Global Allergy Diagnostics Market

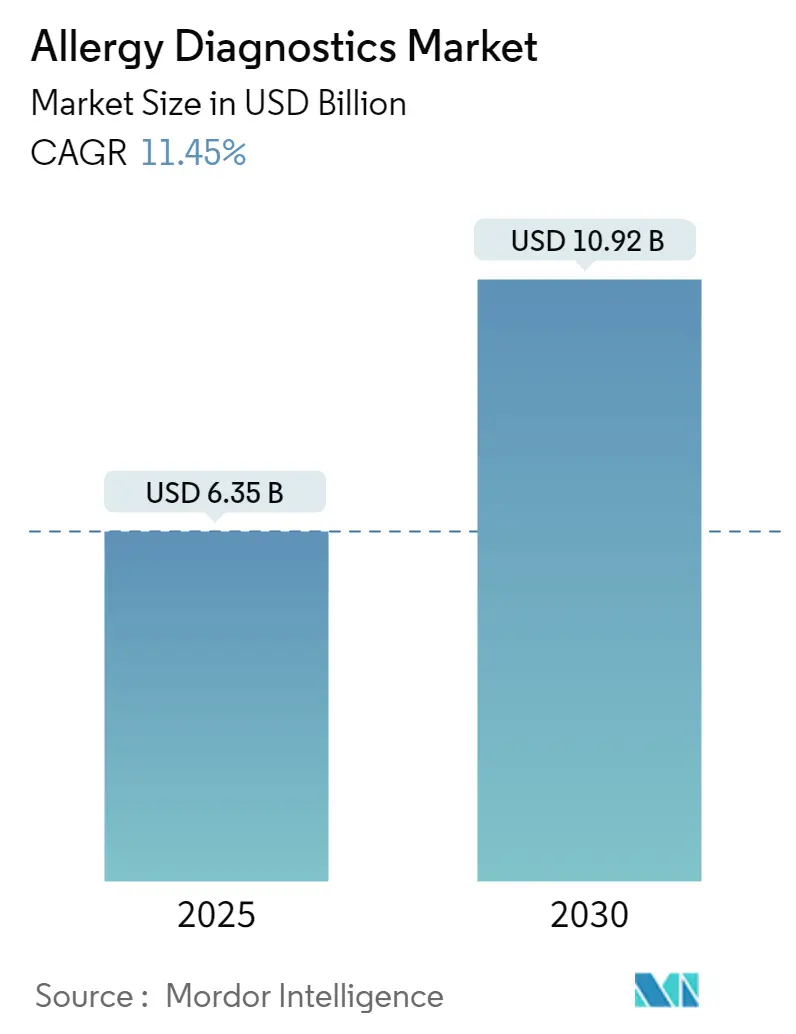

The Allergy Diagnostics Market size is estimated at USD 6.35 billion in 2025, and is expected to reach USD 10.92 billion by 2030, at a CAGR of 11.45% during the forecast period (2025-2030), driven by the increasing prevalence of allergies such as asthma, food allergies, and allergic rhinitis. Advanced immunoassays, molecular diagnostics, and point-of-care testing are enhancing the reliability and accessibility of allergy diagnostics. Heightened awareness of allergic conditions is creating substantial opportunities in the global allergy diagnostics industry, attracting both new entrants and established players.

| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 6.35 Billion |

| Market Size (2030) | USD 10.92 Billion |

| CAGR (2025 - 2030) | 11.45 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Industry Dynamics

As urbanization and industrialization surge globally, lifestyle changes have followed suit, resulting in a sharp uptick in air pollutants. This escalation has, in turn, heightened the prevalence of allergies. Such pollutants encompass cigarette smoke, perfumes, aerosol sprays, emissions from vehicles, and discharges from industrial and energy sources, among others, and play a pivotal role in triggering allergies. Hence, the rise in environmental pollution is likely to boost the market growth.

Moreover, growing awareness about allergies, their potential severity, and the significance of early diagnosis is driving more individuals to pursue allergy testing. Additionally, health campaigns led by governments and organizations play a pivotal role in boosting diagnostic testing rates. Therefore, the rising awareness and surge in government initiatives is anticipated to augment the allergy diagnostics market growth in the coming years.

Furthermore, the demand for convenient testing solutions has surged, particularly in the wake of the COVID-19 pandemic. At-home and point-of-care allergy testing kits present a significant opportunity, enabling users to self-administer tests and access results through mobile apps or online portals.

However, the allergy diagnostics industry grapples with challenges that could hinder its growth. These challenges encompass high costs, restricted access, intricate regulatory landscapes, and the absence of standardized testing. Stringent regulatory standards govern allergy diagnostic products, with variations across regions. For newer companies, navigating these regulations proves both time-consuming and costly, potentially hindering market growth.

Allergy Diagnostics Market Report Coverage

Overview of Market Segments Covered:

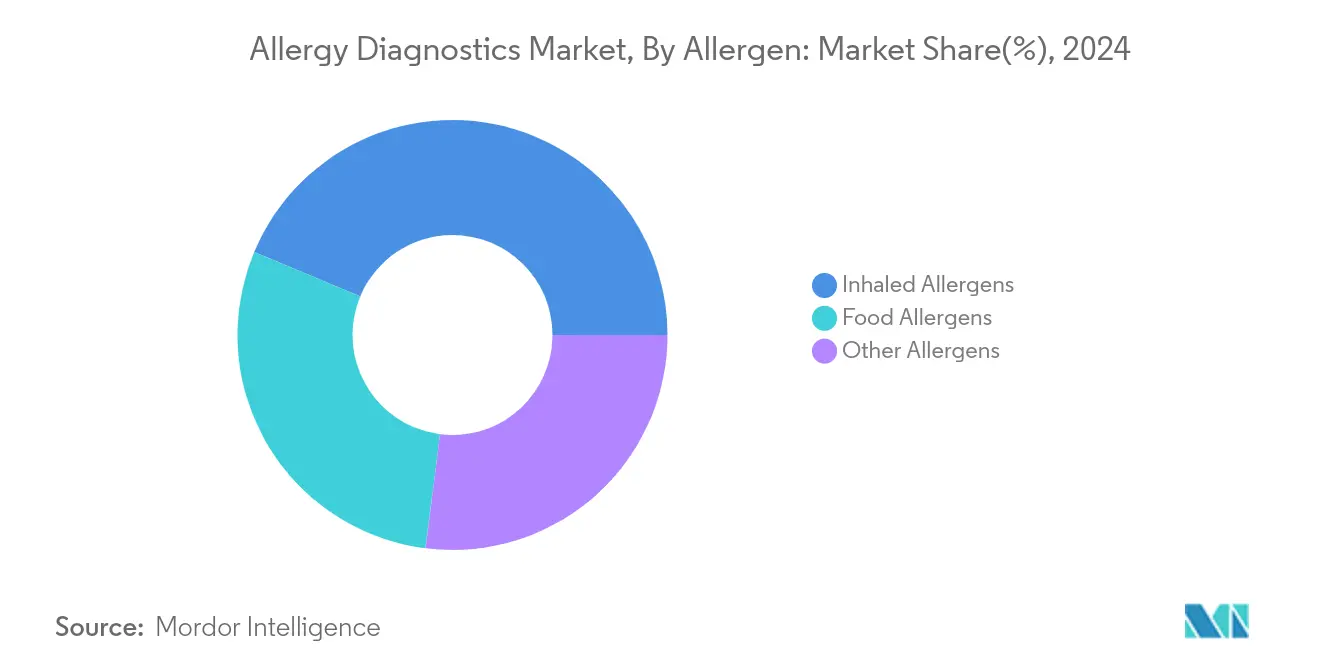

In 2024, inhaled allergens are likely to dominate the allergen segment, capturing a significant 43.51% market share. Projections indicate this segment will grow to an estimated USD 4.59 billion by 2029. Inhaled allergens often lead to allergic rhinitis, commonly known as hay fever. Thus, diagnosis of inhaled allergens is crucial in allergy diagnostics to provide proper and specific medical care to an individual. According to the research study published in Frontiers in Medicine Journal in April 2022, approximately 400 million individuals worldwide suffer from allergic rhinitis (AR) in a year. The condition impacts around 25% of children and 40% of adults. Notably, the incidence rate of AR in children during their first five years stands at 17.2%, with diagnoses peaking between 24 and 29 months. Given that allergic rhinitis is predominantly triggered by inhaled allergens, a growing demand for diagnostic tools targeting these allergens is anticipated in the coming years.

The allergy diagnostics market is segmented by allergen, product, test type, and end user. By allergen, the market is segmented into inhaled allergens, food allergens, and other allergens. By product, the market is segmented into instruments, consumables, and luminometers. Consumables refer to the various materials and products that are used during diagnostic procedures. These consumables are used during different types of allergy tests, such as skin prick tests and blood tests. By test type, the market is segmented into in-vivo allergy tests and in-vitro allergy tests. By end user, the market is segmented into diagnostic laboratories, hospitals, and other end users. Equipped with advanced tools, diagnostics laboratories ensure the reliability of allergy tests. Their expertise not only allows for precise test execution and interpretation but also enhances the overall understanding and management of allergic conditions.

Regional Market Scope of this Report:

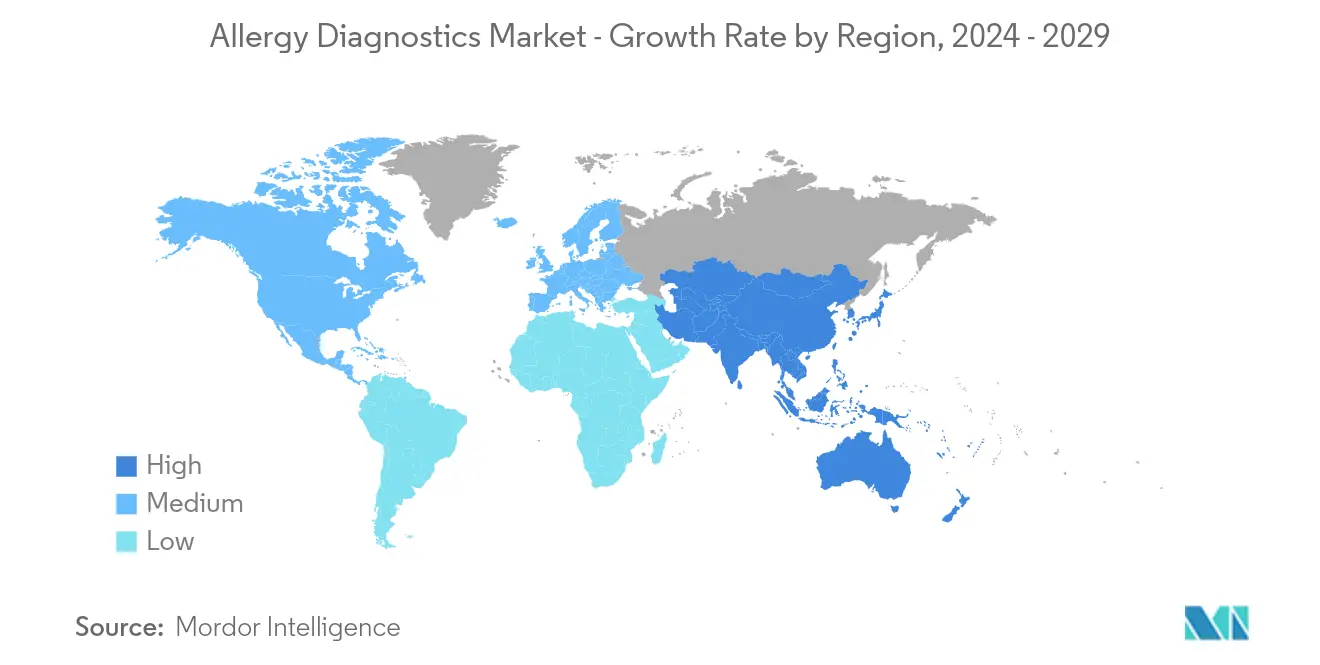

In 2024, North America is expected to dominate the market, capturing a significant 45.06% of global allergy diagnostics market share. Projections indicate this North America market value will grow to an estimated USD 4.78 billion by 2029, witnessing significant growth. This surge is driven by several factors: a rising incidence of allergic diseases, environmental pollution, increased government funding, and intensified activities from companies in the sector. For instance, according to the Asthma and Allergy Foundation Report 2022, more than 50 million Americans suffer from various types of allergies every year. The most common allergic condition is seasonal allergic rhinitis or hay fever. As per the same source mentioned above, about 7.7% of adults and 7.2% of children are diagnosed with seasonal allergic rhinitis every year. Furthermore, for instance, the Canadian Government allocated a budget for the treatment and diagnosis of allergies, which is likely to create a demand for diagnostics tests, thereby boosting the market’s growth. For instance, in May 2023, the Canadian Society of Allergy and Clinical Immunology (CSACI) allocated USD 4.5 million to initiate the National Food Allergy Action Plan, which, once fully funded and implemented, will save lives, reduce food allergy prevalence, lower healthcare costs, reduce the economic impact, and improve the quality of life for the millions of impacted Canadians. Hence, owing to these factors, the allergy diagnostics market size in North America is expected to propel in the forecast period.

By geography, the market is segmented into North America (United States, Canada, Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, Rest of Asia-Pacific), Middle East and Africa (GCC, South Africa, Rest of Middle East and Africa), and South America (Brazil, Argentina, Rest of South America). Due to rising allergy prevalence, urbanization, and enhanced healthcare access, the Asia-Pacific and Middle East regions, especially its emerging markets, is poised to see a surge in demand for allergy diagnostic tests. The allergy diagnostic industry size is expected to be high in the North America and Europe regions in the coming years.

Competitive Landscape and Ecosystem Analysis:

Some of the key players in the market are BioMerieux SA, Danaher Corporation, Abionic SA, HOB Biotech Group Corp. Ltd, HYCOR Biomedical, Lincoln Diagnostics Inc., Omega Diagnostics Group PLC, Siemens Healthineers AG, Stallergenes Greer Ltd, Thermo Fischer Scientific Inc., Revvity Inc. (PerkinElmer Inc.), R-Biopharm AG, Immunodiagnostic Systems Holdings PLC (IDS), Biomerica, Inc., among others. The key market players are involved in various strategic activities such as partnerships, product launches, and agreements, which are further expected to bolster the market growth. For instance, in August 2022, Thermo Fisher Scientific announced that the United States Food & Drug Administration (FDA) had approved ImmunoCAP Specific IgE Allergen components for in vitro diagnostic procedures for wheat and sesame allergies. For patients at risk of a severe allergic reaction, these cutting-edge blood tests are expected to serve as diagnostic tools, assisting healthcare professionals in identifying wheat and sesame allergies. The allergy diagnostics industry is moderately fragmented and consists of several market players.

Allergy Diagnostics Market Report Scope

| By Allergen | |

| Inhaled Allergens | |

| Food Allergens | |

| Other Allergens |

| By Product | |

| Instruments | |

| Consumables | |

| Luminometers |

| By End-User | |

| Diagnostic Laboratories | |

| Hospitals | |

| Other End-Users |

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Industry Developments

- In October 2024, researchers at the University of Bern, in collaboration with Bern University Hospital, created a test aimed at streamlining allergy diagnoses. This test's efficacy has been validated using clinical samples from children and adolescents with peanut allergies.

- In October 2024, ALK licensed a new range of ALK-branded allergy skin testing devices. The lineup features the AllerTest-1, AllerTest-8, and AllerTest-10 devices designed for allergy testing and diagnosis.

- In October 2024, ATANIS Biotech, a frontrunner in allergy diagnostics, secured funding to propel its innovative allergy test, FAST-PASE, forward.

- In June 2024, YorkTest, a prominent player in the health and wellness sector, introduced a new initiative aimed at making at-home food sensitivity and allergy testing more accessible to United States households. This move underscores YorkTest's dedication to empowering individuals with essential knowledge for informed health choices.

Allergy Diagnostics Market Research FAQs

How big is the Allergy Diagnostics Market?

The Allergy Diagnostics Market size is expected to reach USD 6.35 billion in 2025 and grow at a CAGR of 11.45% to reach USD 10.92 billion by 2030.

What are the biggest allergy companies?

The top key players in allergy diagnostics include BioMerieux SA, Siemens Healthineers AG, Thermo Fischer Scientific Inc., Omega Diagnostics Group PLC and Danaher Corporation.

Who are the key players in Allergy Diagnostics Market?

BioMerieux SA, Siemens Healthineers AG, Thermo Fischer Scientific Inc, Omega Diagnostics Group PLC and Danaher Corporation are the major companies operating in the Allergy Diagnostics Market.

What challenges does the allergy diagnostics market face?

The lack of awareness about allergic diseases and issues related to affordability of the allergic diagnostic products is likely to limit the market growth in the forecast period.

What innovations are emerging in allergy diagnostic technologies?

The three foremost innovations emerging in allergy diagnostic technologies are molecular allergy diagnostics, point-of-care testing, and multiplex testing platforms.

What key trends are driving the allergy diagnostics market?

Few of the key trends in the global market include increasing prevalence of allergies, advancements in technology, and growing focus on food allergy diagnostics.

Allergy Diagnostics Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.2.1 Increasing Incidences of Allergic Diseases

4.2.2 Environmental Pollution

4.3 Market Restraints

4.3.1 Lack of Awareness About Allergic Diseases

4.3.2 Affordability of Allergy Diagnostics

4.4 Porter's Five Forces Analysis

4.4.1 Threat of New Entrants

4.4.2 Bargaining Power of Buyers/Consumers

4.4.3 Bargaining Power of Suppliers

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value in USD)

5.1 By Allergen

5.1.1 Inhaled Allergens

5.1.2 Food Allergens

5.1.3 Other Allergens

5.2 By Product

5.2.1 Instruments

5.2.2 Consumables

5.2.3 Luminometers

5.3 By End-User

5.3.1 Diagnostic Laboratories

5.3.2 Hospitals

5.3.3 Other End-Users

5.4 Geography

5.4.1 North America

5.4.1.1 United States

5.4.1.2 Canada

5.4.1.3 Mexico

5.4.2 Europe

5.4.2.1 Germany

5.4.2.2 United Kingdom

5.4.2.3 France

5.4.2.4 Italy

5.4.2.5 Spain

5.4.2.6 Rest of Europe

5.4.3 Asia-Pacific

5.4.3.1 China

5.4.3.2 Japan

5.4.3.3 India

5.4.3.4 Australia

5.4.3.5 South Korea

5.4.3.6 Rest of Asia-Pacific

5.4.4 Middle East and Africa

5.4.4.1 GCC

5.4.4.2 South Africa

5.4.4.3 Rest of Middle East and Africa

5.4.5 South America

5.4.5.1 Brazil

5.4.5.2 Argentina

5.4.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

6.1 Company Profiles

6.1.1 BioMerieux SA

6.1.2 Danaher Corporation

6.1.3 Abionic SA

6.1.4 HOB Biotech Group Corp. Ltd

6.1.5 HYCOR Biomedical

6.1.6 Lincoln Diagnostics Inc.

6.1.7 Omega Diagnostics Group Plc

6.1.8 Siemens Healthineers AG

6.1.9 Stallergenes Greer Ltd

6.1.10 Thermo Fischer Scientific Inc

6.1.11 Revvity Inc. (PerkinElmer Inc.)

6.1.12 R-Biopharm AG

6.1.13 Immunodiagnostic Systems Holdings PLC (IDS)

6.1.14 Biomeric, Inc.

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS