Market Size of Aluminum Cans Industry

| Study Period | 2019 - 2029 |

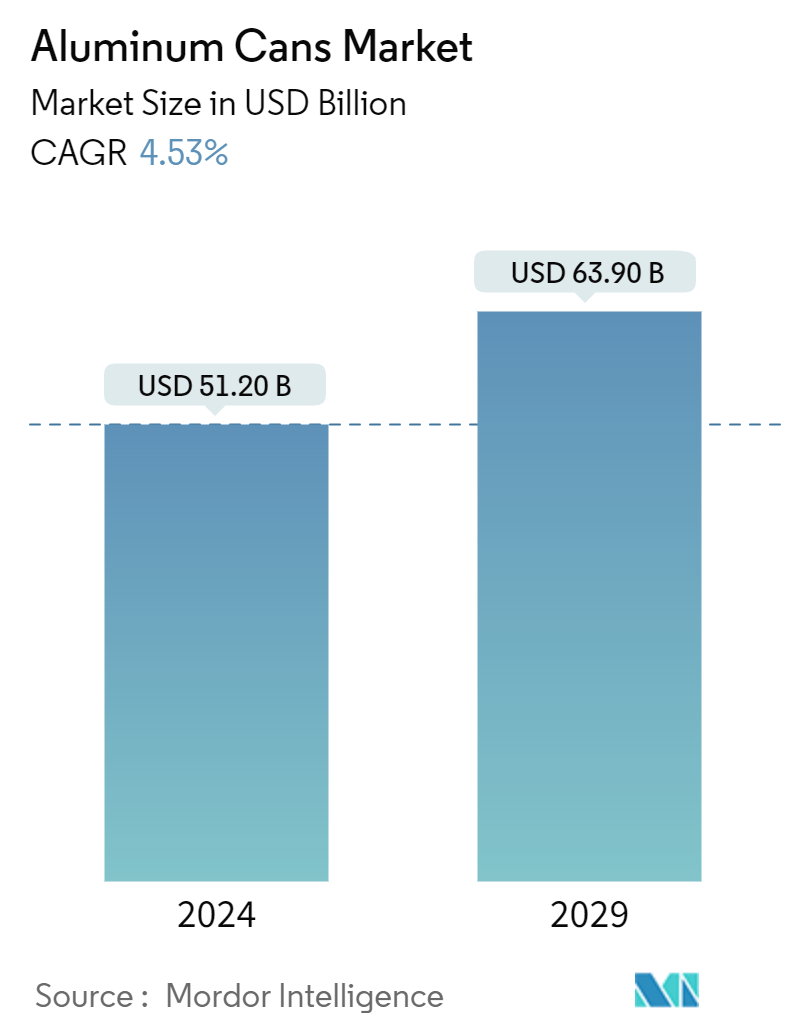

| Market Size (2024) | USD 51.20 Billion |

| Market Size (2029) | USD 63.90 Billion |

| CAGR (2024 - 2029) | 4.53 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Aluminum Cans Market Analysis

The Aluminum Cans Market size is estimated at USD 51.20 billion in 2024, and is expected to reach USD 63.90 billion by 2029, growing at a CAGR of 4.53% during the forecast period (2024-2029).

- Aluminum cans offer long-term food quality preservation benefits. They deliver nearly 100% protection against light, oxygen, moisture, and other contaminants. They do not rust and are corrosion-resistant, providing one of the most extended shelf lives of any packaging. Additionally, designers, engineers, and manufacturers leverage aluminum's diverse physical properties. Compared to many metals, aluminum has a lighter weight per volume, making it easier to handle and more cost-effective to ship. This fuels the usage of aluminum cans in the market.

- The food and beverage industry's increasing adoption of aluminum cans stems from their protective nature, sustainability benefits, and consumer ease. This trend is set to persist, given that manufacturers and consumers alike are increasingly acknowledging the advantages of aluminum packaging. Notably, aluminum stands out as the most recyclable material globally, boasting a nearly 100% recyclability rate. Moreover, aluminum retains its integrity through multiple recycling cycles, making it a highly sustainable choice. The environmental benefits are significant, such as recycling aluminum conserves energy, reduces millions of tons of greenhouse gas emissions, and decreases the demand for transportation fuel. Manufacturing aluminum cans from recycled materials consumes significantly less energy than producing new cans, driving the adoption of recyclable aluminum cans.

- Aluminum cans stand out in recycling, undergoing a closed-loop process where they are recycled repeatedly. In contrast, glass and plastic, once recycled, often transform into products that are either not recyclable or have low chances of being recycled again. Aluminum cans outshine their counterparts by being infinitely recyclable, primarily to create fresh cans. Moreover, aluminum boasts premium qualities that set it apart in packaging. Its distinct physical attributes not only pave the way for new brand launches but also facilitate the expansion of existing brands into untapped markets, propelling the demand for aluminum can packaging in the food and beverage industry.

- However, aluminum can packaging faces high competition from alternative packaging solutions. Plastic, paper, and glass packaging solutions are the alternative packaging options available. Also, the increasing importance of e-commerce worldwide is expected to influence the overall packaging industry. Moreover, incremental enhancements in plastic packaging are posing a threat to the market, which can primarily be attributed to the popularity of plastics, such as polyethylene terephthalate (PET), as substitutes. PET plastics threaten to displace aluminum can solutions in the food and beverage industry.

- The global economy was significantly affected by the COVID-19 pandemic. Industries faced substantial challenges from supply chain disruptions and government-mandated lockdowns. The war between Russia and Ukraine also triggered economic sanctions against multiple nations, escalating commodity prices and straining supply chains, which reverberated through global markets and led to trade disruptions. This caused European aluminum firms to scale back production due to metal shortages. With the war intensifying these shortages for European manufacturers reliant on Russian supplies, commodity traders registered low profits by shipping aluminum from China. Furthermore, Europe witnessed a notable surge in energy costs, directly impacting the production volume of aluminum cans in the market.

Aluminum Cans Industry Segmentation

Aluminum cans are used due to their sustainability characteristics. They have higher recycling rates and more recycled content than competing package types. Aluminum cans are lightweight, stackable, and strong, allowing brands to package and transport more products using less material.

The aluminum cans market is segmented by type (slim, sleek, and standard), by end-user industry (beverage, food, and aerosol), and by geography (North America (the United States and Canada), Europe (the United Kingdom, Germany, France, Spain, and Rest of Europe), Asia-Pacific (China, India, Japan, South Korea, Thailand, and Rest of Asia Pacific), Latin America (Brazil, Mexico, and Rest of Latin America), and Middle East and Africa (United Arab Emirates, Saudi Arabia, South Africa, and Rest of Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Type | |

| Slim | |

| Sleek | |

| Standard | |

| Other Types |

| By End-user Industry | |

| Beverage | |

| Food | |

| Aerosol | |

| Other End-user Industries |

| By Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Aluminum Cans Market Size Summary

The aluminum cans market is poised for significant growth, driven by their inherent advantages in food quality preservation and sustainability. Aluminum cans offer nearly complete protection against light, oxygen, and moisture, ensuring extended shelf life for packaged products. Their corrosion-resistant nature and high recyclability make them a preferred choice in the food and beverage industry. The increasing consumer preference for sustainable packaging solutions, coupled with the environmental benefits of aluminum recycling, is propelling the demand for aluminum cans. The market is witnessing a trend towards smaller, multi-pack formats, catering to the convenience-seeking younger demographics and urban consumers. This shift is further supported by the growing popularity of canned beverages, including wine and cocktails, which are traditionally packaged in glass but are now increasingly offered in aluminum cans for portability and ease of use.

Despite the robust growth prospects, the aluminum cans market faces competition from alternative packaging materials such as plastic, paper, and glass. The rise of e-commerce and advancements in plastic packaging pose challenges to aluminum's market share. However, the market's resilience is evident in its ability to adapt to changing consumer behaviors and preferences, particularly in the wake of the COVID-19 pandemic, which has heightened the demand for long-shelf-life products. North America leads the market, driven by the region's focus on sustainable packaging and the expansion of the personal care sector. The market's competitive landscape is characterized by the presence of major players like Ball Corporation, Crown Holdings, and Ardagh Group, who are actively engaging in initiatives to enhance recycling rates and promote circular economy practices.

Aluminum Cans Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Value Chain Analysis

-

1.3 Industry Attractiveness - Porter's Five Forces Analysis

-

1.3.1 Bargaining Power of Suppliers

-

1.3.2 Bargaining Power of Consumers

-

1.3.3 Threat of New Entrants

-

1.3.4 Threat of Substitute products

-

1.3.5 Intensity of Competitive Rivalry

-

-

1.4 Assessment of the Impact of COVID-19 on the industry

-

-

2. MARKET SEGMENTATION

-

2.1 By Type

-

2.1.1 Slim

-

2.1.2 Sleek

-

2.1.3 Standard

-

2.1.4 Other Types

-

-

2.2 By End-user Industry

-

2.2.1 Beverage

-

2.2.2 Food

-

2.2.3 Aerosol

-

2.2.4 Other End-user Industries

-

-

2.3 By Geography

-

2.3.1 North America

-

2.3.1.1 United States

-

2.3.1.2 Canada

-

-

2.3.2 Europe

-

2.3.2.1 United Kingdom

-

2.3.2.2 Germany

-

2.3.2.3 France

-

2.3.2.4 Spain

-

2.3.2.5 Rest of Europe

-

-

2.3.3 Asia-Pacific

-

2.3.3.1 China

-

2.3.3.2 India

-

2.3.3.3 Japan

-

2.3.3.4 South Korea

-

2.3.3.5 Thailand

-

2.3.3.6 Rest of Asia-Pacific

-

-

2.3.4 Latin America

-

2.3.4.1 Brazil

-

2.3.4.2 Mexico

-

2.3.4.3 Rest of Latin America

-

-

2.3.5 Middle East and Africa

-

2.3.5.1 United Arab Emirates

-

2.3.5.2 Saudi Arabia

-

2.3.5.3 South Africa

-

2.3.5.4 Rest of Middle East & Africa

-

-

-

Aluminum Cans Market Size FAQs

How big is the Aluminum Cans Market?

The Aluminum Cans Market size is expected to reach USD 51.20 billion in 2024 and grow at a CAGR of 4.53% to reach USD 63.90 billion by 2029.

What is the current Aluminum Cans Market size?

In 2024, the Aluminum Cans Market size is expected to reach USD 51.20 billion.