Animal Intestinal Health Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

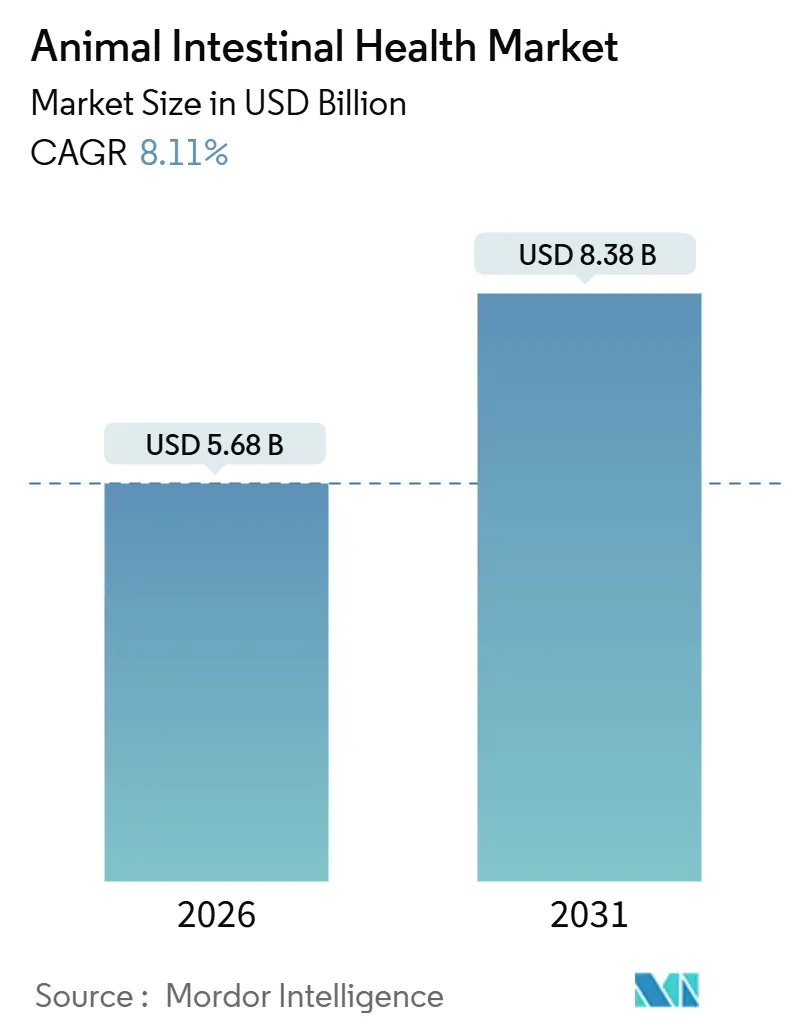

| Market Size (2026) | USD 5.68 Billion |

| Market Size (2031) | USD 8.38 Billion |

| Growth Rate (2026 - 2031) | 8.11% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

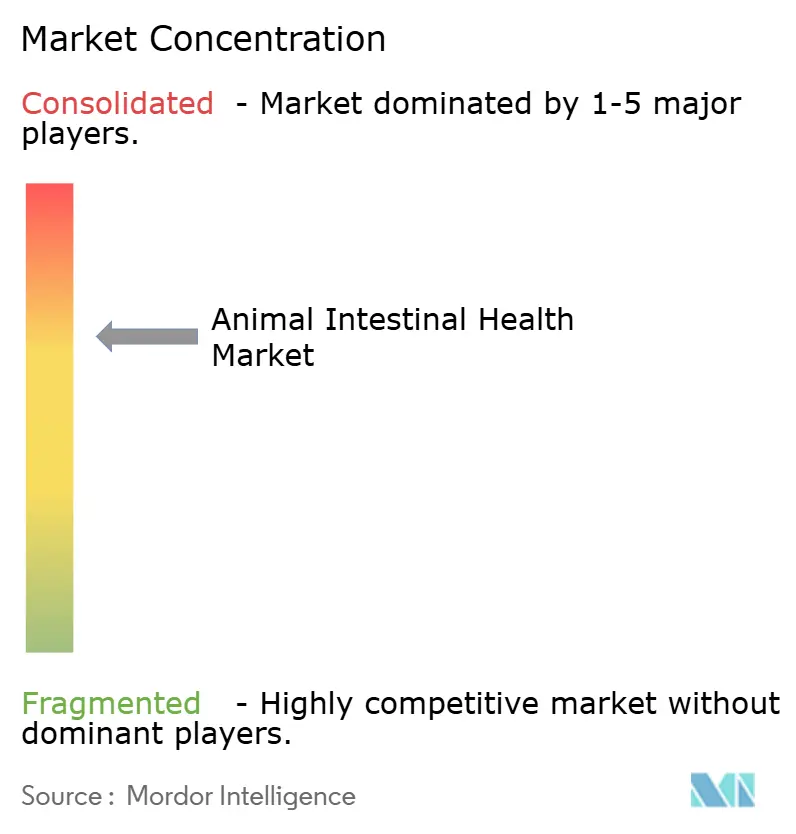

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Animal Intestinal Health Market Analysis by Mordor Intelligence

The Animal Intestinal Health Market size is estimated at USD 5.68 billion in 2026, and is expected to reach USD 8.38 billion by 2031, at a CAGR of 8.11% during the forecast period (2026-2031).

Momentum follows the global shift away from antibiotic growth promoters toward evidence-based gut health solutions that safeguard productivity while conforming to regulatory limits. Demand also rises because intestinal disorders have become more prevalent in high-density production systems, thereby reducing feed efficiency and driving the adoption of preventive additives. Prebiotics, probiotics, immunostimulants, and phytogenics now form the core toolkit producers use to keep livestock performance on track. Artificial intelligence is broadening that toolkit by matching specific additive blends to each species’ and breed’s distinct microbiome, lowering trial-and-error costs and improving consistency. Meanwhile, supply chain complexity and premium raw material pricing place steady upward pressure on finished product costs, especially in price-sensitive regions.

Key Report Takeaways

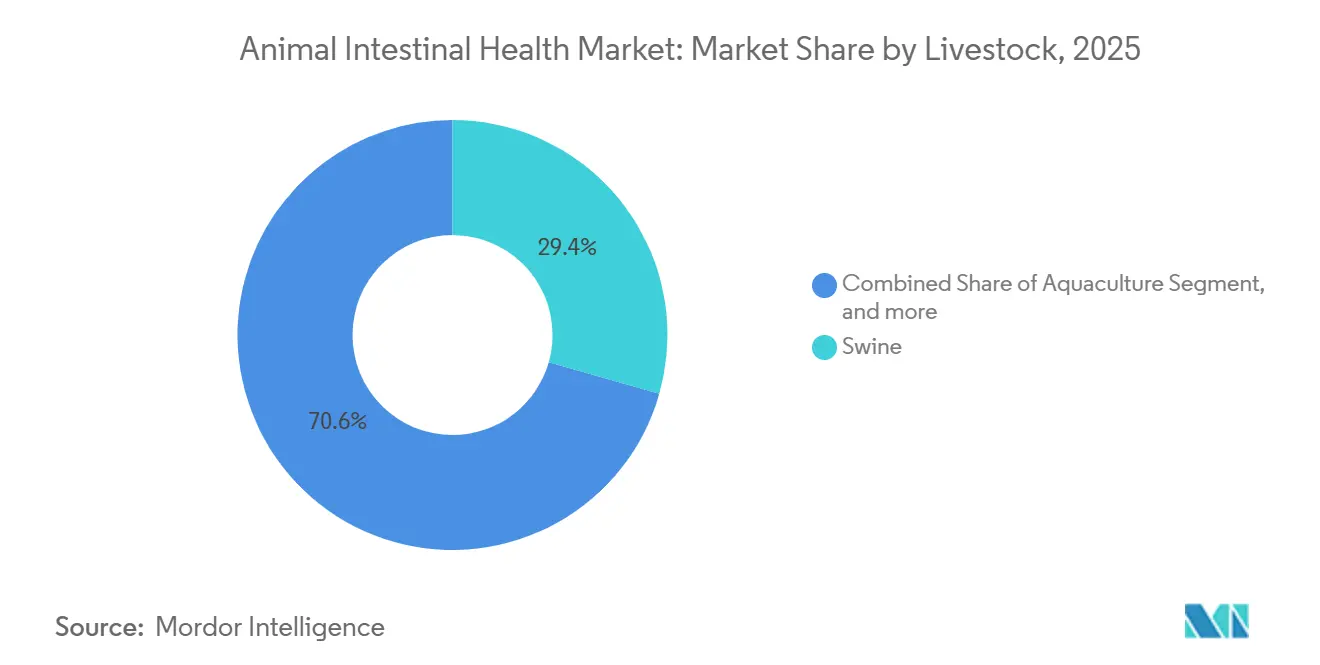

- By livestock, swine held 29.45% of the animal intestinal health market share in 2025, while aquaculture is expanding at a 10.34% CAGR through 2031.

- By additive, prebiotics led with 27.54% revenue share in 2025; phytogenics post the fastest CAGR at 9.89% to 2031.

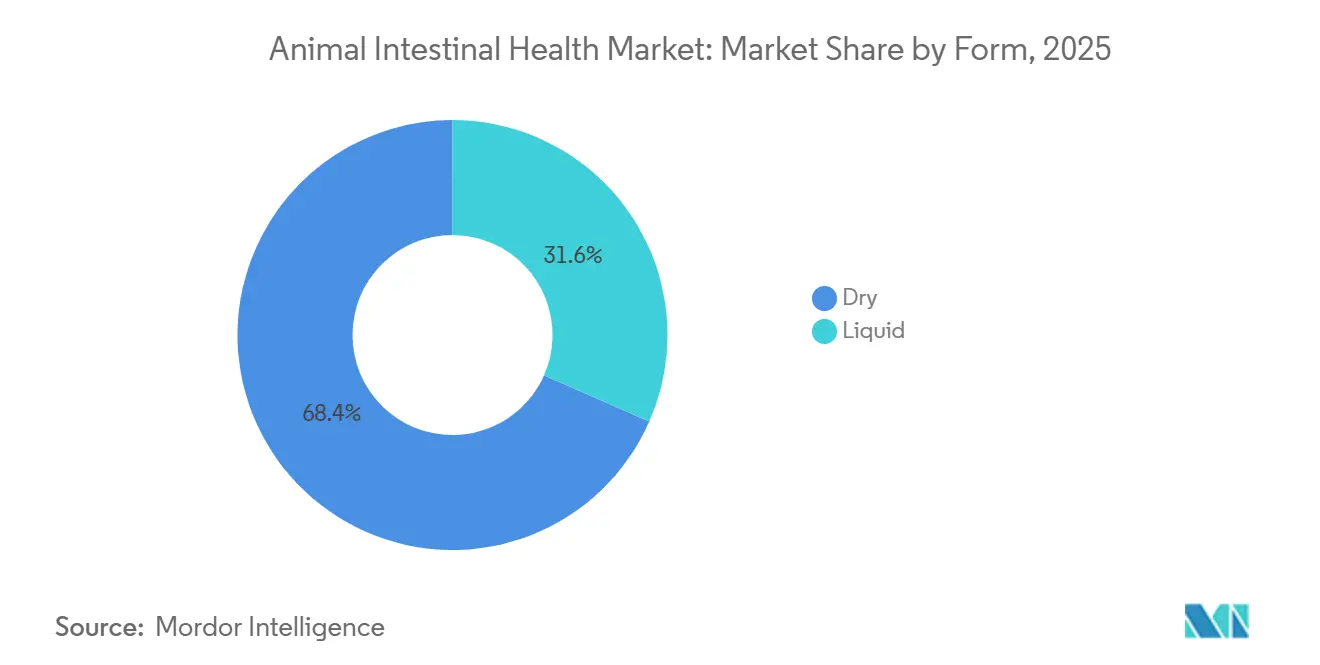

- By form, dry formats commanded 68.43% of the animal intestinal health market size in 2025, whereas liquid products are advancing at a 10.11% CAGR.

- By source, microbial ingredients accounted for 58.32% share in 2025, and plant-based sources are projected to grow at an 11.43% CAGR.

- By geography, North America dominated with 41.33% share in 2025, whereas Asia-Pacific is projected to register a 9.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Animal Intestinal Health Market Trends and Insights

Driver Impact Analysis

| Driver | (%) (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising intestinal disorders among livestock | +2.1% | Global, most pronounced in intensive systems | Medium term (2-4 years) |

| Growth in functional animal-feed production | +1.8% | North America and EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| AGP bans shifting demand to gut-health aids | +2.3% | EU and North America, spillover to emerging markets | Short term (≤ 2 years) |

| Insect-protein farming spurring prebiotic use | +0.9% | Asia-Pacific core, adoption in Netherlands and Canada | Long term (≥ 4 years) |

| AI-driven microbiome profiling | +1.0% | United States, EU, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Intestinal Disorders Among Livestock Drive Market Expansion

Higher stocking densities, faster growth cycles, and fluctuating temperatures have increased the prevalence of gut disorders in most commercial species. Post-weaning diarrhea now affects up to one-fifth of modern swine cohorts and has become costlier than respiratory disease in some units. Poultry producers navigating AGP withdrawals face similar pressure from necrotic enteritis outbreaks that trim weight gain and raise mortality. Producers calculate that each percentage point loss in feed conversion adds thousands of dollars to feed bills every cycle, prompting rapid investment in protective additives. Integrating probiotics and prebiotics into starter diets has cut diarrhea incidence by 30% in large trials. Demand therefore scales directly with the push to preserve margins without antibiotics, reinforcing the upward trajectory of the animal intestinal health market.

Functional Animal-Feed Production Growth Accelerates Additive Integration

Feed mills increasingly design complete rations that embed gut health ingredients instead of selling them as stand-alone supplements. The practice simplifies logistics for livestock enterprises and guarantees uniform additive delivery from the first to the last bite. Major European integrators have expanded functional-feed lines by nearly one-third since 2024. In parallel, extruders and pelleting lines have been upgraded with temperature-controlled zones that protect probiotic viability, allowing higher inclusion levels without sacrificing live-cell counts. Savings accrue because one production pass now accomplishes what used to require multiple on-farm steps, and additive makers benefit from more predictable off-take agreements with feed formulators. These trends anchor a structural rise in bulk orders and underpin sustained revenue growth for the animal intestinal health market.

AGP Bans Accelerate Transition to Gut Health Alternatives

Regulators have outlawed or curtailed antibiotic growth promoters across most of the developed world, and emerging economies are following suit. India’s food-safety agency extended its ban to additional drug classes in 2024, while Thailand introduced voluntary reduction targets that poultry exporters already meet to protect market access. Producers that relied on cheap AGPs now face a 12- to 18-month adjustment period in which performance dips unless replaced by robust gut-health programs. Combination packs featuring synergistic blends of probiotics, prebiotics, and phytogenics restore 95-98% of historical growth rates in European swine and poultry barns[1]European Food Safety Authority, “Scientific Opinion on the Safety of Phytogenics,” efsa.europa.eu. These documented field results strengthen confidence in non-antibiotic solutions and fast-track procurement decisions, enlarging the addressable base for the animal intestinal health market.

AI-Driven Microbiome Profiling Enables Precision Nutrition Strategies

Machine-learning platforms are lowering the cost of selecting the right additive for each flock, pond, or pen. Cargill, DSM, and several start-ups now offer services that analyze fecal or water microbiome samples, match observed microbial signatures to a proprietary strain database, and recommend an optimized formulation within day[2]D. Kelly et al., “Machine Learning in Microbiome Analysis,” nature.com. Early adopters cite additive cost savings of 15-20% and steadier production metrics. The approach holds particular value in aquaculture, where variations in salinity, temperature, and stocking density destabilize microbial communities. Real-time dashboards signal when microbiome composition drifts outside target ranges, letting managers adjust dosing before disease pressure intensifies. Widespread rollout of these digital services promises to lock customer loyalty and expand high-margin revenue streams across the animal intestinal health market.

Restraints Impact Analysis

| Restraint | (%) (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory approval timelines | −1.2% | Global, most acute in EU and North America | Medium term (2-4 years) |

| High cost of specialty gut-health ingredients | −0.8% | Latin America and parts of Asia | Short term (≤ 2 years) |

| Microbiome variability across breeds limits standardisation | −0.7% | Global, especially in multi-breed production systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Approval Timelines Constrain Innovation Deployment

Bringing a novel probiotic or phytogenic to market can require two to three years of dossier preparation and review in major jurisdictions. EFSA’s Qualified Presumption of Safety process demands extensive genomic and toxicology data, while the U.S. FDA’s GRAS route insists on multi-species feeding trials that together can cost USD 2–5 million per application[3]European Food Safety Authority, “Regulatory Guidance for Feed Additives,” efsa.europa.eu. Such hurdles lengthen the payback period and deter small biotechnology firms from entering the space, narrowing the pipeline of disruptive solutions. Even large multinationals must stagger launches geographically to recoup cost, which slows the global diffusion of breakthroughs and tempers near-term expansion in the animal intestinal health market.

High Costs of Specialty Ingredients Limit Market Penetration

Advanced probiotic cultures and purified oligosaccharides command premiums three- to fivefold above conventional additives, pushing total feed costs up by as much as 12% in intensive systems. While vertically integrated producers in North America and Europe can absorb these costs, price-sensitive operators in Latin America and Southeast Asia often delay adoption or select cheaper, less potent alternatives. Manufacturers now experiment with lower-dose formulations and controlled-release coatings to stretch efficacy and mitigate price concerns. Success will hinge on proving that incremental performance gains outweigh extra feed expense, particularly where live-weight prices remain volatile.

Segment Analysis

By Livestock: Swine Remains Core While Aquaculture Surges

Swine contributed 29.45% to the animal intestinal health market size in 2025 as production systems tightened biosecurity and replaced AGPs with multi-strain probiotic and prebiotic packages. Post-weaning programs now emphasize early gut colonization to limit pathogenic E. coli proliferation that erodes growth. Meanwhile, aquaculture posts a 10.34% CAGR, the highest among all species, supported by rising seafood demand and chronic bacterial challenges in intensive ponds. Freshwater tilapia and brackish shrimp farms adopt coated probiotics that survive water dispersion and improve feed conversion. Poultry retains steady demand, mainly from broiler complexes combating necrotic enteritis after AGP removal. Ruminant adoption centers on calf and lamb starter feeds, with specialty blends easing the transition from milk to solid feed. Insect farming, led by black soldier fly larvae, appears small today but opens an innovative niche for targeted prebiotics that raise protein-conversion efficiency.

The animal intestinal health market share edge held by swine is expected to compress as aquaculture’s absolute spending climbs. Shrimp growers in Vietnam and India already dedicate up to 4% of feed budgets to gut additives, mirroring levels typical in swine systems. Competitive intensity therefore shifts toward water-stable formulations, with suppliers leveraging patents on micro-encapsulation and spore-forming strains. Cross-species platforms also gain traction, letting companies repurpose IP developed for terrestrial livestock in aquatic settings. This convergence lifts volumes and strengthens economies of scale across the value chain.

Note: Segment shares of all individual segments available upon report purchase

By Additive: Prebiotics Lead While Phytogenics Gain Ground

Prebiotics accounted for 27.54% of the animal intestinal health market share in 2025, anchored by fructo-oligosaccharides and mannan-rich fractions that enhance beneficial bacteria growth. Their compatibility with most regulatory frameworks and ability to tolerate high pelleting temperatures secure widespread usage. Phytogenics grow fastest at 9.89% CAGR, buoyed by plant-derived compounds such as essential oils that exhibit antimicrobial and anti-inflammatory properties without the residue concerns linked to synthetic additives. Probiotics comprise a mature but innovation-active cluster, with researchers tailoring strains for heat resistance and spore formation to widen use in pelleted feeds. Immunostimulants, while niche, attract attention for reducing vaccine-stress impacts in young animals.

Producers gravitate toward multi-component solutions that blend prebiotics with phytogenics, achieving synergistic action on microbial balance and intestinal integrity. This holistic tilt differentiates premium offerings and raises switching costs for end users. Suppliers that validate such combinations through peer-reviewed trials enjoy faster listing by international feed formulators. Regulatory bodies in the European Union and Brazil have begun approving specific phytogenic molecules, a milestone that encourages broader uptake and dilutes historical skepticism around botanical variability.

By Form: Dry Products Hold the Bulk, Liquids Scale Quickest

Dry formats generated 68.43% of the animal intestinal health market size in 2025 owing to easier handling, longer shelf life, and compatibility with existing feed-mill infrastructure. Uniform particle distribution in mash and pelleted rations ensures consistent intake without extra on-farm labor. Liquid additions, however, log a 10.11% CAGR, propelled by recirculating aquaculture systems and precision-feeding setups that meter supplements via automated pumps. Liquid carriers also allow higher inclusion of heat-sensitive compounds and enzymes that would denature during pelleting.

Manufacturers mitigate the packaging and cold-chain hurdles inherent to liquids by developing concentrated emulsions and shelf-stable paste formats. In swine nurseries, water-soluble probiotics deliver immediate gut support during stress periods such as transport and weaning. Dry-format leaders respond by upgrading micro-encapsulation technology to boost gastric acid resistance, leveling efficacy across forms. The resulting competition sharpens performance claims and expands choice for end users.

Note: Segment shares of all individual segments available upon report purchase

By Source: Microbial Dominance Meets Plant-Based Momentum

Microbial ingredients supplied 58.32% of 2025 revenue, benefiting from decades of fermentation know-how and scalable stainless-steel capacity worldwide. Robust quality systems maintain viable cell counts across long supply chains, reinforcing customer trust. Plant-based extracts now advance at an 11.43% CAGR, fueled by clean-label trends and breakthroughs in selective extraction that concentrate active phytochemicals. Algal beta-glucans and yeast-derived nucleotides occupy middle ground, bridging microbial and plant categories.

Sourcing diversification reduces reliance on corn and soybean streams tied to commodity price swings, a strategic plus during raw-material inflation. Additionally, synergistic blends combining microbial and plant actives reduce inclusion rates yet broaden functional coverage, appealing to integrators seeking fewer SKUs without performance trade-offs. Intellectual-property filings therefore increasingly target dual-source compositions that leverage distinct mechanisms for barrier function, immune modulation, and pathogen control.

Geography Analysis

North America held 41.33% of the animal intestinal health market in 2025, led by the United States, where mandatory veterinary feed directives and early AGP withdrawals fostered rapid alternative adoption. Large integrators deploy real-time monitoring devices that link pen-side sensors with cloud-based nutrition platforms, allowing quick dosing adjustments when gut dysbiosis signals emerge. Canada’s thriving black soldier fly sector also boosts prebiotic sales, as larvae growers refine microbiome management to improve protein yield, while Mexico’s feed industry scales probiotic use to satisfy export-market residue limits.

Asia-Pacific demonstrates the swiftest climb with a projected 9.54% CAGR, underpinned by surging fish and shrimp output and continued rise in regional protein demand. China’s post-ASF swine rebuilding accelerates spending on gut health to safeguard newly installed high-biosecurity units. India’s dairy cooperatives invest in calf nutrition programs to curb early-life scours and raise lifetime milk output. Japan and South Korea, characterized by high technology adoption, pilot AI-guided microbiome tools that refine additive selection, providing templates other nations aim to replicate.

Europe records solid, regulation-driven expansion as producers must comply with the world’s toughest antimicrobial curbs. Feed formulators there lead in functional-feed innovations, integrating multiple gut support agents into single pellets accepted by organic certification bodies. Scandinavian poultry complexes showcase low antibiotic-usage benchmarks through probiotics plus oat-based beta-glucans. In contrast, South America and the Middle East & Africa register lower current penetration but deliver new volume growth as local authorities tighten drug-residue controls and export-oriented farms seek certification.

Competitive Landscape

The animal intestinal health market remains moderately concentrated. DSM, Cargill, and Chr. Hansen together account for just under half of global revenue and leverage extensive fermentation assets, formulation labs, and regulatory teams to stay ahead. Their portfolios increasingly marry additive ranges with data analytics and advisory services, shifting the value proposition from commodity sales to outcome-based partnerships. Mid-tier incumbents, such as Kemin and Alltech, compete by focusing on niche actives like algae-derived immunomodulators or fermentation by-products that target specific production phases.

Strategic acquisitions shape the field. Cargill’s purchase of AquaHealth Solutions injects deep aquaculture know-how, while DSM-Firmenich’s USD 150 million digital-nutrition program funds cloud platforms that link microbiome sequencing with feed-mill automation. Start-ups bring genomic precision, using AI to predict strain efficacy before costly barn trials, and often license their libraries to larger players seeking a rapid way to refresh pipelines. Patent filings increasingly cover encapsulation designs that stabilize probiotics during feed processing, a vital differentiator as pelleting temperatures climb to inactivate pathogens.

Partnership patterns emphasize co-development with academic institutes to validate mechanisms, securing faster regulatory clearance and marketing traction. Suppliers also lock in exclusive distribution deals with regional feed mills, which guarantees baseline volumes and discourages brand switching. Competitive focus now shifts to insect and alternative-protein channels, where first movers aim to establish specifications that could become de facto standards as the segment scales.

Animal Intestinal Health Industry Leaders

AB Vista

DuPont

Kemin Industries, Inc.

Lesaffre

Bluestar Adisseo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Lallemand Animal Nutrition launched a comprehensive educational program on ruminant digestive welfare as part of Lallemand Animal Nutrition Services, featuring the newly relaunched ruminantdigestivesystem.com in an enhanced interactive format. The program provides nutritionists, farmers, advisers, and veterinarians with valuable training information on critical topics related to the entire ruminant digestive track and its impact on overall cattle welfare and productivity.

- August 2025: Protexin launched a new online digestive health information hub for pet owners. The platform combines vet-authored articles on topics such as probiotics, gut health, nutrition and behaviour with an online storefront selling Protexin’s range of digestive supplements.

Global Animal Intestinal Health Market Report Scope

As per the scope of this report, animal intestinal health refers to gut health as physiological and functional factors, including nutrient digestion and absorption, host metabolism and energy generation, a stable and applicable microbiota/microbiome, defense mechanisms, and the interactions between these factors.

The Animal Intestinal Health market is segmented by by Livestock (Aquaculture, Poultry, Ruminant, Swine, and Others), Additive (Probiotics, Prebiotics, Immunostimulants, and Phytogenics), Form (Dry and Liquid), Source (Microbial and Plant-Based), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Aquaculture |

| Poultry |

| Ruminant |

| Swine |

| Others |

| Probiotics |

| Prebiotics |

| Immunostimulants |

| Phytogenics |

| Dry |

| Liquid |

| Microbial |

| Plant-Based |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Livestock | Aquaculture | |

| Poultry | ||

| Ruminant | ||

| Swine | ||

| Others | ||

| By Additive | Probiotics | |

| Prebiotics | ||

| Immunostimulants | ||

| Phytogenics | ||

| By Form | Dry | |

| Liquid | ||

| By Source | Microbial | |

| Plant-Based | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the animal intestinal health market?

The sector is valued at USD 5.68 billion in 2026 and is projected to climb to USD 8.38 billion by 2031.

Which livestock category spends the most on gut health solutions?

Swine operations lead, representing 29.45% of global revenue in 2025.

Which additive type is growing the fastest?

Phytogenic compounds are expanding at a 9.89% CAGR through 2031.

Why is Asia-Pacific the fastest-growing region?

Rapid expansion of aquaculture and rising consumer demand for protein push the regional CAGR to 9.54%.

How are AI tools changing gut health management?

Machine-learning platforms match additive blends to specific microbiome profiles, cutting additive costs by up to 20% while improving consistency.

What level of market concentration exists among suppliers?

The market scores 6 on a 1–10 scale, indicating moderate concentration with room for disruptive entrants.