| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 14.22 Billion |

| Market Size (2030) | USD 18.14 Billion |

| CAGR (2025 - 2030) | 5.00 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Aluminum Forging Market Analysis

The Aluminium Forging Market size is estimated at USD 14.22 billion in 2025, and is expected to reach USD 18.14 billion by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

The aluminum forging industry is experiencing significant transformation driven by technological advancements in manufacturing processes and increasing emphasis on sustainable production methods. Advanced forging techniques, including precision forging and near-net-shape forging, are gaining prominence as they minimize material waste and reduce energy consumption during the manufacturing process. The integration of automation and digital technologies in forging operations has led to improved process control, enhanced quality consistency, and increased production efficiency. This technological evolution is particularly evident in the development of complex geometries and high-performance components required across various industrial applications.

The industry's landscape is being reshaped by shifting global supply chain dynamics and regional manufacturing capabilities. According to global production statistics, the automotive sector alone manufactured 85.01 million vehicles in 2022, representing a 5.99% increase from the previous year, highlighting the robust demand for forged components. The establishment of new manufacturing facilities and the expansion of existing ones are creating regional manufacturing hubs, particularly in emerging economies. This geographical diversification of production capabilities is helping manufacturers better serve local markets while reducing logistics costs and supply chain vulnerabilities.

The aerospace and defense sectors continue to be significant influencers in the forgings industry evolution. The commercial airline industry generated revenues of USD 732 billion in 2022, marking a substantial 43.6% year-on-year growth, indicating strong recovery and demand for aircraft components. Additionally, global military expenditure reached USD 2,240 billion in 2022, growing by 3.7% in real terms, driving demand for specialized forged components in defense applications. These sectors' requirements for high-performance, lightweight components are pushing manufacturers to innovate in terms of material composition and manufacturing processes.

The construction and infrastructure development sector is emerging as a key growth catalyst for the aluminum forging industry. According to industry forecasts, the global construction industry is expected to grow by USD 4.5 trillion by 2030, creating substantial opportunities for forged aluminum components in building systems and structural applications. The increasing adoption of sustainable building practices and the growing preference for lightweight, durable materials in construction projects are driving innovations in forged aluminum products. Manufacturers are developing specialized alloys and forging techniques to meet the specific requirements of modern construction applications, including enhanced structural integrity and improved corrosion resistance.

Aluminum Forging Market Trends

Growing Use of Aluminum Forged Products from Various End-Use Sectors

The increasing adoption of aluminum forged products across multiple industries is primarily driven by their superior properties, including a high strength-to-weight ratio, excellent ductility, and high corrosion resistance. In the automotive sector, aluminum forging has become crucial as manufacturers focus on fuel efficiency and emissions reduction. According to recent industry data, global vehicle production reached 85.01 million units in 2022, registering a growth rate of 5.99% compared to the previous year. The electric vehicle segment has shown particularly strong growth, with global sales exceeding 10 million units in 2022, representing 14% of all new car sales. This trend is expected to accelerate, with projections indicating electric vehicle sales will reach 14 million units by the end of 2023, marking a 35% year-over-year increase.

The aerospace industry represents another significant growth driver for aluminum forged products, with manufacturers increasingly utilizing these components in aircraft construction due to their lightweight properties and strength. According to the Boeing Commercial Outlook 2023-2042, the total global deliveries of airplanes are estimated to be 42,595 units by 2042, indicating substantial long-term demand for aluminum forging components. In the construction sector, aluminum forgings are gaining prominence in applications ranging from structural components to architectural elements, driven by their durability and corrosion resistance. The industrial forging market is also witnessing increased adoption of aluminum forged parts, particularly in equipment requiring high-performance components that can withstand demanding operational conditions while maintaining structural integrity.

The marine industry has emerged as another significant consumer of aluminum forged products, particularly in shipbuilding applications where components must withstand harsh maritime environments. The material's natural corrosion resistance and strength make it ideal for various marine applications, from structural components to propulsion systems. Additionally, in the power generation sector, aluminum forgings are increasingly utilized in both conventional and renewable energy installations, particularly in wind turbine components and power transmission equipment, where their lightweight properties and durability provide significant advantages over traditional materials.

Understand The Key Trends Shaping This Market

Download PDF

Segment Analysis: Forging Type

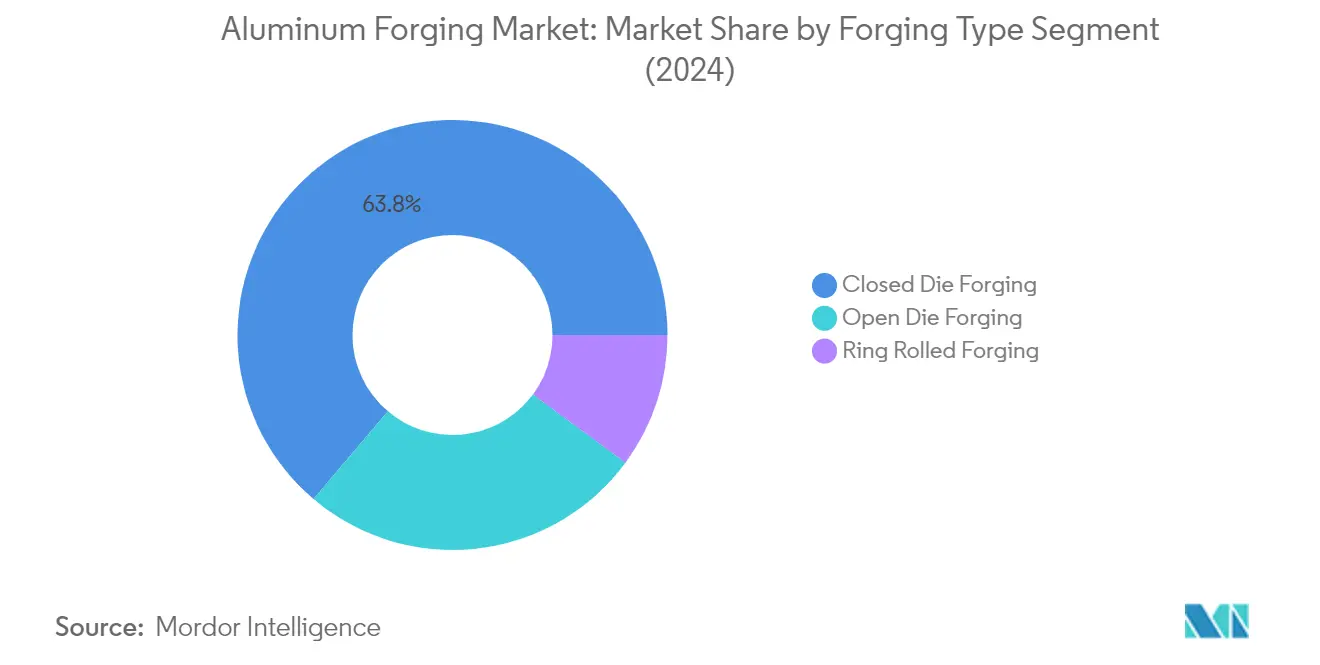

Closed Die Forging Segment in Aluminum Forging Market

Closed die forging dominates the aluminum forgings market, accounting for approximately 64% of the total market share in 2024. This segment's prominence can be attributed to its superior capabilities in producing intricate designs with tighter tolerances compared to other forging methods. The aluminum forging process involves compressing heated aluminum between two dies that contain a pre-cut profile of the desired part, resulting in high-strength components with excellent grain flow and minimal material waste. The segment is also experiencing the fastest growth rate in the market, projected to grow at around 5% from 2024 to 2029, driven by increasing demand from the automotive and aerospace industries where precision-engineered components are crucial. The automotive sector particularly favors closed die forging for manufacturing critical components like connecting rods, crankshafts, and suspension parts, while the aerospace industry relies on it for producing turbine blades, structural components, and landing gear parts.

Remaining Segments in Forging Type

The aluminum forging market also encompasses open die forging and ring rolled forging segments, each serving distinct industrial applications. Open die forging, characterized by its flexibility in producing various shapes and sizes, is particularly valuable for manufacturing large industrial components and custom parts where the construction of expensive closed dies is not economically justified. Ring rolled forging, while representing a smaller market share, plays a crucial role in producing seamless rings used in aerospace, power generation, and industrial machinery applications. These segments complement the closed die forging segment by offering solutions for specific applications where size, shape, or production volume requirements make them more suitable than closed die forging.

Segment Analysis: End-User Industry

Automotive and Transportation Segment in Aluminum Forging Market

The automotive and transportation segment continues to dominate the global aluminum forgings market, commanding approximately 39% of the market share in 2024. This significant market position is driven by the increasing adoption of aluminum forged components in vehicles to reduce weight and improve fuel efficiency. The automotive industry's shift towards electric vehicles has further accelerated the demand for aluminum forgings, as manufacturers seek lightweight yet durable materials for various components, including chassis parts, suspension systems, and powertrain components. The segment's growth is particularly strong in regions like Asia-Pacific and North America, where major automotive manufacturers are increasingly incorporating aluminum forged parts in their vehicle designs to meet stringent emission standards and enhance vehicle performance.

Aerospace and Defense Segment in Aluminum Forging Market

The aerospace and defense segment is projected to exhibit the highest growth rate of approximately 6% during the forecast period 2024-2029. This accelerated growth is primarily attributed to the increasing demand for lightweight and high-strength components in aircraft manufacturing and defense applications. The segment's expansion is further supported by rising investments in commercial aviation, military modernization programs, and space exploration initiatives across major economies. The challenging and harsh environments in airspace necessitate structures that are both strong and durable, yet lightweight, making forged aluminum an ideal material choice. Additionally, the growing focus on fuel efficiency and reduced emissions in the aviation sector continues to drive the adoption of aluminum forged components in aircraft manufacturing.

Remaining Segments in End-User Industry

The construction, industrial machinery, and other end-user industries collectively represent significant portions of the aluminum forging market. The construction segment maintains a strong presence due to the increasing use of aluminum forgings in structural components, architectural elements, and building systems. The industrial machinery sector utilizes aluminum forgings in various applications requiring high-performance components, while other industries, including power generation, marine, and electronics, continue to adopt aluminum forgings for their specific applications. These segments benefit from aluminum forging's advantages such as corrosion resistance, durability, and design flexibility, contributing to the overall market growth across diverse industrial applications.

Aluminium Forging Market Geography Segment Analysis

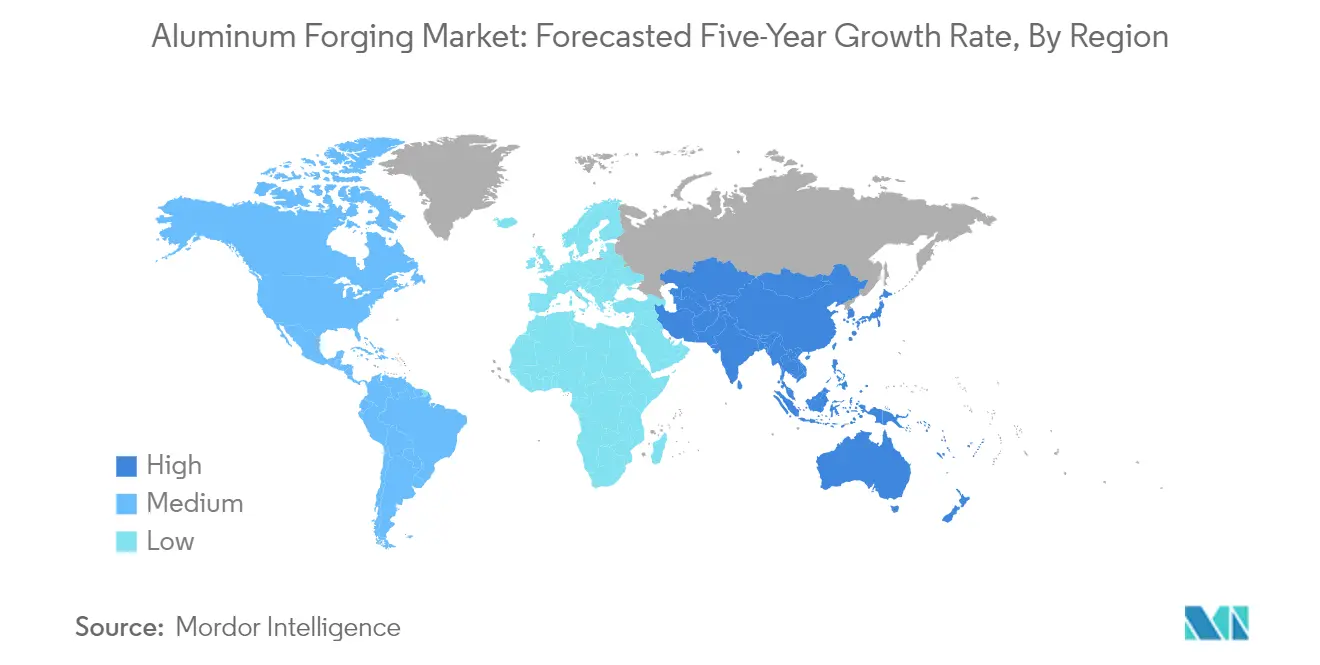

Aluminum Forging Market in Asia-Pacific

The Asia-Pacific region represents the largest market for aluminum forging globally, driven by robust manufacturing capabilities and expanding end-use industries. China leads the regional market, followed by Japan and India, with significant contributions from South Korea. The region's dominance is supported by its strong automotive manufacturing base, growing aerospace sector, and extensive industrial machinery production. The presence of major automotive manufacturers, increasing defense spending, and rapid industrialization continue to drive market growth across these countries.

Aluminum Forging Market in China

China dominates the Asia-Pacific aluminum forging market, holding approximately 57% of the regional market share. The country's market leadership is driven by its extensive automotive manufacturing capabilities, robust aerospace industry, and significant investments in industrial machinery. China's dominance is further strengthened by its position as the world's largest automotive producer and its growing focus on electric vehicle manufacturing. The country's industrial production showcases consistent growth, particularly in high-tech manufacturing and equipment manufacturing sectors, which continue to drive demand for aluminum forged components.

Aluminum Forging Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, with a projected growth rate of approximately 7% during 2024-2029. The country's growth is fueled by rapid industrialization, an expanding automotive sector, and increasing aerospace manufacturing activities. India's automotive industry shows remarkable development across various sectors, with significant growth in both domestic production and exports. The country's ambitious infrastructure development plans, coupled with increasing foreign direct investments in manufacturing, continue to create substantial opportunities for aluminum forging suppliers and applications in the Indian metal forging market.

Aluminum Forging Market in North America

North America represents a significant market for aluminum forging, characterized by advanced manufacturing capabilities and high demand from the aerospace and automotive sectors. The United States leads the regional market, followed by Canada and Mexico. The region's market is driven by its strong aerospace industry, robust automotive manufacturing sector, and increasing focus on lightweight materials in various applications. The presence of major aerospace manufacturers and automotive companies continues to drive innovation and demand in the North American forging market.

Aluminum Forging Market in United States

The United States maintains its position as the largest market in North America, commanding approximately 76% of the regional market share. The country's dominance is attributed to its extensive aerospace and defense industry, robust automotive sector, and advanced manufacturing capabilities. The US market benefits from significant defense spending, a strong commercial aviation sector, and continuous technological advancements in manufacturing processes. The country's focus on lightweight materials in automotive and aerospace applications continues to drive market growth, supported by leading aluminum forging companies in the USA.

Aluminum Forging Market in United States (Growth Focus)

The United States also leads the region in terms of growth potential, with a projected growth rate of approximately 5% during 2024-2029. This growth is driven by increasing investments in the aerospace and defense sectors, expanding automotive production, and growing adoption of aluminum forgings in various industrial applications. The country's focus on electric vehicle manufacturing and sustainable transportation solutions further supports market expansion. The robust construction sector and increasing infrastructure development projects continue to create new opportunities for aluminum forging applications, attracting interest from various aluminum forging companies.

Aluminum Forging Market in Europe

Europe represents a mature market for aluminum forging, with significant contributions from Germany, the United Kingdom, France, and Italy. The region's market is characterized by its strong automotive manufacturing base, advanced aerospace industry, and high-end industrial machinery production. The presence of major automotive manufacturers and aerospace companies, coupled with stringent environmental regulations promoting lightweight materials, drives the market dynamics in the region.

Aluminum Forging Market in Germany

Germany maintains its position as the largest market for aluminum forging in Europe. The country's market leadership is driven by its robust automotive industry, being the third-largest aerospace-exporting nation globally, and its position as a technology development leader. Germany's machinery and equipment sector, being the world's leading supplier of machinery, significantly contributes to the demand for aluminum forgings. The country's focus on electric vehicle manufacturing and sustainable technologies continues to drive market growth.

Aluminum Forging Market in United Kingdom

The United Kingdom emerges as the fastest-growing market in Europe. The country's growth is driven by its strong aerospace and defense sectors, expanding automotive industry, and increasing focus on sustainable manufacturing practices. The UK's commitment to reducing carbon emissions and promoting lightweight materials in transportation applications continues to create new opportunities for aluminum forging applications. The country's focus on advanced manufacturing and innovation in industrial processes further supports market expansion.

Aluminum Forging Market in South America

The South American aluminum forging market is primarily driven by Brazil and Argentina, with Brazil leading both in market size and growth rate. The region's market is characterized by its growing automotive sector, expanding aerospace industry, and increasing industrial manufacturing activities. Brazil's position as a major aircraft manufacturer and Argentina's developing automotive sector contribute significantly to regional market growth. The region's focus on industrial development and increasing investments in manufacturing capabilities continue to create opportunities for market expansion.

Aluminum Forging Market in Middle East and Africa

The Middle East and Africa region shows promising growth in the aluminum forging market, with South Africa and Saudi Arabia as key contributors. The region's market is driven by increasing investments in construction projects, a growing automotive sector, and an expanding industrial manufacturing base. South Africa leads the region in market size, while Saudi Arabia shows significant growth potential due to its ambitious industrial development plans and increasing focus on manufacturing capabilities. The region's ongoing infrastructure development projects and growing focus on industrial diversification continue to drive market growth, contributing to the broader metal forging market.

Get Analysis on Important Geographic Markets

Download PDF

Aluminum Forging Industry Overview

Top Companies in Aluminum Forging Market

The global aluminum forging companies market features established players like Howmet Aerospace, Bharat Forge, ThyssenKrupp AG, Kobe Steel, and Nippon Steel Corporation leading the industry through continuous innovation and strategic expansion. Companies are increasingly focusing on developing specialized forging techniques and advanced manufacturing processes to meet the evolving demands of the aerospace, automotive, and industrial sectors. The industry witnesses ongoing investments in R&D capabilities, with players developing proprietary technologies and expanding their product portfolios to maintain competitive advantages. Operational excellence is being achieved through automation, digitalization of manufacturing processes, and the establishment of integrated facilities that optimize production efficiency. Market leaders are strengthening their global presence through strategic partnerships, capacity expansions, and the establishment of regional manufacturing hubs to better serve local markets and reduce supply chain complexities.

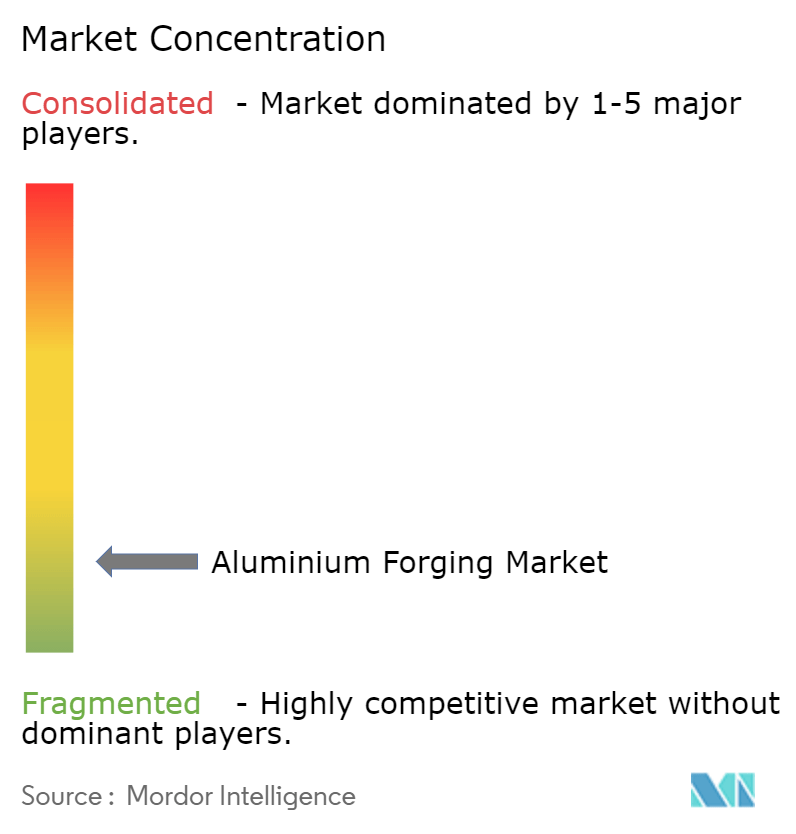

Market Structure Shows Mixed Competition Dynamics

The aluminum forging market exhibits a fragmented structure with a mix of global conglomerates and specialized regional players competing across different application segments. Large multinational corporations leverage their extensive manufacturing networks, technological capabilities, and established customer relationships to maintain market positions, while specialized players focus on niche applications and regional markets. The industry is characterized by the presence of integrated manufacturers who control multiple stages of the value chain, from raw material processing to finished product delivery, alongside pure-play forging specialists who focus on specific market segments.

The market demonstrates moderate consolidation tendencies, with larger players pursuing strategic acquisitions to expand their technological capabilities and geographic reach. Companies are increasingly focusing on vertical integration strategies to ensure raw material security and enhance cost competitiveness. The competitive landscape is further shaped by the presence of numerous small and medium-sized enterprises that serve local markets and specific industry segments, contributing to the overall market dynamism. Regional players are gaining prominence through specialized offerings and strong local customer relationships, while global players continue to strengthen their positions through technology leadership and scale advantages. The metal forging market share is influenced by these dynamics, with companies striving to capture larger portions of the market through innovation and strategic initiatives.

Innovation and Sustainability Drive Future Success

Success in the aluminum forging market increasingly depends on companies' ability to innovate while maintaining cost competitiveness and sustainability credentials. Market incumbents are focusing on developing advanced forging technologies, implementing smart manufacturing processes, and expanding their sustainable product offerings to maintain their competitive edge. The ability to provide customized solutions, maintain consistent quality standards, and offer value-added services has become crucial for market success. Companies are also investing in developing lightweight solutions for the automotive and aerospace sectors, while strengthening their positions in emerging application areas.

Future market leadership will require companies to effectively address growing end-user demands for sustainable manufacturing practices and enhanced product performance. Players must navigate challenges related to raw material price volatility, increasing environmental regulations, and evolving customer specifications. Success factors include developing strong research and development capabilities, maintaining efficient supply chain networks, and building long-term customer relationships. Companies entering or expanding in the market need to focus on technological differentiation, strategic partnerships, and specialized market segments to establish sustainable competitive positions. The ability to adapt to changing metal forging market trends, maintain operational flexibility, and provide innovative solutions will be crucial for long-term success. Additionally, the forging machinery market is expected to evolve, with advancements in technology driving efficiency and sustainability in production processes.

Aluminum Forging Market Leaders

-

Howmet Aerospace

-

Bharat Forge

-

Thyssenkrupp AG

-

Kobe Steel, Ltd.

-

Nippon Steel Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Aluminum Forging Market News

- September 2024: Ramkrishna Forgings Ltd is set to invest INR 575 million (~USD 6.9 million) in a new aluminum forging facility located in Jamshedpur, Jharkhand, India. The facility will primarily focus on the electric vehicle segment. With an annual capacity of 3,000 tonnes, it is slated to commence operations by Q2 of the 2025-26 fiscal year. This strategic investment underscores Ramkrishna Forgings' dedication to vehicle lightweighting, a pivotal element in boosting performance, enhancing fuel efficiency, and minimizing the environmental footprint of modern vehicles.

- September 2024: ILJIN has revealed plans to invest around USD 100 million in establishing a new aluminum forging plant in Auburn, Alabama, United States. This facility is set to create approximately 160 jobs and marks ILJIN's strategic entry into the aluminum forging market. With the new Auburn plant, ILJIN will enhance its production capabilities, specifically focusing on forged aluminum control arms tailored for various United States clients.

Aluminium Forging Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Drivers

- 4.1.1 Growing Use of Lightweight Material in Industrial Sector

- 4.1.2 Increasing Demand from the Automotive and Transportation Industry

- 4.1.3 Other Drivers

-

4.2 Restraints

- 4.2.1 Fluctuations in Aluminum Prices

- 4.2.2 Stringent Quality Standards

- 4.2.3 Other Restraints

- 4.3 Industry Value Chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size in Value)

-

5.1 Forging Type

- 5.1.1 Open Die Forging

- 5.1.2 Close Die Forging

- 5.1.3 Ring Rolled Forging

-

5.2 End-User Industry

- 5.2.1 Aerospace and Defense

- 5.2.2 Automotive and Transportation

- 5.2.3 Industrial Machinery

- 5.2.4 Construction

- 5.2.5 Other End-user Industries (Electronics and Instrumentation, Energy Power, Agriculture and Farming)

-

5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Nordic Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Qatar

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) **/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 Accurate Steel Forgings (INDIA) Limited

- 6.4.2 Al Forge Tech Co., Ltd.

- 6.4.3 All Metals & Forge Group

- 6.4.4 Aluminum Precision Products

- 6.4.5 Anchor Harvey

- 6.4.6 Anderson Shumaker Company

- 6.4.7 Bharat Forge

- 6.4.8 Ellwood Group Inc.

- 6.4.9 Howmet Aerospace

- 6.4.10 ILJIN Co., Ltd.

- 6.4.11 Kobe Steel, Ltd.

- 6.4.12 Nippon Steel Corporation

- 6.4.13 Norsk Hydro ASA

- 6.4.14 Ramkrishna Forgings Ltd

- 6.4.15 Scot Forge Company

- 6.4.16 Thyssenkrupp AG

- 6.4.17 Wheel India Limited

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advanced Forging Techniques and Simulation Technologies

- 7.2 Other Opportunities

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Aluminium Forging Industry Segmentation

Aluminum forging involves shaping aluminum through methods like hammering, rolling, or pressing. Depending on the temperature, forging can be categorized into three types: warm, cold, or hot. Aluminum and its alloys boast a unique blend of properties, establishing them as some of the most adaptable materials in engineering and construction. These alloys can be forged into diverse shapes and types, leading to a wide array of final parts tailored to specific design criteria and applications.

The aluminum forging market is segmented by forging type, end-user industry, and geography. By forging type, the market is segmented into open-die forging, close-die forging, and ring-rolled forging. By end-user industry, the market is segmented into aerospace and defense, automotive and transportation, industrial machinery, construction, and other end-user industries (electronics and instrumentation, energy power, agriculture, and farming). The report also covers the market sizes and forecasts for the global aluminum forging market in 27 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Forging Type | Open Die Forging | ||

| Close Die Forging | |||

| Ring Rolled Forging | |||

| End-User Industry | Aerospace and Defense | ||

| Automotive and Transportation | |||

| Industrial Machinery | |||

| Construction | |||

| Other End-user Industries (Electronics and Instrumentation, Energy Power, Agriculture and Farming) | |||

| Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Malaysia | |||

| Thailand | |||

| Indonesia | |||

| Vietnam | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordic Countries | |||

| Turkey | |||

| Russia | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Rest of South America | |||

| Middle East and Africa | Saudi Arabia | ||

| Qatar | |||

| United Arab Emirates | |||

| Nigeria | |||

| Egypt | |||

| South Africa | |||

| Rest of Middle-East and Africa | |||

Need A Different Region or Segment?

Customize Now

Aluminium Forging Market Research FAQs

How big is the Aluminium Forging Market?

The Aluminium Forging Market size is expected to reach USD 14.22 billion in 2025 and grow at a CAGR of greater than 5% to reach USD 18.14 billion by 2030.

What is the current Aluminium Forging Market size?

In 2025, the Aluminium Forging Market size is expected to reach USD 14.22 billion.

Who are the key players in Aluminium Forging Market?

Howmet Aerospace, Bharat Forge, Thyssenkrupp AG, Kobe Steel, Ltd. and Nippon Steel Corporation are the major companies operating in the Aluminium Forging Market.

Which is the fastest growing region in Aluminium Forging Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Aluminium Forging Market?

In 2025, the Asia-Pacific accounts for the largest market share in Aluminium Forging Market.

What years does this Aluminium Forging Market cover, and what was the market size in 2024?

In 2024, the Aluminium Forging Market size was estimated at USD 13.51 billion. The report covers the Aluminium Forging Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Aluminium Forging Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Aluminium Forging Market Research

Mordor Intelligence delivers a comprehensive analysis of the aluminium forging market. We leverage our extensive experience in tracking metal forging market trends and industry developments. Our latest report examines the complete ecosystem, from aluminum forging manufacturers to end-users. It covers crucial aspects, including aluminium forging temperature specifications and processes. The analysis encompasses both aluminum forged products and manufacturing capabilities across the North America forging market and global regions. It provides detailed insights into the operations of aluminum forging companies USA.

Stakeholders gain access to detailed forging data and analysis through our easy-to-download report PDF. This report covers everything from automotive forging market dynamics to industrial forging market applications. It provides valuable insights for aluminium forging suppliers and manufacturers. The report includes a comprehensive evaluation of aluminum forging cost factors and market size projections. Our analysis extends to specialized segments such as the aerospace forging market and the defense and aerospace forgings market. It offers stakeholders a complete understanding of market dynamics, technological advancements, and growth opportunities across the forgings industry.