Anti Infective Drugs Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

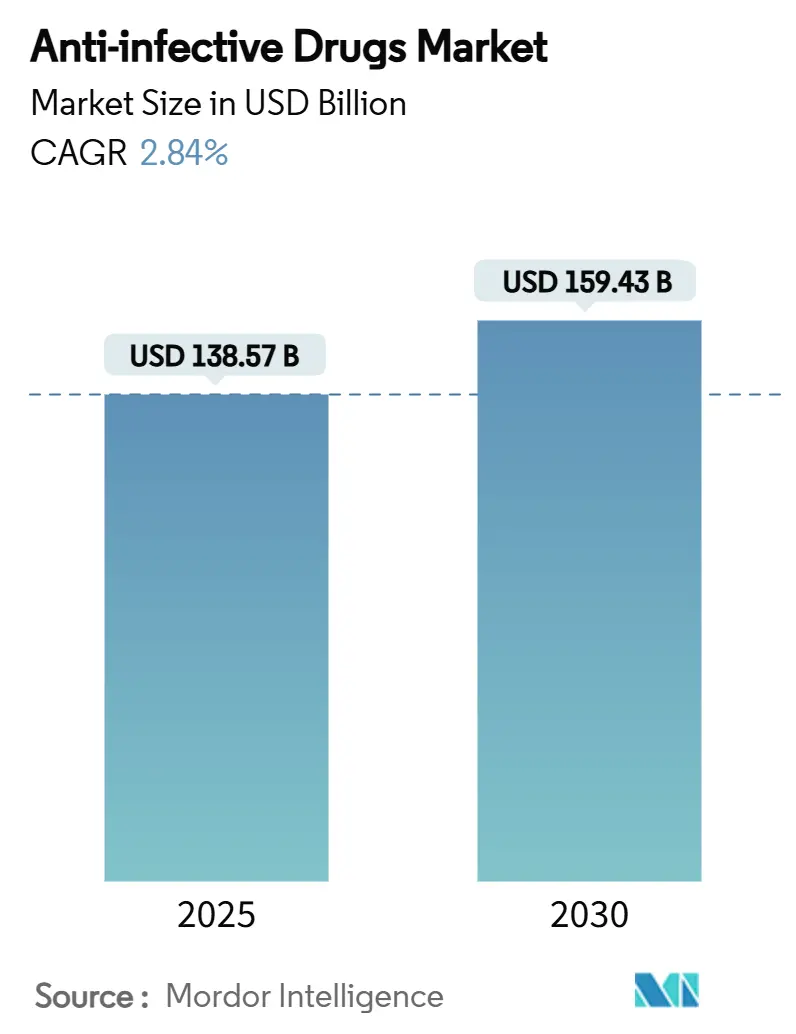

| Market Size (2025) | USD 138.57 Billion |

| Market Size (2030) | USD 159.43 Billion |

| Growth Rate (2025 - 2030) | 2.84% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Anti Infective Drugs Market Analysis by Mordor Intelligence

The Anti-infective Drugs Market size is estimated at USD 138.57 billion in 2025, and is expected to reach USD 159.43 billion by 2030, at a CAGR of 2.84% during the forecast period (2025-2030).

This steady expansion in the anti-infective drugs market is sustained by urgent public-health demand, regulatory incentives, and sustained R&D funding against a backdrop of rising antimicrobial resistance (AMR). The regulatory environment remains supportive, exemplified by the FDA’s June 2025 final guidance that streamlines antibacterial development pathways for high-unmet-need infections. Supply-chain vulnerabilities persist because 67% of global active-pharmaceutical-ingredient capacity clusters in India and China, exposing the anti-infective drugs market to geopolitical and logistics risk. Meanwhile, technology-enabled stewardship initiatives and AI-driven discovery partnerships underpin new therapeutics that address resistant pathogens, tempering the downside impact of maturing first-generation drug classes on overall growth.

Key Report Takeaways

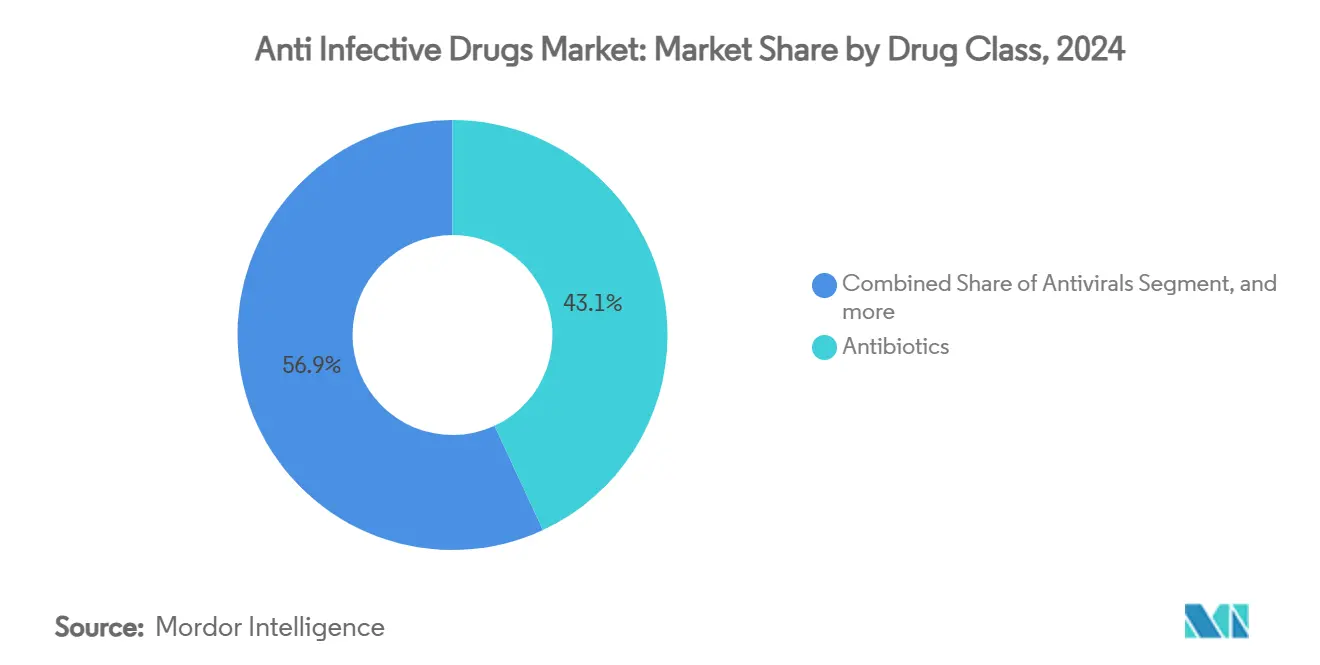

- By drug class, antibiotics led with 43.08% of the anti-infective drugs market share in 2024, while antivirals are projected to expand at a 4.73% CAGR through 2030.

- By indication, HIV infection commanded 27.33% of the anti-infective drugs market size in 2024, and respiratory virus infections are advancing at a 4.51% CAGR to 2030.

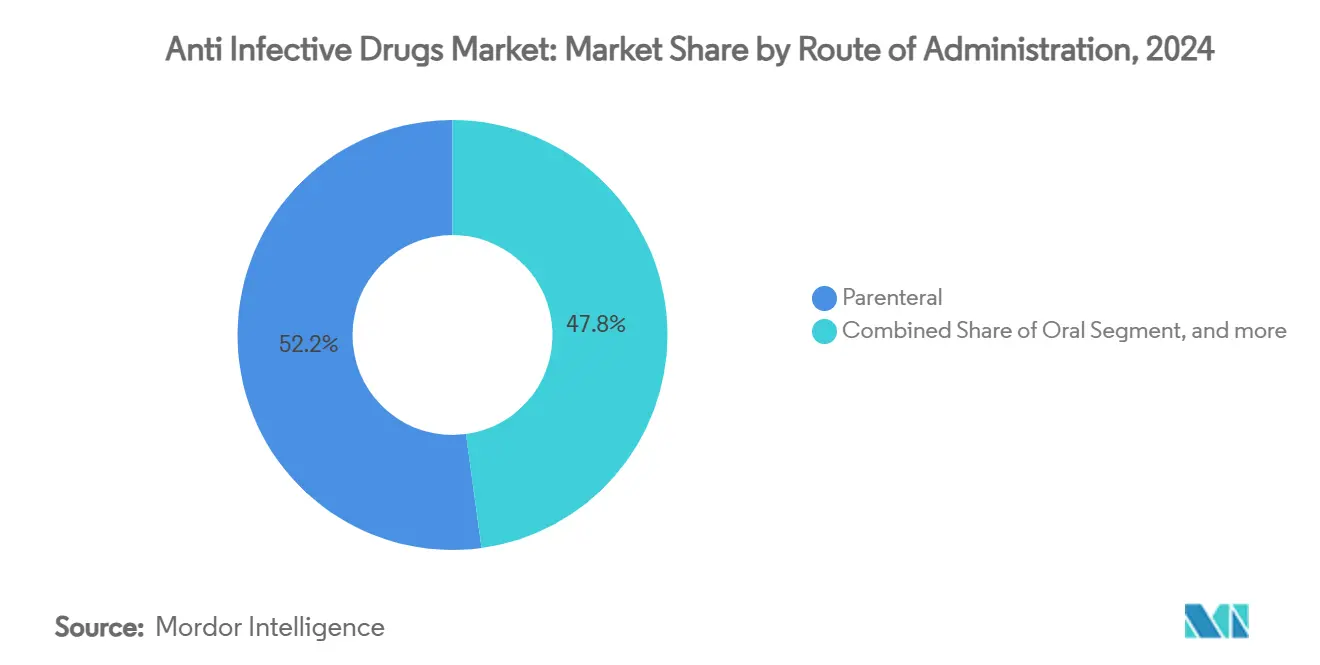

- By route of administration, parenteral delivery accounted for 52.16% share of the anti-infective drugs market size in 2024; inhalation systems are growing at a 5.22% CAGR over the forecast horizon.

- By distribution channel, hospital pharmacies controlled 59.24% share of the anti-infective drugs market size in 2024, whereas online pharmacies record the highest projected CAGR at 6.77% through 2030.

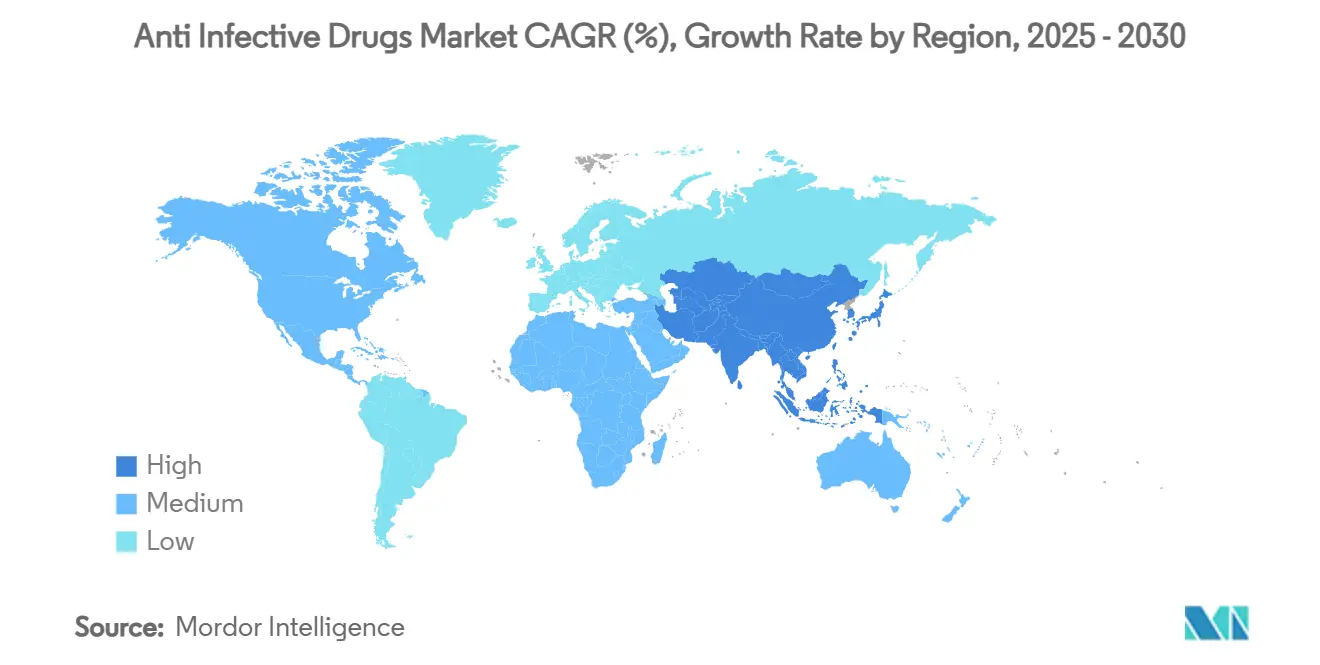

- By geography, North America dominated with 33.74% share of the anti-infective drugs market size in 2024, yet Asia-Pacific is the fastest-growing region at 3.77% CAGR to 2030.

Global Anti Infective Drugs Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of infectious diseases | +0.8% | Global, highest in Asia-Pacific & Sub-Saharan Africa | Medium term (2-4 years) |

| Growing resistance among pathogens | +0.6% | Global, acute in South Asia & Eastern Europe | Long term (≥ 4 years) |

| Robust R&D investment & public-private ties | +0.4% | North America & EU core; spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Advanced drug-development technologies | +0.3% | North America & EU; emerging adoption in China & India | Medium term (2-4 years) |

| Access via stewardship & global programs | +0.2% | Global, priority focus on low- and middle-income countries | Medium term (2-4 years) |

| Analytics-driven antimicrobial stewardship | +0.1% | North America & EU; expanding into major Asia-Pacific markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Infectious Diseases

Sepsis-linked inpatient stays, costs and mortality continue to rise in most healthcare systems, magnifying demand for reliable anti-infective regimens.[1]Agency for Healthcare Research & Quality, “Costs of Sepsis Hospitalizations,” ahrq.gov Older adults and immunocompromised patients now present more frequently with severe infections that require prompt, broad-spectrum cover, lengthening inpatient admissions and driving average lengths of stay above pre-pandemic levels. Heightened disease prevalence has stimulated investment in AI-enabled rapid-diagnostic platforms that can shave hours off identification times, thus enabling earlier and more targeted therapy. Global policymakers channel resources toward community-based infection programs that serve disadvantaged groups, helping shape decentralized treatment models in the anti-infective drugs market. The net effect is an enduring demand baseline that offsets price erosion in traditional molecules and anchors volume growth even in mature economies.

Growing Resistance Among Pathogens

Hyper-resistant strains of Klebsiella pneumoniae and Acinetobacter baumannii now circulate across hospitals worldwide, lifting carbapenem resistance to 31.3% in Asia-Pacific and prompting urgent shifts toward β-lactam/β-lactamase inhibitor combinations.[2]World Health Organization, “GLASS Surveillance Data 2025,” who.int Pharmaceutical pipelines increasingly prioritize mechanisms that impede resistance emergence, such as dual-binding site antibiotics that raise mutation barriers by several orders of magnitude. Economic implications are material: resistant infections lengthen hospital stays and require costlier diagnostics, diluting payer budgets and forcing value-based price negotiations. Geographic variation is pronounced; South Asia leads global resistance curves, whereas nitrofurantoin remains broadly effective against urinary isolates in North America and Western Europe. Heightened surveillance and incentives for novel mode-of-action molecules create fresh revenue headroom for innovators within the anti-infective drugs market.

Robust R&D Investment & Public-Private Collaborations

Landmark alliances such as Pfizer–Evotec and the Boehringer Ingelheim-Evotec-bioMérieux Aurobac joint venture underscore growing appetite for co-development models that defray cost and share early-stage risk. U.S. agencies expand grant funding for sepsis detection technologies, cementing North America’s position as an epicenter of early-stage antimicrobial innovation. AI-powered discovery partnerships, typified by Eli Lilly–OpenAI, have begun generating candidate lists in months rather than years, potentially compressing traditional discovery timelines. Collectively, these collaborative frameworks inject sustained momentum into the anti-infective drugs market even as resistance raises development complexity.

Advanced Drug Development Technologies

Next-generation inhalable formulations enable direct pulmonary delivery of tuberculosis and RSV therapeutics, achieving fine-particle fractions approaching 70% and improving macrophage targeting. Triple-agent dry-powder combinations have produced sub-microgram minimum inhibitory concentrations in vitro, reducing systemic exposure and enhancing adherence for chronic pulmonary infections. Nanocarrier platforms now facilitate targeted hepatic, CNS, and ocular penetration, overcoming legacy bioavailability constraints. Machine-learning models drive sepsis triage algorithms that increase diagnostic accuracy, while genomic profiling guides personalized anti-infective regimens based on host immune response variability.[3]MDPI, “AI-Assisted Diagnostics in Infectious Diseases,” mdpi.com These technological advances collectively tilt the anti-infective drugs market toward high-value, precision-medicine niches with stronger pricing power.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating antimicrobial resistance (AMR) | –0.5% | Global, acute in hospital settings & LMICs | Long term (≥ 4 years) |

| Strict regulatory environment & safety concerns | –0.3% | North America & EU; expanding worldwide | Medium term (2-4 years) |

| Global supply-chain disruptions | –0.2% | Global, highest in API-dependent geographies | Short term (≤ 2 years) |

| Falsified or substandard medicines | –0.1% | LMICs primarily; spill-over into regulated markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Antimicrobial Resistance (AMR)

Bedaquiline resistance has already reached 5.7% globally, peaking at 10.4% in South Africa, compressing therapeutic windows for multidrug-resistant tuberculosis. Hospitals report rising vancomycin-resistant Enterococcus and carbapenem-resistant Acinetobacter rates, complicating empiric therapy and elevating mortality. Pharmaceutical firms confront diminishing returns as resistance shortens product life, deterring investment in traditional broad-spectrum classes that once delivered decades of revenue. Payers respond by limiting premium pricing to drugs with demonstrable resistance-suppression properties, constraining top-line prospects for molecules lacking novel mechanisms. The compounding clinical and economic toll moderates the longer-term momentum of the anti-infective drugs market.

Strict Regulatory Environment & Safety Concerns

The FDA’s 2025 guidance requires developers to submit resistance emergence modeling and post-market stewardship commitments, expanding dossier size and cost. European regulators now demand pan-EU real-world evidence panels that capture resistance-trend data for new launches, adding at least 12 months to commercialization timelines. Safety monitoring intensifies for agents with QT-prolongation or mitochondrial toxicity risks; bedaquiline’s cardiac surveillance obligations exemplify regulatory vigilance. Smaller biotechs, which drive much anti-infective innovation, struggle to fund these requirements, often exiting programs or sublicensing candidates, thinning the drug pipeline. Delays erode the competitive edge of novel molecules against rapidly evolving pathogens, crimping the anti-infective drugs market growth potential.

Segment Analysis

By Drug Class: Antivirals Accelerate Within a Dominant Antibiotics Landscape

Antibiotics delivered a 43.08% market share of the anti-infective drugs market share, as clinical reliance on β-lactams, macrolides, and carbapenems remained heavy in hospital protocols. Persistent resistance and stewardship initiatives, however, have capped volume growth, channeling R&D investment toward next-generation combinations such as aztreonam-avibactam, which gained FDA clearance in February 2025. Antivirals posted the most robust 4.73% CAGR outlook as HIV, RSV, and hepatitis formulations shift to long-acting injectables and antibody cocktails that promise quarterly or semi-annual dosing convenience. That innovation pipeline repositioned the segment as a strategic growth engine inside the anti-infective drugs market.

Breakthrough respiratory antivirals also benefit from pandemic preparedness budgets that bankroll surge capacity and stockpiling. Competitive intensity deepens as brand-name incumbents defend share against biosimilars in mature classes while venture-backed biotech entrants introduce narrow-spectrum bacteriophages. Price-volume dynamics therefore diverge: antibiotics witness modest price erosion offset by large installed volume, whereas antivirals command premium pricing but face smaller treated-patient bases. The interplay sustains overall revenue growth and shapes long-term R&D capital allocation.

Note: Segment shares of all individual segments available upon report purchase

By Indication: Respiratory Virus Infections Outpace a Stable HIV Franchise

HIV therapy retained 27.33% of the anti-infective drugs market size in 2024 thanks to widespread adoption of integrase inhibitor backbones and growing uptake of pre-exposure prophylaxis (PrEP). Lenacapavir’s potential annual production cost of USD 40 invites broader LMIC access, underpinning volume stability even as mature Western markets plateau. In contrast, respiratory virus infections are projected to log a 4.51% CAGR as RSV prophylaxis gains momentum following data showing a 78% reduction in infant hospitalizations with nirsevimab.

Tuberculosis remains a major clinical focus, with shorter six-month BPaL/M regimens projected to treat 126,792 patients globally by 2026, shrinking total therapy days and reducing health-system cost burdens. Sepsis protocols that prioritize broad-spectrum coverage within the first hour have driven a 4.9-fold survival benefit, intensifying demand for ready-to-reconstitute injectables in emergency settings. These varied indication trajectories collectively reinforce the anti-infective drugs market diversification, lessening dependence on any single pathogen area.

By Route of Administration: Inhalation Platforms Gain Momentum

Parenteral delivery commanded 52.16% of 2024 revenue as IV formulations remain indispensable for severe systemic infections requiring immediate pharmacodynamic exposure. However, inhalation therapies are projected to expand at 5.22% CAGR, propelled by advanced particle-engineering that achieves deep-lung deposition and mitigates systemic toxicity in tuberculosis and viral pneumonia. Oral regimens still dominate outpatient treatment; fosfomycin, for instance, retains 96% sensitivity against E. coli urinary isolates and can be dispensed via community pharmacies.

Alternative routes such as topical ophthalmic gels and intrathecal preparations cater to niche central-nervous-system infections. Marketplayers strategically broaden device portfolios nebulizers, dry-powder inhalers, smart inhalers to secure lifecycle extensions for off-patent molecules via innovative delivery. The route of administration spectrum thereby acts as an incremental revenue lever for manufacturers striving to differentiate within the anti-infective drugs market.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Digital Dispensing Reshapes Access

Hospital pharmacies held 59.24% of distribution in 2024 owing to the high acuity of in-hospital infections and the technical requirements of IV drug preparation. Simultaneously, online pharmacies are on track for a 6.77% CAGR as telemedicine adoption soars and direct-to-patient logistics mature in North America and parts of Asia. U.S. drug distribution remains highly consolidated McKesson, Cencora, and Cardinal Health together control more than 90% of throughput limiting bargaining power for smaller manufacturers.

Digital platforms integrate e-prescribing modules, real-time inventory feeds, and automated cold-chain validation, enhancing supply resilience. Mail-order fulfillment models improve adherence for chronic HIV patients, while click-and-collect programs support same-day antibiotic access in urban centers. Regulatory frameworks are adjusting: the FDA now allows remote verification for certain prescription renewals, smoothing repeat antiviral dispensing. This omnichannel evolution adds flexibility and widens the treated-patient footprint of the anti-infective drugs market.

Geography Analysis

North America controlled 33.74% of 2024 revenue through an entrenched innovation ecosystem, dynamic payer mix, and early adoption of novel agents. The FDA’s streamlined unmet-need guidance reduces scientific advice cycles, yet heightened post-market study obligations inflate compliance costs that manufacturers must factor into pricing models. U.S. sepsis admissions number 2.5 million annually with aggregate costs of USD 52.1 billion, anchoring steady utilization of broad-spectrum injectables and driving formulary turnover. Canada and Mexico augment the regional footprint by contributing specialized fill-finish capacity that feeds northbound and southbound trade flows, though divergent pharmaceutical price controls remain a commercial consideration.

Europe exhibits a unified strategic stance against AMR. Revised EU pharmaceutical legislation harmonizes resistance-monitoring requirements, enabling companies to file a single surveillance plan for all member states. Public-private alliances exemplified by the GSK-UK AMR program demonstrate how shared-risk funding accelerates late-stage antibiotic candidates. However, austerity in Southern Europe constrains reimbursement for premium-priced agents, forcing differential pricing strategies that weigh on pan-European average selling prices. Brexit introduces regulatory bifurcation, with companies navigating dual approval channels to achieve full market reach.

Asia-Pacific is projected to grow at 3.77% CAGR to 2030, making it the fastest-expanding component of the anti-infective drugs market. China dominates global antibiotic active-ingredient output and hosts 20 antibacterial projects across 17 local firms that align with national AMR priorities. India leverages cost-competitive chemistry capabilities but grapples with environmental discharge controls that could raise long-term manufacturing overhead. Japan’s expedited approval pathway for high-priority antimicrobials shortens time-to-market by up to 12 months, while Australia funds market-entry rewards for innovative antibiotics to safeguard local supply. Yet, elevated carbapenem resistance 31.3% regional prevalence amplifies clinical urgency and shapes procurement preferences toward agents with robust resistance-suppression data.

Competitive Landscape

The anti-infective drugs market demonstrates moderate consolidation as top developers pursue scale to weather approaching patent cliffs. Strategic rationale focuses on replenishing late-stage pipelines and leveraging established commercialization networks to extract value from newly acquired assets. Merck’s publicly signaled appetite for bolt-on deals addresses looming Keytruda exclusivity loss, a template echoed by several peers.

Emerging disruptors occupy white-space niches: Eli Lilly and OpenAI exploit transformer models to elucidate antimicrobial peptide sequences, claiming a ten-fold acceleration in hit identification. Aurobac Therapeutics blends diagnostics and therapeutics to offer integrated AMR solutions that may command premium health-economic valuations. Delivery-platform specialists target inhaled and long-acting injectable formats that can extend exclusivity timelines for legacy molecules.

Competitive differentiation increasingly hinges on post-approval stewardship and supply-security commitments, areas scrutinized by institutional investors wary of drug-shortage and resistance-liability risks. Companies able to guarantee continuity of supply while demonstrating measurable resistance-mitigation outcomes secure preferential listing on value-based procurement frameworks, reinforcing a virtuous market position.

Anti Infective Drugs Industry Leaders

-

Merck & Co., Inc

-

Novartis AG

-

Gilead Sciences Inc.

-

Pfizer Inc.

-

GlaxoSmithKline plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Wockhardt is progressing toward the Indian market launch of Zaynich, its novel antibiotic aimed at treating multidrug-resistant gram-negative infections. Following the successful global Phase III trials and submission of India-specific data to the DCGI, the company anticipates regulatory approval within nine to ten months, setting the stage for a robust US launch in mid-2026.

- June 2025: Fortrea entered a strategic collaboration with Emery Pharma to perform rapid lot-by-lot impurity testing of rifampin used in drug-drug interaction (DDI) studies. By ensuring compliance with FDA’s Acceptable Intake limits for 1-methyl-4-nitrosopiperazine (MNP), Fortrea reinforces its commitment to drug safety and precision. This partnership strengthens Fortrea's clinical capabilities and supports its leadership in global pharmaceutical research.

- March 2025: Avenacy announced the launch of a comprehensive suite of critical injectable antibiotics, reinforcing its commitment to supply continuity in acute-care settings.This development underscores Avenacy's role in addressing urgent therapeutic needs with high-quality sterile products.

- February 2025: AbbVie secured FDA approval for EMBLAVEO (aztreonam and avibactam), the first fixed-dose monobactam/β-lactamase inhibitor combination. Used alongside metronidazole, it provides a powerful treatment option for complicated intra-abdominal infections (cIAI), especially in cases involving highly resistant Gram-negative pathogens. The approval is a milestone in AbbVie’s anti-infective pipeline targeting antimicrobial resistance.

Global Anti Infective Drugs Market Report Scope

As per the scope of the report, anti-infective drugs/agents are described as substances that prevent infectious agents or organisms from spreading. These are mostly communicable diseases spread by viruses, bacteria, fungi, and other organisms. The Anti-infective Drugs Market is Segmented by Product Type (Antibiotics, Antivirals, Antifungals, and Other Products), Indication (HIV Infection, Pneumonia, Respiratory Virus Infection, Sepsis, Tuberculosis, and Other Indications), Distribution Channel (Hospital Pharmacy, Retail Pharmacy, and Other Distribution Channels), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends of 17 countries across major regions globally. The report offers the value in USD million for the above segments.

| Antibiotics | β-lactam & β-lactamase inhibitors |

| Macrolides | |

| Tetracyclines | |

| Fluoroquinolones | |

| Cephalosporins | |

| Carbapenems | |

| Others | |

| Antivirals | NRTIs |

| NNRTIs | |

| Protease inhibitors | |

| Integrase inhibitors | |

| Polymerase inhibitors | |

| Others | |

| Antifungals | Azoles |

| Echinocandins | |

| Polyenes | |

| Allylamines | |

| Others | |

| Antiparasitics | Antimalarials |

| Anthelmintics | |

| Antiprotozoals | |

| Others |

| HIV Infection |

| Pneumonia |

| Respiratory Virus Infection |

| Sepsis |

| Tuberculosis |

| Urinary Tract Infection |

| Skin & Soft-Tissue Infections |

| Other Indications |

| Oral |

| Parenteral |

| Topical |

| Inhalation |

| Others |

| Hospital Pharmacy |

| Retail Pharmacy |

| Online Pharmacy |

| Mail-order Pharmacy |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Antibiotics | β-lactam & β-lactamase inhibitors |

| Macrolides | ||

| Tetracyclines | ||

| Fluoroquinolones | ||

| Cephalosporins | ||

| Carbapenems | ||

| Others | ||

| Antivirals | NRTIs | |

| NNRTIs | ||

| Protease inhibitors | ||

| Integrase inhibitors | ||

| Polymerase inhibitors | ||

| Others | ||

| Antifungals | Azoles | |

| Echinocandins | ||

| Polyenes | ||

| Allylamines | ||

| Others | ||

| Antiparasitics | Antimalarials | |

| Anthelmintics | ||

| Antiprotozoals | ||

| Others | ||

| By Indication | HIV Infection | |

| Pneumonia | ||

| Respiratory Virus Infection | ||

| Sepsis | ||

| Tuberculosis | ||

| Urinary Tract Infection | ||

| Skin & Soft-Tissue Infections | ||

| Other Indications | ||

| By Route of Administration | Oral | |

| Parenteral | ||

| Topical | ||

| Inhalation | ||

| Others | ||

| By Distribution Channel | Hospital Pharmacy | |

| Retail Pharmacy | ||

| Online Pharmacy | ||

| Mail-order Pharmacy | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the anti-infective drugs market?

The anti-infective drugs market size is USD 138.57 billion in 2025, with a forecast of USD 159.43 billion by 2030 at a 2.84% CAGR.

Which drug class is growing fastest?

Antivirals post the highest 4.73% CAGR, propelled by long-acting HIV agents and breakthrough RSV therapies.

Why is Asia-Pacific the fastest-growing regional market?

Asia-Pacific combines huge infectious-disease burden, expanding healthcare investment, and dominant antibiotic manufacturing capacity, translating to a 3.77% CAGR.

How are inhalation delivery systems shaping the market?

Advanced inhalable powders and microparticles enable targeted lung deposition, driving a 5.22% CAGR for inhalation routes and expanding treatment options for pulmonary infections.

What role do online pharmacies play in market growth?

Online pharmacies link telehealth prescribing with direct shipment, accelerating anti-infective access and registering a 6.77% CAGR through 2030.

How is antimicrobial resistance affecting new-drug development?

Escalating resistance shortens product lifecycles, raises regulatory evidence demands, and incentivizes investment in novel mechanisms and stewardship initiatives on which future growth depends.

Page last updated on: