| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 5.77 Billion |

| Market Size (2030) | USD 9.01 Billion |

| CAGR (2025 - 2030) | 9.31 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Anti-Jamming Equipment Market Analysis

The Anti Jamming Equipment Market size is estimated at USD 5.77 billion in 2025, and is expected to reach USD 9.01 billion by 2030, at a CAGR of 9.31% during the forecast period (2025-2030).

The anti-jamming equipment industry continues to evolve rapidly as wireless networks become increasingly vulnerable to sophisticated interference threats. Traditional anti-jamming technologies like sequence-based frequency hopping and direct sequence spread spectrum face limitations in spectral efficiency and rigid communication patterns. The advancement of software-defined radio has led to more complex and efficient jamming devices, necessitating more robust protection measures. GPS signals are particularly susceptible to interference, with studies showing that even a small 10-watt jammer can disrupt signals within a 30-kilometer line of sight, highlighting the critical need for enhanced protection mechanisms.

The industry is witnessing significant technological transformation through the integration of artificial intelligence and machine learning capabilities. In February 2024, ADVA launched a centralized GNSS monitoring and assurance tool leveraging AI and machine learning for remote identification of problems and protection against GNSS vulnerabilities, including jamming and spoofing attacks. This technological evolution reflects the industry's move towards more sophisticated and automated protection systems. The global installed base of GNSS devices is projected to reach 9.5 billion units by 2029, indicating the expanding scope and criticality of anti-jamming solutions.

Strategic industry partnerships and collaborations are reshaping the competitive landscape. In October 2023, CS Group partnered with Thales to develop a cyber-secure, jam-resistant navigation system inspired by civil aviation technologies. Similarly, infiniDome, Honeywell, and Easy Aerial demonstrated the first UAV-tailored resilient navigation solution in late 2023, integrating GPS anti-jamming technology with inertial and radar velocity systems. These collaborations are driving innovation in specialized anti-jamming system solutions for different applications and environments.

The market is experiencing a shift towards comprehensive electronic warfare protection systems. In November 2023, EDGE launched GPS-Protect, an innovative anti-jamming system covering aeronautical, land, and sea applications, demonstrating the industry's move towards integrated solutions. Honeywell has enhanced its GPSdome anti-jamming system with additional protection layers, including a Compact Inertial Navigation System and Radar Velocity System, showcasing the industry's focus on multi-layered defense mechanisms. These developments indicate a growing trend towards more sophisticated and comprehensive anti-jamming technology solutions that can address multiple threat vectors simultaneously.

Anti Jamming Equipment Market Trends

Increased Demand for GPS Technology in Military Applications

The ubiquity of GPS technology and growing requirements for superior military navigation systems are driving significant innovations in GPS design, with a focus on reducing size and weight while improving precision. Military forces worldwide are investing heavily in modernizing their aircraft and unmanned aerial vehicles, with most platforms utilizing GNSS (GPS) and TACAN positioning and navigation systems. A notable development is the U.S. Air Force's initiative to equip its fighter aircraft fleet with next-generation GPS receivers, starting with the F-16 fleet receiving the latest-generation Digital GPS Anti-Jam Receiver (DIGAR) from Rockwell Collins, marking a significant advancement in military GPS technology adoption.

The military's increasing reliance on GPS-enabled equipment for mission-critical operations has expanded beyond basic navigation to include sophisticated applications such as target acquisition, search and rescue, command and control, and precise digital mapping. This expansion is evidenced by Japan's record defense budget approval of JPY 7.95 trillion (USD 55.9 billion) for 2024, representing a 16.5% increase from FY2023, with a significant portion allocated to modernizing GPS and navigation systems. The integration of GPS anti-jamming technology in military applications has become more sophisticated, with systems now capable of collecting and processing satellite data to determine precise geographic locations while maintaining operational security in contested environments. The military jammer market is also seeing growth as these technologies become more essential.

Understand The Key Trends Shaping This Market

Download PDF

Improving Overall GPRS Infrastructure

The evolution of GPRS infrastructure has been marked by significant technological advancements, transitioning from traditional packet-switched services to more sophisticated systems that support modern military and civilian applications. The emergence of EDGE and Universal Mobile Telecommunications Service (UMTS), coupled with the advancement of GSM with GPRS, has established cellular data technology as a crucial component in global communications. These improvements have led to reduced connection setup times and optimized radio resource utilization, with GPRS services now capable of multiplexing packet data from multiple stations efficiently.

Current GSM operators are leveraging GPRS as a fundamental network platform to not only expand the wireless data market but also to create IMT-2000 frequencies when acquired. The technology's ability to cover large geographical areas, adapt to varying terrain conditions, and its ease of installation make it particularly valuable for military applications. In February 2024, this advancement was exemplified by Safran Electrical & Power's announcement of a new facility in Singapore dedicated to manufacturing and maintaining aeronautical electrical equipment, demonstrating the ongoing evolution of GPRS infrastructure and its integration with modern aviation systems.

Rising Demand for Unmanned Airborne Vehicles and Systems

The unmanned airborne vehicles (UAV) sector is experiencing unprecedented growth, driven by both military and commercial applications requiring sophisticated anti-jamming device capabilities. The stakes in aerial operations are particularly high, with GNSS interference representing one of the most serious threats to drone safety. At minimum, satellite signal disruptions can degrade position quality, triggering fallbacks from high-precision RTK and PPP modes to less-precise modes, while severe cases can result in complete loss of signal tracking and positioning capabilities. This has led to increased investment in developing robust anti-jamming system solutions specifically designed for UAV applications.

The integration of GNSS anti-jamming technology in UAV systems has become increasingly sophisticated, with companies developing specialized solutions to address the unique challenges faced by unmanned systems. For instance, in February 2024, Safran's expansion in Singapore with a new facility focused on aeronautical electrical equipment manufacturing and maintenance demonstrates the growing emphasis on developing robust UAV systems with enhanced anti-jamming capabilities. The proximity of other electrical and electronic devices in UAVs, due to limited space, has made the implementation of anti-jamming device solutions particularly crucial, driving innovations in compact, efficient anti-jamming technologies that can maintain reliable GNSS connectivity while operating in contested environments.

Segment Analysis: By Technology

Beam Steering Techniques Segment in Anti-Jamming Equipment Market

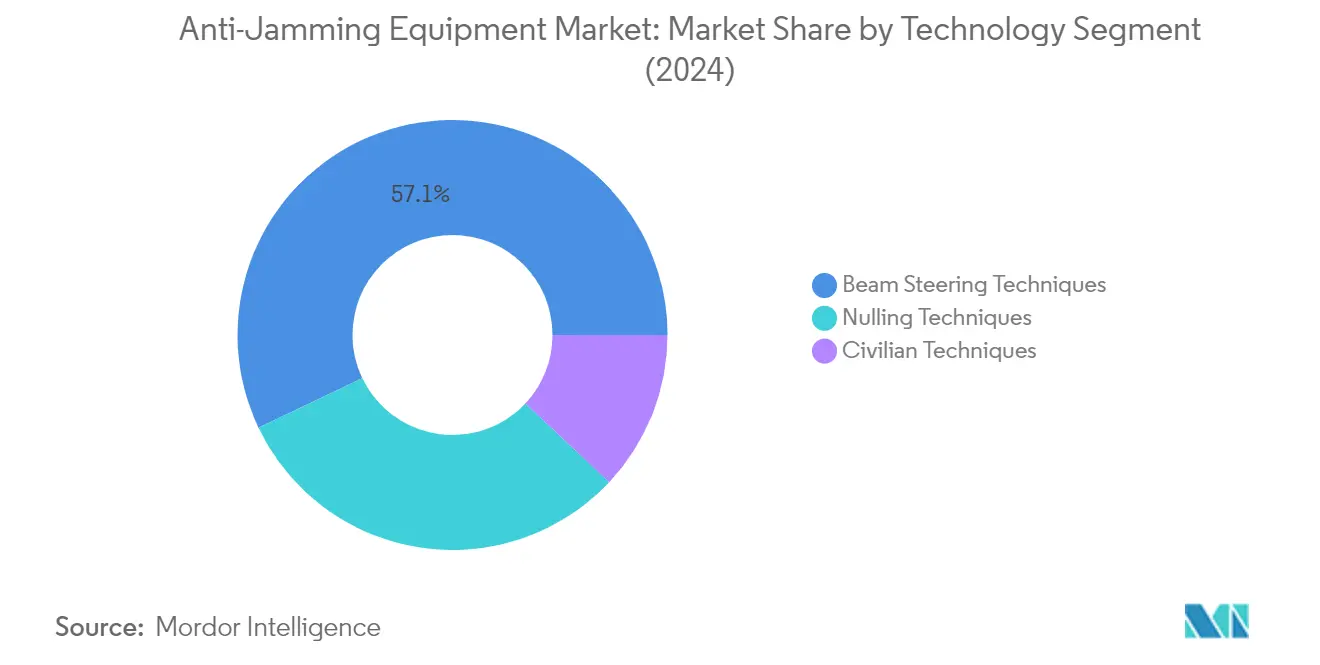

The Beam Steering Techniques segment dominates the global anti-jamming equipment market, commanding approximately 57% market share in 2024, equivalent to USD 2,668.94 million. This segment's prominence is driven by its superior effectiveness in providing vital protection against opposing jammers and spoofers through high-end beam-steering capability, allowing host platforms to survive the harshest contested environments. The technology's ability to maintain continuous satellite tracking in high levels of hostile jamming while offering seamless integration with existing systems has made it particularly attractive for military applications. Additionally, this segment is experiencing the fastest growth rate of around 13% through 2024-2029, attributed to its increasing adoption in advanced defense platforms, unmanned aerial vehicles, and modern warfare systems requiring precise navigation capabilities.

Civilian Techniques Segment in Anti-Jamming Equipment Market

The Civilian Techniques segment represents a crucial component of the anti-jamming equipment market, focusing on providing enhanced GPS signal reception capabilities for commercial and civilian applications. This segment has gained significant traction due to the growing adoption of GPS technology in various civilian sectors, including commercial vehicles, autonomous systems, and critical infrastructure. The technology's ability to counter unintentional jamming and commercial-grade interference while maintaining cost-effectiveness has made it particularly attractive for civilian applications. The segment's growth is further supported by increasing investments in civilian GPS infrastructure and the rising demand for reliable navigation systems in commercial transportation and logistics sectors.

Remaining Segments in Anti-Jamming Equipment Market by Technology

The Nulling Techniques segment plays a vital role in the anti-jamming equipment market by offering specialized solutions for signal interference mitigation. This technology utilizes sophisticated algorithms to create null patterns in the direction of jamming sources, effectively eliminating interference while maintaining desired signal reception. The segment's significance is particularly evident in applications requiring robust protection against multiple jamming sources, including military communications, surveillance systems, and critical infrastructure protection. The technology's ability to adapt to various jamming scenarios while maintaining operational efficiency has established it as a crucial component in the overall anti-jamming ecosystem.

Segment Analysis: By End-User Application

Navigation, Position & Timing Segment in Anti-Jamming Equipment Market

The Navigation, Position & Timing segment dominates the anti-jamming system market, holding approximately 35% market share in 2024. This segment's prominence is driven by the universal use of GPS for critical navigation and timing applications across military and commercial sectors. The increasing concern over GPS signal jamming has led to significant investments in anti-jamming systems, particularly for military operations where precise positioning and timing are crucial. Modern navigation, communication, and electronic warfare systems heavily depend on GNSS availability for Position, Navigation, and Timing (PNT), making assured PNT a critical requirement. The segment's growth is further supported by the development of next-generation GPS III programs and the transition from selective-availability anti-spoofing module (SAASM) to modernized M-code encryption, enhancing the resilience of space and control segments of the GNSS architecture.

Surveillance & Reconnaissance Segment in Anti-Jamming Equipment Market

The Surveillance & Reconnaissance segment is experiencing the most rapid growth in the anti-jamming equipment market, with an expected CAGR of approximately 14% from 2024 to 2029. This exceptional growth is primarily driven by the increasing adoption of unmanned aerial vehicles (UAVs) for surveillance and reconnaissance missions, which require robust anti-jamming device capabilities to maintain continuous operation in contested environments. The segment's expansion is further fueled by the rising focus on enhancing surveillance and anti-terrorism capabilities, particularly in regions experiencing heightened security concerns. Military forces worldwide are increasingly investing in GPS anti-jamming solutions for their surveillance platforms to ensure uninterrupted intelligence gathering and reconnaissance operations, even in environments with sophisticated jamming threats.

Remaining Segments in Anti-Jamming Equipment Market by End-User Application

The remaining segments in the anti-jamming equipment market include Flight Control, Casualty Evacuation, and Other End-user Applications, each serving crucial roles in military and civilian operations. The Flight Control segment is particularly significant for aircraft operations, ensuring reliable navigation and communication systems in contested airspace. The Casualty Evacuation segment focuses on maintaining uninterrupted GPS signals during critical medical evacuations and emergency response situations. Other End-user Applications encompass various specialized uses, including law enforcement operations and logistics applications, where maintaining reliable positioning and navigation capabilities is essential for mission success.

Anti Jamming Equipment Market Geography Segment Analysis

Anti-Jamming Equipment Market in North America

North America maintains a dominant position in the global anti-jamming equipment market, driven by significant military modernization initiatives and extensive GPS technology adoption across defense applications. The United States and Canada are the key contributors to the region's market growth, with both countries investing heavily in advanced anti-jamming solutions for their military platforms. The region's market is characterized by the presence of major defense contractors and continuous technological innovations in GPS anti-jamming systems, particularly for applications in flight control, surveillance, and reconnaissance operations.

Anti-Jamming Equipment Market in United States

The United States leads the North American anti-jamming market as the largest country segment, commanding approximately 87% of the regional market share in 2024. The country's dominance is attributed to its extensive military infrastructure and substantial defense budget allocations for GPS technology advancement. The US Department of Defense's continued focus on enhancing military navigation capabilities and protecting critical GPS-dependent systems drives market growth. The presence of leading defense contractors and research institutions further strengthens the country's position in developing cutting-edge anti-jamming solutions for various military applications.

Anti-Jamming Equipment Market in Canada

Canada emerges as the fastest-growing market in North America, with a projected growth rate of approximately 14% during 2024-2029. The country's market expansion is driven by increasing investments in military modernization programs and a growing emphasis on securing navigation systems for defense applications. Canadian defense forces are actively incorporating advanced anti-jamming technologies across their military platforms, particularly in surveillance and reconnaissance operations. The country's focus on developing indigenous defense capabilities and partnerships with global defense contractors continues to create new opportunities in the anti-jamming equipment market.

Anti-Jamming Equipment Market in Europe

The European anti-jamming equipment market demonstrates robust growth potential, supported by increasing defense modernization initiatives across major economies, including the United Kingdom, Germany, and France. The region's market is characterized by strong technological capabilities and a strategic focus on enhancing military navigation systems. European nations are actively investing in advanced anti-jamming solutions to counter emerging threats to GPS-dependent military operations, while also fostering collaboration between defense contractors and research institutions to develop innovative anti-jamming technologies.

Anti-Jamming Equipment Market in United Kingdom

The United Kingdom maintains its position as the largest market in Europe, holding approximately 33% of the regional market share in 2024. The country's strong market position is supported by its comprehensive defense modernization programs and significant investments in military GPS technology. British defense forces are actively incorporating advanced anti-jamming systems across various military platforms, including aircraft, naval vessels, and ground vehicles. The presence of major defense contractors and research institutions further strengthens the UK's position in developing sophisticated anti-jamming solutions.

Anti-Jamming Equipment Market in France

France demonstrates the highest growth potential in the European market, with a projected growth rate of approximately 12% during 2024-2029. The country's market expansion is driven by an increasing focus on military modernization and growing investments in advanced navigation protection systems. French defense forces are actively upgrading their military platforms with sophisticated anti-jamming capabilities, particularly in aerospace and naval applications. The country's strong aerospace and defense industrial base, coupled with ongoing military modernization initiatives, continues to drive innovation in anti-jamming technologies.

Anti-Jamming Equipment Market in Asia-Pacific

The Asia-Pacific region represents a rapidly evolving market for anti-jamming equipment, with China, Japan, and South Korea emerging as key contributors to regional growth. The market is characterized by increasing defense budgets, growing regional tensions, and rising adoption of GPS technology in military applications. Countries across the region are actively investing in advanced anti-jamming solutions to enhance their military capabilities and protect critical navigation systems from emerging threats.

Anti-Jamming Equipment Market in China

China maintains its position as the largest market in the Asia-Pacific region, driven by extensive military modernization programs and significant investments in GPS technology. The country's defense forces are actively incorporating advanced anti-jamming systems across various military platforms, including aircraft, naval vessels, and ground vehicles. China's strong domestic defense industrial base and focus on technological self-reliance continue to drive innovations in anti-jamming solutions.

Anti-Jamming Equipment Market in South Korea

South Korea emerges as the fastest-growing market in the Asia-Pacific region, supported by increasing defense modernization initiatives and a growing focus on securing military navigation systems. The country's defense forces are actively upgrading their military platforms with sophisticated anti-jamming capabilities, particularly in response to regional security challenges. South Korea's strong technological capabilities and partnerships with global defense contractors continue to drive advancements in anti-jamming solutions.

Anti-Jamming Equipment Market in Rest of the World

The Rest of the World market, encompassing regions such as Latin America and the Middle East & Africa, demonstrates growing potential in the anti-jamming equipment market. These regions are witnessing increased adoption of GPS technology in military applications and growing investments in defense modernization programs. The market is characterized by rising awareness about the importance of securing navigation systems and increasing defense budgets across various countries. The presence of emerging military powers and a growing focus on enhancing defense capabilities continue to create new opportunities for anti-jamming equipment manufacturers in these regions.

Get Analysis on Important Geographic Markets

Download PDF

Anti-Jamming Equipment Industry Overview

Top Companies in Anti-Jamming Equipment Market

The anti-jamming equipment market features prominent players like Raytheon Technologies, Collins Aerospace, BAE Systems, Lockheed Martin, and Thales Group leading the innovation landscape. These companies demonstrate a strong focus on developing advanced digital beamforming technologies, controlled reception pattern antennas (CRPA), and integrated GPS anti-jamming systems. Strategic collaborations with defense agencies and research institutions have accelerated product development cycles and market penetration. Companies are expanding their portfolios through investments in size, weight, and power (SWaP) optimization and multi-constellation compatibility. The emphasis on M-Code compliance and enhanced jamming immunity has driven continuous product improvements. Market leaders are also pursuing geographical expansion through local partnerships and the establishment of regional centers of excellence.

Defense Conglomerates Dominate Consolidated Market Structure

The anti-jamming equipment market exhibits a relatively consolidated structure dominated by large defense and aerospace conglomerates with established government relationships and extensive R&D capabilities. These major players leverage their broad technology portfolios, manufacturing scale, and deep customer relationships to maintain market leadership. The high barriers to entry, including significant capital requirements, stringent regulatory compliance needs, and complex certification processes, have limited the emergence of new independent players. The market has witnessed strategic acquisitions aimed at enhancing technology capabilities and regional market access.

The competitive dynamics are shaped by the presence of specialized technology providers focusing on niche applications alongside the dominant integrated solution providers. While global defense contractors maintain leadership in military applications, regional players have carved out positions in commercial and civilian segments. The industry has seen increased collaboration between established players and technology startups, particularly in areas like artificial intelligence integration and software-defined solutions. Market participants are also pursuing vertical integration strategies to strengthen their position in the value chain.

Innovation and Integration Drive Market Success

Success in the anti-jamming equipment market increasingly depends on the ability to deliver integrated solutions that address evolving threat scenarios while maintaining cost competitiveness. Incumbent players must focus on continuous innovation in digital signal processing, adaptive antenna technologies, and artificial intelligence integration to maintain their market positions. The development of modular, scalable architectures that enable easy upgrades and customization has become crucial. Companies need to strengthen their cybersecurity capabilities and demonstrate the ability to protect against sophisticated jamming and spoofing threats.

Market contenders can gain ground by focusing on specialized applications and emerging market segments while building strategic partnerships for technology access and market reach. The ability to offer flexible deployment options and seamless integration with existing systems will be critical for market success. Companies must also navigate the complex regulatory landscape while maintaining strong relationships with defense agencies and system integrators. The increasing focus on commercial applications presents opportunities for differentiation through innovative business models and service-based offerings. Future success will depend on balancing technical excellence with operational efficiency and customer responsiveness.

Anti Jamming Equipment Market Leaders

-

RTX Corporation

-

Chelton Limited

-

Novatel Inc. (Hexagon AB)

-

Mayflower Communications

-

Lockheed Martin Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Anti-Jamming Equipment Market News

- September 2024: Lockheed Martin and Tata Advanced Systems Limited solidified their partnership with a partnership agreement centered on the C-130J Super Hercules tactical airlift. This move would bolster India’s defense and aerospace and strengthen the strategic bond between India and the United States.

- April 2024: Raytheon, a leading US defense contractor and a subsidiary of RTX, planned to enhance its 'Controlled, Advanced, Distributed Radio Frequency Effects' (CADRE) system for seamless integration with the US Navy's Next Generation Jammer.

Anti Jamming Equipment Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of Macroeconomic Factors on the Market

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Increased Demand for GPS Technology in Military Applications

- 5.1.2 Improving Overall GPRS Infrastructure

- 5.1.3 Rising Demand for Unmanned Airborne Vehicles and Systems

-

5.2 Market Restraints

- 5.2.1 Complexity in Manufacturing

- 5.2.2 Interoperability with Existing Systems

6. MARKET SEGMENTATION

-

6.1 Technology

- 6.1.1 Nulling Technique

- 6.1.2 Civilian Techniques

- 6.1.3 Beam Steering Techniques

-

6.2 End-user Application

- 6.2.1 Flight Control

- 6.2.2 Defense

- 6.2.3 Surveillance and Reconnaissance

- 6.2.4 Navigation, Position, and Timing

- 6.2.5 Casualty Evacuation

- 6.2.6 Other End-user Applications

-

6.3 Geography***

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 Germany

- 6.3.2.2 United Kingdom

- 6.3.2.3 France

- 6.3.3 Asia

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 South Korea

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles

- 7.1.1 RTX Corporation

- 7.1.2 Chelton Limited

- 7.1.3 Novatel Inc. (Hexagon AB)

- 7.1.4 Mayflower Communications

- 7.1.5 Lockheed Martin Corporation

- 7.1.6 Safran

- 7.1.7 L3Harris Technologies Inc.

- 7.1.8 BAE Systems PLC

- 7.1.9 Israel Aerospace Industries Ltd

- 7.1.10 Thales Group

- 7.1.11 Forsberg Services Ltd

- 7.1.12 Tualcom

- 7.1.13 Septentrio NV

- *List Not Exhaustive

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

**Subject to Availability

***In the final report, Asia, Australia, and New Zealand will be studied together as 'Asia Pacific' and Latin America and Middle East and Africa will be considered together as 'Rest of the World'.' The final report's geography segment will also include Rest of Europe and Asia Pacific.

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Anti-Jamming Equipment Industry Segmentation

Anti-jamming equipment protects signal receivers from intervention and deliberate jamming. For instance, when a GPS signal reaches the earth's surface, it becomes weak and susceptive to being overcome by more powerful radio frequency (RF) energy. GPS anti-jamming handles power minimization to decrease the effect of interference and jamming so that the GPS receiver can continue to function correctly. The market's scope is limited to anti-jamming equipment offered by market vendors, which includes civilian and defense applications.

The anti-jamming equipment market is segmented by technology (nulling technique, civilian techniques, and beam steering techniques), end-user application (flight control, defense, surveillance and reconnaissance, navigation, position, timing, casualty evacuation, and other end-user applications), and geography (North America (United States, Canada), Europe (Germany, United Kingdom, France, rest of Europe), Asia-Pacific (China, Japan, South Korea, rest of Asia-Pacific) and rest of the World). The report offers market forecasts and size in value (USD) for all the above segments.

| Technology | Nulling Technique | ||

| Civilian Techniques | |||

| Beam Steering Techniques | |||

| End-user Application | Flight Control | ||

| Defense | |||

| Surveillance and Reconnaissance | |||

| Navigation, Position, and Timing | |||

| Casualty Evacuation | |||

| Other End-user Applications | |||

| Geography*** | North America | United States | |

| Canada | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Asia | China | ||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Latin America | |||

| Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Anti Jamming Equipment Market Research FAQs

How big is the Anti Jamming Equipment Market?

The Anti Jamming Equipment Market size is expected to reach USD 5.77 billion in 2025 and grow at a CAGR of 9.31% to reach USD 9.01 billion by 2030.

What is the current Anti Jamming Equipment Market size?

In 2025, the Anti Jamming Equipment Market size is expected to reach USD 5.77 billion.

Who are the key players in Anti Jamming Equipment Market?

RTX Corporation, Chelton Limited, Novatel Inc. (Hexagon AB), Mayflower Communications and Lockheed Martin Corporation are the major companies operating in the Anti Jamming Equipment Market.

Which is the fastest growing region in Anti Jamming Equipment Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Anti Jamming Equipment Market?

In 2025, the North America accounts for the largest market share in Anti Jamming Equipment Market.

What years does this Anti Jamming Equipment Market cover, and what was the market size in 2024?

In 2024, the Anti Jamming Equipment Market size was estimated at USD 5.23 billion. The report covers the Anti Jamming Equipment Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Anti Jamming Equipment Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Anti Jamming Equipment Market Research

Mordor Intelligence provides a comprehensive analysis of the anti jamming equipment market, utilizing our extensive expertise in defense and navigation technology research. Our detailed report explores the evolution of anti jamming technology across various applications. This includes GPS anti-jamming solutions and advanced GNSS anti jamming systems. The analysis covers emerging trends in anti-jamming system development, with a particular focus on military jammer market dynamics and navigation security solutions.

The report, available as an easy-to-download PDF, offers stakeholders actionable insights into anti jamming device innovations and military radio jamming solutions. Our analysis addresses critical developments in navigation anti interference antenna technologies and signal jammer market trends. It also examines the growing importance of GPS anti-jamming capabilities in military applications. The report provides valuable intelligence on military GNSS devices and anti-jamming solutions, enabling businesses to make informed decisions in this rapidly evolving sector.