| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 2.55 Billion |

| Market Size (2030) | USD 7.92 Billion |

| CAGR (2025 - 2030) | 25.46 % |

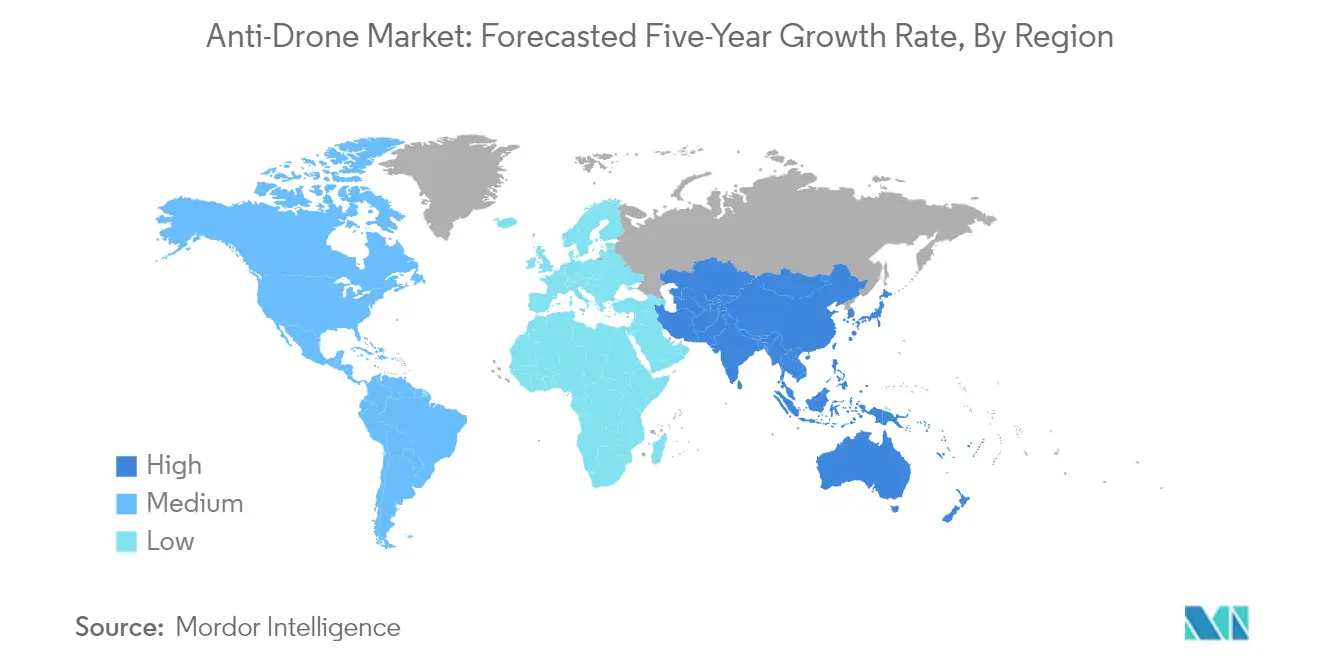

| Fastest Growing Market | Latin America |

| Largest Market | North America |

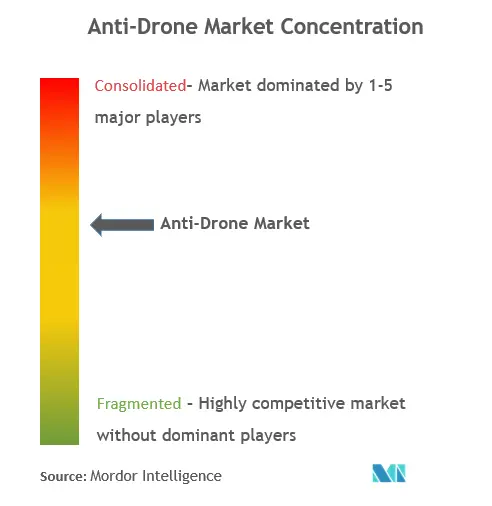

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Anti Drone Market Analysis

The Anti-Drone Market size is estimated at USD 2.55 billion in 2025, and is expected to reach USD 7.92 billion by 2030, at a CAGR of 25.46% during the forecast period (2025-2030).

The anti-drone industry is experiencing rapid technological evolution driven by the increasing sophistication of drone threats and the need for more comprehensive defense solutions. The integration of artificial intelligence, machine learning, and cloud computing is revolutionizing anti-drone technology, enabling more accurate threat detection and faster response times. Multi-sensor fusion technology is becoming increasingly prevalent, combining radar, radio frequency, optical, and acoustic sensors to provide more reliable drone detection and identification of potential threats. The industry's focus on technological advancement is reflected in recent developments, such as the November 2022 integration of Axis Communications' cameras into Dedrone's counter-UAV command and control platform, marking a significant step forward in multi-sensor visual detection capabilities.

The market is witnessing a significant shift toward multi-layered defense approaches, particularly in protecting critical infrastructure and sensitive facilities. Airport security has become a primary focus, with major facilities worldwide implementing sophisticated drone detection systems. The industry has moved beyond simple detection and jamming solutions to incorporate more comprehensive protection strategies, including artificial intelligence-based RF detection systems and sophisticated long-range cameras for additional verification. These advanced systems are capable of detecting multiple drones and devices at various frequencies simultaneously, while ensuring no interference with existing airport communications systems.

The emergence of mobile and adaptable anti-drone solutions represents a notable trend in the industry, with manufacturers developing systems that can be deployed across various platforms and scenarios. Companies are exploring new opportunities in mobile and aerial anti-drone technologies to support the growing demand for territorial security against unwanted aerial systems. The industry is witnessing increased innovation in size, weight, and power (SWaP) parameters, leading to the development of more compact and efficient systems. This evolution in system design is enabling greater mobility options and customization flexibility, while potentially reducing manufacturing costs and timeframes.

Strategic partnerships and collaborations are becoming increasingly prevalent in the anti-drone market as companies seek to combine complementary technologies and expertise. The industry is seeing a rise in joint ventures and technology-sharing agreements aimed at developing more effective counter-drone solutions. These collaborations are particularly focused on creating systems capable of operating in complex, variable, and communications-limited environments. The trend toward partnerships is exemplified by recent developments in integrating various detection and neutralization technologies, including radar systems, electronic warfare capabilities, and advanced optical sensors, to create more comprehensive and effective counter-drone solutions.

Anti Drone Market Trends

Incidences of Security Breaches by Unidentified Drones

The proliferation of unmanned aerial systems has led to an alarming increase in drone security breaches and potential threats across various sectors. Commercial venues have proven particularly vulnerable to small UAS, which can discreetly circumvent traditional security measures and cause significant damage in both intentional and negligent scenarios. For instance, the Allegiant Stadium in Las Vegas suffered structural damage after a drone crashed into panels approximately 100 feet above the ground, highlighting the growing concern of unregistered drones being operated in restricted airspaces. The threat extends beyond infrastructure damage, as reports from border communities like Coral Gates in San Ysidro, California, have documented increasing drone flights from across the Mexican border, allegedly carrying contraband and drugs.

The military and critical infrastructure sectors face even more severe challenges from hostile drone activities. Terrorist groups have demonstrated their capability to modify commercial and recreational UAS for planning, preparing, and executing attacks on the battlefield. Recent incidents include bomb-laden drones being used in Iraq, Ukraine, and Syria, showcasing how small drones can be weaponized to bypass existing terrestrial defenses. According to recent FAA UAS sightings reports, there were over 2,500 sightings of UAS from pilots, citizens, and law enforcement in the United States in 2021, emphasizing the growing scale of unauthorized drone surveillance operations. These incidents have necessitated the development and deployment of sophisticated drone defense technologies to protect sensitive installations and public spaces.

Understand The Key Trends Shaping This Market

Download PDF

Adoption and Development of Anti-Drone Systems by Major Defense Spending Countries

The escalating global security environment has prompted major defense-spending nations to significantly increase their investments in anti-drone technologies. According to SIPRI, the global defense expenditure reached USD 2.4 trillion in 2022, with the United States leading at USD 877 billion, demonstrating the massive financial commitment towards enhancing defensive capabilities. The US Department of Defense has allocated substantial resources specifically for drone threat detection technologies, planning to spend approximately USD 668 million on research into new drone defense technologies and about USD 78 million for procurement of such technology in the coming year. This commitment is reflected in practical implementations, such as the US Army's creation of a guided air and missile-defense modernization program focusing on countering drone threats.

The adoption of counter-drone systems has gained significant momentum across other major military powers as well. India's armed forces, for instance, placed orders worth USD 1.5 billion for counter-drone technologies with domestic firms in August 2021, demonstrating the push towards indigenous development of these critical systems. The Ukrainian military's deployment of thousands of advanced Lithuanian counter-unmanned aircraft systems (C-UASs) in their conflict with Russia highlights the practical application and growing importance of these systems in modern warfare. Additionally, strategic partnerships and technological collaborations are emerging as key drivers, exemplified by General Dynamics Land Systems' launch of the TRX SHORAD in October 2023, an unmanned vehicle specifically designed as an anti-drone solution featuring advanced capabilities including a 30mm automatic cannon and Stinger surface-to-air missile launchers.

Segment Analysis: Application

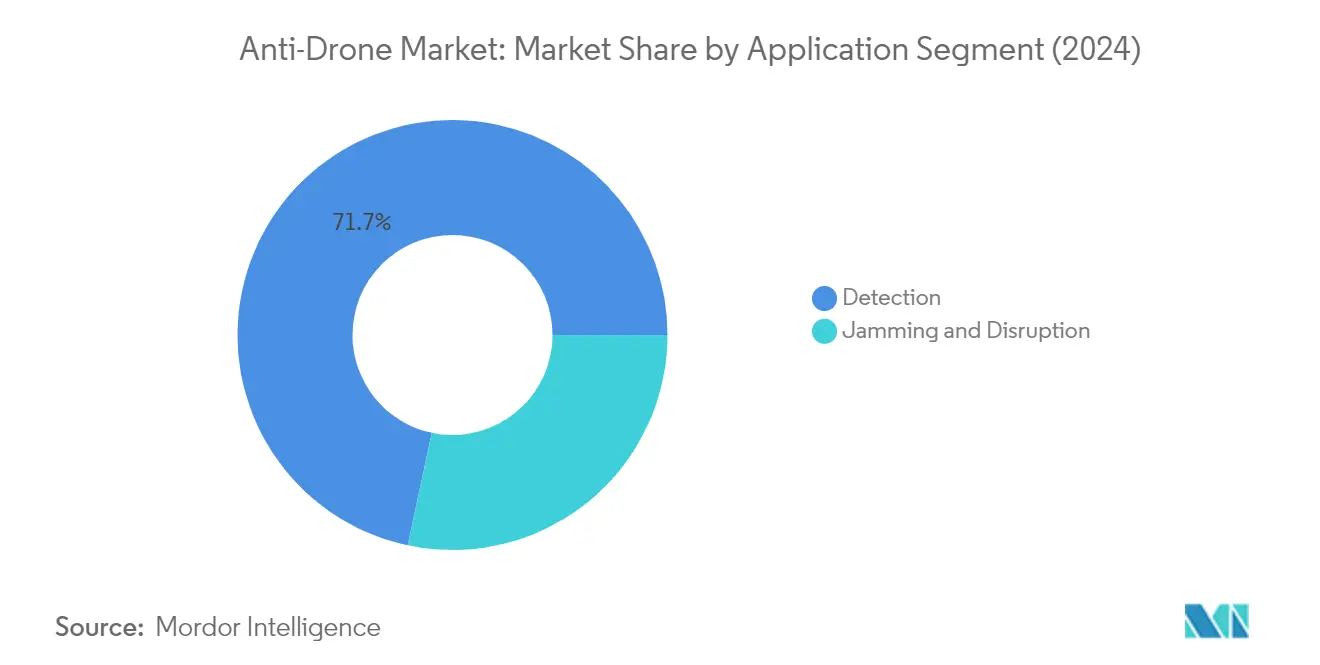

Detection Segment in Anti-Drone Market

The drone detection segment has established itself as the dominant force in the global anti-drone market, commanding approximately 72% of the market share in 2024. This segment's prominence is driven by the increasing adoption of sophisticated drone radar system technologies, including radar systems, RF sensors, acoustic sensors, and optical systems. The segment's growth is particularly notable in airport security applications, where high-precision drone detection capabilities are crucial for identifying and tracking unauthorized drone activities. Modern detection systems are incorporating artificial intelligence and machine learning algorithms to improve accuracy and reduce false positives, while also expanding their capability to detect smaller and more agile drones. The integration of multiple detection technologies into unified systems has become a key trend, allowing for more reliable threat identification across various environmental conditions. The segment is expected to maintain its market leadership position through 2029, with an estimated growth rate of around 30% during the forecast period 2024-2029, driven by continuous technological advancements and increasing investment in drone detection infrastructure by both government and private sectors.

Jamming and Disruption Segment in Anti-Drone Market

The drone jamming and disruption segment represents a critical component of the anti-drone market, focusing on neutralizing identified drone threats through various countermeasure technologies. This segment encompasses a range of solutions, including RF jammers, GPS spoofers, directed energy weapons, and physical interception systems. The technology has evolved to include more sophisticated and precise drone jamming capabilities that can target specific frequencies while minimizing interference with legitimate communications. Modern jamming systems are being designed with increased mobility and reduced form factors, making them suitable for both fixed installations and mobile applications. The segment is witnessing increased adoption in military and critical infrastructure protection, where the ability to safely neutralize drone threats is paramount. Manufacturers are focusing on developing systems that can effectively counter multiple drones simultaneously, addressing the growing threat of drone swarms. The integration of smart jamming technologies with automated threat assessment systems is emerging as a key trend in this segment.

Segment Analysis: Vertical

Defense Segment in Anti-Drone Market

The defense segment continues to dominate the global anti-drone market, accounting for approximately 46% of the market share in 2024. This significant market position is driven by increasing investments from major defense-spending countries toward the development and deployment of counter-drone technologies. The defense sector's dominance is particularly evident in countries like the United States, China, and India, where substantial budgets are allocated for counter-drone capabilities. Military organizations worldwide are increasingly focusing on protecting their bases, personnel, and critical assets from potential drone-based threats, leading to widespread adoption of anti-drone systems. The segment's strong performance is further bolstered by ongoing technological advancements in detection, tracking, and drone neutralization capabilities specifically designed for military applications.

Airports Segment in Anti-Drone Market

The airports segment is experiencing rapid growth in the anti-drone market, driven by increasing incidents of drone-related disruptions at airports worldwide. The segment's growth is fueled by stringent aviation safety regulations and the critical need to protect airport operations from unauthorized drone activities. Airports are increasingly investing in sophisticated drone detection and countermeasure systems to prevent potential collisions with aircraft and maintain uninterrupted flight operations. The integration of advanced technologies like AI-powered detection systems, radio frequency analyzers, and automated response mechanisms is becoming standard practice at major international airports. This trend is particularly evident in regions with high air traffic density, where the risk of drone-related incidents is more pronounced.

Remaining Segments in Vertical Segmentation

The other critical infrastructures segment plays a vital role in the anti-drone market, encompassing protection for nuclear facilities, power plants, government buildings, and other sensitive installations. This segment is characterized by the deployment of customized anti-drone solutions that meet the specific security requirements of different infrastructure types. The segment's growth is driven by increasing awareness of drone-based threats to critical infrastructure and the need for comprehensive security solutions. The adoption of integrated security systems that combine multiple detection and countermeasure technologies is becoming increasingly common in this segment, reflecting the complex nature of protecting diverse types of critical infrastructure from aerial threats.

Anti-Drone Market Geography Segment Analysis

Anti-Drone Market in North America

North America represents a crucial market for anti-drone technologies, driven by significant defense spending and increasing security concerns around critical infrastructure. The United States and Canada are the key markets in this region, with both countries actively investing in counter-drone capabilities for military and civilian applications. The region's growth is supported by the presence of major defense contractors, advanced technological infrastructure, and strong government initiatives to counter unauthorized drone activities near sensitive locations like airports, government buildings, and military installations.

Anti-Drone Market in United States

The United States dominates the North American anti-drone market, holding approximately 79% market share in 2024. The country's leadership position is reinforced by substantial military spending and advanced research programs in counter-drone technologies. The US Department of Defense maintains a dedicated Joint Counter-small UAS Office (JCO) to streamline counter-drone initiatives across military branches. The country's robust defense industrial base, including major contractors and innovative startups, continues to develop sophisticated anti-drone solutions incorporating artificial intelligence, machine learning, and advanced sensor technologies. The integration of counter-drone systems across military, law enforcement, and critical infrastructure protection demonstrates the market's maturity and widespread adoption.

Anti-Drone Market Growth Dynamics in United States

The United States is also leading the growth trajectory in North America, with a projected CAGR of approximately 29% during 2024-2029. This growth is driven by continuous technological innovations and increasing investment in counter-drone capabilities. The US military's focus on developing comprehensive counter-drone solutions for various threat scenarios, including drone swarms, has spurred research and development activities. The country's emphasis on protecting critical infrastructure, securing major events, and enhancing border surveillance continues to create new opportunities for anti-drone system deployments. The integration of advanced technologies like directed energy weapons and AI-powered detection systems further strengthens the market's growth potential.

Anti-Drone Market in Europe

Europe represents a significant market for anti-drone technologies, characterized by diverse requirements across different countries and strong regional cooperation in defense initiatives. The United Kingdom, France, and Germany are the primary markets, each contributing significantly to the region's growth. The European market is distinguished by its focus on developing integrated solutions that can protect both military installations and civilian infrastructure, particularly airports and critical facilities. The region's approach to counter-drone technology emphasizes the balance between security requirements and regulatory compliance.

Anti-Drone Market in United Kingdom

The United Kingdom leads the European anti-drone market, commanding approximately 31% of the regional market share in 2024. The country's strong position is supported by its comprehensive approach to counter-drone security, particularly following high-profile drone incidents at major airports. The UK's defense strategy emphasizes the development and deployment of advanced counter-drone systems across military and civilian applications. The nation's robust research and development ecosystem, combined with strategic partnerships between government agencies and private sector companies, continues to drive innovation in anti-drone technologies.

Anti-Drone Market Growth Dynamics in France

France demonstrates the highest growth potential in the European market, with an expected CAGR of approximately 30% from 2024-2029. The country's dynamic growth is driven by its ambitious plans to enhance counter-drone capabilities, particularly in preparation for major international events. France's focus on developing advanced technologies, including laser-based counter-drone systems and AI-powered detection capabilities, positions it at the forefront of innovation. The French military's investment in next-generation counter-drone solutions and the country's strong aerospace industry continue to fuel market expansion.

Anti-Drone Market in Asia-Pacific

The Asia-Pacific region represents a rapidly evolving market for anti-drone technologies, characterized by diverse security challenges and increasing defense modernization initiatives. Countries including China, India, Japan, and South Korea are making significant investments in counter-drone capabilities. The region's market is driven by rising security concerns, border protection needs, and the increasing adoption of drones for both commercial and military applications. The diversity of requirements across different countries has led to the development of varied counter-drone solutions suited to specific regional needs.

Anti-Drone Market in China

China leads the Asia-Pacific anti-drone market, demonstrating strong capabilities in developing indigenous counter-drone technologies. The country's leadership is supported by substantial investments in research and development, particularly in radar detection systems and artificial intelligence-based solutions. China's approach to counter-drone technology emphasizes self-reliance and technological innovation, with a focus on developing comprehensive systems that can address various threat scenarios. The nation's defense industry continues to advance its capabilities in areas such as radar technology, electronic warfare, and integrated air defense systems.

Anti-Drone Market Growth Dynamics in India

India emerges as the fastest-growing market in the Asia-Pacific region, driven by increasing security concerns and substantial investments in defense modernization. The country's rapid market expansion is supported by growing domestic manufacturing capabilities and strategic partnerships with international technology providers. India's focus on developing indigenous anti-drone solutions, combined with its efforts to protect critical infrastructure and military installations, creates a robust growth environment. The nation's emphasis on self-reliance in defense technology and the increasing adoption of counter-drone systems across various security agencies continue to drive market development.

Anti-Drone Market in Latin America

The Latin American anti-drone market is experiencing significant transformation, with Mexico and Brazil emerging as key players in the region. The market is characterized by increasing awareness of drone-related security threats and growing investments in border security infrastructure. Brazil leads the regional market in terms of both size and growth rate, driven by its comprehensive approach to airspace security and protection of critical infrastructure. Mexico's market is supported by its focus on border security applications and protection of sensitive installations. The region's growth is further supported by increasing cooperation between countries in addressing common security challenges and sharing technological expertise in counter-drone capabilities.

Anti-Drone Market in Middle East & Africa

The Middle East & Africa region demonstrates strong potential in the anti-drone market, with Saudi Arabia and the United Arab Emirates leading regional developments. The market is characterized by significant investments in protecting critical infrastructure, particularly oil and gas facilities, and military installations. Saudi Arabia emerges as both the largest and fastest-growing market in the region, driven by its comprehensive approach to airspace security and substantial defense modernization programs. The UAE's market is distinguished by its focus on developing advanced counter-drone technologies through international partnerships and domestic capability building. The region's unique security challenges and substantial defense budgets continue to drive innovation in counter-drone technologies.

Get Analysis on Important Geographic Markets

Download PDF

Anti Drone Industry Overview

Top Companies in Anti-Drone Market

The anti-drone market features prominent anti-drone companies like Raytheon Technologies, Lockheed Martin, IAI, QinetiQ Group, Thales Group, and SAAB AB leading the industry through continuous innovation and strategic developments. Companies are focusing on developing sophisticated detection sensors, anti-drone systems, and directed energy weapons while incorporating artificial intelligence and cloud computing capabilities to enhance system effectiveness. The industry witnesses extensive collaboration between defense contractors and technology firms to create comprehensive anti-drone solutions that can detect, identify, track, and neutralize various types of unmanned aerial threats. Market leaders are investing heavily in research and development to address emerging challenges like drone swarms and miniaturized UAVs, while also expanding their global footprint through strategic partnerships and local presence in key defense markets. The competitive landscape is characterized by significant investments in developing modular, scalable solutions that can be customized for different applications ranging from military installations to critical infrastructure protection.

Fragmented Market with Strong Defense Focus

The anti-drone market exhibits a fragmented structure with a mix of large defense conglomerates and specialized technology providers competing for market share. Major defense contractors leverage their established relationships with military customers and extensive research capabilities to maintain their market positions, while numerous start-ups and local players bring innovative solutions targeting specific market segments. The industry is witnessing increasing consolidation through strategic acquisitions and partnerships, as larger counter-drone companies seek to acquire innovative technologies and expand their product portfolios.

The market demonstrates a strong regional dimension, with companies establishing local manufacturing and development capabilities to better serve domestic defense requirements and comply with country-specific regulations. Major players are pursuing vertical integration strategies to control key technologies and maintain competitive advantages, while also forming strategic alliances with local partners to penetrate new markets. The industry's competitive dynamics are shaped by the need to offer comprehensive solutions that combine multiple technologies and capabilities, leading to increased collaboration between traditional defense contractors and technology specialists.

Innovation and Integration Drive Market Success

Success in the anti-drone market increasingly depends on companies' ability to develop integrated solutions that can address evolving threat scenarios while maintaining cost-effectiveness. Incumbent players must focus on continuous innovation in detection and neutralization technologies, while also building flexible architectures that can accommodate future technological advances and changing customer requirements. The ability to offer customizable solutions that can be rapidly deployed and integrated with existing security infrastructure has become a critical differentiator in the market.

Market contenders can gain ground by focusing on specialized capabilities and niche applications, particularly in emerging areas like autonomous operation and artificial intelligence-driven threat assessment. Companies must navigate complex regulatory environments while maintaining strong relationships with defense and security agencies, as government approvals and certifications remain crucial for market success. The industry's future will be shaped by the ability to address concerns about collateral damage and interference with legitimate drone operations, while also maintaining effectiveness against evolving threats. Success will increasingly depend on developing solutions that can operate in complex urban environments and handle multiple simultaneous threats while minimizing disruption to legitimate activities. Companies are also exploring the integration of counter-UAS companies technologies to enhance their offerings in the anti-drone defense system sector.

Anti Drone Market Leaders

-

Lockheed Martin Corporation

-

RTX Corporation

-

THALES

-

Israel Aerospace Industries Ltd.

-

QinetiQ Group plc

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Anti Drone Market News

- August 2023: DroneShield Ltd. introduced satellite denial systems for specific target areas. Various Global Navigation Satellite Systems (GNSS) are used worldwide, including the well-known US GPS, the Chinese BeiDou, the Russian GLONASS, and the European Galileo system. DroneShield’s GNSS disruption solutions for drones and UAVs incorporate intelligent defeat capabilities.

- July 2023: The Swedish Defence Materiel Administration (FMV) and Thales agreed to deliver and install SMART-L Multi-Mission Fixed (MM/F) long-range radars. These radars, featuring the latest Active Electronically Scanned Array (AESA) technology, are designed to offer versatile capabilities for air and surface surveillance and target designation.

Anti Drone Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions And Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

-

4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Application

- 5.1.1 Detection

- 5.1.1.1 RADARs

- 5.1.1.2 Other Sensors

- 5.1.2 Jamming and Disruption

-

5.2 Vertical

- 5.2.1 Defense

- 5.2.2 Airports

- 5.2.3 Other Critical Infrastructures

-

5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 France

- 5.3.2.3 Germany

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Mexico

- 5.3.4.2 Brazil

- 5.3.4.3 Rest of Latin America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

-

6.2 Company Profiles

- 6.2.1 Drone Defence

- 6.2.2 DeTect Inc.

- 6.2.3 Zen Technologies Limited

- 6.2.4 DroneShield Ltd

- 6.2.5 METIS Aerospace Ltd

- 6.2.6 QinetiQ Group plc

- 6.2.7 THALES

- 6.2.8 Lockheed Martin Corporation

- 6.2.9 SRC Inc.

- 6.2.10 Dedrone

- 6.2.11 SAAB AB

- 6.2.12 RTX Corporation

- 6.2.13 Israel Aerospace Industries Ltd.

- 6.2.14 Citadel Defense

- 6.2.15 Robin Radar Systems

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Anti Drone Industry Segmentation

An anti-drone system is a customizable integrated system that includes different equipment and solutions depending on the customer's needs and requirements. It prevents security breaches at private houses, prisons, commercial venues, government buildings, industrial installations, airports, border security, critical infrastructure, and military facilities.

The anti-drone market is segmented by application, vertical, and geography. By application, the market is segmented into detection, jamming, and disruption. The detection segment is further segmented into radars and other sensors (which include RF, acoustic, infrared, and optical technologies). By vertical, the market is segmented into defense, airports, and other critical infrastructures. The report also offers the market sizes and forecasts for the anti-drone market across the major regions across the globe. For each segment, the market sizing and forecasts are done on the basis of revenue (USD).

| Application | Detection | RADARs | |

| Other Sensors | |||

| Jamming and Disruption | |||

| Vertical | Defense | ||

| Airports | |||

| Other Critical Infrastructures | |||

| Geography | North America | United States | |

| Canada | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Latin America | Mexico | ||

| Brazil | |||

| Rest of Latin America | |||

| Middle-East and Africa | Saudi Arabia | ||

| United Arab Emirates | |||

| Rest of Middle-East and Africa | |||

Need A Different Region or Segment?

Customize Now

Anti Drone Market Research FAQs

How big is the Anti-Drone Market?

The Anti-Drone Market size is expected to reach USD 2.55 billion in 2025 and grow at a CAGR of 25.46% to reach USD 7.92 billion by 2030.

What is the current Anti-Drone Market size?

In 2025, the Anti-Drone Market size is expected to reach USD 2.55 billion.

Who are the key players in Anti-Drone Market?

Lockheed Martin Corporation, RTX Corporation, THALES, Israel Aerospace Industries Ltd. and QinetiQ Group plc are the major companies operating in the Anti-Drone Market.

Which is the fastest growing region in Anti-Drone Market?

Latin America is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Anti-Drone Market?

In 2025, the North America accounts for the largest market share in Anti-Drone Market.

What years does this Anti-Drone Market cover, and what was the market size in 2024?

In 2024, the Anti-Drone Market size was estimated at USD 1.90 billion. The report covers the Anti-Drone Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Anti-Drone Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Anti-Drone Market Research

Mordor Intelligence delivers comprehensive insights into the rapidly evolving anti-drone and counter UAS industry. This is achieved through detailed market analysis and consulting services. Our extensive research covers the complete spectrum of drone security solutions. These include drone detection, drone surveillance, and anti-drone technology. The report provides an in-depth analysis of key technologies such as drone jamming, drone RF detection, and drone radar systems. It also examines crucial aspects of drone protection and drone defense strategies. Our expert analysts evaluate various counter drone companies and anti-drone companies. This evaluation offers a complete industry perspective, available in an easy-to-read report PDF format for download.

Stakeholders across the CUAS and counter UAV sectors benefit from our comprehensive coverage of drone countermeasure systems and drone interdiction technologies. The report examines emerging trends in drone neutralization and drone mitigation. It also provides detailed counter drone market forecasts and anti-drone market size analysis. Our research encompasses drone deterrent solutions and anti-drone defense systems. These offer valuable insights for industry participants involved in drone threat detection and counter drone operations. The analysis includes a detailed examination of drone protection technologies and counter UAS market dynamics. This is supported by extensive primary research and data-driven insights.