Saudi Arabia Aquaculture Market Analysis by Mordor Intelligence

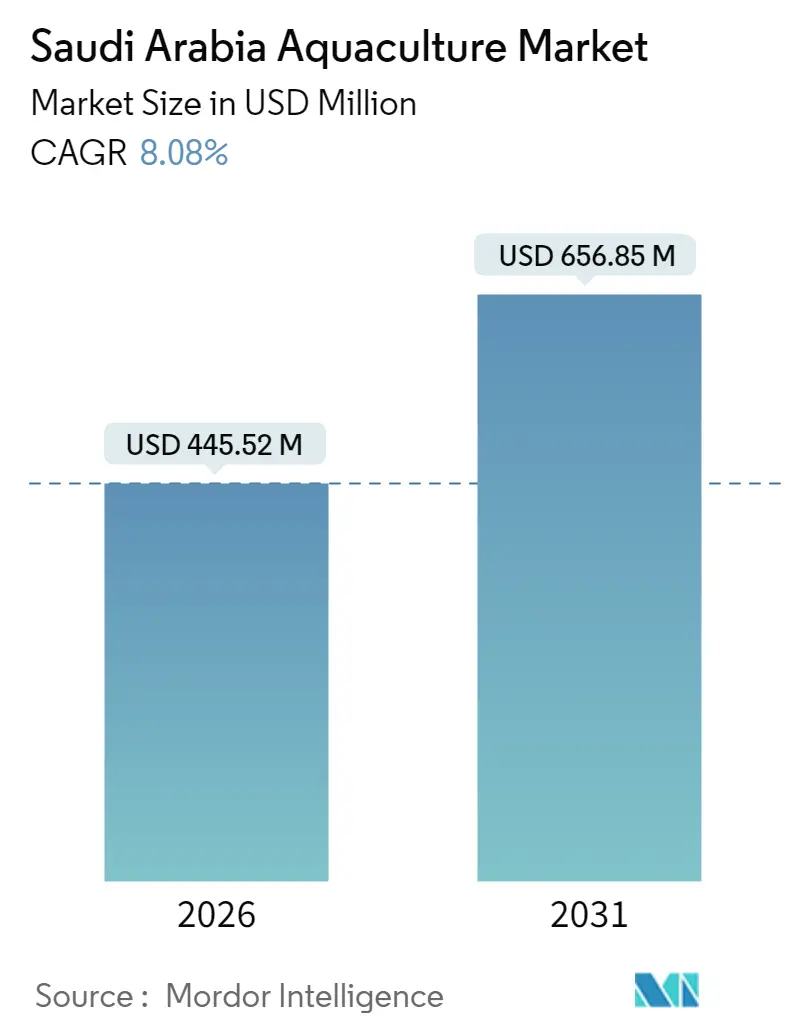

The Saudi Arabia aquaculture market size in 2026 is estimated at USD 445.52 million, growing from 2025 value of USD 412.20 million with 2031 projections showing USD 656.85 million, growing at 8.08% CAGR over 2026-2031. Recent investments in recirculating aquaculture systems (RAS), coastal cage farming, and inland desert facilities are reshaping the competitive and geographic structure of production. Government incentives, such as low-interest loans from the Saudi Agricultural Development Fund and streamlined permits under the Naama digital system, have reduced capital and administrative barriers. Rapid adoption of IoT water-quality sensors, integration of renewable-energy micro-grids, and R&D advances at King Abdullah University of Science and Technology (KAUST) are helping operators improve survival rates and lower operating costs. The sector’s gradual shift toward higher-value species, including grouper, sea bream, and marine shrimp, signals a move away from bulk, low-margin production into premium, traceable offerings that meet rising domestic food-service demand.

Key Report Takeaways

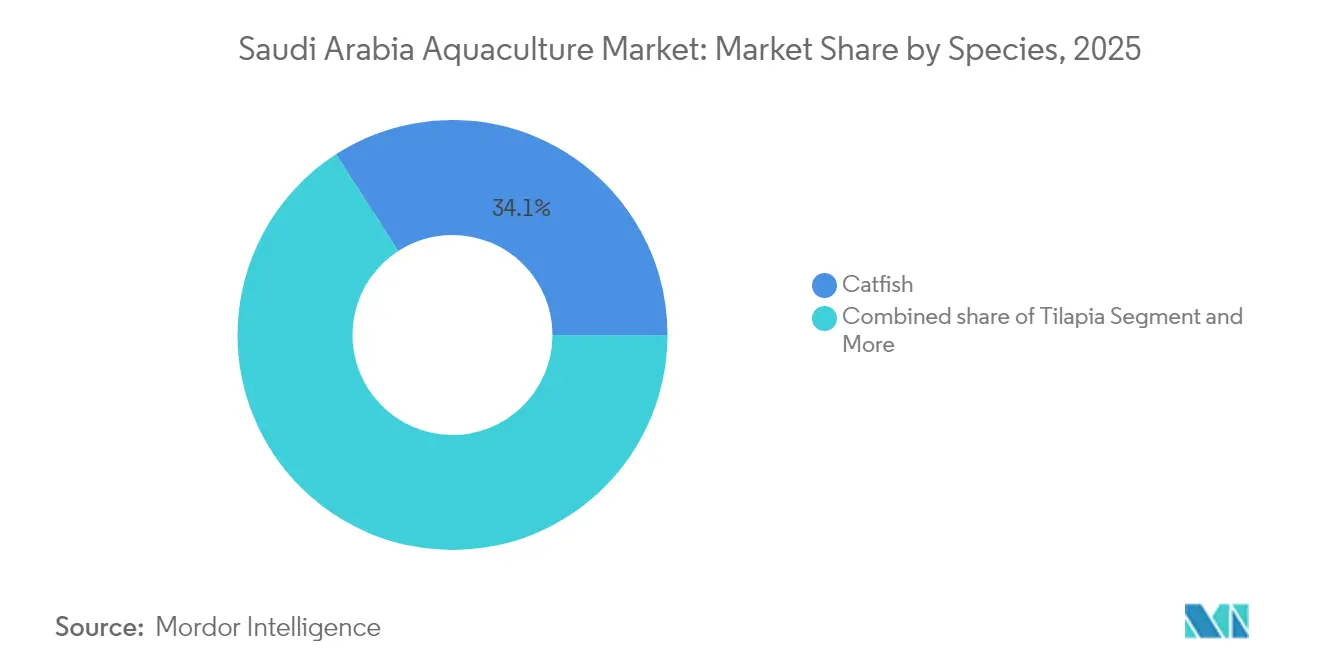

- By species, catfish held the largest 34.12% of the Saudi Arabia aquaculture market share in 2025, while shrimp is projected to post the fastest 8.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Aquaculture Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Subsidy expansion under the USDA Seafood Import Substitution Program | +1.2% | National, with a concentration in the Red Sea coastal regions | Medium term (2-4 years) |

| Growing consumer preference for domestic, traceable seafood | +1.8% | National, with higher impact in urban centers (Riyadh, Jeddah, Dammam) | Short term (≤ 2 years) |

| Advances in Recirculating Aquaculture Systems Commercial Viability | +2.1% | National, with early adoption in NEOM and Eastern Province | Long term (≥ 4 years) |

| Rapid adoption of IoT-enabled water-quality sensors in inland farms | +0.9% | National, with a focus on inland desert facilities | Medium term (2-4 years) |

| Corporate off-take agreements with food-service majors | +1.4% | National, with a concentration in major metropolitan areas | Short term (≤ 2 years) |

| State-level aquaculture permitting reforms | +0.8% | National, through MEWA's Naama digital system | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Subsidy expansion under USDA Seafood Import Substitution Program

Subsidized credit from the Saudi Agricultural Development Fund expanded lending capacity. In February 2025, combined with Sharia-compliant financing options, this has enabled companies like Balady Poultry Trading to secure USD 304 million for integrated protein production facilities that include aquaculture components. Domestic feed manufacturers have begun scaling production lines dedicated to aquafeed, locking in cost advantages across the value chain. This financial architecture creates a competitive advantage for domestic aquaculture operations by lowering capital costs and extending repayment terms beyond what traditional commercial lending would offer. In December 2024, Modern Mills' USD 40 million investment in feed milling expansion specifically targets aquaculture feed production, indicating that subsidy benefits extend throughout the value chain.

Growing consumer preference for domestic, traceable seafood

Post-pandemic supply-chain disruptions heightened demand for provenance-verified seafood, especially in fine-dining and hotel chains that dominate inbound tourism. Premium buyers are now willing to pay 15-20% premiums for locally certified product lines. These price signals, coupled with expanding e-commerce channels, have improved producer margins and incentivized investment in certification systems that log origin, feed type, and harvest date. Corporate food service contracts, particularly those serving the expanding tourism and hospitality sectors in NEOM and The Red Sea Project, are establishing long-term off-take agreements that provide revenue certainty for aquaculture investments.

Advances in Recirculating Aquaculture Systems (RAS) commercial viability

KAUST researchers have cut desalination energy demand to 2.27 kWh/m³, lowering water-treatment costs for inland RAS operations. Integration of rooftop solar arrays and battery storage has enabled some farms to cover 30–40% of electricity loads via renewables. As scale increases, hybrid power configurations are projected to reach parity with grid tariffs, making inland production commercially competitive with coastal cage farming. The commercial breakthrough is further evidenced by the emergence of specialized RAS equipment suppliers and engineering firms targeting the Saudi market, indicating mature supply chain development.

Rapid adoption of IoT-enabled water-quality sensors in inland farms

Networked probes feeding real-time dissolved-oxygen, pH, and ammonia data into cloud dashboards now underpin automated feeding and aeration algorithms. Operators report labor savings up to 30% and survival-rate improvements of 5–8 percentage points. In a desert setting where water chemistry can shift within hours, predictive alerts mitigate mass-mortality risk and reduce insurance premiums. The data generated by these sensor networks is increasingly being integrated with artificial intelligence platforms to optimize feeding schedules, predict disease outbreaks, and maximize production efficiency.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited vaccine availability for emerging pathogens | -1.1% | National, with a higher impact on marine cage operations | Medium term (2-4 years) |

| High electricity costs for energy-intensive RAS facilities | -1.6% | National, with a concentration in inland desert facilities | Long term (≥ 4 years) |

| Coastal zoning conflicts with recreational stakeholders | -0.8% | Red Sea and Arabian Gulf coastal zones | Short term (≤ 2 years) |

| Fragmented cold-chain infrastructure for live shellfish logistics | -0.7% | National, with critical gaps in remote coastal areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited vaccine availability for emerging pathogens

Recent White Spot Syndrome outbreaks underscored the vulnerability of shrimp operators relying on generic vaccines formulated for other oceans. Lack of region-specific biologics forces farms to employ costly biosecurity protocols that cap stocking densities, raising unit costs by 10–15%. International suppliers remain hesitant to invest in tailored R&D until volumes justify scale, prolonging exposure to disease shocks. This gap forces Saudi operators to rely on prophylactic treatments and enhanced biosecurity measures that increase operational costs while limiting production density and growth rates.

High electricity costs for energy-intensive RAS facilities

Industrial tariffs consume up to 25% of total operating expenses for large-scale RAS farms. Mandatory backup generators and redundant chillers inflate both capital and maintenance budgets. Solar retrofits offset part of the daytime load yet require high initial outlays and land footprints, slowing adoption among mid-sized operators. Without affordable power-purchase agreements, inland expansion could decelerate. While renewable energy integration offers long-term solutions, the upfront capital requirements for solar installations and energy storage systems create additional financing hurdles for aquaculture developers. The constraint is particularly acute for inland desert facilities that cannot benefit from natural seawater cooling and must rely entirely on mechanical systems for temperature control.

Segment Analysis

By Species: Shrimp Drives Premium Growth

Catfish maintained a 34.12% Saudi Arabia aquaculture market share in 2025 due to entrenched pond assets and a price point suited to mass retail. Shrimp is on track for a 8.72% CAGR through 2031, the fastest among all species, fueled by USD 3.7 billion Saudi-Chinese joint-venture funding for genetics and hatchery scale-up. Strong export premiums and expanding Gulf airline cargo hold capacity underpin the species’ margin profile. Tilapia holds a sizeable share in inland provinces because it tolerates variable water quality and commands lower feed costs, while niche operators are trialing high-value grouper, barramundi, and salmon in pilot RAS modules.

Consumer demand for sustainably raised crustaceans motivates farms to invest in traceability and antibiotic-free grow-out protocols, winning certification from the SAMAQ national quality mark. Arabian Shrimp Company’s hatchery expansions point to centralized post-larvae supply, reducing biosecurity risk for smaller growers. Although catfish volumes will continue to anchor domestic protein supply, revenue contribution from shrimp is projected to surpass catfish by 2030 as the price per kilogram doubles that of freshwater staples. These dynamics indicate an increasing bifurcation between affordable mass protein and premium export-oriented lines.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The Arabian Gulf coast, anchored by Dammam and Jubail, complements Red Sea output with quick access to major population hubs. Operators here leverage industrial utilities, existing cold-storage hubs, and petrochemical by-products for feedstock and energy integration. Higher salinity and seasonal thermal spikes necessitate species selection attuned to extreme parameters, yet offer niche premium species that command elevated price points in gourmet channels. The Red Sea Project's marine spatial planning process, while comprehensive, has designated significant coastal areas for tourism and conservation uses that exclude traditional aquaculture operations.

Production clusters span the Red Sea coast, Arabian Gulf shoreline, and emerging desert interiors. The Red Sea stretch from Jeddah to Umluj hosts the bulk of licensed cage capacity owing to stable salinity and year-round temperature profiles. NEOM-linked infrastructure upgrades, including dedicated service harbors and solar-powered desalination plants, position the region as a springboard for premium export campaigns. Environmental-baseline surveys completed in 2024 furnish granular data that inform site placement and carrying-capacity thresholds, aiding sustainable expansion.

Desert-based RAS campuses form a third node, freeing investors from maritime zoning while exploiting cheap land and abundant solar irradiance. Proximity to logistics corridors shortens haul times to Riyadh’s wholesale markets. KAUST pilot sites demonstrate integrated water-reuse and mineral-extraction schemes that upgrade waste brine into commercial co-products, creating circular-economy revenue streams. As policy incentives target water-efficient agriculture, desert aquaculture stands to capture incremental slices of the Saudi Arabia aquaculture market share in the medium term.

Recent Industry Developments

- May 2025: Saudi Arabia formalized SAR 14 billion (USD 3.7 billion) in agriculture and fisheries investment agreements during a bilateral business forum, earmarking funds for shrimp genetics, seaweed farms, and integrated food-security cities with aquaculture components.

- March 2025: Modern Mills invested USD 40 million to expand its feed milling operations in Saudi Arabia, focusing on aquaculture feed production. This expansion supports the government's initiatives to strengthen domestic feed supply chains and reduce the aquaculture sector's dependence on imports.

- February 2024: NEOM and Tabuk Fisheries established a joint venture, Topian Aquaculture, with approval from Saudi Arabia's Ministry of Environment, Water, and Agriculture (MEWA). The venture plans to construct the Middle East and North Africa region's largest hatchery and marine-pen finfish production facility, supporting Saudi Arabia's goal to produce 600,000 metric tons of fish products annually by 2030.

Saudi Arabia Aquaculture Market Report Scope

Aquaculture is the farming of aquatic organisms, including fish, mollusks, and crustaceans. Fisheries can be defined as raising and harvesting wild marine and freshwater fish for food or industrial purposes. Aquaculture is one of Saudi Arabia's fastest-expanding food production sectors. The Saudi Arabia Aquaculture Market is Segmented by Type Into Unprocessed, and Processed. The report includes Production Analysis (Volume), Consumption Analysis (Value and Volume), Export Analysis (Value and Volume), Import Analysis (Value and Volume), and Price Trend Analysis. The report offers market size and forecasts in terms of value (USD) and volume (Metric Tons) for all the above segments.

By Species (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis)

| Catfish |

| Salmonids (Atlantic, Steelhead) |

| Tilapia |

| Shellfish (Oysters, Mussels, Clams) |

| Shrimp |

| Other Species (Sturgeon, Striped Bass) |

| By Species (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis) | Catfish |

| Salmonids (Atlantic, Steelhead) | |

| Tilapia | |

| Shellfish (Oysters, Mussels, Clams) | |

| Shrimp | |

| Other Species (Sturgeon, Striped Bass) |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Saudi Arabia aquaculture market in 2026?

The sector is valued at USD 445.52 million in 2026 and is on track to reach USD 656.85 million by 2031.

What growth rate is projected for Saudi aquaculture through 2031?

The Saudi Arabia aquaculture market is forecast to register an 8.08% CAGR over 2026-2031.

Which species is growing the quickest?

Shrimp is forecast to register a 8.72% CAGR as export demand and genetics programs scale up.

How are energy costs affecting inland aquaculture?

Electricity accounts for up to 25% of RAS operating expenses, prompting operators to adopt solar and battery solutions to mitigate tariff exposure.

Which factors most limit coastal cage expansion?

Zoning conflicts with tourism, conservation mandates, and recreational stakeholders restrict site availability along prime Red Sea and Arabian Gulf coastlines.