Aerospace & Defense

8th MayFeasibility Analysis for FBO Services in East Africa

3 Min Read

The Airport Lounges Market Report is Segmented by Service Type (Food and Beverage, Connectivity and Entertainment, and Passenger Services), Lounge Ownership (Airline, Airport, and Government and Privately Owned), Lounge Class (Economy Lounge and Premium Lounge), and Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 10.53 Billion |

| Market Size (2031) | USD 13.95 Billion |

| Growth Rate (2026 - 2031) | 5.79 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

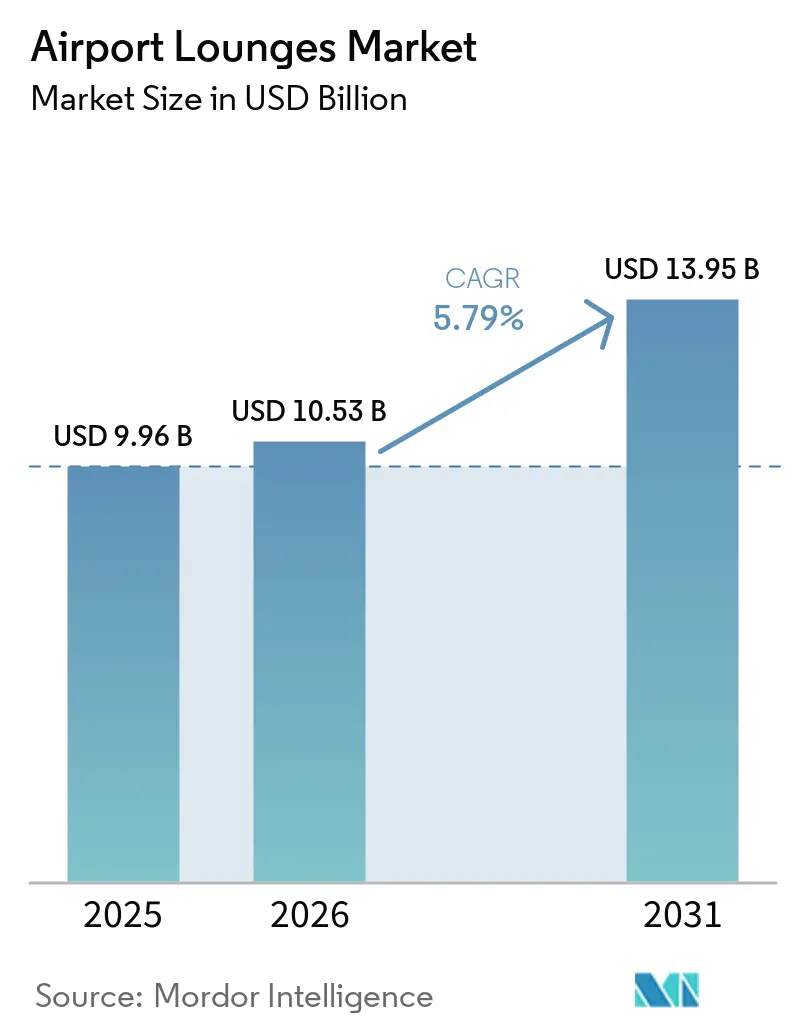

The airport lounges market size reached USD 9.96 billion in 2025, is projected at USD 10.53 billion in 2026, and is set to reach USD 13.95 billion by 2031, reflecting a 5.79% CAGR. Expansion demonstrates a shift in how airlines, credit card networks, and independent operators compete for premium travelers, with ground experiences now influencing airline choice and route decisions in the airport lounges market. Airports are recasting lounges as non-aeronautical revenue anchors, as shown by Chicago Midway's first premium common-use lounge under a USD 75 million concessions program. The Omaha Airport Authority's announcement of Escape Lounges at Eppley Airfield (OMA) for 2027 highlights a strategic move to enhance passenger services. This development aligns with industry trends, improving competitiveness and diversifying airport revenue streams. Travelers are increasingly prioritizing seamless entry and enhanced dining experiences. A majority prefer biometric processes to expedite entry, while operators are focusing on improving culinary standards to gain a competitive edge in the airport lounges market. Sustainability is becoming a proof point of quality, as seen in LEED Gold-certified lounges and food-waste reduction programs that improve both brand and operating metrics in the airport lounges market.[1]Source: Airport Dimensions, “California Inspires at San Francisco International,” Airport Dimensions, airportdimensions.com

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Revival of premium and business travel demand across international routes Revival of premium and business travel demand across international routes | +1.2% | Global, with concentration in North America and Asia-Pacific | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast :+1.2% | Geographic Relevance:Global, with concentration in North America and Asia-Pacific | Impact Timeline:Short term (≤ 2 years) |

Deployment of contactless and biometric solutions to enhance passenger throughput Deployment of contactless and biometric solutions to enhance passenger throughput | +1.1% | Europe (high early adoption), Asia-Pacific, gradually North America | Medium term (2-4 years) | |||

Accelerated lounge investments fueled by airport commercialization initiatives Accelerated lounge investments fueled by airport commercialization initiatives | +0.9% | North America, Middle East, secondary hubs in Asia-Pacific | Medium term (2-4 years) | |||

Diversification of lounge offerings through curated food menus and regionally inspired cuisines Diversification of lounge offerings through curated food menus and regionally inspired cuisines | +0.8% | Global, particularly North America premium hubs and Asia | Medium term (2-4 years) | |||

Growth of secondary airport hubs in emerging aviation markets worldwide Growth of secondary airport hubs in emerging aviation markets worldwide | +0.7% | Asia-Pacific (India, Southeast Asia), South America, secondary US markets | Long term (≥ 4 years) | |||

Rising demand for sustainable and carbon-neutral lounge operations aligned with ESG objectives Rising demand for sustainable and carbon-neutral lounge operations aligned with ESG objectives | +0.6% | Europe (regulatory pressure), North America (corporate mandates), spreading to Asia | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Revival of Premium and Business Travel Demand Across International Routes

Corporate travel regained momentum in 2026, prompting airlines and airports to enhance lounges to attract high-yield itineraries. Airlines in North America and Asia-Pacific are upgrading and expanding clubs to pair premium cabins with consistent ground experiences, raising the perceived value of long-haul and connecting journeys. As travel buyers resume in-person engagements, lounge access has become an integral part of the service offering, helping carriers maintain premium yields and distinguish themselves from low-cost competitors. Operators are also capitalizing on a clear passenger preference for faster, contactless processes, with biometric-enabled entry improving throughput and reducing queuing friction. Intra-regional corporate travel in Asia-Pacific is supporting steady lounge footfall, aligning with increased visits across top destinations and giving airports a reason to expand hospitality footprints.[2]Source: Collinson Group, “Catering to strong regional travel momentum,” Collinson Group Newsroom, collinsongroup.com

Accelerated Lounge Investments Fueled by Airport Commercialization Initiatives

Airport authorities are positioning lounges at the center of non-aeronautical revenue programs, leveraging premium hospitality to boost spend per passenger and enhance the overall mix in the airport lounges market. Chicago Midway’s first common-use lounge opened as part of a USD 75 million concessions overhaul, signaling that even busy point-to-point airports now court premium dwell time and ancillary sales. Infrastructure programs across North America present a broad runway for lounge development, with airports seeking partners that can deliver consistent service and flexible access models within constrained footprints in the airport lounges market. Gulf and Turkish gateways are also scaling premium hospitality, including new domestic and premium concepts that feature differentiated F&B and upgraded amenities to raise the service quality benchmark.

Deployment of Contactless and Biometric Solutions to Enhance Passenger Throughput

Passenger expectations have increasingly shifted toward digital identity and touchless processes, with the majority preferring biometric authentication over traditional documentation for faster processing. Lounges that integrate biometric entry reduce bottlenecks and align the last step before boarding with the broader airport journey, creating a consistent experience in the airport lounges market. Operators in Europe face stricter privacy considerations and are standardizing consent and data-retention practices to meet GDPR requirements while pursuing efficiency gains. Across Asia-Pacific and North America, contactless access is being paired with digital service features, such as online ordering and real-time capacity displays, to manage dwell time without adding staffing burden. The combined effect is higher throughput reliability and better crowding control, which supports both guest satisfaction and revenue capture in the market.

Rising Demand for Sustainable and Carbon-Neutral Lounge Operations Aligned with ESG Objectives

Sustainability is moving from messaging to measurable design and operations, with LEED-certified lounges demonstrating that low-carbon materials and efficient systems can support premium ambience in the airport lounges market. Vendors are using data to curb food waste and optimize sourcing, with AI-supported analytics showing sharp reductions in common waste items at high-traffic locations. Airports and operators are also expanding circularity efforts and local sourcing to align with corporate client mandates, integrating sustainability criteria into tender scoring and partner selection in the airport lounges market. ESG practices are now blending into brand identity, primarily where operators publicize third-party certifications that carry weight in airport procurement. These practices also mitigate cost volatility by reducing utility and waste-haulage costs, reinforcing the business case for green lounge investments.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Fluctuating airline profitability cycles limiting capital investment in lounge infrastructure Fluctuating airline profitability cycles limiting capital investment in lounge infrastructure | -0.7% | Global, acute in Europe and North America where cost pressures highest | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast :-0.7% | Geographic Relevance:Global, acute in Europe and North America where cost pressures highest | Impact Timeline:Short term (≤ 2 years) |

High operational costs and affordability High operational costs and affordability | -0.6% | Global, particularly impacting independent operators in competitive markets | Medium term (2-4 years) | |||

Space constraints at high-traffic terminals restricting lounge expansion opportunities Space constraints at high-traffic terminals restricting lounge expansion opportunities | -0.5% | North America and Europe mature hubs, select Asia-Pacific gateways | Medium term (2-4 years) | |||

Regulatory challenges related to biometric systems and passenger data privacy Regulatory challenges related to biometric systems and passenger data privacy | -0.4% | Europe (GDPR compliance), spreading to Asia-Pacific and North America | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Fluctuating Airline Profitability Cycles Limiting Capital Investment in Lounge Infrastructure

Capital intensity, multi-year build times, and rising input costs are complicating lounge investment decisions as airlines manage cyclical profitability, which dampens near-term project approvals in the airport lounges market. Airports are prioritizing projects with clear revenue uplift and resilience, which makes common-use models and third-party partnerships attractive in constrained periods. Operators are also adjusting access rules to control crowding and reduce service strain during peak periods, improving consistency without adding significant staffing overhead. These measures help stabilize guest experience while preserving the brand advantages of premium ground touchpoints. For airlines and airports, capital decisions increasingly favor scalable concepts and modernization of existing footprints over bespoke flagships unless network economics justify the spend in the airport lounges market.

Space Constraints at High-Traffic Terminals Restricting Lounge Expansion Opportunities

Prime real estate in mature hubs is scarce, forcing many operators to renovate and densify existing spaces rather than expand their footprints in the airport lounges market. New lounges at the busiest airports often require reallocation from retail or support zones and can proceed only after complex stakeholder negotiations. Secondary airports that lacked premium amenities are now carving out dedicated lounge areas within broader terminal upgrades, easing the access gap and enabling more consistent service levels. Credit-card networks and independent operators are competing for limited parcels, which increases lease pressure and favors partners who can guarantee steady volumes. The result is a gradual rebalance toward multi-operator or common-use formats that make better use of constrained terminal geometry in the airport lounges market.

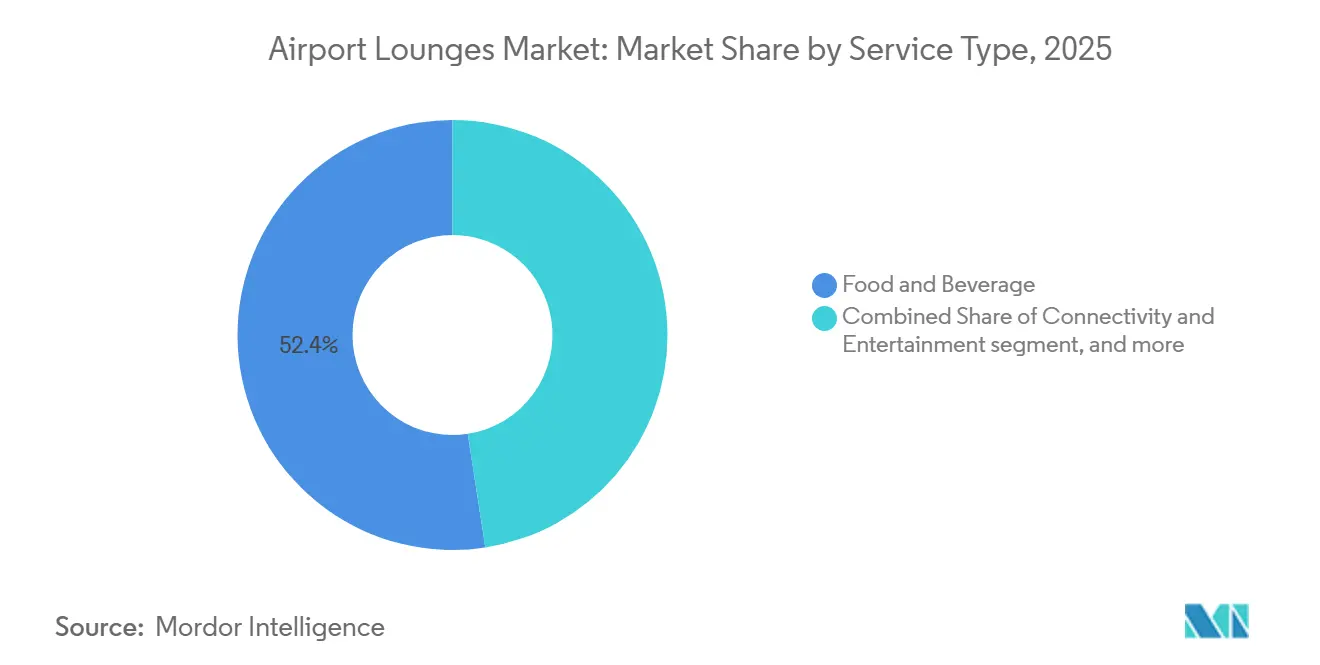

By Service Type: Food and Beverage Anchors Demand, Passenger Services Gains Momentum

Food and beverage captured 52.44% of the market share in 2025, while passenger services are forecast to grow fastest at a 5.87% CAGR through 2031, highlighting the influence of menus and wellness on perceived value. Culinary programs have emerged as key features. Operators are increasingly implementing chef-led initiatives on a larger scale, including menus and local sourcing to elevate the core offer and differentiate against crowded terminals. At the same time, wellness and convenience services such as showers, sleep pods, spa add-ons, and concierge support are accelerating, signaling broader passenger priorities beyond seating and beverages in the airport lounges industry. Network strategies now mix premium dining with smart grab-and-go for short connections, using dayparting and layout changes to balance throughput with longer-stay monetization. Access partnerships are evolving in parallel, with aggregators expanding non-lounge experiences, which adds capacity elasticities during peak flows.

Passenger services are benefiting from rising expectations for health and productivity during travel, as operators layer wellness zones and on-demand support into redesigned airport lounge spaces. The mix aligns with the growing acceptance of contactless service, including digital menus and queue management, improving delivery without linear staffing growth. During the forecast period, the market will be driven by menus incorporating regional influences and amenities designed to help travelers recharge within tight schedules. Dining partnerships also reinforce brand recognition through campaigns with notable chefs and curated beverage lists, giving operators marketing reach beyond the terminal.[3]Source: American Express, “American Express Partners with Award Winning Chefs to Create New Menus at U.S. Centurion Lounges,” American Express Newsroom, americanexpress.com Together, these shifts indicate that the airport lounges industry is converging on a two-track model that pairs restaurant-grade food programs with targeted wellness and convenience services.

Note: Segment shares of all individual segments available upon report purchase

By Lounge Ownership: Airline-Airport-Government Entities Reclaim Control

Airline, airport, and government-operated facilities held a 63.12% share in 2025 and are projected to grow the fastest at a 6.83% CAGR through 2031, showing a strategic move to protect premium touchpoints. Major carriers are upgrading and expanding networks to keep benefits closely tied to core loyalty tiers and premium cabins, while tightening access rules to improve the experience for top-value guests. Meanwhile, aggregators still provide wide coverage and flexible entry, with Priority Pass offering access across a large set of airports and partners, and renewing ties that increase choices in crowded hubs. Airports are increasingly adopting common-use lounges to provide premium services irrespective of the airline, enabling secondary hubs to attract more corporate travelers.

Privately owned facilities continue to innovate with new formats, premium-first concepts, and domestic lounge launches in high-growth regions, often leveraging culinary and wellness to stand apart in the market. Partnerships that blend airport landlords, independent operators, and loyalty platforms are becoming common, as stakeholders share risk and match offers to each terminal’s constraints in the airport lounges industry. Operators are also refining capacity management through digital waitlists and advance reservations, reducing overcrowding at boarding gates without significant footprint changes. As ownership models evolve, the balance favors approaches that can flex access rules and product depth by daypart and route mix, supporting both the guest promise and unit economics in the airport lounges market.

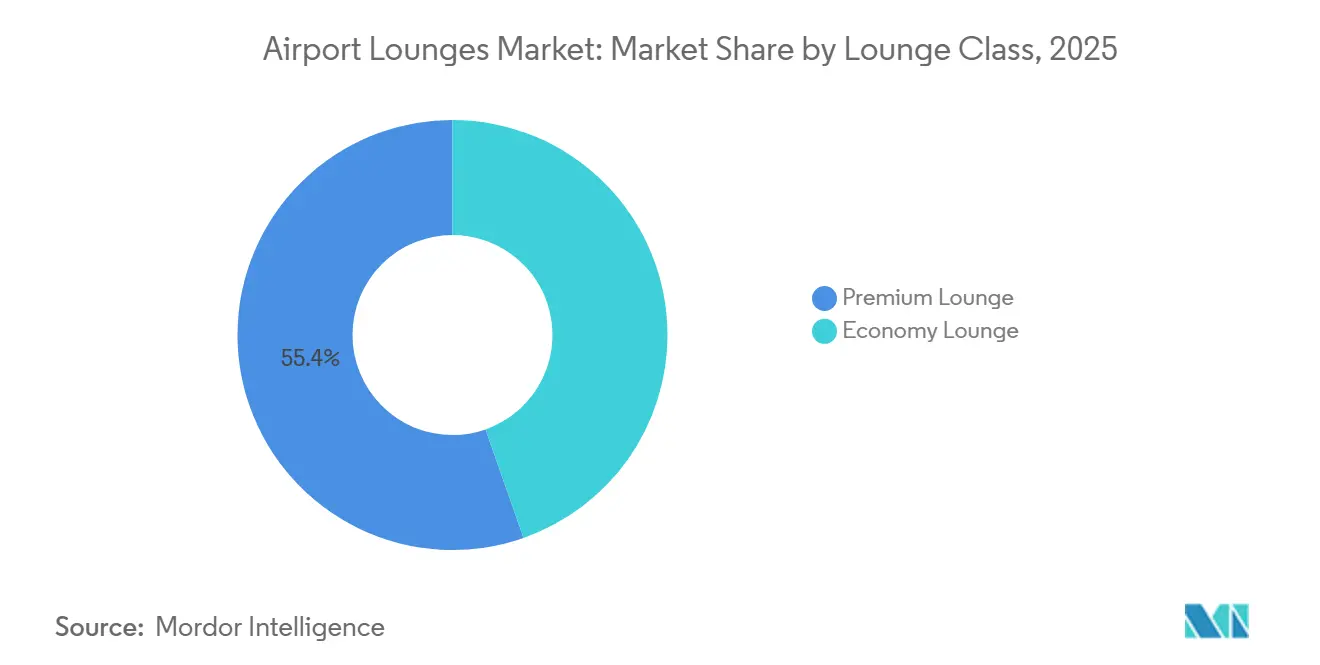

By Lounge Class: Premium Dominates, Economy Democratizes Access

Premium lounges accounted for 56.47% of 2025 demand, while economy lounges are growing fastest at a 6.17% CAGR as access broadens through cards and pay-per-use options. The top tier is adding table-service dining, curated bars, and dedicated wellness zones, positioning the lounge as an essential part of long-haul itineraries rather than a simple waiting area in the airport lounge market. Standard premium formats still serve a wide set of elite and card-linked customers, with ongoing refurbishments to improve seating density, food variety, and power access reliability.

Economy and mass-access concepts, including common-use and hybrid formats, are gaining ground as airports seek to ensure more passengers can find a quiet seat with basic refreshments. Aggregator-led networks help expand access while giving operators additional throughput, supporting the use of smaller lounges in constrained footprints. Premium-first additions at major hubs coexist with compact concepts and curated F&B-led spaces at secondary airports, which rounds out a ladder of options that can flex by route and time of day in the airport lounges market. The net result is a broader set of price points and amenity levels that maintain premium differentiation while bringing more travelers into the airport lounge ecosystem.

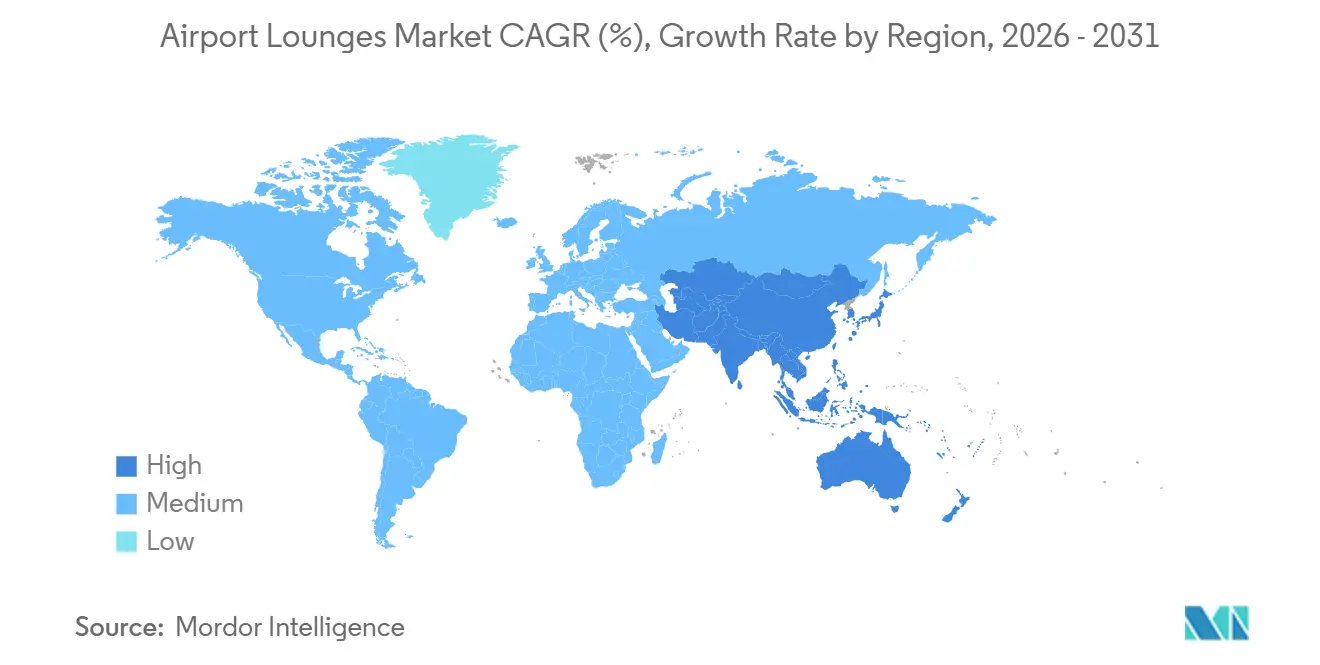

Asia-Pacific accounted for 31.14% of the market share in 2025 and is projected to grow at a CAGR of 7.26% through 2031, driven by infrastructure upgrades, rising affluence, and intra-regional travel, which are expected to sustain demand in the airport lounges market. Lounge visits across Asia-Pacific increased by 18% year-on-year between January and November 2025, with India, China, Thailand, Japan, and Singapore as top destinations, and Indian travelers accounting for a large share of regional traffic. Operators are enlarging footprints in key hubs such as Hong Kong, where a second premium lounge opened in Terminal 1 West Hall to meet rising demand. As airports add non-lounge experiences like dining and spa options under aggregator programs, capacity can flex with peak schedules, improving coverage without requiring large new builds in the airport lounges market.

North America benefits from deep loyalty ecosystems and a wide installed base of carrier and independent lounges that anchor premium travel flows in the airport lounges market. Airlines have continued to invest in large-format clubs and top-tier concepts at major hubs, including new facilities at Salt Lake City and expanded or refreshed spaces at other high-traffic locations. Access policies are being tuned to improve guest experience and manage peak-time crowding, reinforcing the value proposition for top-status and premium-fare customers. Secondary hubs are closing gaps through common-use lounges added within terminal modernization programs, making premium amenities a standard part of the journey in more cities across the airport lounges market.

Europe, the Middle East, and Africa show substantial investment in premium hospitality as well as heightened focus on privacy and sustainability standards that shape lounge design and operations in the airport lounges market. European passengers report stronger privacy concerns about biometric systems, which is driving the need for explicit consent and data policies as part of lounge access processes. In the Middle East and Turkey, airports and partners are adding premium and domestic lounges, including elevated concepts in Istanbul that reflect growing traffic and rising expectations for service depth. Regionally, authorities and operators are positioning premium hospitality as part of broader tourism and transit strategies, sustaining a pipeline of openings across the market's top hubs. In South America, aggregator growth and selective airport upgrades are improving coverage in Tier I and II cities, aligning network expansion with evolving demand patterns in the airport lounges market.

Market Concentration

The airport lounges market is moderately fragmented, comprising large airline-operated networks, independent operators, and aggregators, all of which are enhancing their positions through targeted investments and policy adjustments. Carriers are upgrading spaces and adding new lounges at large hubs to match premium-cabin growth, reinforcing brand loyalty through consistent ground experiences. Access is being calibrated to improve reliability during peaks, as seen in tightened rules that prioritize top-tier members and high-fare customers. Independent operators and airport landlords are also advancing common-use lounges to fill service gaps, a trend supported by modernization programs across secondary airports in the airport lounges market.

Aggregators and access networks continue to expand coverage and add non-lounge experiences to meet volume demands and spread guest loads in the airport lounges market. Priority Pass offers broad access across regions, while renewed agreements with major operators have added capacity and choice in key airports. At the same time, premium-first concepts in growth markets, including new facilities planned and opened in Turkey and Asia, indicate that independent providers are moving upmarket with curated F&B and elevated design. This interplay between airline control, aggregator coverage, and airport landlord initiatives creates a multi-format competitive field that adapts to both premium and mass-access needs in the airport lounges market.

Product and sustainability differentiation are now central to competitive strategy, with culinary partnerships and verifiable green design prominently featured in new and refreshed airport lounges. Chef-led programs in premium lounges elevate the experience and tell brand stories that support customer acquisition and retention. LEED-certified buildings and waste-reduction programs show that ESG outcomes can align with guest satisfaction and operational efficiency. As capacity management and throughput become key points of difference, operators are using digital tools to manage demand and deliver consistent service without continuous footprint growth in the airport lounges market.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

The airport lounges market encompasses the global commercial ecosystem of airport lounge facilities, including those operated by airlines, airport authorities or governments, and independent entities. The market covers offerings such as food and beverages, connectivity, entertainment, and passenger services across both economy-class and premium-class lounge categories. It accounts for capital and operational revenues from lounge operations, as well as demand influenced by passenger traffic, rising disposable incomes, and growing preferences for comfort and convenience in air travel.

The airport lounges market is segmented by service type, lounge ownership, lounge class, and geography. By service type, the market is segmented into food and beverages, connectivity and entertainment, and passenger services. By lounge ownership, the market is segmented into airline, airport, and government-operated, and privately owned. By lounge class, the market is segmented into economy lounge and premium lounge. The report also covers the market sizes and forecasts for the airport lounges market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

Feasibility Analysis for FBO Services in East Africa

3 Min Read

Unlocking Saudi Arabia’s Regional Tourism Growth Potential

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.