Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 60.78 Billion |

| Market Size (2031) | USD 80 Billion |

| Growth Rate (2026 - 2031) | 5.65% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Real Estate Market Analysis by Mordor Intelligence

The Thailand real estate market size is estimated at USD 60.78 billion in 2026 and is expected to reach USD 80.00 billion by 2031, growing at a 5.65% CAGR during 2026 to 2031. The 2026 inflection reflects pressure from weak mid-income purchasing power, high household debt, and tighter underwriting, while public infrastructure projects, targeted government stimulus, and foreign capital in luxury and logistics help sustain activity in select corridors. Developers listed in Bangkok are shifting toward logistics and industrial assets within the Eastern Economic Corridor, where demand links to e-commerce and data center investments. Government measures such as fee cuts on property transfers and loan-to-value relaxations are intended to clear transactions at the margin, even as banks maintain prudent credit standards due to balance sheet risks. Monetary easing since August 2025 and mass transit additions around the MRT Orange Line are expected to improve sentiment and stabilize transfer volumes into mid-2026 as project timelines progress.[1]https://www.bot.or.th/th/coverpage.html

Key Report Takeaways

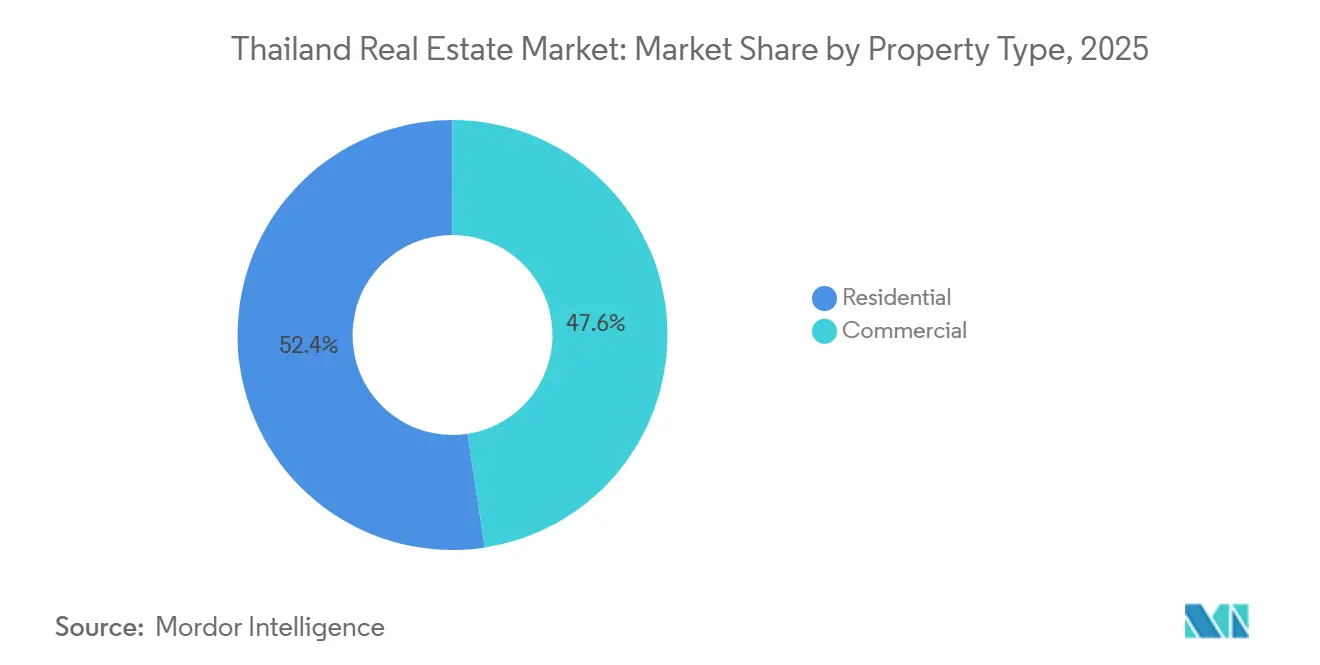

- By property type, residential accounted for 52.4% revenue share in 2025, while commercial is projected to expand at a 6.22% CAGR through 2031.

- By business model, sales held a 70.2% share in 2025, while rentals are forecast to grow at a 6.41% CAGR through 2031.

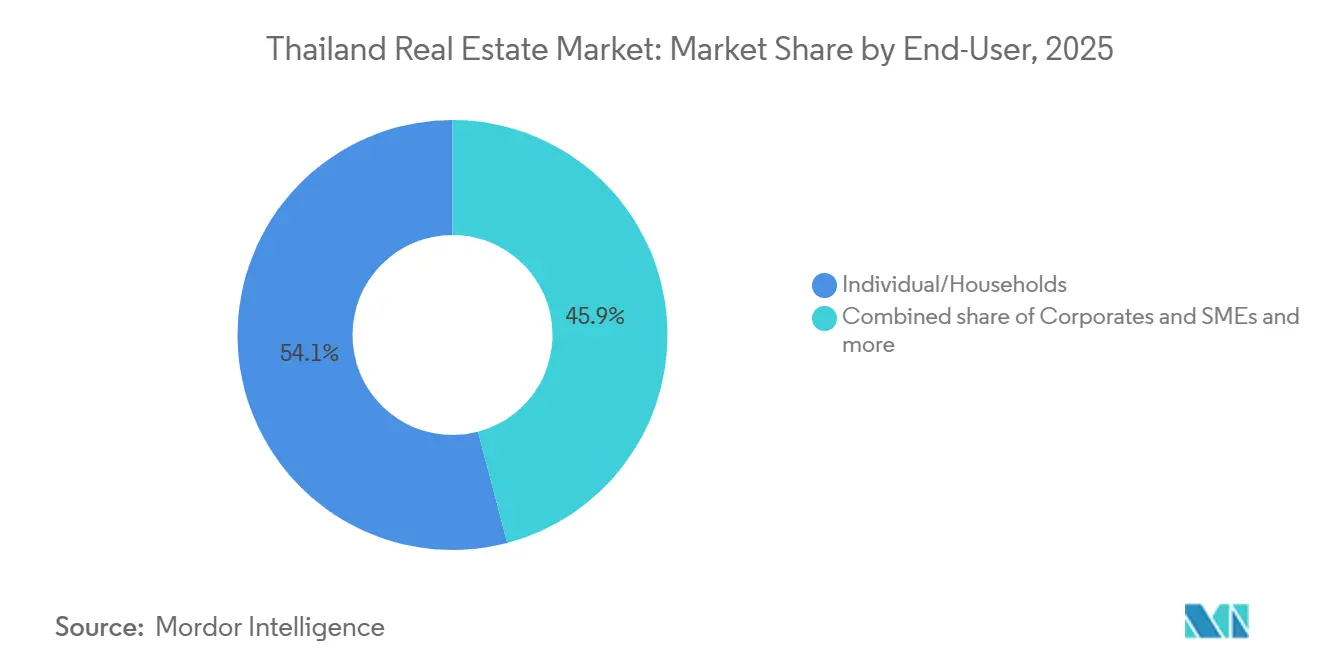

- By end-user, individuals and households captured a 54.1% share in 2025, while corporates and SMEs are projected to record a 6.30% CAGR through 2031.

- By geography, Bangkok led with a 53.1% share in 2025, while Phuket is projected to grow at a 4.10% CAGR during 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Thailand Real Estate Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Transit expansion and infrastructure upgrades | +2.0% | Bangkok, Eastern Economic Corridor, regional cities | Long term (≥ 4 years) |

| E-commerce driven logistics demand | +1.7% | Eastern Economic Corridor core, Bangkok Metropolitan Region (Samut Prakan) | Medium term (2–4 years) |

| Government incentives and fee cuts | +1.3% | Nationwide, Bangkok-centric | Medium term (2–4 years) |

| Rising foreign buyer interest | +1.2% | Bangkok, Phuket, Pattaya, Chiang Mai | Medium term (2–4 years) |

| Large mixed-use schemes | +1.0% | Bangkok, CBD, Phuket | Medium term (2–4 years) |

| Limited premium supply and higher build costs | +1.0% | Bangkok, CBD, Phuket | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Transit expansion and infrastructure upgrades

Transit additions are shaping how demand forms across Bangkok’s core and periphery in 2026. New mass-transit lines improve accessibility and are expected to lift values and absorption near stations as construction progresses in the 2026 to 2027 window. The Bangkok to Nakhon Ratchasima high-speed rail, slated to open in 2028, also supports land assembly and planning activity in secondary cities that benefit from future connectivity. Early data on the Pink Line’s launch showed a burst of transfers followed by softer absorption in mid-priced suburban condominiums, which signals that station proximity alone does not guarantee sustained take-up without strong job anchors nearby. Developers are increasing focus on transit-proximate, lower-rise projects priced below THB 10 million (USD 285,714), targeting owner-occupiers who value safety, access, and resilience. This selective transit-oriented strategy favors corridors that pair mobility gains with employment density and livability improvements, rather than transit alignment alone.[2]https://www.nationthailand.com/

Government incentives and fee cuts

Fiscal and macroprudential steps are supporting transactions, but cannot fully offset household debt constraints. Authorities reduced transfer and mortgage registration fees to 0.01% for homes priced up to THB 7 million (USD 200,000), which is expected to lift near-term transaction counts but does not resolve credit screening hurdles for mid-income buyers. The loan-to-value relaxation to 100% for second homes priced below THB 10 million (USD 285,714) was designed to stimulate upper mid-market demand, yet bank underwriting remains cautious in segments exposed to high rejection rates. Developers postponed some planned projects in 2025 as presales fell short of targets, while luxury units maintained stronger absorption, underscoring liquidity concentration at the top end. Subsidized housing programs expand access and create price reference points, but private developers still face margin pressure in overlapping catchments. New responsible lending rules effective January 2025, including preemptive debt restructuring guidelines, acknowledge that fee cuts alone will not revive mass-market demand without household balance sheet repair.[3]https://www.siam-legal.com/

Rising foreign buyer interest

Foreign buying has shifted toward lifestyle-led ownership in tourism and business nodes, replacing pre-pandemic speculative activity. Phuket registered a year-over-year rise in foreign condominium transfers in 2025 despite variability in tourist arrivals, which points to longer-stay usage and family-oriented purchases. Bangkok submarkets such as Sukhumvit and Sathorn continue to draw cross-border demand, with branded residences appealing to buyers who value professional property management and asset quality. Regulators tightened anti-money-laundering disclosures for higher value transactions in late 2025, which improves transparency and should support investor confidence in premium segments. The decision in September 2025 to shelve an extended leasehold tenure proposal and to maintain the current regime of freehold for condominiums continues to influence buyer preference toward freehold assets. This pattern supports long-duration demand in select urban and resort markets and concentrates activity within internationally familiar ownership frameworks.

Logistics Demand Absorbing EEC Industrial Land Faster Than Residential Recovers

Warehouse and logistics assets are outpacing residential recovery in 2026. Occupancy remains high even as new supply enters, helped by e-commerce growth and network expansion in fulfillment and last mile logistics. The Eastern Economic Corridor concentrates the majority of future warehouse pipeline and is benefitting from data center investment, which lifts industrial land values and REIT demand. Developers historically oriented to residential are redirecting capital toward built-to-suit warehouses as access to institutional capital and REIT structures supports stable yields. Leading industrial REITs have maintained strong occupancy and competitive distribution yields, reinforcing a financing edge relative to housing-focused structures. Power transmission capacity is an execution risk in parts of the EEC, and authorities are prioritizing approvals and upgrades to sustain the data center and manufacturing pipeline.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Weak mid-income housing demand amid high debt | -1.5% | Nationwide, suburban Bangkok | Short term (≤ 2 years) |

| Urban condo oversupply | -1.0% | Bangkok Metropolitan Region | Medium term (2-4 years) |

| Broader economic uncertainty and inflation | -0.7% | Nationwide | Short term (≤ 2 years) |

| Planning delays and zoning issues | -0.4% | Bangkok and secondary cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Weak mid-income housing demand amid high debt

Household debt levels and prudent underwriting are suppressing approval rates for homes priced below THB 3 million (USD 85,714). Rising non-performing and special mention loans have led banks to formalize affordability testing and residual income thresholds under responsible lending rules introduced in January 2025. High rejection rates for lower-priced homes raise inventory carry and discount pressure for developers focused on mid-income segments. Developers have experimented with rent-to-own and seller financing to convert the pipeline, which shifts credit risk back to corporate balance sheets. New housing launches were curtailed in 2025 as firms recalibrated exposure to the most credit-constrained demand pools. Structural affordability will remain a constraint until income growth and household deleveraging improve debt service metrics in this price band.

Urban condo oversupply

Urban condo inventory remains elevated in some suburban corridors, which slows absorption and flattens pricing during 2026. Developers who front-loaded launches during earlier transit announcements found demand concentrated in core CBD locations rather than fringe stations with weaker job proximity. Investors have become more selective on project quality, management, and long-run rental prospects in these corridors. Developers responded by reducing new launch exposure and prioritizing formats with more predictable take-up, including low-rise housing and build-to-rent near employment nodes. The oversupply overhang will take time to resolve through a combination of moderated launches, unit reconfiguration, and incremental owner-occupier absorption aligned with new transit and job growth.

Segment Analysis

By Property Type: Commercial Assets Outpacing Residential as Data Centers Reshape Industrial Estates

Residential properties were the largest by revenue with a 52.4% share in 2025, indicating the balance of consumer demand within the Thailand real estate market. Commercial assets are advancing at the fastest 6.22% CAGR during 2026 to 2031 as data center approvals and logistics expansion in the EEC attract new capital allocations. The Board of Investment cleared a wave of digital infrastructure and related investments in 2024 to 2025, including multi-billion-dollar commitments that anchor industrial estate leasing and power procurement strategies. This cycle raises the importance of power availability and zoning near hyperscale sites and has prompted listed developers to build warehousing capacity consistent with institutional-grade tenancy. Apartments and condominiums still hold the largest share within residential, while detached houses are benefiting from buyer preference for more space and safety in outer Bangkok zones.

Hospitality shows steady recovery on the back of tourism, with operators emphasizing asset enhancements and mixed-use integration to improve earnings durability. Office fundamentals are mixed in 2026 as Grade A vacancy remains elevated during a flight to quality, with ESG-certified towers gaining relative strength while secondary assets deploy concessions and upgrades. Retail assets in prime locations continue to attract tenants, though e-commerce competition keeps pressure on formats that do not provide experiential value. Logistics warehouse occupancy and rents are supported by e-commerce and cold chain requirements, with REIT demand providing additional liquidity and development pipeline certainty. Against this backdrop, commercial momentum is expected to remain the outlier for the Thailand real estate market through 2031 based on anchor tenant demand and financing models suited to long leases.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Business Model: Rental Operations Gaining as Generation Rent Emerges

Sales accounted for 70.2% in 2025, reflecting entrenched ownership patterns in value terms across the Thailand real estate market. Rentals are growing faster at a 6.41% CAGR through 2031 due to younger cohorts that prefer flexibility, stricter mortgage screening, and steady demand from expatriates and remote workers. Surveys in 2025 indicated a clear tilt by Gen Z and Gen Y toward leasing, which supports the buy-to-rent pipeline and the professionalization of property management. In prime Bangkok locations, rental inflation outpaced purchase price gains in parts of 2025, which helped stabilize yields for well-located units. These patterns are consolidating a durable renter base near mass transit, job hubs, and international schools, and they reinforce multi-format strategies that blend serviced apartments with branded residence management.

Institutional structures reinforce this shift. Industrial REITs such as FPT Industrial REIT maintained 90.6% occupancy in FY2025 and delivered competitive distributions, which underpins new warehouse development by listed sponsors. SET rule changes that reduced barriers to REIT formation have expanded monetization paths for mid-tier developers, aligning with a greater share of recurring income in the corporate mix. Developers are testing rent-to-own to convert unqualified buyers over multi-year horizons, which could broaden eventual ownership for households outside bank credit boxes. This evolution points to a more balanced Thailand real estate industry structure by 2031, in which sales-led models coexist with scalable rental platforms that can be securitized.

By End-user: Corporates Driving Fastest Growth Through EEC Manufacturing Relocations

Individuals and households represented 54.1% of end-user demand in 2025 and continue to anchor residential activity in the Thailand real estate market. Corporates and SMEs are the fastest-growing cohort at a 6.30% CAGR, driven by relocations under China Plus One strategies and a rising tally of BOI applications in electronics, EVs, and semiconductors. FDI commitments in manufacturing and digital infrastructure are spurring demand for worker dormitories, serviced apartments, and built-to-suit facilities that cluster near EEC estates. Office leasing also reflects corporate consolidation into higher-quality assets with stronger sustainability credentials and building systems. This corporate-led demand adds a stable layer to the Thailand real estate market through long leases and capex plans linked to production timelines.

Within individuals and households, high-net-worth buyers sustained activity in the luxury segments, while mid-income cohorts faced bank screening hurdles that delayed transfers and capped presales momentum in 2025. Large developers allocated new project pipelines toward higher price points and more resilient locations where take-up has proven more consistent. Public sector programs, including subsidized housing, help at the margin and guide private supply into designated corridors, particularly near future transit. This mix keeps corporates as the main incremental growth engine across EEC-linked assets while households continue to determine absolute volume in core residential formats.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Bangkok led in 2025 with 53.1% of the national value, underscoring its central role in the Thailand real estate market size, and it is expected to remain the anchor while growth diffuses to select corridors. Absorption patterns show a split between premium CBD inventories and mid-tier suburban condominiums, with luxury units supported by brand, service, and global buyer familiarity. Grade A office vacancy stayed high into late 2025, although top-tier ESG-certified buildings in core nodes continue to outperform with better occupancy and pricing power. Upcoming mass transit extensions, including the Orange Line and the Dark Red Line extension, are expected to lift nearby land values and support a measured pickup in launches and transfers through 2026 to 2027. The city planning revision expected in 2027 is likely to unlock density in targeted zones and encourage mixed-use development around stations.

Phuket is the fastest-growing major city with a projected 4.10% CAGR during 2026 to 2031 on the back of sustained foreign interest and an upgraded infrastructure base. Foreign condominium transfers increased in 2025, with purchases oriented to longer stays and professionally managed projects. Villa markets in key subdistricts remain supported by limited titled land, enhanced connectivity, and resident-led spending that supports premium services. Hotel and resort pipelines continue to expand, which requires careful pacing to avoid near-term occupancy pressure during seasonal and origin-market swings. Phuket’s positioning complements Bangkok by offering a resort-led alternative that attracts extended-stay buyers and families who value service and lifestyle over purely investment-led returns.

The EEC provinces anchor industrial and logistics growth, with patterns that spill into residential and rental housing near estates and data centers. Pattaya and Chonburi benefit from proximity to Bangkok and a planned high-speed rail that will shorten travel times, while demand in Hua Hin and other coastal towns reflects lifestyle and weekend-home preferences. Chiang Mai continues to serve a mix of retirees and remote professionals with more modest price growth compared with coastal or Bangkok locations. Regulatory rules that cap foreign freehold ownership in condominiums and the shelving of longer leasehold proposals continue to shape geographic flows of foreign capital toward freehold units in approved zones. These regional dynamics together define how the Thailand real estate industry balances its core capital region with targeted growth poles along the eastern seaboard and tourism-led islands.

Competitive Landscape

The Thailand real estate market is moderately concentrated. The five largest residential developers together account for a little more than half of active project value, while industrial logistics and hospitality are led by specialized operators and listed REIT sponsors. Competitive intensity in mid-income housing has compressed margins to single digits for several listed developers as sales costs and financing burdens rose relative to revenue. In response, balance sheets are tilting toward logistics, light industrial, and recurring-income platforms that align with institutional capital and REIT structures. Luxury-branded residences that command pricing premiums serve as another hedge for developers with established marketing and property management capabilities. This set of strategies helps mitigate volatility in mass-market sales while preserving exposure to growth nodes and resilient tenancy.

Regulatory recalibration continues to influence competitive positions in 2026. Responsible lending rules raise the cost and time to resolve non-performing exposures, which weighs more on smaller developers without internal workout capabilities. New sustainability disclosure expectations for listed companies heighten reporting costs and governance requirements, further encouraging scale and process investment. The REIT framework remains a core enabler for logistics and hospitality sponsors to recycle capital and grow portfolios under professional management. Corporate strategies now converge on a mix of recurring income assets, targeted luxury development, and selective overseas diversification to balance domestic market cyclicality. These combined moves are shaping a Thailand real estate market that is more institutionally oriented and diversified by 2031.

Thailand Real Estate Industry Leaders

AP (Thailand) Public Company Limited

Sansiri PCL

Supalai PCL

Land and Houses PCL

SC Asset Corporation PCL

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2026: TikTok's THB 126.8 billion data center mega-investment (largest single commitment).

- November 2025: BOI approval of 4 data centers totaling USD 3.1 billion + fast-track licenses for USD 9.2 billion stalled projects.

- August 2025: KS Hotels & Resorts' USD 128.8M Australian acquisition + BTS Group's USD 78.9M Czech acquisition (outbound M&A diversification).

- August 2025: FTREIT's THB 1.92 billion industrial property acquisition across 3 provinces (institutional capital into logistics)

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Thailand real estate market as the aggregate value of completed residential, commercial, industrial, and land transactions, both sales and long-term rentals, recorded across the kingdom's formal registry system and reputable brokerage channels during a calendar year. Property development activities still under construction are tracked as leading indicators but are not counted in annual market value.

(Scope exclusion: pure construction-services revenue and short-stay hospitality turnovers are outside this valuation.)

Segmentation Overview

- By Property Type

- Residential

- Apartments & Condominiums

- Villas & Landed Houses

- Commercial

- Office

- Retail

- Logistics

- Others

- Residential

- By End-user

- Individuals / Households

- Corporates & SMEs

- Others

- By Major Cities

- Bangkok

- Phuket

- Pattaya

- Chiang Mai

- Rest of Thailand

Detailed Research Methodology and Data Validation

Primary Research

To refine assumptions, our team interviewed developers active in Bangkok and the Eastern Economic Corridor, brokerage heads handling foreign buyer cohorts in Phuket and Pattaya, industrial-estate managers, and institutional investors allocating to Thai REITs. Feedback on average selling prices, lease terms, vacancy swings, and pipeline intentions helped validate desk findings and close data gaps.

Desk Research

Mordor analysts began with authoritative open data sets such as the Bank of Thailand's mortgage statistics, the Real Estate Information Center's deed-transfer filings, Department of Lands transaction ledgers, National Economic and Social Development Council GDP tables, and UN DESA urbanization series. These were blended with company filings, SET disclosures from listed developers, housing price indices published by the Government Housing Bank, and credible press archives. Paid repositories like D&B Hoovers and Dow Jones Factiva were tapped to cross-check developer revenue splits and deal announcements. The sources cited illustrate the breadth of inputs; numerous additional references were assessed to complete evidence gathering.

Market-Sizing & Forecasting

A top-down model starts with national deed-transfer value, adjusts for recorded mortgages to capture cash sales, and layers in rental income estimated from occupancy and average rents. Results are then balanced against bottom-up cross-checks such as sampled developer revenues and condominium unit launches multiplied by achieved ASPs. Key variables guiding the model include urban population growth, tourist arrivals, average household disposable income, policy-driven fee incentives, and benchmark lending rates. Multivariate regression links these drivers to historical market value, and the fitted equation projects through 2030, while scenario analysis tests interest-rate and tourism shocks. Where bottom-up samples under-represent secondary cities, interpolation from land-office records bridges the gap.

Data Validation & Update Cycle

Initial outputs pass a variance screen against independent metrics, GDP share, construction GDP, and listed-developer turnovers. Material anomalies trigger a second analyst review before sign-off. The Thailand real estate dataset refreshes every twelve months; interim updates occur when policy shifts, natural disasters, or large corporate defaults materially move the market. A final pre-publication sweep ensures clients receive the latest view.

Why Our Thailand Real Estate Baseline Earns Trust

Published estimates often differ because firms pick disparate property types, treat rental flows inconsistently, or freeze exchange rates at varying points.

By anchoring values to notarized deed data and layering rentals only where tenure exceeds twelve months, Mordor's base case avoids double counting and currency drift. Other studies may merge construction spend or report aspirational pipeline values, creating inflated or understated totals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 58.78 B (2025) | Mordor Intelligence | - |

| USD 29.54 B (2024) | Global Consultancy A | Omits industrial land transfers and converts THB at average 2023 FX, understating growth |

| USD 54.90 B (2025) | Regional Consultancy B | Includes only primary sales, excludes long-term rentals, and applies uniform ASP across provinces |

| USD 95 B (2024) | Industry Association C | Adds construction output and hotel turnovers, inflating total market value |

In summary, the disciplined scope selection, dual-track modeling, and annual refresh cadence mean Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can trace to clear variables and replicate with confidence.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the Thailand real estate market size and growth outlook through 2031?

The Thailand real estate market size is USD 60.78 billion in 2026 and is projected to reach USD 80.00 billion by 2031 at a 5.65% CAGR, supported by infrastructure, selective foreign demand, and a pivot to logistics and industrial assets.

Which property type and business model are growing fastest in Thailand’s real estate?

Commercial assets are advancing at the fastest 6.22% CAGR, while rentals are the fastest-growing business model at a 6.41% CAGR as leasing gains traction near transit and job hubs.

How is policy shaping buyer activity in the Thailand real estate market?

Fee cuts on transfers and mortgages and LTV relaxations are lifting transactions at the margin, while responsible lending rules require affordability checks and preemptive restructuring, which keeps credit tight for mid-income buyers in 2026.

Where is geographic growth strongest across Thailand?

Bangkok leads by value with 53.1% in 2025, while Phuket is the fastest-growing major city in 2026 to 2031 given sustained foreign demand and infrastructure upgrades.

What is driving logistics and industrial real estate in Thailand?

E-commerce growth, hyperscale data center approvals, and EEC-focused investment are lifting warehouse occupancy and rents, supported by REIT funding and long leases with multinational tenants.

How are developers adjusting strategies in 2026?

Leading developers are tilting toward recurring income from logistics and mixed-use assets, expanding branded residences at the top end, and using REITs and ESG-linked financing to optimize cost of capital and portfolio resilience.