Analog Integrated Circuit Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

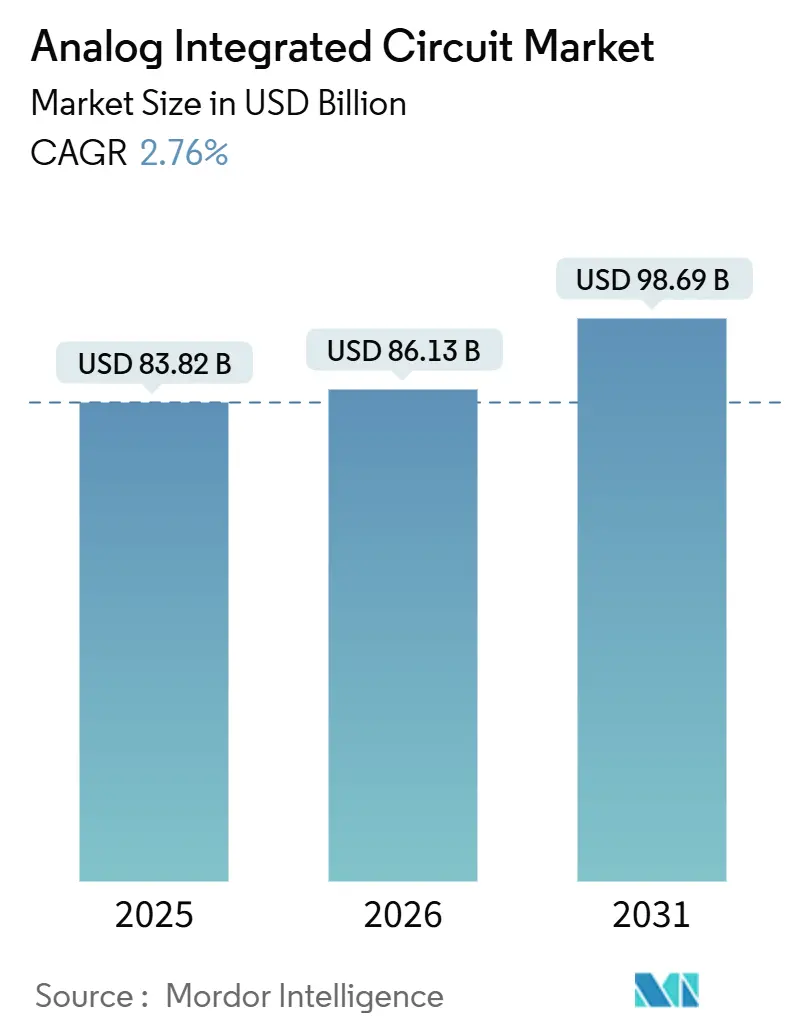

| Market Size (2026) | USD 86.13 Billion |

| Market Size (2031) | USD 98.69 Billion |

| Growth Rate (2026 - 2031) | 2.76% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analog Integrated Circuit Market Analysis by Mordor Intelligence

The analog integrated circuit market size is projected to expand from USD 83.82 billion in 2025 and USD 86.13 billion in 2026 to USD 98.69 billion by 2031, registering a 2.76% CAGR between 2026 and 2031. Electrification in transportation, densification of 5G infrastructure, and edge-AI adoption are adding more precision power-management and RF content to every device even though unit volumes in legacy consumer electronics have flattened. The analog supply base is pivoting from catalog products to application-specific devices that integrate several analog blocks on a single die, reducing system bill-of-material and locking-in design wins for up to a decade. Vertically integrated manufacturers are converting 200 mm fabs to 300 mm wafers to realize 40% lower die cost, a move that is reshaping cost curves and favoring high-volume players. Competitive pressure from Chinese mixed-signal foundries is compressing prices in commoditized low-voltage power and audio, prompting incumbents to allocate more capital to wide-bandgap power devices and high-value healthcare and aerospace sockets.

Key Report Takeaways

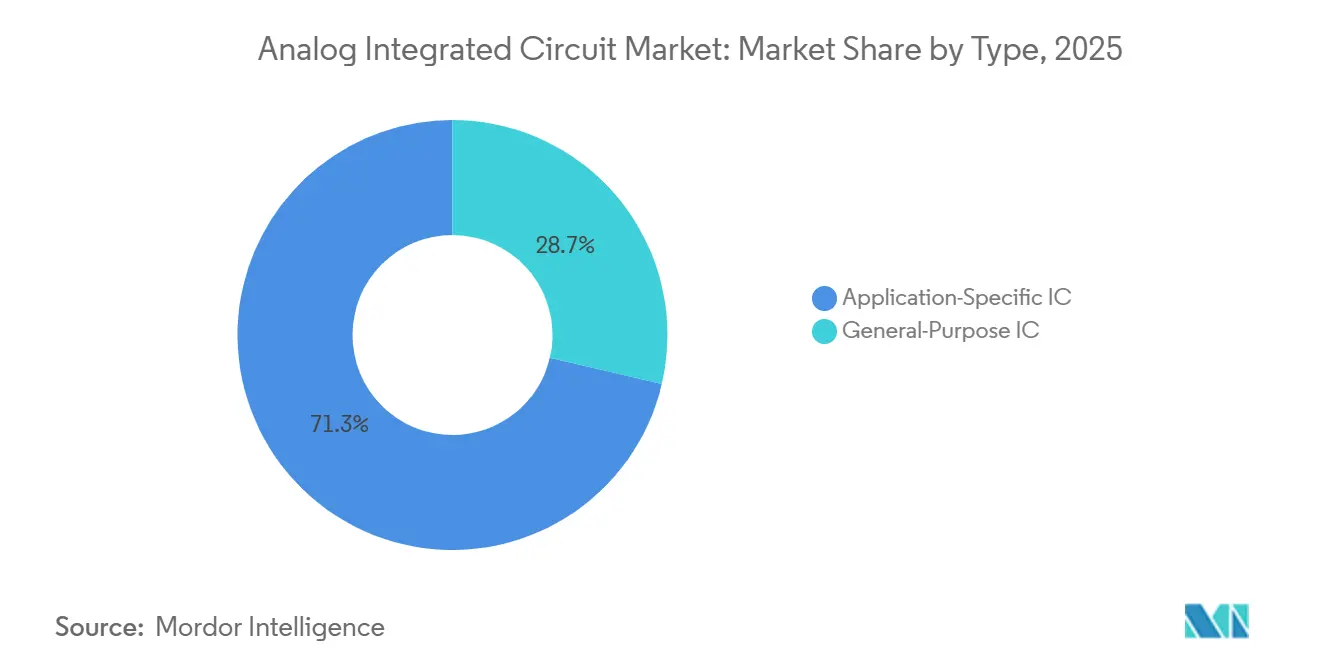

- By type, application-specific ICs led with 71.34% revenue share in 2025 and are projected to advance at a 3.11% CAGR through 2031.

- By technology node, above-65 nm processes held 49.67% of production in 2025, while below-28 nm devices are forecast to grow at a 3.56% CAGR over the same period.

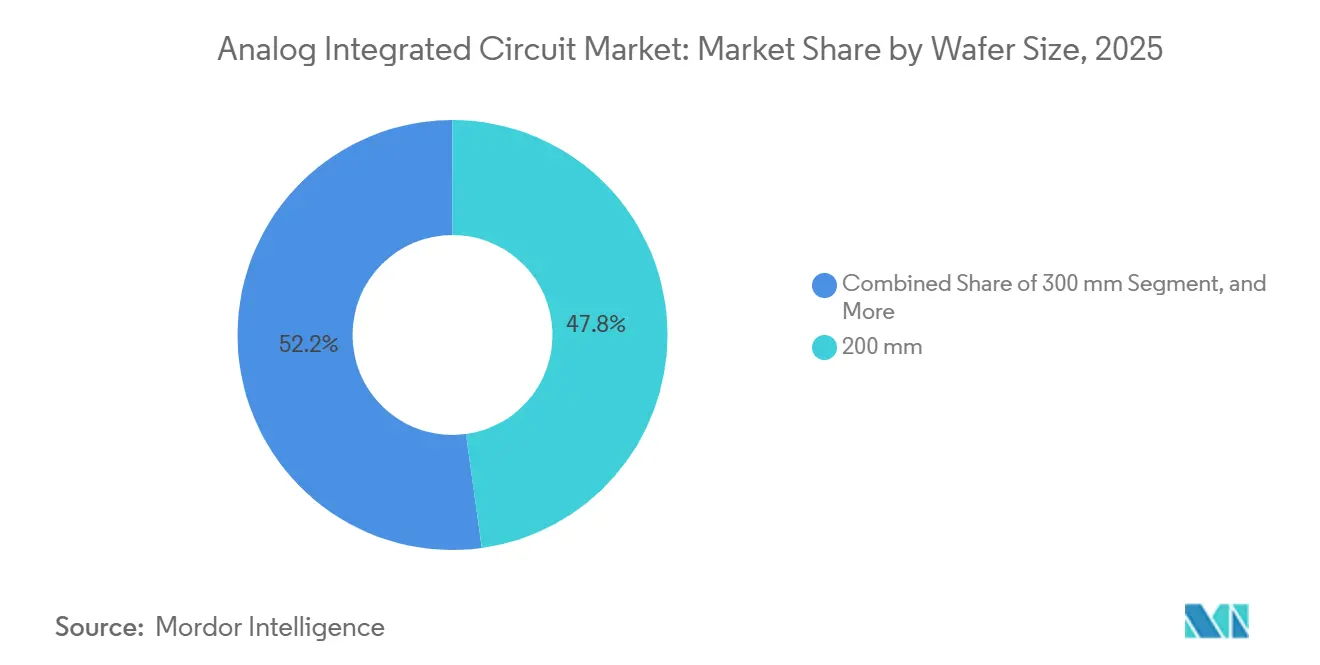

- By wafer size, 200 mm capacity commanded 47.83% of the base in 2025, whereas 300 mm output is set to rise at a 3.34% CAGR to 2031.

- By end-use application, automotive accounted for 28.64% share of the analog integrated circuit market size in 2025, and healthcare is on track to expand at a 3.73% CAGR through 2031.

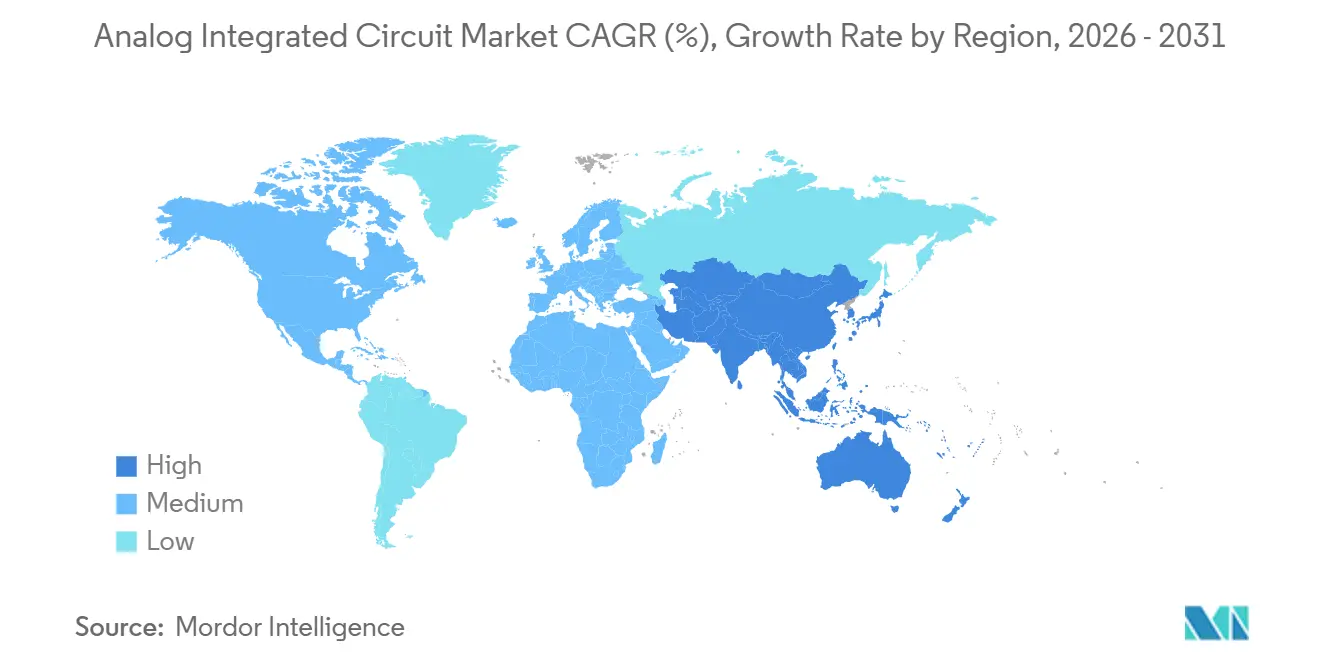

- By geography, Asia-Pacific dominated with 46.91% of 2025 demand, while the Middle East is expected to register the fastest 3.79% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Analog Integrated Circuit Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating 5G and 6G RF Front-End Content | +0.8% | Asia-Pacific and North America | Medium term (2-4 years) |

| Rapid EV Power-Train Electrification | +0.7% | Europe, China, North America | Long term (≥ 4 years) |

| Industrial Automation Ramp-Up | +0.5% | Europe and Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Edge-AI Inference Power-Management | +0.4% | North America and Asia-Pacific | Short term (≤ 2 years) |

| Next-Gen Satellite Constellations | +0.2% | North America and Europe | Long term (≥ 4 years) |

| Smart-Meter Retrofit Programs | +0.2% | India, Southeast Asia, Brazil, Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating 5G and 6G RF Front-End Content per Handset

Fifth-generation smartphones integrate three to five times more RF analog than 4G models because millimeter-wave and sub-6 GHz bands require separate high-linearity transmit-receive chains. Premium handsets in 2025 carried USD 25 of RF front-end content, up from USD 18 in 2023, with discrete envelope trackers and low-noise amplifiers spanning 24 GHz to 39 GHz bands.[1]Skyworks Solutions, “FY 2025 Annual Report,” skyworksinc.com Gallium nitride power amplifiers captured 40% of 5G base-station sockets by leveraging 50% power-added efficiency at 3.5 GHz. Early 6G consortia are prototyping sub-terahertz radios that will need cryogenic LNAs, opening entirely new design-in cycles for ultra-wideband analog converters. Spectrum unlocked at 12.7 GHz in 2024 accelerated North American deployments, cementing a multiyear demand tail for high-linearity RF blocks.

Rapid EV Power-Train Electrification Boosting High-Voltage Analog Demand

A modern battery pack installs 15-20 high-voltage analog ICs ranging from isolated current sensors to SiC gate drivers. Over 10 million EiceDRIVER gate drivers shipped in 2025, securing 99.2% switching efficiency in 400 V and 800 V inverters.[2]Infineon Technologies, “EiceDRIVER Shipments,” infineon.com New battery monitors integrate 16-channel simultaneous sampling and ASIL-D diagnostics, slicing BOM costs by 25% versus discrete alternatives. The European Euro 7 rules, effective July 2025, require real-time impedance spectroscopy and guarantee incremental analog sockets for at least 5 years. Even where EV unit growth moderates, analog content per vehicle keeps climbing, sustaining revenue expansion.

Industrial Automation Ramp-Up (Industry 4.0, IIoT)

Factory retrofits add precision converters, isolated power rails, and single-pair Ethernet transceivers that translate physical variables into digitized data streams. A motor-control platform introduced in 2024 cut discrete counts by 60%, slashing panel size in programmable logic controllers. Eight-channel sigma-delta converters achieve 110 dB of SNR, enabling predictive-maintenance analytics to flag bearing wear 6 months earlier than 16-bit predecessors. Germany earmarked EUR 500 million (USD 565 million) in 2025 to subsidize SME upgrades, directly stimulating demand for isolated analog channels.[3]Federal Ministry for Economic Affairs and Climate Action, “Industry 4.0 Subsidy Program,” bmwk.de The IEC 61131-9 standard, finalized in 2024, unified analog I/O over single-pair Ethernet, simplifying wiring and creating design-in incentives for robust ±60 V transceivers.

Edge-AI Inference Requiring Precision Power-Management

Always-on vision and speech recognition at the edge demands dynamic voltage scaling within microseconds and efficiency above 95%. A power-management unit released in 2024 maintained that efficiency across a 10-to-1 load range, allowing wearables to idle below 10 mW. Embedded switched-capacitor regulators harvest charge during neural accelerator idle cycles, extending battery life by 40% in health trackers. Renesas doubled its edge-AI power revenue year over year on smart-camera wins. The CHIPS and Science Act funneled USD 200 million into ultralow-power analog front-end research, anchoring a public-private ecosystem committed to analog-in-memory computing.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Design Complexity for Sub-28 nm Analog | -0.6% | North America and Europe | Short term (≤ 2 years) |

| Cyclical Consumer-Electronics Demand | -0.5% | Asia-Pacific consumer hubs | Short term (≤ 2 years) |

| Analog Talent Shortage | -0.3% | North America and Europe | Long term (≥ 4 years) |

| GaN / SiC Module Integration | -0.3% | Automotive and industrial power markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Design Complexity and Verification Cost for Sub-28 nm Analog

Electromagnetic simulation, parasitic extraction, and Monte Carlo analysis now consume up to half of total design time, driving non-recurring engineering beyond USD 10 million for a single analog IP block. EDA revenue from analog verification jumped 22% in 2025, underscoring this escalating burden. Even with an AI-assisted layout that promises 30% faster closure, automotive-grade mixed-signal ASICs still require 18-24 month cycles. An IEEE study showed a 15% drop in transistors-per-engineer productivity between 2020 and 2024, with advanced-node analog concentrated within a handful of cash-rich IDMs.

Cyclical Consumer-Electronics Demand Volatility

Smartphone and PC shipments contracted 8% in 2025, eroding demand for audio codecs, display drivers, and chargers that together represent roughly a quarter of analog revenue. One leading audio IC vendor saw 12% year-over-year revenue erosion due to OEMs delaying product cycles. Larger suppliers cushioned the impact by accelerating automotive and industrial diversification, but second-tier players reliant on handsets endured margin compression. The volatility underscores why long-lifecycle automotive and factory sockets are strategic hedges despite their slower qualification ramps.

Segment Analysis

By Type: Application-Specific Solutions Capture Majority Share

Application-specific ICs held 71.34% of the market share in 2025, and the analog integrated circuit market size tied to these devices is projected to rise at a 3.11% CAGR through 2031. Demand stems from integrated power management, signal conditioning, and RF blocks that shrink board area while meeting OEM functional-safety targets. Automotive radar, battery monitoring, and infotainment audio each added double-digit revenue in 2025, proving that tight co-design with system software extends product lifecycles and locks in multiyear volume. Communication infrastructure contributed 35% of application-specific revenue as 5G base stations and Wi-Fi 7 routers carried discrete transmit-receive chains that catalog parts cannot match for linearity.

General-purpose offerings, including interface ICs, regulators, converters, and amplifiers, retained a 28.66% share but are growing just 2.1% as customers migrate toward optimized SoC companions. Industrial and medical designers still favor catalog operational amplifiers and precision references for long-life equipment, sustaining mid-single-digit revenue growth in those subsegments. Power-management ICs account for 45% of the general-purpose mix, yet commoditization invites price undercutting from pin-compatible Chinese suppliers that quote discounts of 30% to 40%. Stand-alone data converters remain profitable when 24-bit to 32-bit resolution is mandatory for test instrumentation, but many 12-bit to 16-bit devices are now integrated into digital ASICs. This divergence pushes incumbents to concentrate new product introductions on differentiated application-specific platforms while pruning low-margin catalog lines.

By Technology Node: Mature Processes Dominate, Advanced Nodes Accelerate

Above-65 nm processes accounted for 49.67% of 2025 production, delivering the largest slice of the analog integrated circuit market share, as high-voltage power rails and RF front ends require thick gate oxides and high breakdown voltages. Vertical integration at 130 nm to 180 nm achieves 40% gross margins through high tool utilization and proven automotive quality flows. The 40 nm to 65 nm band accounted for 28% of output, balancing mixed-signal density with manageable verification costs for radar transceivers and precision converters.

Below-28 nm designs are the fastest lane, with the analog integrated circuit market for this node forecast to grow at a 3.56% CAGR through 2031. A 22 nm FD-SOI radar platform doubled revenue year over year, while 16 nm FinFET analogs trim power by 20% versus 28 nm planar, drawing smartphone power-management and biosensor wins. However, sub-28 nm verification inflates non-recurring engineering above USD 10 million per IP block, concentrating activity inside cash-rich IDMs and top-tier fabless firms with leading-edge foundry access. Mid-tier suppliers remain anchored to mature nodes where capital intensity is lower, but pricing pressure is acute. The node bifurcation underscores how process choice is now as much a business decision as a technical one.

By Wafer Size: 200 mm Installed Base Meets Rising 300 mm Economics

Two-hundred-millimeter lines supplied 47.83% of 2025 capacity, making these fabs the largest wafer-based slice of the analog integrated circuit market share, as they host proven power and RF technologies. Several suppliers sustain 65% gross margins by pairing high-mix manufacturing with long product lifetimes that exceed 15 years. The 150 mm niche, 8% of capacity, remains relevant for ultra-high-voltage and radiation-hardened devices where larger wafers offer no advantage.

The 300 mm segment reached 44.17% in 2025 and is set to grow at a 3.34% CAGR, making it the fastest-growing wafer size contributor to gains in the analog integrated circuit market. Converting legacy 200 mm tools can cut die cost by as much as 40% while doubling output per cycle, a combination that strengthens price leadership for vertically integrated vendors. One leader’s USD 11 billion program aims to shift 70% of analog output to 300 mm by 2030, forcing competitors to accelerate conversion roadmaps or risk margin erosion. Fabless firms without firm 300 mm foundry allocations face tighter wafer access during demand peaks, potentially limiting share capture in fast-moving automotive and telecom sockets. Consequently, the wafer-diameter strategy has become a critical lever in corporate capital-allocation debates.

Note: Segment shares of all individual segments available upon report purchase

By End-Use Application: Automotive Leads, Healthcare Accelerates

Automotive electronics absorbed 28.64% of the 2025 analog integrated circuit market size, buoyed by battery packs that carry 15-20 high-voltage ICs and ADAS modules that add USD 150–200 of analog content per vehicle. Silicon-carbide traction inverters operating at 800 V require isolated gate drivers and current sensors, thereby increasing dollar content even as global vehicle units plateau. Radar transceivers at 77 GHz and infotainment audio amplifiers round out incremental sockets, ensuring the segment remains the largest single end market through 2031.

Healthcare is the fastest-growing vertical, with a 3.73% CAGR forecast. Wearable biosensors now integrate 19-bit sigma-delta converters that consume sub-1 mA, enabling continuous SpO₂ and ECG measurements without daily charging, while portable ultrasound systems rely on multichannel analog front ends that combine beamforming with on-probe digitization. The U.S. FDA cleared 47 AI-enabled devices in 2025, most of which embed precision analog signal chains, and reimbursement updates are encouraging at-home diagnostic adoption. Industrial automation maintains a 24% share on the back of predictive-maintenance sensor nodes and isolated single-pair Ethernet transceivers, whereas telecommunications holds 22% thanks to 5G massive-MIMO RRUs and optical line cards. Consumer electronics slipped to 18% amid smartphone stagnation, illustrating why suppliers are reallocating R&D toward automotive safety and medical certification programs.

Geography Analysis

Asia-Pacific commanded 46.91% of the analog integrated circuit market share in 2025, powered by China’s electric vehicle capacity, Japan’s precision automotive sensor exports, and South Korea’s memory interface demand. High regional volumes translated into sustained wafer utilization, which kept average selling prices stable despite global softness in consumer devices. Regional governments continue to subsidize 300 mm analog fabs, a policy stance expected to keep the Asia-Pacific CAGR close to the overall analog integrated circuit market trajectory through 2031.

North America accounted for 24% of 2025 revenue, supported by edge-AI power management, 5G infrastructure rollouts, and aerospace programs that require radiation-hardened analog. Federal incentives are catalyzing new wafer starts, which in turn improve supply resilience for automotive and industrial customers across the United States and Canada. Europe captured 18% in 2025, but its growth rate sits modestly below the global average because EV sales have plateaued and industrial capital spending has slowed.

The Middle East is the fastest-growing region, with a projected 3.79% CAGR to 2031, driven by sovereign wealth investments in greenfield fabs and defense-grade electronics. South America accounted for 6% of 2025 demand and is leveraging large-scale smart-meter rollouts to boost near-term consumption of mixed-signal power devices. Africa contributed 5%, anchored by South African telecom upgrades and Egyptian industrial automation, yet both subregions remain sensitive to foreign exchange swings and infrastructure financing cycles.

Competitive Landscape

The five largest suppliers captured roughly 45% of the analog integrated circuit market revenue in 2025, yet no single company exceeded 12%, confirming a moderately concentrated environment. Vertically integrated leaders favor 300 mm conversion because a 40% reduction in die costs strengthens gross margins and raises barriers to fabless peers. One market leader that operates 14 fabs is targeting 70% of its output at 300 mm by 2030, a milestone that underscores its scale advantage.

Hybrid manufacturing models are flourishing. A prominent player in precision analog technology operates four internal 200 mm lines for diverse products, while outsourcing advanced mixed-signal ASICs to foundries specializing in 22 nm and 16 nm processes. In a strategic move, another leading supplier has allocated EUR 2.5 billion towards silicon-carbide and gallium-nitride capacities, aiming to boost its power portfolio share to 30% by 2027.

Strategic moves intensified in 2025. A Japanese IDM acquired an electronic design automation firm for USD 5.9 billion, linking PCB tools to its microcontroller ecosystem to lock customers into long design cycles. An American power specialist unveiled a platform that bundles intelligent power modules with embedded analog control, trimming discrete counts by 60% in industrial drives. Chinese mixed-signal foundries continue to price 30% below global peers for low-voltage audio and battery charging, forcing incumbents to prune catalog product lines and reallocate spending toward healthcare, aerospace, and automotive safety ICs.

Analog Integrated Circuit Industry Leaders

Texas Instruments Incorporated

STMicroelectronics N.V.

NXP Semiconductors N.V.

Skyworks Solutions Inc.

Qorvo Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Texas Instruments commenced production at its USD 11 billion Richardson, Texas 300 mm analog fab targeting 70% wafer conversion by 2030.

- December 2025: STMicroelectronics formed a EUR 5 billion joint venture with Sanan Optoelectronics to build a 200 mm silicon-carbide wafer fab in Chongqing, China.

- November 2025: Infineon Technologies invested USD 2.1 billion to expand its Kulim, Malaysia 200 mm facility, adding 30,000 wafer starts per month for automotive gate drivers.

- October 2025: Analog Devices launched the MAX32664D biosensor hub with an integrated 19-bit analog front end and embedded ML accelerator for wearables.

Global Analog Integrated Circuit Market Report Scope

The Analog Integrated Circuit Market Report is Segmented by Type (General-Purpose IC, and Application-Specific IC), Technology Node (Above 65 nm, 40-65 nm, 28-40 nm, Below 28 nm), Wafer Size (150 mm, 200 mm, 300 mm), End-Use Application (Automotive, Industrial, Consumer Electronics, Telecommunications, Healthcare), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| General-Purpose IC | Interface | |

| Power Management | ||

| Signal Conversion | ||

| Amplifiers / Comparators | ||

| Application-Specific IC | Consumer | Audio / Video |

| Digital Cameras and Camcorders | ||

| Automotive | Infotainment | |

| Advanced Driver-Assistance Systems (ADAS) | ||

| Communication | Cell Phone | |

| Infrastructure | ||

| Wired Communication | ||

| Short-Range Wireless | ||

| Computer | System and Display | |

| Peripherals | ||

| Storage | ||

| Industrial and Other Application-Specific IC | ||

| Above 65 nm |

| 40–65 nm |

| 28–40 nm |

| Below 28 nm |

| 150 mm |

| 200 mm |

| 300 mm |

| Automotive |

| Industrial |

| Consumer Electronics |

| Telecommunications |

| Healthcare |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Type | General-Purpose IC | Interface | |

| Power Management | |||

| Signal Conversion | |||

| Amplifiers / Comparators | |||

| Application-Specific IC | Consumer | Audio / Video | |

| Digital Cameras and Camcorders | |||

| Automotive | Infotainment | ||

| Advanced Driver-Assistance Systems (ADAS) | |||

| Communication | Cell Phone | ||

| Infrastructure | |||

| Wired Communication | |||

| Short-Range Wireless | |||

| Computer | System and Display | ||

| Peripherals | |||

| Storage | |||

| Industrial and Other Application-Specific IC | |||

| By Technology Node | Above 65 nm | ||

| 40–65 nm | |||

| 28–40 nm | |||

| Below 28 nm | |||

| By Wafer Size | 150 mm | ||

| 200 mm | |||

| 300 mm | |||

| By End-Use Application | Automotive | ||

| Industrial | |||

| Consumer Electronics | |||

| Telecommunications | |||

| Healthcare | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will the analog integrated circuit market be by 2031?

It is projected to reach USD 98.69 billion by 2031, growing at a 2.76% CAGR from 2026 to 2031.

Which segment is expanding fastest within the market?

Healthcare applications are forecast to advance at a 3.73% CAGR owing to ultra-low-power biosensors and portable diagnostics.

Why are 300 mm fabs important for analog suppliers?

Moving to 300 mm wafers reduces die cost about 40%, giving vertically integrated firms a lasting cost advantage over fabless peers.

Which geography offers the highest growth through 2031?

The Middle East shows the fastest trajectory at 3.79% as sovereign funds back fab projects and defense-grade analog demand.

How concentrated is supplier power in this space?

The top five vendors hold near 45% revenue share, resulting in a moderate concentration level that leaves room for niche specialists.

What key risk could slow market growth?

Cyclical downturns in smartphones and PCs can trim revenue because consumer devices still represent about 18% of demand.