Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

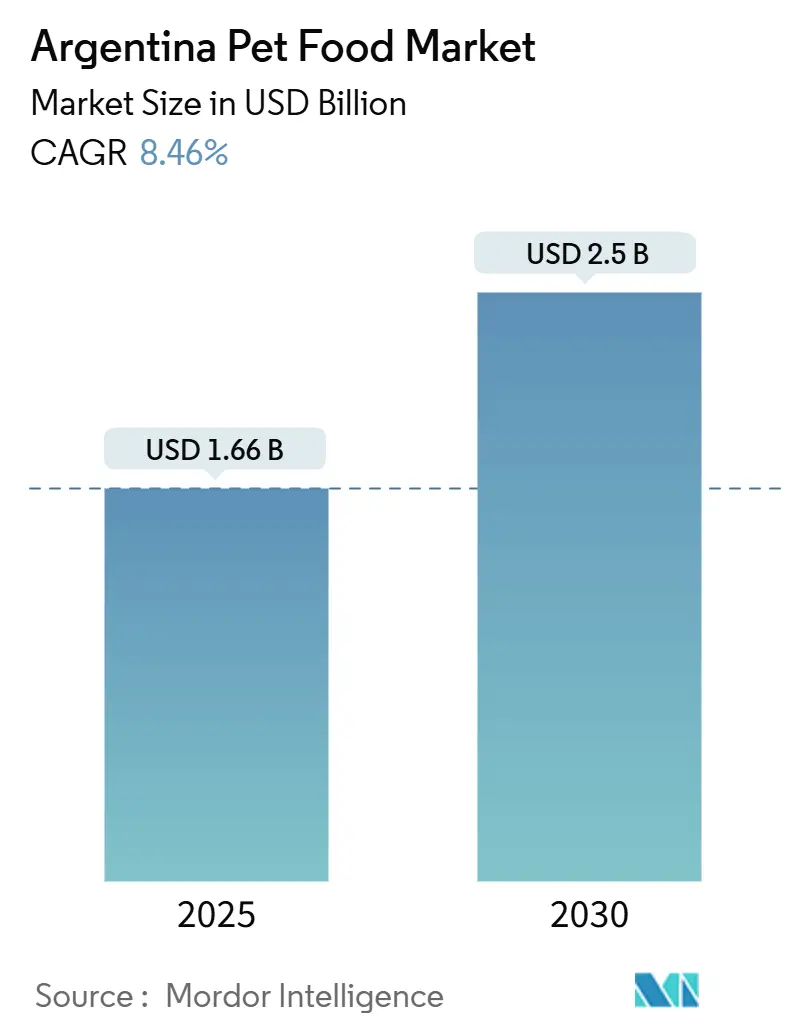

| Market Size (2025) | USD 1.66 Billion |

| Market Size (2030) | USD 2.5 Billion |

| Growth Rate (2025 - 2030) | 8.46% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Argentina Pet Food Market Analysis by Mordor Intelligence

The Argentina pet food market size was USD 1.66 billion in 2025 and is forecast to reach USD 2.50 billion by 2030, advancing at a 8.46% CAGR during the period 2025-2030. Robust pet ownership, more than 80% of households keep at least one animal, continues to anchor structural demand, while a base of over 30 million companion animals stimulates steady volume growth[1]Source: Buenos Aires Times staff, “Argentina is the world’s most pet-rich country,” batimes.com.ar. Multinational capacity expansions, such as Mars Pet Nutrition’s Mercedes facility, complement domestic investments by Agroindustrias Baires and Grupo Pilar, reinforcing local supply resilience. Regulatory modernization through SENASA Resolution 1415/2024 streamlines product registration and bolsters export competitiveness for the Argentina pet food market. Digital commerce further lifts prospects; online channel volume is rising by double digits as retailers adopt omnichannel models and subscription services

Key Report Takeaways

- By product category, food commanded 67.2% of the Argentina pet food market share in 2024, and they are also projected to expand at a 9% CAGR through 2030.

- By species, dogs held 70.8% of the Argentina pet food market size in 2024, and the same recorded the fastest household penetration growth to 2030.

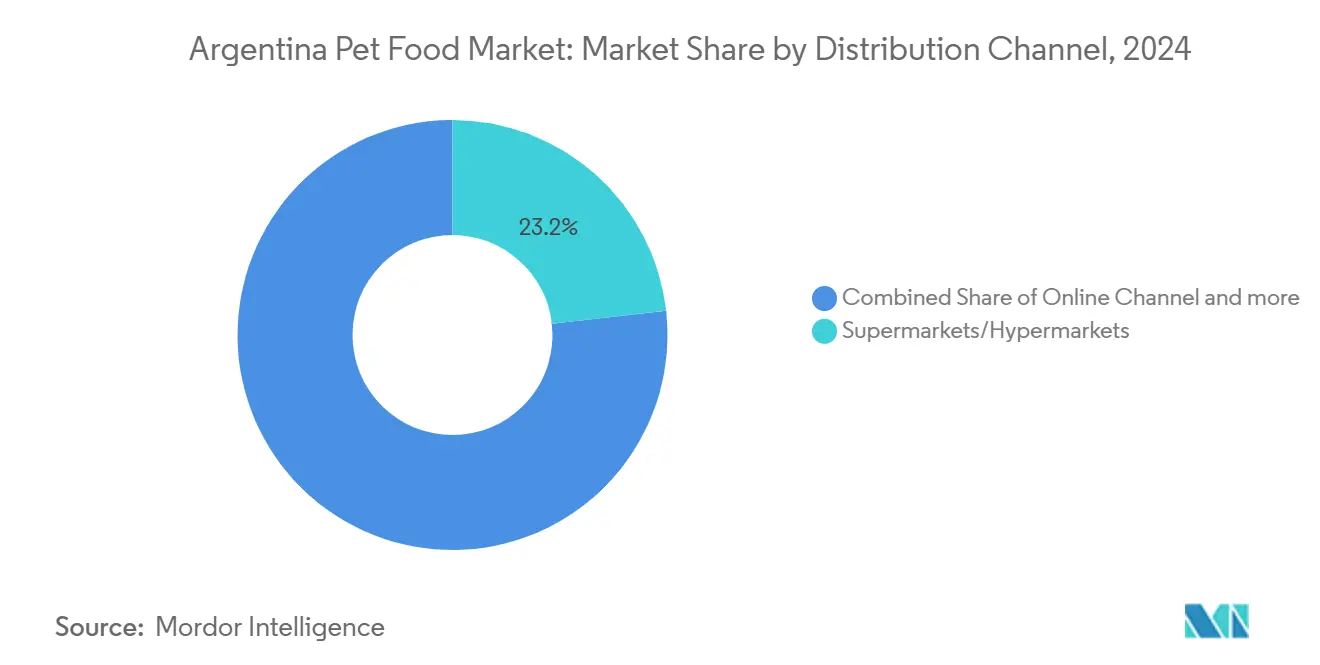

- By distribution channel, supermarkets and hypermarkets accounted for 23.2% revenue in 2024; online retail is forecast to post an 11.2% CAGR between 2025-2030.

Argentina Pet Food Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid premiumization of pet diets | +1.2% | National, strongest in Buenos Aires and urban centers | Medium term (2-4 years) |

| Surging e-commerce adoption in emerging economies | +0.3% | Buenos Aires, Córdoba, major metropolitan areas | Long term (≥ 4 years) |

| Plant-based protein inclusion for sustainability pledges | +0.8% | National, with early gains in Buenos Aires, Córdoba, Rosario | Short term (≤ 2 years) |

| Integration of AI-enabled feeding devices boosting demand | +0.4% | Urban centers, expanding to secondary cities | Medium term (2-4 years) |

| Personalized nutrition formulated via DTC genetic testing | +0.2% | Buenos Aires metropolitan area, premium segments | Long term (≥ 4 years) |

| Veterinary endorsement of functional treats | +0.6% | National, veterinary clinic networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Premiumization of Pet Diets

Premium lines already outpace overall category growth, driven by 94% of owners who view pets as family and 77% of high-income shoppers who prefer organic formulations. Domestic manufacturers are scaling next-generation extruders and automated lines to guarantee nutrient integrity and substantiate health claims. Product launches now target clinical needs such as renal, obesity, and gastrointestinal management, underscoring the sophistication of the Argentina pet food market. Companies like Grupo Molino Chacabuco have responded by launching specialized nutrition products, including formulations for spayed and neutered cats enriched with prebiotics and balanced minerals for urinary health.

Surging E-Commerce Adoption in Emerging Economies

The online share of pet expenditures climbed in 2024, with Mercado Libre naming pet food its top-selling Animals and Pets product and average ticket sizes of ARS 36,000 (USD 45). Tiendanube hosts nearly 400 dedicated pet shops, most integrating social media marketing and click-and-collect, reflecting the omnichannel pivot reshaping the Argentina pet food market. Leading brands like Royal Canin, Excellent, and Old Prince dominate online searches, while retailers increasingly adopt omnichannel strategies, including click-and-collect services and automated replenishment systems, to capture growing digital demand.

Plant-based Protein Inclusion for Sustainability Pledges

National climate policies such as Law 27520 encourage lower-emission ingredients, and innovators like NotCo use AI to replicate amino acid profiles from 20,000 plant species, trimming R&D cycles to three months. Life Cycle Assessment work shows an 82% reduction in environmental cost when animal proteins are replaced by plant or insect meals, stimulating investment in circular economy inputs across the Argentina pet food market[2]Source: Candela Bonaura, “Sostenibilidad en la industria de los alimentos para mascotas,” allpetfood.net. Vitalcan has pioneered circular economy initiatives through partnerships with Procens to incorporate insect-derived proteins, promoting regenerative agricultural practices while producing organic soil amendments as byproducts.

Integration of AI-enabled Feeding Devices Boosting Demand

Argentina's pet food market experiences an emerging transformation through artificial intelligence integration in feeding technology, though adoption remains concentrated in premium segments and metropolitan areas. Smart bowls that automate portion control and real-time dietary tracking are gaining traction among premium consumers, pushing manufacturers to bundle compatible nutrition SKUs and reinforcing brand lock-in within the Argentina pet food market. Economic constraints limit widespread adoption, as 2024 conditions led some consumers to prioritize cheaper pet food formats and supplement commercial kibble with home-cooked alternatives, suggesting price sensitivity that may delay premium technology adoption among middle-income segments.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile raw-material prices | -0.9% | National, affecting all producers | Short term (≤ 2 years) |

| Regulatory scrutiny on novel proteins | -0.3% | National, SENASA oversight | Medium term (2-4 years) |

| Supply-chain emission targets discouraging meat inclusion | -0.2% | National, export-oriented producers | Long term (≥ 4 years) |

| Rising incidences of pet-food recalls hurting trust | -0.4% | National, brand-dependent impact | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Raw-Material Prices

Argentina's pet food industry faces significant input cost volatility, particularly affecting soybean meal and corn prices that serve as primary protein and energy sources in many formulations. Corn prices spiked 9.3% to USD 213 per metric ton during harvest delays, compelling formulators to juggle cost pass-throughs in the Argentina pet food market[3]Source: Control Union Argentina, “Agri Market Report,” controlunion.com. July 2025 tariff cuts on grains alleviate some pressure, but currency controls continue to inject pricing uncertainty.

Regulatory Scrutiny on Novel Proteins

Argentina's pet food industry faces increasing regulatory oversight on novel protein sources through SENASA's modernized framework under Resolution 1415/2024, which establishes comprehensive technical standards requiring detailed documentation for all animal feed ingredients, including emerging protein alternatives such as insect-based, plant-derived, and cultured proteins. Export considerations add complexity, as Argentine manufacturers targeting international markets must ensure novel protein formulations comply with destination country regulations, including stringent requirements from markets like China, where only five Argentine pet food facilities maintain export certification, and the European Union, which maintains specific novel food regulations affecting pet food ingredients.

Segment Analysis

By Pet Food Product: Premium Innovation Drives Category Evolution

Food products maintain a dominant market position with a 67.2% share in 2024, and also emerge as the fastest-growing segment at 9% CAGR through 2030. Dry pet food represents the largest subsegment within food products, supported by Argentina's advanced extrusion technology capabilities and automated production lines that ensure consistent quality and nutritional preservation. Pet nutraceuticals and supplements show robust development, with companies incorporating milk bioactives, omega-3 fatty acids, probiotics, and specialized vitamins targeting specific health conditions, including diabetes, digestive sensitivity, and urinary tract disease.

Veterinary diets represent a specialized growth area, with formulations addressing renal conditions, oral care, and other therapeutic applications gaining veterinary endorsement and professional recommendation. The treats segment benefits from humanization trends and premiumization, with formats resembling human indulgence products, including sticks, filled snacks, and single-serve options that strengthen the owner-pet emotional bond

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Pets: Dogs Dominate While Cats Accelerate

Dogs held 70.8% of the Argentina pet food market size in 2024, and recorded the fastest household penetration growth to 2030. Cat ownership is widening more rapidly, lifting demand for urinary health and weight-management formulas that address spay and neuter prevalence. Cat food production increased over the past five years, driven primarily by premium segment growth as manufacturers develop specialized formulations addressing feline-specific nutritional requirements, including urinary health, weight management for spayed and neutered cats, and life-stage appropriate nutrition.

Manufacturers such as Nestlé Purina tailor recipes for feline digestive sensitivity and life-stage needs, using lower-magnesium and balanced mineral profiles that align with veterinary protocols. Regulatory compliance through National Agri-Food Health and Quality Service (SENASA) registration ensures product safety and quality across all pet species categories, supporting consumer confidence and enabling export market access for Argentine manufacturers targeting regional expansion.

By Distribution Channel: Digital Transformation Reshapes Traditional Retail

Supermarkets and hypermarkets delivered 23.2% of national revenue in 2024 as mass merchants leverage price promotions and a broad footprint to capture staple purchases. Online platforms, however, are tracking an 11.2% CAGR to 2030, enhanced by subscription replenishment and doorstep convenience that resonate with time-pressed urban consumers within the Argentina pet food market.

Specialty stores and veterinary clinics remain critical, representing nearly three-quarters of turnover and offering trusted consultation that underpins premium trade-ups. Chain retailers such as Puppis are expanding medical services and grooming to deepen engagement, while Mercado Libre and company direct-to-consumer portals extend assortments beyond physical shelf space, creating an omnichannel ecosystem that redefines reach in the Argentina pet food market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Buenos Aires City alone houses about 500,000 dogs and 300,000 cats in 2023, making it the epicenter of premium demand in the Argentina pet food market. The province also hosts Mars’s 44-hectare Mercedes plant, supplying nine South Latin American countries with more than 80% local content sourcing. Santa Fe’s industrial corridor adds depth through Nestlé Purina’s Santo Tomé complex and the recently inaugurated Lokal plant backed by a USD 6 million cooperative investment.

Córdoba strengthens manufacturing nodes via Alican’s USD 30 million capacity tripling plan, positioning the province as a logistics bridge to central and northwest consumption regions. Patagonia’s Tierra del Fuego benefits from fiscal incentives; Vitalcan deployed a USD 9 million facility there to serve domestic and export flows, underscoring geographic diversification in the Argentina pet food market.

Interior provinces like Entre Ríos and Mendoza are witnessing rising penetration as average disposable income edges upward and specialty retail chains extend coverage. Nonetheless, unequal income distribution means down-trading remains more visible in these regions during inflationary spikes, leading to elastic demand shifts within the Argentina pet food market. SENASA enforces uniform standards through satellite offices, facilitating traceability and export certification across all geographies

Competitive Landscape

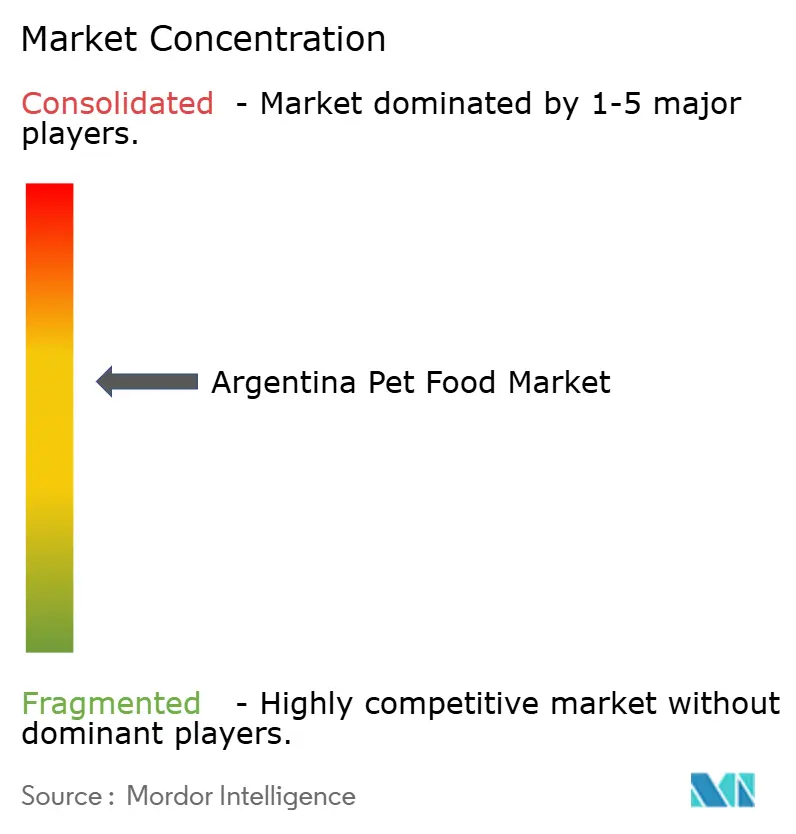

Argentina's pet food market exhibits moderate concentration with strong competition between multinational corporations and established domestic players, creating a dynamic environment that supports both innovation and price competition. Mars Pet Nutrition operates as a major regional player through its Mercedes facility, which serves as the sole manufacturing plant for the nine-country South Latin America cluster, producing dry, wet, and care and treats products with over 80% local supplier integration.

Companies are investing heavily in capacity expansion and technology, with Alican committing USD 30 million over four years to triple production capacity while targeting export share growth, and Vitalcan expanding internationally to reach 40 countries through subsidiary establishments in Panama and Costa Rica.

Technology adoption differentiates leaders: fully automated lines, in-house laboratories, and AI-driven formulation shorten innovation cycles to as little as three months. Wet-food capacity is emerging as a white-space frontier, with only 2% penetration locally compared with 30% in developed economies, presenting opportunity for share gain within the Argentina pet food market. SENASA's harmonized rules level compliance expectations, favoring firms that already uphold Hazard Analysis and Critical Control Points (HACCP) and International Organization for Standardization (ISO) protocols while nudging smaller operators toward consolidation or niche specialization

Argentina Pet Food Industry Leaders

-

ADM

-

Agroindustrias Baires

-

Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

-

Mars Incorporated

-

Nestle (Purina)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: Mars opened a new wet pet food factory in Ponta Grossa, Brazil, with R$450 million (USD 90 million) investment and 20,000 metric tons annual capacity, strategically positioned to serve Argentine and regional markets through proximity to distribution networks.

- May 2025: Guillermo Lehmann Cooperative launched Lokal premium pet food brand through USD 6 million state-of-the-art facility in San Jerónimo Norte, Santa Fe, featuring 2.5 metric tons per hour extrusion capacity and automated ingredient dosing systems for natural, additive-free formulations.

- May 2024: Alican unveiled a USD 30 million expansion program spanning four years to triple its production capacity at its Córdoba facilities. The company aims to increase annual revenue to USD 100 million and double its export volumes to reach a 30% share in international sales.

Argentina Pet Food Market Report Scope

Food, Pet Nutraceuticals/Supplements, Pet Treats, Pet Veterinary Diets are covered as segments by Pet Food Product. Cats, Dogs are covered as segments by Pets. Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets are covered as segments by Distribution Channel.

Pet Food Product

| Food | By Sub Product | Dry Pet Food | By Sub Dry Pet Food | Kibbles |

| Other Dry Pet Food | ||||

| Wet Pet Food | ||||

| Pet Nutraceuticals/Supplements | By Sub Product | Milk Bioactives | ||

| Omega-3 Fatty Acids | ||||

| Probiotics | ||||

| Proteins and Peptides | ||||

| Vitamins and Minerals | ||||

| Other Nutraceuticals | ||||

| Pet Treats | By Sub Product | Crunchy Treats | ||

| Dental Treats | ||||

| Freeze-dried and Jerky Treats | ||||

| Soft & Chewy Treats | ||||

| Other Treats | ||||

| Pet Veterinary Diets | By Sub Product | Diabetes | ||

| Digestive Sensitivity | ||||

| Oral Care Diets | ||||

| Renal | ||||

| Urinary tract disease | ||||

| Other Veterinary Diets |

Pets

| Cats |

| Dogs |

| Other Pets |

Distribution Channel

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| Pet Food Product | Food | By Sub Product | Dry Pet Food | By Sub Dry Pet Food | Kibbles |

| Other Dry Pet Food | |||||

| Wet Pet Food | |||||

| Pet Nutraceuticals/Supplements | By Sub Product | Milk Bioactives | |||

| Omega-3 Fatty Acids | |||||

| Probiotics | |||||

| Proteins and Peptides | |||||

| Vitamins and Minerals | |||||

| Other Nutraceuticals | |||||

| Pet Treats | By Sub Product | Crunchy Treats | |||

| Dental Treats | |||||

| Freeze-dried and Jerky Treats | |||||

| Soft & Chewy Treats | |||||

| Other Treats | |||||

| Pet Veterinary Diets | By Sub Product | Diabetes | |||

| Digestive Sensitivity | |||||

| Oral Care Diets | |||||

| Renal | |||||

| Urinary tract disease | |||||

| Other Veterinary Diets | |||||

| Pets | Cats | ||||

| Dogs | |||||

| Other Pets | |||||

| Distribution Channel | Convenience Stores | ||||

| Online Channel | |||||

| Specialty Stores | |||||

| Supermarkets/Hypermarkets | |||||

| Other Channels | |||||

Need A Different Region or Segment?

Customize Now

Market Definition

- FUNCTIONS - Pet foods are usually intended to provide complete and balanced nutrition to the pet but are primarily used as functional products. The scope includes the food and supplements consumed by pets including veterinary diets. Supplements/nutraceuticals that are directly supplied to pets are considered within the scope.

- RESELLERS - Companies engaged in reselling of pet food without value addition have been excluded from the market scope, in order to avoid double counting.

- END CONSUMERS - Pet owners are considered to be the end-consumers in the market studied.

- DISTRIBUTION CHANNELS - Supermarkets/hypermarkets, specialty stores, convenience stores, online channels and other channels are considered within the scope. The stores which are exclusively providing pet related basic and custom products are considered within the scope of specialty stores.

| Keyword | Definition |

|---|---|

| Pet Food | The scope of pet food includes the food that is eatable by pets including food, treats, veterinary diets, and nutraceuticals/supplements. |

| Food | Food is animal feed intended for consumption by pets. It is formulated to provide essential nutrients and meet the dietary needs of various types of pets, including dogs, cats, and other animals. These are generally segmented into dry and wet pet foods. |

| Dry Pet Food | Dry pet foods may be extruded/baked (kibbles) or flaked. They have a lower moisture content, typically around 12-20%. |

| Wet Pet Food | Wet pet food, also known as canned pet food or moist pet food, generally has a higher moisture content compared to dry pet food, often ranging from 70-80%. |

| Kibbles | Kibbles are dry, processed pet food in small, bite-sized pieces or pellets. They are specifically formulated to provide balanced nutrition for various domestic animals, such as dogs, cats, and other animals. |

| Treats | Pet Treats are special food items or rewards given to pets, to show affection, and encourage good behavior. They are especially used during training. Pet treats are made from various combinations of meat or meat-derived materials with other ingredients. |

| Dental Treats | Pet dental treats are specialized treats that are formulated to promote good oral hygiene in pets. |

| Crunchy Treats | It is a type of pet treat that has a firm and crispy texture which can be a good source of nutrition for pets. |

| Soft and chewy treats | Soft and Chewy pet treats are a type of pet food product that is formulated to be easy to chewy and digest. They are usually made from soft and pliable ingredients, such as meat, poultry, or vegetables, that have been blended and formed into bite-sized pieces or strips. |

| Freeze-dried & Jerky Treats | Freeze-dried and jerky treats are snacks given to pets, that are prepared through a special preservation process, without damaging the nutritional content, resulting in long-lasting, nutrient-rich treats. |

| Urinary Tract Disease Diets | These are commercial diets that are specifically formulated to promote urinary health and reduce the risk of urinary tract infections and other urinary problems. |

| Renal Diets | These are specialized pet foods formulated to support the health of pets with kidney disease or renal insufficiency. |

| Digestive Sensitivity Diets | Digestive-sensitive diets are specially formulated to meet the nutritional needs of pets with digestive issues such as food intolerances, allergies, and sensitivities. These diets are designed to be easily digestible and to reduce the symptoms of digestive problems in pets. |

| Oral Care Diets | Oral care diets for pets are specially formulated diets produced to promote oral health and hygiene in pets. |

| Grain-Free Pet Food | Pet food that does not contain common grains like wheat, corn, or soy. Grain-free diets are often preferred by pet owners seeking alternative options or if their pets have specific dietary sensitivities. |

| Premium Pet Food | High-quality pet food formulated with superior ingredients often offers additional nutritional benefits compared to standard pet food. |

| Natural Pet Food | Pet food made from natural ingredients, with minimal processing and without artificial preservatives. |

| Organic Pet Food | Pet food is produced using organic ingredients, free from synthetic pesticides, hormones, and genetically modified organisms (GMOs). |

| Extrusion | A manufacturing process used to produce dry pet food, where ingredients are cooked, mixed, and shaped under high pressure and temperature. |

| Other Pets | Other pets include birds, fish, rabbits, hamsters, ferrets, and reptiles. |

| Palatability | The taste, texture, and aroma of pet food influence its appeal and acceptance by pets. |

| Complete and Balanced Pet Food | Pet food that provides all essential nutrients in appropriate proportions to meet the nutritional needs of pets without additional supplementation. |

| Preservatives | These are the substances that are added to pet food to extend its shelf life and prevent spoilage. |

| Nutraceuticals | Food products that offer health benefits beyond basic nutrition, often contain bioactive compounds with potential therapeutic effects. |

| Probiotics | Live beneficial bacteria that promote a healthy balance of gut flora, supporting digestive health and immune function in pets. |

| Antioxidants | Compounds that help neutralize harmful free radicals in the body, promoting cellular health and supporting the immune system in pets. |

| Shelf-Life | The duration of which pet food remains safe and nutritionally viable for consumption after its production date. |

| Prescription diet | Specialized pet food formulated to address specific medical conditions under veterinary supervision. |

| Allergen | A substance that can cause allergic reactions in some pets, leading to food allergies or sensitivities. |

| Canned food | Wet pet food that is packed in cans and contains higher moisture content than dry food. |

| Limited ingredient diet (LID) | Pet food formulated with a reduced number of ingredients to minimize potential allergens. |

| Guaranteed Analysis | The minimum or maximum levels of certain nutrients present in pet food. |

| Weight management | Pet food designed to help pets maintain a healthy weight or support weight loss efforts. |

| Other Nutraceuticals | It includes prebiotics, antioxidants, digestive fiber, enzymes, essential oils and herbs. |

| Other Veterinary Diets | It includes weight management diets, skin and coat health, cardiac care, and joint care. |

| Other Treats | It includes rawhides, mineral blocks, lickables, and catnips. |

| Other Dry Foods | It includes cereal flakes, mixers, meal toppers, freeze-dried foods, and air-dried foods. |

| Other Animals | It includes birds, fish, reptiles, and small animals (rabbits, ferrets, hamsters). |

| Other Distribution Channels | It includes veterinary clinics, local unregulated stores, and feed and farm stores. |

| Proteins and Peptides | Proteins are large molecules composed of basic units called amino acids which help in the growth and development of pets. Peptides are the short string of 2 to 50 amino acids. |

| Omega-3 fatty acids | Omega-3 fatty acids are essential polyunsaturated fats that play a crucial role in the overall health and well-being of Pets |

| Vitamins | Vitamins are the essential organic compounds that are essential for vital physiological functioning. |

| Minerals | Minerals are naturally occurring inorganic substances that are essential for various physiological functions in pets. |

| CKD | Chronic Kidney Disease |

| DHA | Docosahexaenoic Acid |

| EPA | Eicosapentaenoic Acid |

| ALA | Alpha-linolenic Acid |

| BHA | Butylated Hydroxyanisol |

| BHT | Butylated Hydroxytoluene |

| FLUTD | Feline Lower Urinary Tract Disease |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF