Anti-Biofilm Wound Dressing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

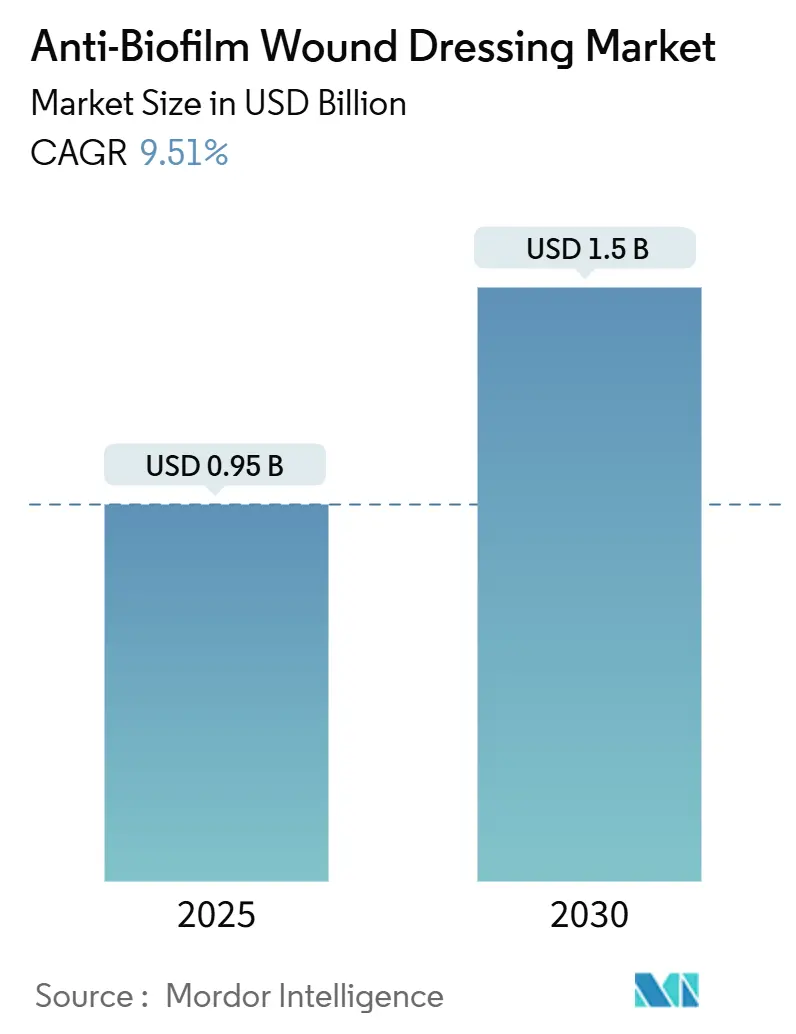

| Market Size (2025) | USD 0.95 Billion |

| Market Size (2030) | USD 1.5 Billion |

| Growth Rate (2025 - 2030) | 9.51% CAGR |

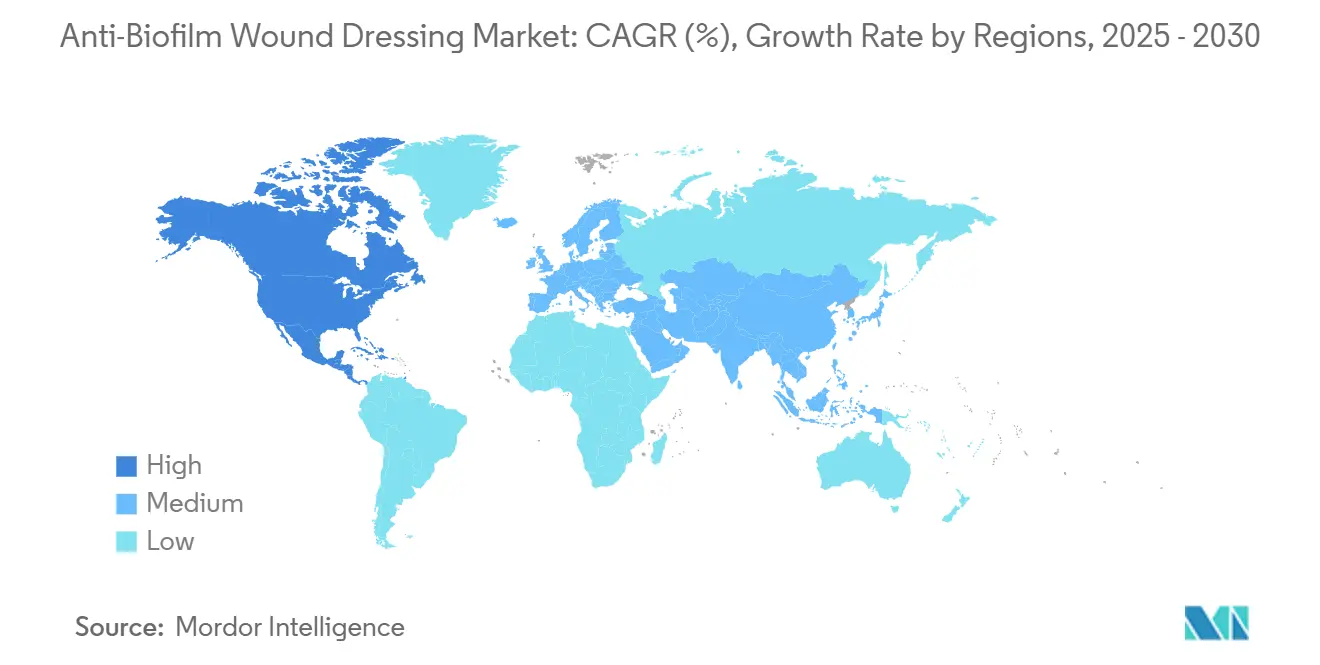

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anti-Biofilm Wound Dressing Market Analysis by Mordor Intelligence

The anti-biofilm wound dressings market is valued at USD 0.95 billion in 2025 and is forecast to reach USD 1.50 billion by 2030, advancing at a 9.51% CAGR. This growth rests on the clinical reality that 78.2% of chronic wounds carry biofilms that slow or stall healing. Health-care systems are moving topical therapy to the front line as antimicrobial-resistance stewardship reduces systemic antibiotic use. Regulatory focus is sharpening: the United States Food and Drug Administration proposed a November 2023 re-classification that may limit indiscriminate silver use, driving demand for technologies able to clear biofilms without fueling resistance. North America led with 41.54% revenue in 2024, yet Asia-Pacific is the fastest climber at an 11.07% CAGR on the back of hospital capacity additions and ageing populations. Chemical mechanisms, especially silver, still dominate, but biological mechanisms are the fastest riser, reflecting a pivot toward enzymatic and immune-modulating approaches.

Key Report Takeaways

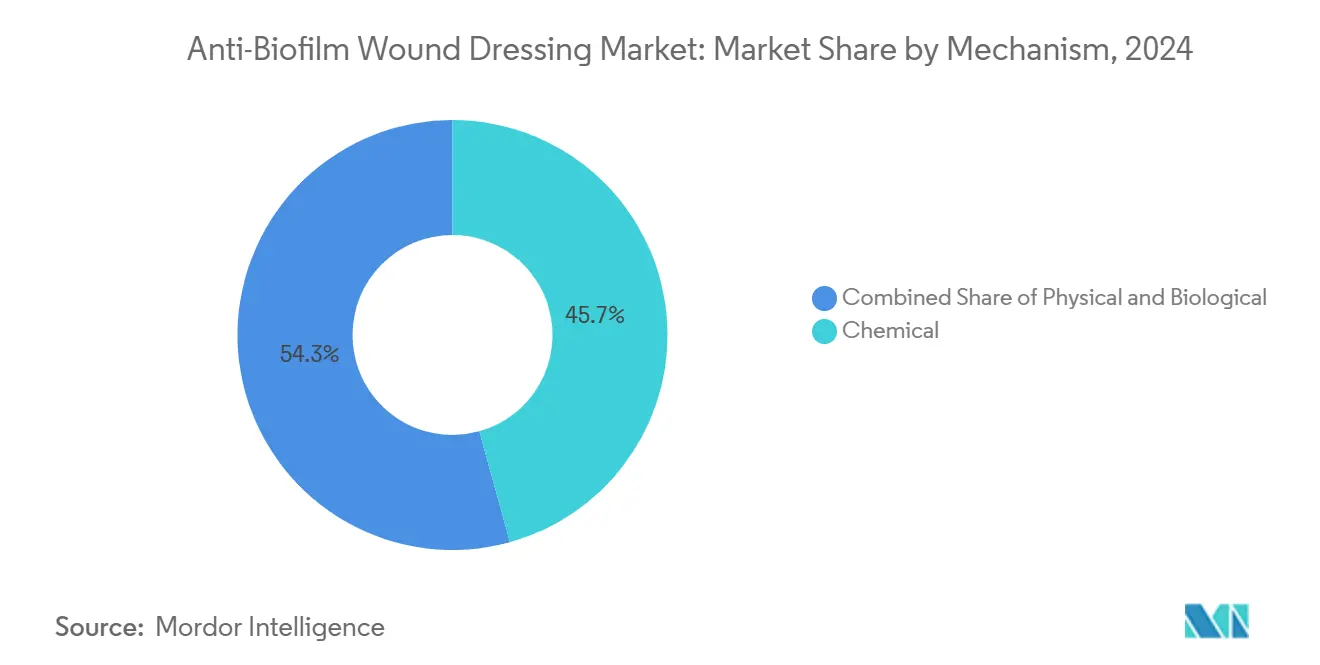

- By mechanism, chemical platforms held 45.73% of the anti-biofilm wound dressings market share in 2024, while biological approaches are tracking a 10.12% CAGR through 2030.

- By material, alginates led with 39.76% of the anti-biofilm wound dressings market size in 2024; hydrocolloids are on course for a 9.87% CAGR to 2030.

- By antimicrobial agent, silver commanded 57.25% of the anti-biofilm wound dressings market size in 2024; biopolymers such as chitosan are expanding at 10.24% CAGR.

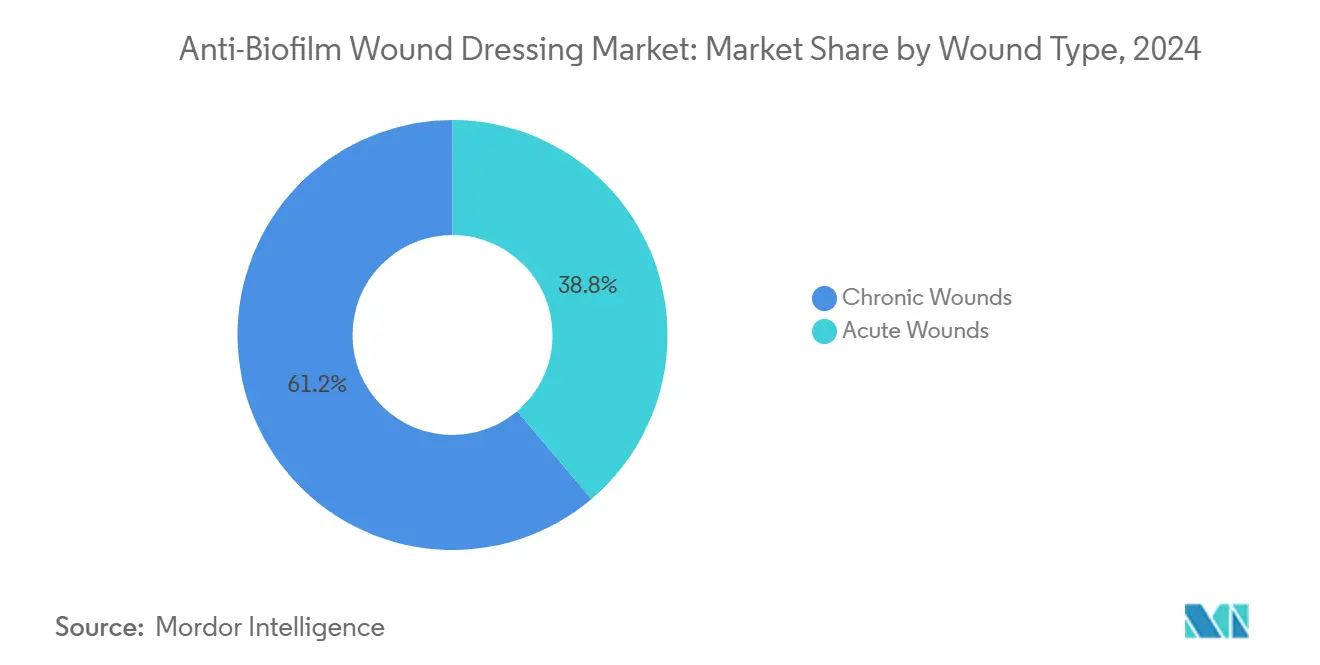

- By wound type, chronic wounds accounted for 61.25% of the anti-biofilm wound dressings market size in 2024, whereas acute wounds are growing at 10.82% CAGR.

- By end user, hospitals and clinics captured 54.35% revenue in 2024; home health-care settings show the highest growth at 10.94% CAGR.

Global Anti-Biofilm Wound Dressing Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic wounds | +2.1% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Surge in surgical procedures | +1.8% | Global, led by Asia-Pacific growth | Short term (≤ 2 years) |

| Product innovation in advanced wound care | +2.3% | North America & EU regulatory leadership | Long term (≥ 4 years) |

| Reimbursement support for antimicrobial dressings | +1.4% | North America, expanding to EU | Medium term (2-4 years) |

| Stewardship shift from systemic to topical therapies | +1.2% | Global, driven by regulatory mandates | Long term (≥ 4 years) |

| AI-enabled digital wound platforms accelerating adoption | +0.7% | North America & select EU markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Wounds

Chronic wounds now impose an AUD 2–4 billion (USD 1.3–2.6 billion) annual burden in Australia alone. Older adults and people with diabetes present impaired immunity that fosters biofilm formation, and 80% of non-healing ulcers have biofilms. The epidemiology is shifting treatment protocols toward dressings able to dismantle biofilm architecture. Procurement policies now specify anti-biofilm capability, especially for home health programs where nurse oversight is limited. This momentum elevates demand for solutions that shorten healing time and curb systemic antibiotic use.

Surge in Surgical Procedures

Global surgical volume is rising fastest in Asia-Pacific. Acute wounds from operations can form biofilms within hours, prompting hospitals to add anti-biofilm dressings to peri-operative bundles. Silver-coated sutures cut Staphylococcus aureus and multi-drug-resistant Pseudomonas aeruginosa colonization in controlled trials. Orthopedic and cardiac centers now extend biofilm-prevention protocols to closed-incision care, expanding addressable demand beyond chronic wounds. As a result, the anti-biofilm wound dressings market is embedding into surgical infection control budgets.

Product Innovation in Advanced Wound Care

Hydrogel dressings that generate reactive oxygen species in acidic micro-environments and quench them in physiological pH sped diabetic-ulcer closure in animals without auxiliary phototherapy. Developers also blend alginate with nano-zinc oxide for dual antimicrobial and regenerative action. Intellectual-property race is intensifying as firms secure patents on smart materials that balance biofilm clearance and tissue biocompatibility. Investors value platforms that can carry multiple actives, paving the way for single-SKU portfolios that treat diverse wound types while reducing inventory pressure for care providers.

Stewardship Shift to Topical Therapies

World-wide antimicrobial stewardship guidelines encourage topical over systemic use to slow resistance. Hospitals report 15% less systemic antibiotic exposure after integrating biofilm-targeted dressings into formularies. Regulators in Europe and the United States are signaling preference for combination dressings that deliver precise antimicrobial doses at the wound interface. This policy context accelerates adoption of advanced dressings and supports premium pricing structures.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High product cost vs. conventional dressings | -1.9% | Global, acute in price-sensitive markets | Short term (≤ 2 years) |

| Regulatory ambiguity for combination dressings | -1.1% | North America & EU primarily | Medium term (2-4 years) |

| Emerging bacterial tolerance to silver ions | -0.8% | Global, concentrated in high-usage facilities | Long term (≥ 4 years) |

| Environmental disposal concerns for nano-dressings | -0.6% | EU leading, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Product Cost vs. Conventional Dressings

Premium price points challenge uptake, especially in publicly funded systems that still reimburse commodity gauze. Yet real-world evidence shows total treatment expense drops when anti-biofilm dressings cut healing time and facility visits. The 2025 Medicare Physician Fee Schedule expands tele-wound codes, letting clinicians guide community nurses remotely and reduce inpatient stays. As payers reward outcome-based pathways, budget silos are breaking, and upfront cost barriers are softening.

Emerging Bacterial Tolerance to Silver Ions

Laboratory studies confirm Escherichia coli aggregates flagellin to neutralize silver nanoparticles, while Staphylococcus aureus thickens biofilms to the same end. Manufacturers are responding with combination chemistries—pomegranate-rind-extract or cyanographene carriers—to keep silver effective. The long-term threat is steering R&D funds toward biopolymer and enzymatic antimicrobials that do not rely on heavy metals.

Segment Analysis

By Mechanism: From Chemical Dominance to Biological Momentum

Chemical mechanisms retained 45.73% of the anti-biofilm wound dressings market in 2024 on the back of mature silver and iodine technologies that hospitals trust for broad-spectrum cover. Physical strategies, such as structured foams that shear microbial films, hold a middle share for patients needing exudate control. Yet biological platforms are carving space at a 10.12% CAGR. Enzymatic disruptors like recombinant Tarumase digest fibrin, collagen, and elastin—the scaffolds that stabilize biofilms—overcoming the penetration limits of many chemicals.

Second-generation dressings now blend biological and chemical modes. A single substrate may release PHMB for immediate bactericidal action and a protease for matrix breakdown, delivering a one-two punch that clinicians can deploy without double dressing changes. Integrated mechanisms lower nursing hours, a key cost driver in chronic-care wards, and they future-proof portfolios against emerging silver tolerance. Because reimbursement codes reward evidence-based outcomes, suppliers that validate multi-mechanism efficacy are pulling formulary preference away from single-mode incumbents.

Note: Segment shares of all individual segments available upon report purchase

By Dressing Material: Alginate Strength Meets Hydrocolloid Acceleration

Alginate fibers commanded 39.76% of revenue in 2024 due to high absorptive capacity and gentle gel formation that does not strip fragile tissue during changes. Their calcium-rich lattice also binds ionic silver, making alginate a favored carrier for antimicrobial release. Foam dressings remain widespread for moderate exudate because of cushioning and cost advantages, while thin hydrogels serve niche rehydration roles.

Hydrocolloids are on track for a 9.87% CAGR. New formulations impregnate hydrophobic particles that breach biofilms and subsequently swell to seal the wound, limiting environmental contamination. Manufacturers extend wear time to seven days, which reduces change frequency and nursing labor. Nanofiber mats and electrospun membranes are gaining clinical trial traction, but production scale remains a hurdle. Bacterial cellulose, harvested through green fermentation, is entering value-based procurement lists because it is biodegradable and naturally antimicrobial—aligning with hospital sustainability mandates.

By Active Antimicrobial Agent: Silver Supremacy Faces Biopolymer Innovation

Silver’s 57.25% share in 2024 stems from its wide kill spectrum and decades of clinical data. Innovations include porous ceramic carriers that meter ionic release and limit systemic uptake. Iodine maintains a presence in trauma settings needing rapid action, while PHMB resonates in European sites wary of heavy metals.

Chitosan oligomers now headline the fastest-growing category at 10.24% CAGR. A recently granted United States patent combines chitosan with zinc-oxide nanoparticles for synergistic impact against multi-drug-resistant strains [1]United States Patent 10,675,301, “Chitosan-zinc oxide antimicrobial composite,” uspto.gov. Biopolymers double as scaffolds for tissue repair, letting manufacturers argue for dual clinical benefits. Metal-oxide nanoparticles such as bismuth-thiol complexes also show promise; a 2023 patent application demonstrated high activity against mature Pseudomonas biofilms.

By Wound Type: Chronic Complexity Spurs Acute Opportunity

Chronic wounds represented 61.25% of revenue in 2024 because diabetic foot and pressure ulcers stubbornly harbor biofilms that block epithelial migration. Guidelines now recommend anti-biofilm dressings at the initial assessment when slough or odor suggests microbial burden. Venous ulcers gain from calcium alginate-silver combinations that balance exudate control and biofilm clearance.

Acute wounds are scaling fastest at 10.82% CAGR. Orthopedic and cardiac units are trialing prophylactic biofilm-resistant dressings on closed incisions, citing lower infection readmissions. Burn centers favor nanofiber-silver composites that remain flexible on joints and release silver only when local pH rises, an early infection signal. Emergency departments stock shelf-stable hydrocolloids for trauma use, broadening retail pharmacy demand. The prevention narrative is reframing the anti-biofilm wound dressings market from chronic-only to every surgical suite.

Note: Segment shares of all individual segments available upon report purchase

By End User: Hospital Stronghold Gives Way to Home Health Momentum

Hospitals and clinics held 54.35% share in 2024 because severe chronic wounds require debridement and culture services. Infection-control committees routinely update formularies, and group purchasing organizations secure volume discounts that still favor incumbent technologies. Ambulatory surgical centers now represent a strategic channel where quick turnover amplifies the value of dressings that cut dressing-change time.

Home health-care is advancing at 10.94% CAGR as ageing-in-place becomes policy across OECD economies. Caregivers need intuitive dressings with clear indication windows that signal saturation. Tele-wound platforms such as Swift Medical process 600,000 scans monthly, letting nurses escalate cases showing early biofilm fluorescence. The 2025 Medicare update funds caregiver training modules, easing adoption in the United States. Device makers are bundling dressings with mobile apps and fluorescence probes, creating ecosystem lock-in that raises switching costs.

Geography Analysis

North America continued to lead, delivering 41.54% of 2024 revenue as payers reimbursed advanced dressings and hospitals adopted digital wound surveillance. The region hosts the largest concentration of trials and has clear coding pathways such as the 2025 CMS updates that clarify coverage for skin substitutes [2]U.S. CMS, “2025 Medicare Fee Schedule for Wound Care,” convatec.com . The United States Food and Drug Administration’s re-classification proposal is expected to tighten evidence standards, favoring companies with robust clinical datasets.

Europe offers a sophisticated regulatory environment shaped by the EU Medical Device Regulation 2017/745, which imposes traceability and performance reporting [3]European Commission, “Medical Device Regulation 2017/745,” eur-lex.europa.eu. Environmental stewardship drives hospitals to pilot biodegradable and metal-free platforms. The European Wound Management Association updates consensus documents that influence clinician purchasing. Germany and France run national tender systems rewarding suppliers that can document both efficacy and waste reduction.

Asia-Pacific displayed the highest momentum, expanding at an 11.07% CAGR through 2030. China’s domestic bandage output and hospital modernisation lower price points, widening access. Japan’s super-aged society prioritises home wound care solutions that reduce caregiver burden. India’s production-linked incentives for medical devices lure multinational partners seeking cost-efficient capacity. Australia highlights the economic toll of chronic wounds, boosting reimbursement for advanced dressings through state health plans.

Competitive Landscape

The anti-biofilm wound dressings market is moderately fragmented. 3M, Smith+Nephew, and ConvaTec combine global distribution with regulatory acumen to retain lead positions. Their strategy centers on platform lines—one substrate engineered in various sizes and impregnations—which streamlines approvals in multiple jurisdictions. ConvaTec’s 2024 launch of an extended-wear negative-pressure dressing cuts application time by 61% and cost by 41%, demonstrating process innovation aimed at hospitals seeking labor efficiency.

Intellectual property is a key moat. Bismuth-thiol complexes filed in 2023 show high potency at low doses, and players aggressively licence or acquire start-ups to access novel chemistries. In June 2025, SolasCure secured FDA Fast Track for Aurase, a Tarumase-based hydrogel that enzymatically dismantles biofilms while sparing healthy tissue—signalling regulators’ openness to biological agents. Established firms partner with AI diagnostics vendors like MolecuLight to integrate fluorescence imaging that flags elevated bacterial load at the bedside. ESG pressures spur R&D in biodegradable carriers to pre-empt future disposal regulations.

Start-ups focus on enzyme, peptide, or phage solutions that bypass metal resistance. Venture funding supports nanofiber spinning platforms capable of layering multiple actives, attracting hospital groups that prefer one dressing regimen across wound types. Large incumbents answer by opening innovation hubs that co-develop with clinicians, compressing bench-to-bedside cycles. Competitive intensity is set to rise as patents expire and regional suppliers scale localised production.

Anti-Biofilm Wound Dressing Industry Leaders

Convatec Inc.

Smith+Nephew

3M

B. Braun SE

Mölnlycke Health Care AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: SolasCure received FDA Fast Track Designation for Aurase Wound Gel enzymatic hydrogel targeting biofilm-laden calciphylaxis ulcers.

- September 2024: Solventum introduced V.A.C. Peel and Place Dressing, an extended-wear negative-pressure system reducing application time by 61% and costs by 41%.

- March 2022: ConvaTec acquired Triad Life Sciences for USD 450 million to expand biologically derived dressings for chronic and surgical wounds.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the anti-biofilm wound dressing market as global revenue from single or limited-use dressings that actively disrupt or prevent microbial biofilms on acute or chronic wounds through chemical (silver, iodine, PHMB), physical (debridement, pulsed electrical field), or biological (enzymes, peptides) means.

Scope Exclusion: We exclude negative-pressure devices, standalone topical gels, and systemically administered anti-infectives.

Segmentation Overview

- By Mechanism

- Physical

- Chemical

- Biological

- By Dressing Material

- Foam

- Hydrogel

- Hydrocolloid

- Alginate

- Film & Membrane

- Nanofiber / Electrospun

- Bacterial Cellulose

- By Active Antimicrobial Agent

- Silver-based

- Iodine-based

- Polyhexanide (PHMB)

- Honey / Natural Bio-actives

- Chitosan & Other Biopolymers

- Metal-oxide Nanoparticles

- By Wound Type

- Chronic Wounds

- Diabetic Foot Ulcers

- Pressure Ulcers

- Venous Leg Ulcers

- Other Chronic Wounds

- Acute Wounds

- Surgical / Traumatic Wounds

- Burns

- Chronic Wounds

- By End User

- Hospitals & Clinics

- Ambulatory Surgical Centers

- Home Healthcare Settings

- Military & Emergency Care

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed wound surgeons, specialist nurses, hospital buyers, and distributors across North America, Europe, Asia-Pacific, and the Middle East. Their insights on usage frequency, average selling prices, and formulary hurdles let us fine-tune regional assumptions and confirm model boundaries.

Desk Research

We begin with open datasets, WHO Global Burden of Disease, CDC National Hospital Discharge Survey, Eurostat surgical logs, and UN Comtrade trade codes to map wound incidence, procedure counts, and dressing flows by geography. Peer-reviewed articles, Wound Healing Society white papers, and patent trends on Questel then help us trace biofilm prevalence and technology lifecycles.

Our team adds company 10-Ks, investor decks, and news from Dow Jones Factiva, while D&B Hoovers supplies audited financials that anchor manufacturer revenue splits. These are illustrative; numerous additional publications, registries, and databases underpin secondary validation.

Market-Sizing & Forecasting

A top-down pool combines chronic wound prevalence, surgical volume, and burn incidence with frequency of change factors to derive annual dressing demand, which we multiply by region-specific ASPs. Supplier roll-ups, channel checks, and sampled invoice data provide bottom-up reasonableness tests; gaps are reconciled through three-way cross checks before lock-in. Predictor variables, diabetes prevalence, population over 65, silver price indices, reimbursement shifts, and adoption rates of single-patient foam dressings, feed a multivariate regression plus ARIMA blend. This is where Mordor Intelligence's structured model differentiates, giving a forecast for the forecast period.

Data Validation & Update Cycle

Our outputs undergo variance screens against historical series, peer review, and scenario stress tests. Reports refresh annually, with mid-cycle updates after material regulatory or recall events; just before publication we rerun the latest data so clients receive the freshest baseline.

Why Mordor's Anti-Biofilm Wound Dressing Baseline Commands Reliability

Published estimates diverge because firms vary product inclusions, ASP progression, and refresh cadence.

By anchoring scope to proven anti-biofilm mechanisms and aligning volumes with observed treatment patterns, we deliver a dependable reference.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.95 B (2025) | Mordor Intelligence | |

| USD 0.94 B (2024) | Global Consultancy A | excludes biological dressings, flat ASPs |

| USD 0.86 B (2024) | Trade Journal B | relies solely on hospital procurement tallies |

| USD 0.87 B (2024) | Industry Association C | five-year data refresh, constant currency |

We believe decision-makers gain a balanced, transparent baseline because every figure traces back to clear variables, multi-source validation, and an annual refresh discipline.

Key Questions Answered in the Report

What is the current Anti-Biofilm Wound Dressing Market size?

The anti-biofilm wound dressings market size stands at USD 0.95 billion in 2025.

Who are the key players in Anti-Biofilm Wound Dressing Market?

Convatec Inc., Smith+Nephew, 3M, B. Braun SE and Mölnlycke Health Care AB are the major companies operating in the Anti-Biofilm Wound Dressing Market.

Which is the fastest growing region in Anti-Biofilm Wound Dressing Market?

Asia-Pacific is projected to expand at an 11.07% CAGR thanks to expanding hospital capacity and an ageing population.

Which region has the biggest share in Anti-Biofilm Wound Dressing Market?

In 2025, the North America accounts for the largest market share in Anti-Biofilm Wound Dressing Market.

What restraint could slow near-term adoption?

Higher upfront prices versus conventional gauze remain a barrier in budget-sensitive markets, although total cost of care studies suggest longer-term savings.

Page last updated on: