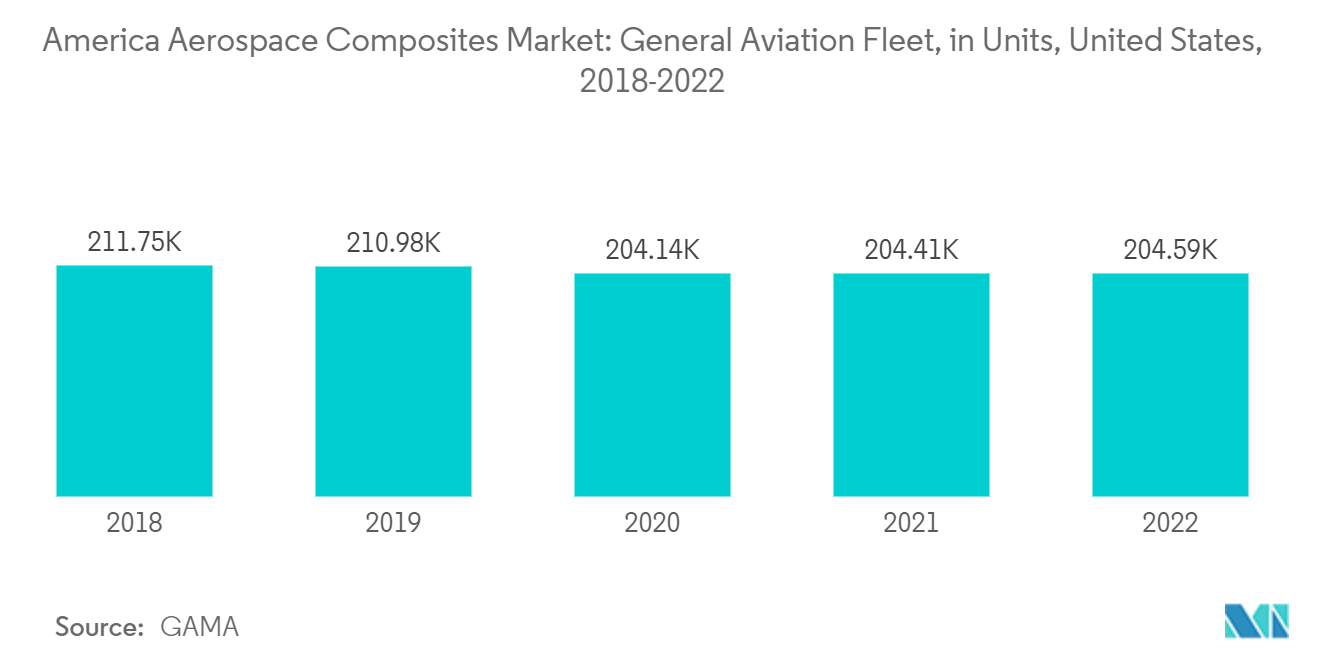

Market Trends of America Aerospace Composites Industry

Commercial Aircraft Segment to have the Largest Market Share During the Forecast Period

According to the IATA report titled Airport Technology Roadmap to 2050, new commercial aircraft will still be revolutionary developments with a traditional tube-and-wing configuration. From 2035 onwards, the industry is expected to witness revolutionary changes in aircraft parts. The new designs include strut-braced wings, blended wing bodies, and battery-electric aircraft. The growth in demand for air travel in North America and Latin America for tourism, personal, and business travel has led to rapid growth in air passenger traffic in the region, which is fueling the expansion plans (fleet as well as route network) of various airlines. The fleet modernization plans of airlines are generating demand for newer generation commercial aircraft like Boeing 787, Boeing 777X, Airbus A320 family, and Airbus A350XWB, among others. The B787 is made of 50% composite materials (by weight), whereas the B777X will have the largest composite aircraft wings in the world. Also, the primary structures of the A320 are of composite construction with aramid fiber (AFRP), glass fiber (GFRP), and carbon fiber (CFRP) reinforced plastics, whereas the wing structures and fuselage of A350XWB are made of CFRP. The growing investments to decrease the weight of the aircraft to minimize the fuel burn are anticipated to increase the investments into composites in commercial aircraft. To achieve this goal, various component manufacturers of wing structures, thrust reversers, aircraft nacelles, and engine components are incorporating composite materials. For instance, in November 2021, Triumph Group was awarded a long-term contract with Boeing to manufacture air distribution system composite ducting and composite cockpit assemblies for the 777X aircraft. Additionally, Triumph Group will provide the thermal-acoustic primary insulation systems for the B737 MAX, B767 Freighter, and B777.

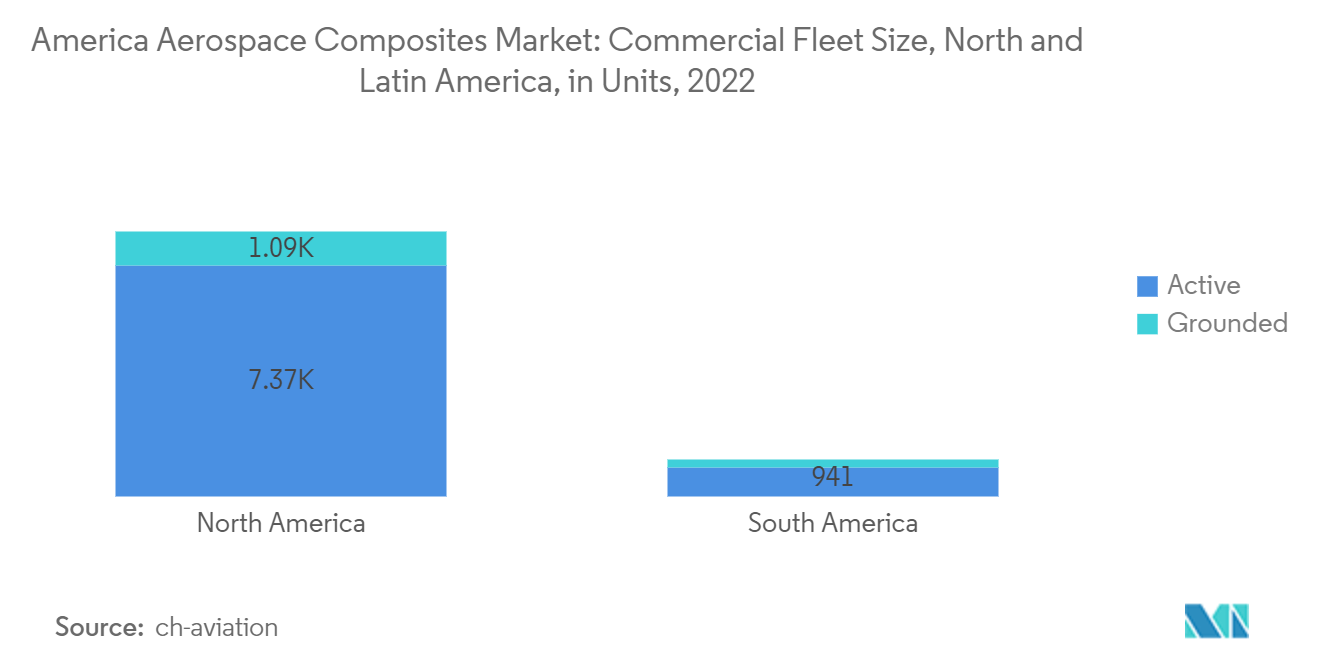

North America will Dominate the Market During the Forecast Period

The North American region currently dominates the market and is expected to continue its dominance during the forecast period. Fleet expansion and modernization plans, as well as an increase in operating routes by the airlines, are propelling new aircraft procurement. Also, under military fleet modernization plans, the US Air Force plans to acquire a wide range of military aircraft in the coming years. The US government in February 2020 announced its plan to acquire the F-15EX fourth-generation version of the F-15 fighter (F-15 airframe is made from 2% composites, which include boron/epoxy empennage skins and a carbon fiber/epoxy speed brake). These aircraft will complement the country’s fleet of F-35 fighter jet aircraft (approximately 40% made from composites), as well as combat drones planned to enter service in the coming years. In addition to these investments, the government is also investing in space exploration programs. For instance, in December 2022, Velocity Composites entered the US market with the signing of an agreement with GKN Aerospace. To support the expansion into US markets, Velocity Composites plans the development of a 40,000-square-foot advanced manufacturing facility near the GKN site in Alabama (US). The new facility will build and supply all the composite material kits for GKN’s aerostructures.