesale pool. The Argentina solar energy market size for on-grid capacity is forecast to reach 3.13 GW in 2031, yet growth moderates as substation congestion bites. Off-grid systems are forecast to deliver a 19.45% CAGR, climbing from 792 MW to roughly 2.27 GW by 2031, largely for lithium brine ponds and copper crushers that need around-the-clock supply.

Mining firms avoid USD 10-12 per MWh in wheeling charges and escape curtailment during weekend lows. Developers deploy containerized battery packs to smooth irradiance swings at 4,000 m altitude, cutting diesel consumption by 60-70%. The regulatory setup exempts these microgrids from CAMMESA oversight, compressing permitting timelines to 12 months. This bifurcated grid dynamic reallocates capital toward captive-load projects, spreading risk and widening the customer base inside the Argentine solar energy market.

By End-User: C&I Rooftop Accelerates on Tariff Pressure

Utility-scale plants commanded 77.60% of 2025 capacity, underscoring their centrality to policy mandates. Yet double-digit tariff hikes spur factories, logistics depots, and cold-chain hubs to self-supply. The Argentina solar energy market size linked to C&I rooftops is set to climb from 270 MW in 2025 to about 830 MW by 2031, a 20.95% CAGR. Net-metering caps were lifted to 300 kW in Buenos Aires in early 2025, broadening system economics. Peso-indexed green bonds bridge the financing gap, and shorter paybacks of under five years entice CFOs.

Residential uptake remains subdued because system sizes are still capped at 10 kW, and consumer finance is scarce. As a result, households will account for less than 5% of incremental capacity through 2031. Overall, C&I portfolios lower peak loads on urban substations, strengthen grid resilience, and establish a secondary growth engine alongside auctions, diversifying revenue within the Argentine solar energy industry.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Salta, Jujuy, and Catamarca form the epicenter of utility-scale capacity owing to direct normal irradiance above 2,200 kWh/m²/year. Salta alone hosted roughly 34.60% of operating megawatts in 2025, spearheaded by the Cauchari complex that is scaling to 500 MW. IDB-financed 500 kV lines will cut network losses and unlock another 800 MW that has sat idle in the grid queue, delaying provincial saturation until at least 2027. Nevertheless, once this headroom is filled, the Argentine solar energy market will pivot toward regions with fresh capacity.

San Juan and Mendoza in Cuyo are the next in line, pairing 2,000 kWh/m²/year resources with streamlined permitting and lower land costs. Genneia’s 270 MW array plus a 200 MWh battery in Mendoza exemplifies scalable projects attractive to dollar lenders and peso bondholders alike. Forecast CAGR across Cuyo could match the Northwest by the late 2020s, propelled by tax credits and substation refurbishments co-funded by CAF. Grid reliability improvements allow wine estates and agro-processors to draft corporate PPAs that blend local demand with wholesale sales, boosting bankability for mid-scale arrays.

Patagonia’s Río Negro and Chubut anchor long-dated plans tied to green hydrogen exports. Though their solar resource averages 1,800-2,000 kWh/m²/year, co-located wind doubles full-load hours, raising electrolyzer utilization. TotalEnergies and Fortescue plan multi-GW clusters to ship hydrogen to Europe and Asia in 2030-plus windows. These projects extend the geographic reach of the Argentine solar energy market and create a strategic hedge against domestic demand cycles, but they depend on port infrastructure and export-contract milestones yet to be met.

Competitive Landscape

Competition is moderate, with the five largest players holding just under 55% of operating capacity. Domestic IPP Genneia leads with nearly 800 MW, followed by YPF Luz at 600 MW, MSU Energy at 260 MW, and international entrants Enel Green Power and Total Eren rounding out the top tier. Chinese manufacturers LONGi, Trina Solar, and JinkoSolar supplied more than 70% of imported modules in 2024, leveraging price leadership and rapid logistics. Their dominance squeezes European suppliers, but quality-assurance audits by CAMMESA maintain a minimum IEC certification threshold that raises switching costs.[5] CAMMESA, “Renewable Generation Statistics 2024,” cammesa.com

Strategic moves include Genneia’s venture into 50 MW/200 MWh storage attached to its Mendoza array, positioning the firm for capacity-market revenue once CAMMESA finalizes rules. YPF Luz executed 150 MW in corporate PPAs with lithium miners, securing dollar cash flows shielded from domestic currency gyrations. Enel Green Power partnered with local agribusiness groups to develop sub-20 MW distributed portfolios that qualify for expedited permits. Smaller developers target off-grid mining clusters, where EPC bundles including batteries and O&M contracts deliver integrated value.

Supply-chain risks compel diversification: peso volatility demands local debt, while FX restrictions push larger firms to warehouse critical components. Tracker manufacturers NEXTracker and Soltec promote Argentine assembly partnerships to qualify for reduced import duties. Inverters from ABB and Sungrow win share because service technicians already support wind farms, lowering downtime risk as the Argentine solar energy market scales toward 5 GW. Integrated offerings that mix equipment supply, EPC, and five-year O&M warranties confer a competitive edge.

Argentina Solar Energy Industry Leaders

Empresa Mendocina De Energías A.P.E.M

Canadian Solar

360 Energy SA

Genneia SA

Trina Solar Limited

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2024: Genneia commenced construction on a 270 MW solar project in Mendoza, awarded under RenovAr Round 4, with a 20-year PPA indexed to the U.S. dollar. The project integrates a 50 MW / 200 MWh battery energy storage system to provide evening peak capacity and is scheduled for commercial operation in late 2025.

- September 2024: The Inter-American Development Bank approved a USD 1.14 billion loan to finance the construction of 500 kV transmission lines from Salta and Jujuy to Buenos Aires, addressing a bottleneck that had delayed over 800 MW of awarded solar capacity.

- August 2024: YPF Luz signed multiple corporate PPAs with mining companies in Jujuy and Catamarca, totaling 150 MW of solar capacity, to supply lithium extraction operations with renewable electricity.

- July 2024: The Argentine government launched the MATER auction mechanism, tendering 500 MW of battery energy storage systems to pair with existing solar assets and provide ancillary services.

Argentina Solar Energy Market Report Scope

Solar energy is heat and radiant light from the Sun that can be harnessed with technologies such as solar power (used to generate electricity) and solar thermal energy (used for applications such as water heating).

The Argentine Solar Energy Market is segmented by technology, grid type, and end-user. By technology, the market is segmented into solar Photovoltaic, concentrated solar power. By grid type, the market is segmented into on-grid and off-grid. By end-user, the market is segmented into utility-scale, commercial, Industrial, and residential. The report also covers the market size and forecasts for Argentina.

For each segment, the market sizing and forecasts have been done based on the installed capacity (GW).

By Technology

| Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) |

By Grid Type

| On-Grid |

| Off-Grid |

By End-User

| Utility-Scale |

| Commercial and Industrial (C&I) |

| Residential |

By Component (Qualitative Analysis)

| Solar Modules/Panels |

| Inverters (String, Central, Micro) |

| Mounting and Tracking Systems |

| Balance-of-System and Electricals |

| Energy Storage and Hybrid Integration |

| By Technology | Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) | |

| By Grid Type | On-Grid |

| Off-Grid | |

| By End-User | Utility-Scale |

| Commercial and Industrial (C&I) | |

| Residential | |

| By Component (Qualitative Analysis) | Solar Modules/Panels |

| Inverters (String, Central, Micro) | |

| Mounting and Tracking Systems | |

| Balance-of-System and Electricals | |

| Energy Storage and Hybrid Integration |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Argentina solar energy market in 2026?

Installed capacity is projected to reach 2.51 GW by 2026, up from 2.15 GW in 2025, sustaining a robust growth path.

What CAGR is expected for Argentina’s utility-scale solar segment through 2031?

Utility-scale installations are forecast to grow at a 15.75% CAGR between 2026 and 2031, supported by auction-backed PPAs and transmission upgrades.

Why are corporate PPAs gaining traction in Argentina?

Mining and agro-export companies sign 10-year dollar-denominated PPAs to hedge tariff inflation and meet low-carbon commitments, creating a parallel demand channel outside auctions.

Which provinces will attract the next wave of solar investment?

Mendoza and San Juan are poised for accelerated growth once IDB-financed transmission links reduce grid congestion in the Northwest.

How do peso-linked green bonds support rooftop solar deployment?

These bonds offer inflation-indexed peso funding with seven-year tenors, aligning debt service with utility-bill savings and eliminating foreign-exchange risk for local businesses.

What role will green hydrogen play in Argentina’s solar build-out?

Patagonia’s hydrogen roadmap could absorb 1.5-2 GW of new PV capacity by 2031, creating export-oriented demand that diversifies revenue streams for developers.